Site Search

582 results for go online now PROBLEMGO.COM pay judge to drop case

-

Cloud DX, Signs Contract with Heart Centre

Our partner, Cloud DX, has signed a 3-year contract with an Ontario hospital to help put patients with congestive heart failure at ease.

Cloud DX’s digital health platform works to improve healthcare delivery, provide better care outcomes, and lessen the burden on our national healthcare system. Now, an Ontario heart centre will use the Cloud DX platform to improve its patient monitoring services.

Cloud DX is a value-added service for Equitable Life’s Critical Illness claimants. Cloud DX delivers clinical grade hardware directly to the client so that they can remotely monitor the client’s vitals to help ensure they stay on the road to recovery*.

To learn more about our partnership with CloudDX, click here or contact your local wholesaler.

Watch our video on YouTube or Vimeo!

*Cloud DX is a non-contractual benefit and may be withdrawn or changed by Equitable Life® at any time. To be eligible for the Cloud DX offering, a claimant must be age 12 or older and have received payment on or after February 12, 2022 for a covered critical condition benefit under an individual critical illness insurance policy issued by Equitable Life. An early detection benefit payment does not qualify. Equitable Life pays for 6 months of Cloud DX subscription fees. If the claimant wishes to continue the Cloud DX service after 6 months, they will be responsible for the cost. The claimant must supply their own device to connect to Cloud DX app– a laptop, tablet or cellphone. As well, the claimant needs to supply their own data or internet service.

® and TM denote trademarks of The Equitable Life Insurance Company of Canada. -

Making it easier to claim for Loss of Independent Existence for EquiLiving Critical Illness insuranc

We have recently changed the definition of Loss of Independent Existence (LOIE). As a result, the Critical Illness claim criteria has also changed. Before, EquiLiving® Critical Illness insurance coverage was issued with a definition of LOIE that required clients to have the total inability to do 3 of 6 Activities of Daily Living (ADLs). Now, clients will only need to give us proof of the total inability to do 2 of 6 Activities of Daily Living (ADLs) to submit a claim for LOIE.

This change makes it easier for clients to claim for this covered critical illness. This change is retroactive to February 2022.

Clients will be sent a notice from us with a personalized endorsement from Equitable Life. This applies to their policy and forms part of their contract. We will approve claims for LOIE as outlined in the endorsement.

LOIE is one of the 26 conditions named as a covered critical illness in an EquiLiving policy or Critical Illness insurance rider on an Equitable Life insurance policy. With a loss of independent existence, some activities of daily living can no longer be done on one’s own. This can happen because of a disease or an injury.

Want to learn more? See the marketing piece: Understanding the Covered Conditions (1248).

For more information, reach out to your local wholesaler.

® denotes a trademark of The Equitable Life Insurance Company of Canada. -

How to talk to clients about CI when they don’t want to

Does this sound familiar?

You’re having a chat with your client about Critical Illness insurance. They suddenly interject: “Critical illness insurance isn’t for me.”

“Why is that?” you ask.

“Because….

- Critical Illness insurance is expensive!

- I don’t understand what it covers exactly.

- I have money to cover me if I get sick, so I don’t need this.

- I’m healthy enough.

- It’s not life insurance, so I don’t need it right now.

- I already have disability coverage through my work.”

If you’ve heard any of these responses, and didn’t know how to respond, we can help.

Our Path to Success program covers all these objections and more with simple-to-follow PDFs and videos. You’ll learn conversation strategies and tips on how to navigate the sale. Most importantly, you’ll know exactly what to say the next time a client objects to Critical Illness insurance.

Want to learn more? Check out our CI Path to Success modules here!

Need CE credits? Take our Path to Success program here. -

Flexibility for a client’s ever-changing life

Term life insurance offers full and partial conversion options to meet changing needs

Life is always changing—whether a client is buying their first home, welcoming a new baby, or sending the kids off to college. While most clients think of term life insurance as a solution to meet a temporary need, they don’t necessarily consider the power of term conversion options to meet their future needs.

Full and partial conversion options can help meet a client’s needs as their life journey and insurance needs change, without having to provide proof of continued good health.

Full conversion:

• With full conversion, clients can convert all of their term coverage from their policy or rider to permanent life insurance. This allows the client to lock in a level premium rate for life.

Partial conversion:

• With a partial conversion, clients can convert a portion of their term coverage from their policy or rider to a permanent plan. This allows them to help cover off both a short-term need and also provides lifetime protection.

Did you know?

Our partial conversion with a term rider carryover is now more flexible than ever. Read more about it here!

For more information, please consult the Equitable Term Life insurance admin guide. -

Savings & Retirement Policy and Procedure updates regarding Electronic Signatures

We have updated our policies and procedures regarding electronic signatures in the Savings and Retirement department. We are now able to accept electronically signed documents, from all major third-party signing vendors.

Including esign@equitable.ca as a non-signing reviewer is the preferred method as it ensures the security embedded documents are accurately and immediately available for Equitable. We will be automatically notified when signing is complete and will download eSigned forms immediately for processing. Including esign@equitable.ca as a non-signing reviewer is secure, quick, and efficient. Documents no longer need to be emailed to us – eSigned documents are sent directly to us once all signatures are completed, therefore you do not need to notify us once the documents are signed.

When esign@equitable.ca is not used to submit electronically signed documents, the following criteria are required:- The original signed form and audit trail with all the security features intact

- The email address used to sign must match what is in our files (as provided on the application, for electronic policy delivery or through previous communication). If an email address has changed, or we don’t have an email contact for the signer, we will follow up for confirmation.

A guide on how to use esign@equitable.ca can be found here.

Please note that Equitable does not accept digital signatures (images or fonts of a signature which are not stamped).

Date posted: June 13, 2024 -

New! Evidence of Insurability Schedule

We are pleased to announce Equitable’s new Evidence of Insurability Schedule. The new schedule applies to all life and critical illness insurance applications signed on or after October 5, 2024.

Here are the benefits to you:

● New chart is easier to read with more clarity and transparency.

● ECG and TST are no longer routinely required for Life applicants.

● Blood and urine requirement is streamlined for Life applicants.

● Detailed underwriting requirements for higher coverage amounts and mature applicants.

Please refer to the new Evidence of Insurability schedule (Form #1343) for full details.

Equitable® has the right to ask for more evidence of insurability. We will do this if we feel it is needed to assess the risk.

Key changes – Age and amount requirements

Life applicants:

● Resting ECG: No longer a routine age and amount requirement. This may still be requested at our underwriter’s discretion.

● Treadmill ECG: No longer required at any age or amount.

● Standalone Urine: Standalone urine changed to blood and urine at $100,001 and $500,000 coverage amounts for clients over age 55.

● Mature Age Focus Interview (MAFI): New for clients aged 75+. As part of the paramedical, we will assess the applicant’s Activities of Daily Living, social activities, and word recall ability.

Life and Critical Illness applicants:

● For clients aged 70+, evidence is now valid (recent) if completed within the past 6 months. For all other applicants (ages 18-69), there is no change – evidence is valid if completed within the past 12 months.

Financial/Third-party verification

Reminder – this is required for life insurance amounts over $5M. Our underwriting team will be pleased to assist you with this step.

Questions? Please contact your Equitable wholesaler or reach out to our underwriting team.

® or TM denotes a trademark of the Equitable Life Insurance Company of Canada. - [pdf] Poster - What did you wish for this year?

-

Secure your GIA with Equitable today!

In uncertain times, a Guaranteed Interest Account (GIA) is a safe and stable investment opportunity. Now is a great time to consider a GIA with Equitable®.

Equitable offers:

• market leading interest rates1, with higher rates for larger deposits;

• many account types, including the First Home Savings Account; and

• options to invest up to age 952.

“GIAs offer a number of benefits for investors, especially in times of market volatility.” said Cam Crosbie, Executive Vice President, Savings & Retirement. Equitable. “In uncertain times, let your investments be certain. Choose GIAs for guaranteed peace of mind and predictable returns, along with estate planning benefits, and potential creditor protection.”

GIAs are simple fixed-income investments that add value to a portfolio. Equitable GIAs provide competitive interest rates and protection from market volatility. For more information visit EquiNet® and don’t forget to register for our interest rate change alert email.

For more information or assistance, please contact your Director, Investment Sales.

1 Equitable has made every effort to ensure accuracy of competitive information. Accuracy is not guaranteed.

2 Some available term lengths may be limited starting at age 90.

Date posted: May 14, 2025 -

New secure encryption process for outstanding Equitable S&R business requirements

The Equitable® Savings and Retirement Operations team is improving how they send secure email messages to advisors. These emails are sent when there are outstanding requirements for an application or missing information for requests.

Previously, advisors had to manually password protect or unlock PDF documents. This caused delays and difficulties for recipients. The new encryption process will remove that confusion and make it easier for advisors to send and receive secure, encrypted messages.

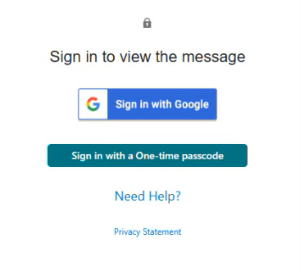

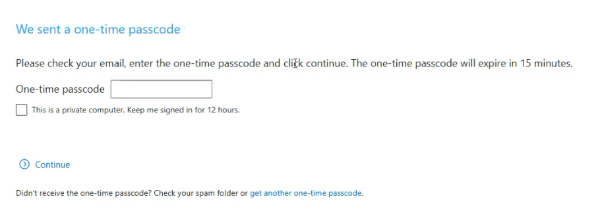

Advisors will now receive secure, encrypted emails from the QA annuity operations mailbox. These emails will use an encrypt option to protect personal client information, such as attachments or requests for personal documents. Recipients will get an email with a subject line saying they have a secure private message. They will need to sign in to view the message or choose to get a one-time passcode (OTP).

Please ensure to check the SPAM folder for the OTP option as it will expire in 15 minutes. Enter the OTP in the secure message

portal.

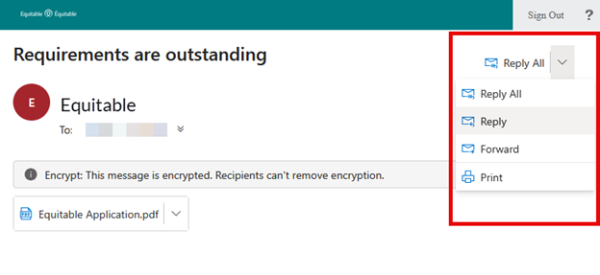

Emails are sent in both English and French, with automatic translation based on browser settings. Recipients must click the view button to access the message in the secure web portal where they can see the encrypted attachment.

Make sure to click Reply in the top right corner of the encrypted message to keep communications within the secure portal.

For more information or assistance, please contact your Director, Investment Sales.

Date posted: May 22, 2025 -

The top individual insurance marketing materials!

In 2025 there were five marketing pieces that advisors turned to most. If you haven’t seen them yet, now’s your chance to catch up. We want to help you connect with clients. These materials help make important topics easy to explain.

Top five individual insurance marketing materials:

1. 1024 Guide to individual underwriting. This guide shows how medical and non-medical conditions can affect insurance approvals.

2. 1038 Understanding participating whole life. Explains Equimax® participating whole life insurance. It also discusses the Participating Account, how dividends are calculated, and how they can impact a policy.

3. 1343 Evidence of insurability. Includes a chart showing the underwriting rules for life insurance products.

4. 1530 Temporary resident underwriting guidelines. This is a list of the documents temporary residents need when applying for individual insurance.

5. 1505 Dividend scale interest rate 30-year historical performance. This chart shows Equitable’s dividend scale interest rate history. It also compares our dividend scale rate to other major economic indicators.

For a list of all our marketing pieces visit our marketing materials page on EquiNet.

Have further questions? Your Equitable Wholesaler is here to help!