Site Search

771 results for click to access MAKEMUR.com how to get goods out of customs without waiting pay

-

Important Information Regarding FHSA Contributions

Many clients have already taken advantage of Equitable’s First Home Savings Account (FHSA), available on Pivotal Select™ Investment Class (75/75) and Pivotal Select Estate Class (75/100).

Below, we answer questions we have received regarding cut-off dates for 2023 FHSA contribution tax receipts.

1. The client submitted an application with a deposit before 11:59 p.m. ET on December 29, 2023. Will they get a 2023 FHSA contribution tax receipt?

Yes, the client will receive a 2023 FHSA contribution tax receipt.

2. The client submitted an application with a deposit on December 30 or 31, 2023. Will they get a 2023 FHSA contribution tax receipt?

No, the client will not receive a 2023 FHSA contribution receipt. The client’s deposit will be made effective the next business day, January 2, 2024. The client will receive a FHSA contribution tax receipt for the 2024 tax year.

However, since the client signed the application on or before December 31, 2023, they are eligible to take advantage of the 2023 contribution room in 2024 (up to $16,000 total*).

3. The client submitted an application with a deposit after January 1, 2024, but it was signed on or before December 31, 2023. Will they be eligible for the 2023 contribution room?

Yes. Any FHSA application received on or before 4:00 p.m. ET on January 12, 2024 that was signed on or before December 31, 2023 will be eligible to take advantage of the 2023 contribution room in 2024*.

4. The client received a confirmation letter stating their deposit was effective in January, but the application and contribution was submitted on or before December 29, 2023, will they receive a 2023 tax receipt for their contribution?

Yes, if the client received a confirmation letter stating their deposit was effective in January but the application and deposit was received at Equitable® on or before December 29, 2023, they will receive a 2023 tax receipt for their contribution. We are currently updating any impacted FHSA policies to reflect a December trade date. The client will receive a revised confirmation letter reflecting the December trade date.

5. When will 2023 FHSA contribution tax receipts be issued?

FHSA contribution receipts for the 2023 tax year will be mailed to clients by February 29, 2024.

If you have further questions, please contact your Regional Investment Sales Manager or one of our Client Services Representatives at 1.866.884.7427.

*Clients must consider all eligible FHSAs with any other institutions to determine their remaining contribution room.

® or ™ denotes a trademark of The Equitable Life Insurance Company of Canada.

Posted January 2, 2024 -

Turn ‘time in the market’ into client momentum

If clients are saving for a first home, contribution frequency matters. A simple compounding lesson helps them understand why bi‑weekly FHSA deposits can build balances faster than monthly contributions and gives you a natural bridge to Equitable’s Grow Your Way Home contest this summer.

Reinforce that bi‑weekly vs. monthly is about time in the market and consistent behaviour, not market timing. Here are a few talking points to reinforce with clients:-

“Earlier dollars work longer.”

Bi‑weekly contributions get part of the money invested sooner than a month‑end deposit, giving those dollars more days in the market. -

“More deposits create more compounding moments.”

Each deposit can begin earning right away and those earnings can earn too. More frequent contributions increase opportunities for that “interest on interest” effect. -

“Make it effortless.”

Align contributions to clients’ paydays. Automating bi‑weekly deposits helps build habit, removes friction and keeps clients steadily moving toward their first home savings goals.

As you continue FHSA conversations this summer, remind clients that contributing more frequently can get their money working sooner. And from May 1 to August 31, 2026, opening an Equitable FHSA account, contributing to their Equitable FHSA, or setting up recurring deposits to their Equitable FHSA earns automatic entries in Equitable’s Grow Your Way Home contest.

Use EZcomplete® and EZtransact® to keep contributions seamless and connect with your Director, Investment Sales for additional support, tools and ideas to help you continue these conversations throughout the summer.

® and ™ denote trademarks of The Equitable Life Insurance Company of Canada.

Equitable’s Grow Your Way Home contest: No purchase necessary. Contest period is May 1, 2026 to August 31, 2026. Enter by: opening an Equitable FHSA during the Contest Period; making a deposit to your Equitable FHSA during the Contest Period; or submitting a no-purchase entry. Two prizes of $8,000 each to be drawn on September 21, 2026 will be awarded to clients. The servicing advisor for the contract to which the selected entrant made the deposit is also an eligible winner and will receive a $1,000 prize. Open to legal residents of Canada of the age of majority. Odds of winning depend on number of eligible entries received during the Contest Period. For full contest rules, including no-purchase method of entry, see the full contest rules

-

- Continuing Education

-

New segregated fund sales charge option from Equitable Life of Canada

On December 7, 2020 Equitable Life® will add a new No Load CB5 (NL-CB5) sales option with a 60-month chargeback schedule to the Pivotal Select™ segregated funds lineup. This new sales charge option complements the recently launched No Load CB (NL-CB) option which has a 36-month chargeback schedule.

This new sales option for Pivotal Select gives you and your clients five sales charge options to choose from: Low Load (LL), No Load (NL), No Load CB (NL-CB), No Load CB5 (NL-CB5) and Deferred Sales Charge (DSC). The addition of NL-CB5 provides an option for those advisors who want to increase the upfront portion of their commission. The benefit to clients is no Deferred Sales Charge to contend with. If your client chooses to withdraw funds within 5 years after purchase, there is a chargeback of commission to you.

By offering five sales charge options, the choice between three distinct guarantee classes (Investment Class (75/75), Estate Class (75/100) and Protection Class (100/100)), and a diverse selection of investment funds, the Pivotal Select contract provides the flexibility to build an investment solution that meets the needs of your clients.

Need to meet with your client online? Our EZcomplete® application makes it easy to process your non-face-to-face applications and do business with Equitable Life. EZcomplete gives you the option to conduct your non face-to-face business easily and quickly, enabling your clients to provide their signature remotely on their own device.

For more information about Equitable’s NL-CB5 or any of Equitable’s products, contact your local Regional Investment Sales Manager or our Advisor Services team at 1.866.881.7427 Monday to Friday 8:30 a.m. – 7:30 p.m. ET or email savingsretirement@equitable.ca.

To learn more, click here.

-

Equitable Life added the Mackenzie Global Strategic Income Fund to Pivotal Select

On June 7, 2021, Equitable Life® launched five additional funds to the Pivotal Select™ segregated funds lineup. Included in the launch is the Mackenzie Global Strategic Income Fund. Designed to deliver growth and income to investors, the underlying fund objective seeks income with the potential for long-term capital growth by investing primarily in fixed-income and/or income-oriented equity securities of issuers anywhere in the world.

At Equitable Life, we pride ourselves on offering quality products. This means always reviewing our investment fund lineup. This fund, along with the other new funds are available on all Pivotal Select load types and guarantee classes, providing you and your clients with even more choice and flexibility.

To learn more about Mackenzie Global Strategic Income Fund, join us on Tuesday, June 22 at 2:00 p.m. ET/11:00 a.m. PT to hear Eric Glover, AVP Investment Director and Hadiza Djataou, VP Investment Director, from Mackenzie Investments, highlight the balanced solution that this fund can bring to your client’s investment portfolio.

Click here to register!

Want to learn more about our new funds? Contact your Regional Investment Sales Manager today.

® and ™ denotes a registered trademark of The Equitable Life Insurance Company of Canada.

-

Cloud DX, Signs Contract with Heart Centre

Our partner, Cloud DX, has signed a 3-year contract with an Ontario hospital to help put patients with congestive heart failure at ease.

Cloud DX’s digital health platform works to improve healthcare delivery, provide better care outcomes, and lessen the burden on our national healthcare system. Now, an Ontario heart centre will use the Cloud DX platform to improve its patient monitoring services.

Cloud DX is a value-added service for Equitable Life’s Critical Illness claimants. Cloud DX delivers clinical grade hardware directly to the client so that they can remotely monitor the client’s vitals to help ensure they stay on the road to recovery*.

To learn more about our partnership with CloudDX, click here or contact your local wholesaler.

Watch our video on YouTube or Vimeo!

*Cloud DX is a non-contractual benefit and may be withdrawn or changed by Equitable Life® at any time. To be eligible for the Cloud DX offering, a claimant must be age 12 or older and have received payment on or after February 12, 2022 for a covered critical condition benefit under an individual critical illness insurance policy issued by Equitable Life. An early detection benefit payment does not qualify. Equitable Life pays for 6 months of Cloud DX subscription fees. If the claimant wishes to continue the Cloud DX service after 6 months, they will be responsible for the cost. The claimant must supply their own device to connect to Cloud DX app– a laptop, tablet or cellphone. As well, the claimant needs to supply their own data or internet service.

® and TM denote trademarks of The Equitable Life Insurance Company of Canada. -

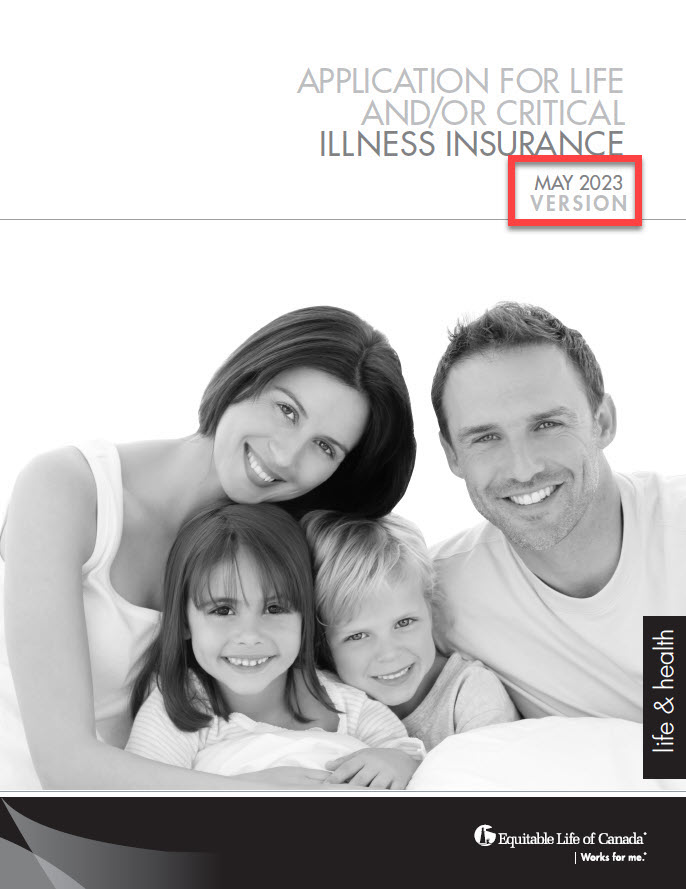

New 350 Life and CI Applications

On August 2nd, 2023, Equitable Life® will be updating the privacy and legal sections on some forms. This includes the form 350 Paper Application for Life and/or Critical Illness Insurance. This change will also be applied on our websites and our online application EZComplete®. These changes are part of Bill 64. The Bill is about the protection of personal and private information in Quebec. This will take effect on September 1st, 2023.

Due to this change, we ask all advisors to use the latest version dated May 2023 of the paper application after August 2nd. Applications in Quebec must use the lastest version from September 1, 2023 onwards.

For all regions outside Quebec, we will support a transition period from ‘old’ to ‘new’ applications until December 31st, 2023. After this date, we will no longer accept older versions of our Life and Critical Illness application.

To make sure you are using the latest version of the application, check the date on the title page. It should say May 2023. See the image below:

.jpg?width=200&height=259 "Form-350-Image-EN-(1).jpg")

To order paper copies, click here.

Email completed applications to supply@equitable.ca.

To learn more about Bill 64, please visit Assemblee nationale du Quebec - Bill 64. You may also contact your wholesaler.

® denote a registered trademark of The Equitable Life Insurance Company of Canada. -

Advisor Code of Conduct - Updated!

Our Advisor Code of Conduct sets out Equitable Life's expectations of advisors in dealing with clients and other stakeholders. The Code of Conduct forms part of your contractual relationship with us.

We have updated our Code to clarify specific expectations to help you meet regulatory compliance requirements, support your needs-based sales, and treat customers fairly.

Please review our updated Advisor Code of Conduct. - Individual Insurance Marketing Materials

-

Let’s “Talk Money”: From first savings to retirement income

Financial Literacy Month may be ending, but the conversation shouldn’t.

Talking with an advisor helps normalize money conversations— including discussions on saving, spending, managing debt, and more. This can help clients feel better and make smarter financial choices. As an advisor, you can guide clients from their first savings through to retirement with Equitable® .

Starting out? Clients can consider:

Tax-Free Savings Account (TFSA)

Save for short- or long-term goals and take out money anytime, tax-free.

First Home Savings Account (FHSA)

Save up to $40,000 tax-free for a first home. Contributions may be tax-deductible, and withdrawals are tax-free for buying a qualifying home.

Growing wealth? Clients can consider:

Registered Retirement Savings Plan (RRSP)

Contributions may be tax-deductible. Good for long-term savings—money grows tax-free until retirement.

Guaranteed Interest Account (GIA) / Daily Interest Account (DIA)

Earn steady interest with flexible terms. Available in a TFSA, RRSP, and FHSA.

Retirement ready? Clients can consider:

Payout annuities

Guaranteed income for life or a set time. Helps make sure savings last.

Resources to support these conversations

Use our easy online tools: EZcomplete® to apply and EZtransact™ for transactions. Let’s help Canadians save smarter—one step at a time. When we work together, success is mutual.

Reach out to your Director, Investment Sales if you have questions.