Site Search

495 results for PROBLEMGO.com How to pay off a parole officer for early termination HMP Wandsworth

-

Equitable Life Group Benefits Bulletin – March 2022

In this issue:

- CLHIA launches industry anti-fraud initiative*

- Provincial biosimilar update*

- Quebec decreasing insurance premium tax*

- Coming soon: A survey to understand how we can better serve your clients’ needs*

- Remind your clients’ plan members in BC, Manitoba and Saskatchewan to register for Pharmacare *

CLHIA launches industry anti-fraud initiative*

In February, the Canadian Life and Health Insurance Association (CLHIA) announced a new anti-fraud initiative that is using advanced artificial intelligence (AI) to further identify and reduce benefits fraud.

Equitable Life is excited to be a part of this important initiative. It will enhance our own fraud detection analytics by using AI to connect the dots across a huge pool of anonymized claims data. This will lead to more investigations and actions to mitigate the impact of fraud on your clients’ plans.

The initiative is being led by the CLHIA and member insurers and is supported by technology provider Shift Technologies. It will be further rolled-out and expanded over the next three years.

Benefits fraud affects more than just insurers. The costs of fraud are felt by employers and their employees as well. We are looking forward to being able to better identify and reduce benefits fraud.

Provincial biosimilar update*

BC expands its biosimilar initiative

BC Pharmacare recently announced it is adding two rapid-acting insulins to the list of drugs included in its ongoing initiative to switch patients to biosimilar versions of high-cost biologics. Patients taking Humalog or NovoRapid for Type 1 or Type 2 diabetes will be required to switch to a biosimilar version of the drugs by May 29, 2022 to maintain coverage under the public plan.

Biologics are drugs that are engineered using living organisms like yeast and bacteria. The first version of a biologic developed is also known as the “originator” biologic. Biosimilars are also biologics. They are highly similar to the originator biologic drugs they are based on, and Health Canada considers them to be equally safe and effective for approved conditions.

How we are responding to protect our clients

To help prevent this change from resulting in additional costs for our clients’ drug plans while still providing plan members with access to safe and effective medications, we will no longer cover Humalog or NovoRapid for plan members in BC. Effective June 1, 2022, claimants currently taking Humalog or NovoRapid will be required to switch to a biosimilar version of the drugs to maintain coverage under their Equitable Life plan and their BC Pharmacare plan.

We will be communicating this change to plan administrators later this week. And we will be communicating with affected claimants in early April to allow ample time to change their prescription and avoid any interruptions in their treatment or their coverage.

If you have any questions about this change, please contact your Group Account Executive or myFlex Sales Manager.

Nova Scotia and Northwest Territories introduce biosimilar initiatives

The governments of Nova Scotia and the Northwest Territories each recently announced they are launching biosimilar initiatives to switch patients from certain originator biologic drugs to biosimilar versions of the drugs.

Patients in Nova Scotia using affected originator biologic drugs will have until February 2023 to switch to a biosimilar version of their medications in order to maintain coverage under the province’s public drug plans. Patients in the Northwest Territories will have until June 20, 2022, to switch.

Equitable Life® actively monitors and investigates all biosimilar policy changes and the ongoing evolution of biosimilar drugs entering Canada. We will keep you informed of any impact on private drug plans and how we are responding.

Quebec decreasing insurance premium tax*

The Quebec Government has announced that it plans to decrease its Insurance Premium Tax rates effective April 1, 2022. The premium tax rates for group life and accident and sickness insurance are expected to decrease from 3.48% to 3.3%. The new tax rates will be applied to premiums for the billing period beginning on or after April 1, 2022.

Coming soon: A survey to understand how we can better serve your clients’ needs*

We are committed to providing your clients and their plan members with industry-leading service. We’ve introduced several enhancements over the past year to make it easier to do business with us. And we’re continually looking for ways to improve.

In the coming weeks, we will conduct a survey of your clients to help us understand how we can better serve them. On March 28, we will send plan administrators an email with a link to the survey. The survey will remain open until the end of the day on April 11 and will take between five and 10 minutes to complete. Please encourage your clients to participate. Their feedback will be confidential, and their responses will help us improve our service and ensure we’re meeting their expectations. We may also follow up with plan administrators directly to address any concerns they’ve identified.

We know your clients’ time is valuable. So, each plan administrator who completes the survey will be entered into a random draw for a chance to win one of 25 prepaid gift cards for $25.

Remind your clients’ plan members in BC, Manitoba and Saskatchewan to register for Pharmacare*

If your clients have plan members in British Columbia, Manitoba or Saskatchewan, the provincial government offers a Pharmacare program to support prescription drug costs. Plan members in these provinces must register for their provincial Pharmacare program to maintain coverage under their Equitable Life drug plan.

Registration is easy! We will send two registration reminder messages directly to plan members’ pharmacists and post them on their Explanation of Benefits. We’ve also created a step-by-step guide that your clients can share with their plan members.

English version

French version

For more information about the provincial Pharmacare programs, including how plan members can register, please visit:

For British Columbia residents: https://www2.gov.bc.ca/gov/content/health/health-drug-coverage/pharmacare-for-bc-residents

For Manitoba residents: https://www.gov.mb.ca/health/pharmacare/apply.html

For Saskatchewan residents: https://www.saskatchewan.ca/residents/health/prescription-drug-plans-and-health-coverage/extended-benefits-and%20drug-plan/drug-cost-assistance#eligibility

- Choosing the right funds

-

What’s your saving style?

A TFSA for its flexibility or an RRSP for tax-deferred growth.

Did you know? More than 65% of people who put money into a TFSA* earn less than $80,000 a year. That’s why TFSAs are popular with middle-income Canadians. They’re simple and flexible: you don’t get a tax break when you put money in, but you don’t pay tax when you take money out. This makes them great for people who don’t get big benefits from tax deductions.

On the other hand, 54% of RRSP contributors earn more than $80,000 per year*. RRSPs often work better for higher-income earners because contributions lower taxable income. That means bigger tax savings for people in higher tax brackets.

Here’s the good news: From January 1 to March 2, 2026, when clients open or add money to an Equitable TFSA or RRSP, they’ll be entered into Equitable’s Snowball Your Savings contest. Two winners will be chosen—and their advisors will celebrate too!

How to Enter

Advisors can help clients submit contributions through EZcomplete® or process transactions using EZtransact®. Every entry is a chance to win!

Want ideas to boost contributions and help Canadians save more? Connect with your Director, Investment Sales today.

* Source: advisor.ca/news/tfsas-more-popular-than-rrsps-in-2023/

® and ™ denote trademarks of The Equitable Life Insurance Company of Canada.

Equitable’s Snowball Your Savings contest: No purchase necessary. Contest period January 1, 2026 to March 2, 2026. Enter by making a deposit to an Equitable Tax-Free Savings Account or Registered Retirement Savings Plan during the contest period or by submitting a no-purchase entry. Two prizes of $5,000 CAD to be drawn on March 23, 2026 will be awarded. The servicing advisor for the contract to which the selected entrants made the deposit is also an eligible winner and will receive a $1,000 CAD prize. For example, if an Equitable client is a winner of the $5,000 prize, the client’s servicing advisor for the relevant contract wins a $1,000 prize. Open to legal residents of Canada of the age of majority. Odds of winning depend on number of eligible entries received during the Contest Period. For full contest rules, including no-purchase method of entry, see the full contest rules. -

Equitable Life Group Benefits Bulletin – December 2021

In this issue:

- Supporting plan members affected by the flooding in Nova Scotia and Newfoundland*

- Update: Changing certificate numbers on EquitableHealth.ca*

- Help plan members take advantage of convenient digital options*

- Ontario optometrists and government to restart negotiations*

- QDIPC updates terms and conditions for 2022*

Supporting plan members affected by the flooding in Nova Scotia and Newfoundland*

The recent flooding in Nova Scotia and Newfoundland is having a devastating impact on the province’s residents.

Here are some of the ways we can help support your clients’ plan members who are affected by the flooding.

Prescription refills

Until Dec. 31, our pharmacy benefit manager, TELUS Health, will allow early refills for plan members who have been evacuated and/or lost their medication due to the flooding.

Replacement of medical or dental equipment and appliances

If plan members in Nova Scotia or Newfoundland need to replace any eligible medical or dental equipment or appliances (e.g. prescription eyeglasses, dentures, etc.) due to the flooding, they can call us at 1.800.265.4556 before incurring additional expenses to see how we can support them.

Disability or other benfit cheques

If plan members affected by the flooding are receiving disability benefits or other benefit reimbursements by cheque, they can visit www.equitable.ca/go/digital for easy instructions on how to sign up for direct deposit. It’s easy and takes just a few minutes. They can call us at 1.800.265.4556 if they need help. We can also arrange for a different mailing address or replacement cheques if necessary.

Mental Health Support

A natural disaster can also take a serious toll on people’s mental health. All of our plan members have access to the Homeweb online portal and mobile app, including numerous articles, tools and resources designed to provide guidance and support in difficult times. Homewood has put together some suggestions on how to help employees affected by a natural disaster.

For your clients with an Employee and Family Assistance Program, remind them that their plan members have 24/7 access to confidential counselling through a national network of mental health professionals. Whether it’s face-to-face, by phone, email, chat or video, plan members will receive the most appropriate, most timely support for the issue they’re dealing with.

If a client wishes to add the EFAP to their plan, we can do this quickly – often in just a few days. Simply contact your Group Account Executive or myFlex Sales Manager.

Plan Administrator support

We realize that the flooding may also be having an impact on the regular business operations of your clients in Nova Scotia and Newfoundland. If any of your clients are unable to carry out day-to-day plan administration, they can call us at 1.800.265.4556 to see how we can support them.

We know this is a challenging time for many of your clients and their plan members. We will continue to monitor the situation and provide additional updates as appropriate.

Update: Changing certificate numbers on EquitableHealth.ca*

Effective Dec. 10th, plan administrators will no longer be able to update or change plan members’ certificate numbers on EquitableHealth.ca. This change will ensure we can manage these changes more effectively to provide a smoother plan member experience.

If your clients need to update a plan member’s certificate number, please have them reach out to Group Benefits Administration for assistance at groupbenefitsadmin@equitable.ca.

Help plan members take advantage of convenient digital options*

We have several digital options available to make it easier for your clients to do business with us and for their plan members to access and use their benefits plan.

To help build awareness among plan members, we’ve created two posters that your clients can post on their intranet sites or in their office. The posters provide easy instructions on how to activate our secure, digital options.

Please click on the links below to download the posters.

EquitableHealth.ca posters: EZClaim mobile app posters:

EquitableHealth.ca English EZClaim mobile app English poster

EquitableHealth.ca French poster EZClaim mobile app French poster

Ontario optometrists and government to restart negotiations*

The Ontario Association of Optometrists (OAO) announced it has paused its job action and will restart negotiations with the Ontario Ministry of Health on funding for optometry services.

In September, Ontario optometrists began withholding services from patients covered by OHIP, including children, senior citizens and other patients with certain medical conditions, after negotiations with the Ministry of Health over compensation broke down.

Residents of Ontario between the ages of 20 to 64 who aren’t eligible for coverage of eye services under OHIP were not affected by the job action. They were able to continue to receive eye exams from their optometrist and submit eligible claims to their benefits plan.

QDIPC updates terms and conditions for 2022*

Every year, the Quebec Drug Insurance Pooling Corporation (QDIPC) reviews the terms and conditions for the high-cost pooling system in the province. Based on its latest review, QDIPC is revising its pooling levels and fees for 2022 to reflect trends in the volume of claims submitted to the pool, particularly catastrophic claims.

Size of group (# of certificates) Threshold per certificate 2022 Annual factor (without dependents Annual factor (with dependents) Fewer than 25 $8,000 $276.00 $771.00 25 – 49 $16,500 $188.00 $527.00 50 – 124 $32,500 $97.00 $328.00 125 – 249 $55,000 $66.00 $223.00 250 – 499 $80,000 $51.00 $173.00 500 – 999 $105,000 $39.00 $153.00 1,000 – 3,999 $130,000 $34.00 $133.00 4,000 – 5,999 $300,000 $18.00 $71.00 6,000 and over Free market – Groups not subject to Quebec Industry Pooling

We will apply the new pooling levels and fees to future renewal calculations that involve Quebec plan members. - [pdf] The Approach to Suitable Sales - Reference

-

Market Commentary July 2025

Key Takeaways

• Markets were very volatile in April to start Q2 but calmed as the quarter progressed. Volatility was driven mostly by headlines about tariffs, but other fiscal policy developments also had an impact.

• Equity markets sold off sharply at the start of the quarter, continuing Q1’s weakness. Markets rebounded sharply once worst-case fears over tariffs eased. The markets continued to rally through the quarter as trade negotiations progressed. Stronger-thanexpected corporate earnings also boosted markets. Despite the shaky start to the quarter, most global equity markets set new all-time highs in Q2.

• Canadian bond markets delivered slightly negative returns in Q2. Weak performance was driven by rising interest rates, which outweighed the impact of tighter credit spreads. Higher interest rates hurt the performance of longer-term bonds most.

• Both the Bank of Canada and the U.S. Federal Reserve adopted a wait-and-see approach. They each held rates steady during Q2, awaiting greater clarity on the impacts of tariffs on both growth and inflation before considering further cuts.

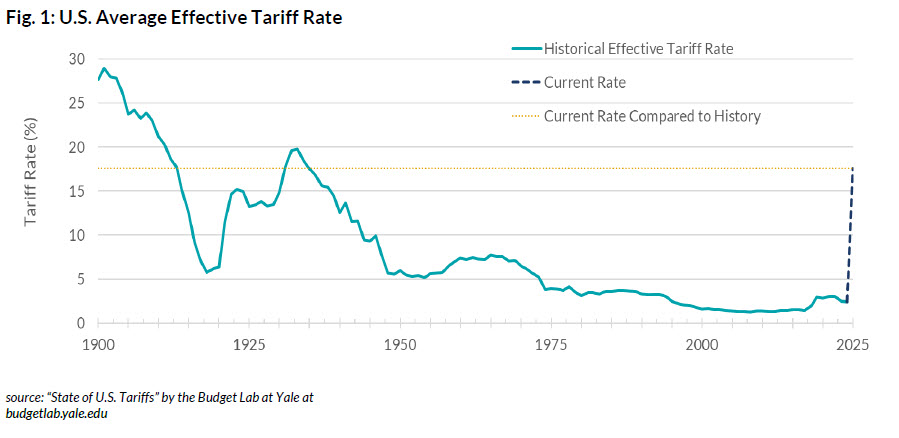

Economic and Market UpdateEconomic Summary: Most indicators of economic activity in the U.S. continued to expand at a decent pace. However, GDP data for the first quarter came in weaker than expected, as higher imports ahead of anticipated tariffs and weaker spending by consumers weighed on Q1 GDP. That said, GDP growth is expected to bounce back in Q2. Tariffs will likely continue to be an evolving story, with potential impacts on both economic growth and inflation. Those impacts will remain uncertain until trade agreements have been finalized.

In early April, President Trump announced larger-than-expected reciprocal tariffs, with the impact most notable on trade with China. However, progress followed with a 90-day pause in tariff implementation. The U.S. then reached trade agreements with the UK, China, and Vietnam. Negotiations with other major trade partners are ongoing. The conflict between Israel and Iran raised inflation concerns, due mostly to the possibility of higher oil prices. Those concerns eased following a ceasefire. Congress passed Trump’s tax cut and spending bill, raising concerns about its potential impact on the U.S. fiscal burden. Meanwhile, U.S. labour market conditions remain resilient, with the unemployment rate remaining low. Inflation has eased slightly but remains above the Federal Reserve’s target. Amid heightened uncertainty, the Federal Reserve held interest rates steady at 4.25%–4.50% at both of its meetings in Q2. Chair Jerome Powell stated that the Fed is “well positioned to wait for greater clarity before considering any adjustments to our policy stance.”

.jpg "Fig-One-(1).jpg")

In Canada, tariffs and trade-related uncertainty continue to weigh on the economy. A pullforward of exports and inventory accumulation ahead of tariffs helped keep first-quarter GDP firm, but growth is expected to slow in the second quarter. The labour market has weakened, particularly in trade-sensitive sectors. Inflation remains within the Bank of Canada’s 1–3% preferred range. However, core CPI remains above the Bank’s preferred 2% target. Canada’s fiscal deficit is expected to widen as Prime Minister Mark Carney aims to fast-track infrastructure development and increase defense spending. Amid ongoing trade uncertainty, the Bank of Canada held its policy rate at 2.75% during its April and June meetings. Governor Tiff Macklem signaled the Bank’s readiness to cut rates further if economic conditions deteriorate.

.jpg "Fig-Two-(1).jpg")

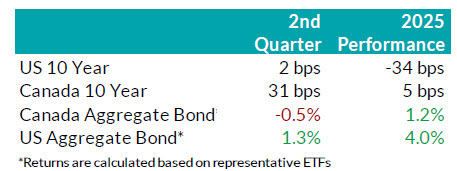

Bond Markets: During Q2, the FTSE Canada Universe Bond Index returned -0.6%. Yields for Canadian bonds rose across all maturities over the quarter. That reflected reduced expectations for rate cuts by the Bank of Canada and a higher risk premium on long-term debt. The impact of higher yields on government bonds was offset in part by tightening of credit spreads on provincial and corporate bonds. Overall corporate bonds saw a positive return for the quarter and outperformed government bonds, in part due to the strong recovery in credit spreads that started in late

April. While corporate issuance slowed considerably in April due to increased trade policy uncertainty, issuance in the Canadian bond markets during May and June were robust. There were 83 deals during Q2 that combined to raise $37 billion for issuers. June 2025 was the 3rd busiest month for issuance on record. We continue to expect higher credit spreads as the U.S. tariffs impact global growth. As such, we have maintained our conservative view with a bias towards shorter corporate bonds but remain ready to invest in longer corporate bonds as valuations become

attractive.

.jpg "Fig-Three-(1).jpg")

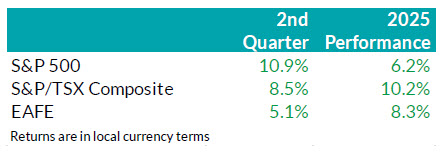

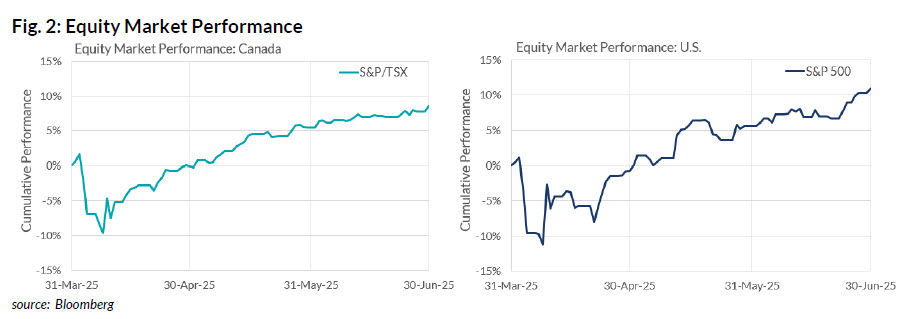

Stock Markets – Overview: Having done a round-trip following April tariff announcements, technology, consumer discretionary and industrial companies propelled the U.S. equity market to another record high. The S&P 500 ended the quarter up about 11%, outperforming Canadian and international markets. Canadian equities gained 8.5% in Q2, buoyed by front-loaded demand that benefited the Materials sector, while Financials recovered from a poor Q1. Meanwhile, as risk sentiment stabilized following the 90-day tariff pause and U.S. equities regained momentum, the appeal of the “Sell America” trade diminished. As a result, Europe, Australasia, and the Far East (EAFE) markets finished the quarter with a more modest gain of just over 5%, lagging the sharper

recovery seen in North America.

.jpg "Fig-Four-(1).jpg")

U.S. Equities: The U.S. equity market staged a V-shaped recovery on strong company earnings data in the second quarter. A stable job market and muted inflation reinforced the view of a resilient U.S. economy. At a company level, we observed positive corporate earnings surprises, steady profit margins and better-than-expected forward earnings guidance. Together they underpinned the equity market’s sharp reversal to the upside. Market breadth also improved over the quarter, with strength extending beyond Technology to include Industrials and Financials. That signalled that the market rally was supported by investors’ confidence in the U.S. economy. Furthermore, structural investment trends in artificial intelligence (AI) continued to accelerate, highlighted by rising enterprise capex in data centres. Beyond AI, Circle, a blockchain-based platform that supports stablecoin issuance, tokenized assets, and digital payment infrastructure, conducted a successful IPO. Its share price jumped 485% from its listing price as of quarter-end. On June 17, the U.S. Senate passed the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act, a regulatory framework for use of tokenized assets. While investors wait for the House’s decision, equity price actions suggest that the policy environment is increasingly supportive of blockchain innovation and digital efficiency.

Canadian Equities: Canadian equities posted solid gains in Q2, with Financials overtaking Materials to lead the market higher. Momentum from the Materials sector, which benefited from the pull-forward demand related to U.S. tariff uncertainty, faded toward quarter-end. Meanwhile, cooling inflation and muted domestic growth pushed investors towards highquality, high-dividend-paying companies. Notably, banks significantly outperformed the broader market, as investors favoured their stable corporate fundamentals. Energy surged briefly amid escalating geopolitical tensions, but those gains proved short-lived. In recap, investors in the Canadian market faced slowing resource demand and a stalling domestic economy, which fueled increased interest in high-quality, high-dividend-paying companies. That is a trend we expect to continue going forward.

Bottom line: Markets remain heavily influenced by sentiment, with U.S. policy developments and ongoing tariff negotiations continuing to cause periodic volatility. However, there is little

evidence of deterioration in the hard data to date. As such, we continue to anchor our positioning on underlying data rather than market narratives. Looking ahead, the combination of a structurally higher-for-longer interest rate environment and increasingly pro-growth policy backdrop presents selective opportunities. In the U.S., this favours highquality growth stocks, particularly within Technology, where strong balance sheets and long-term thematic tailwinds remain intact. In Canada, Financials, especially the relatively inexpensive banks, present a more compelling opportunity as earlier tailwinds from pullforward demand are beginning to wane. While we remain constructive, we are mindful of elevated equity valuations and continue to closely monitor macro conditions and policy developments for signs of inflection.

Downloadable Copy

Mark Warywoda, CFA

VP, Public InvestmentsIan Whiteside, CFA, MBA

AVP, Public InvestmentsJohanna Shaw, CFA

Director, Public InvestmentsJin Li

Director, Equity Investments

Wanyi Chen, CFA, FRM

Sr. Quantitative Analyst

Andrew Vermeer, CFA

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Edward Ng Cheng Hi

Analyst, Credit

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

-

Market Commentary July 2025

Key Takeaways

• Markets were very volatile in April to start Q2 but calmed as the quarter progressed. Volatility was driven mostly by headlines about tariffs, but other fiscal policy developments also had an impact.

• Equity markets sold off sharply at the start of the quarter, continuing Q1’s weakness. Markets rebounded sharply once worst-case fears over tariffs eased. The markets continued to rally through the quarter as trade negotiations progressed. Stronger-thanexpected corporate earnings also boosted markets. Despite the shaky start to the quarter, most global equity markets set new all-time highs in Q2.

• Canadian bond markets delivered slightly negative returns in Q2. Weak performance was driven by rising interest rates, which outweighed the impact of tighter credit spreads. Higher interest rates hurt the performance of longer-term bonds most.

• Both the Bank of Canada and the U.S. Federal Reserve adopted a wait-and-see approach. They each held rates steady during Q2, awaiting greater clarity on the impacts of tariffs on both growth and inflation before considering further cuts.

Economic and Market UpdateEconomic Summary: Most indicators of economic activity in the U.S. continued to expand at a decent pace. However, GDP data for the first quarter came in weaker than expected, as higher imports ahead of anticipated tariffs and weaker spending by consumers weighed on Q1 GDP. That said, GDP growth is expected to bounce back in Q2. Tariffs will likely continue to be an evolving story, with potential impacts on both economic growth and inflation. Those impacts will remain uncertain until trade agreements have been finalized.

In early April, President Trump announced larger-than-expected reciprocal tariffs, with the impact most notable on trade with China. However, progress followed with a 90-day pause in tariff implementation. The U.S. then reached trade agreements with the UK, China, and Vietnam. Negotiations with other major trade partners are ongoing. The conflict between Israel and Iran raised inflation concerns, due mostly to the possibility of higher oil prices. Those concerns eased following a ceasefire. Congress passed Trump’s tax cut and spending bill, raising concerns about its potential impact on the U.S. fiscal burden. Meanwhile, U.S. labour market conditions remain resilient, with the unemployment rate remaining low. Inflation has eased slightly but remains above the Federal Reserve’s target. Amid heightened uncertainty, the Federal Reserve held interest rates steady at 4.25%–4.50% at both of its meetings in Q2. Chair Jerome Powell stated that the Fed is “well positioned to wait for greater clarity before considering any adjustments to our policy stance.”

In Canada, tariffs and trade-related uncertainty continue to weigh on the economy. A pullforward of exports and inventory accumulation ahead of tariffs helped keep first-quarter GDP firm, but growth is expected to slow in the second quarter. The labour market has weakened, particularly in trade-sensitive sectors. Inflation remains within the Bank of Canada’s 1–3% preferred range. However, core CPI remains above the Bank’s preferred 2% target. Canada’s fiscal deficit is expected to widen as Prime Minister Mark Carney aims to fast-track infrastructure development and increase defense spending. Amid ongoing trade uncertainty, the Bank of Canada held its policy rate at 2.75% during its April and June meetings. Governor Tiff Macklem signaled the Bank’s readiness to cut rates further if economic conditions deteriorate.

Bond Markets: During Q2, the FTSE Canada Universe Bond Index returned -0.6%. Yields for Canadian bonds rose across all maturities over the quarter. That reflected reduced expectations for rate cuts by the Bank of Canada and a higher risk premium on long-term debt. The impact of higher yields on government bonds was offset in part by tightening of credit spreads on provincial and corporate bonds. Overall corporate bonds saw a positive return for the quarter and outperformed government bonds, in part due to the strong recovery in credit spreads that started in late

April. While corporate issuance slowed considerably in April due to increased trade policy uncertainty, issuance in the Canadian bond markets during May and June were robust. There were 83 deals during Q2 that combined to raise $37 billion for issuers. June 2025 was the 3rd busiest month for issuance on record. We continue to expect higher credit spreads as the U.S. tariffs impact global growth. As such, we have maintained our conservative view with a bias towards shorter corporate bonds but remain ready to invest in longer corporate bonds as valuations become

attractive.

Stock Markets – Overview: Having done a round-trip following April tariff announcements, technology, consumer discretionary and industrial companies propelled the U.S. equity market to another record high. The S&P 500 ended the quarter up about 11%, outperforming Canadian and international markets. Canadian equities gained 8.5% in Q2, buoyed by front-loaded demand that benefited the Materials sector, while Financials recovered from a poor Q1. Meanwhile, as risk sentiment stabilized following the 90-day tariff pause and U.S. equities regained momentum, the appeal of the “Sell America” trade diminished. As a result, Europe, Australasia, and the Far East (EAFE) markets finished the quarter with a more modest gain of just over 5%, lagging the sharper

recovery seen in North America.

U.S. Equities: The U.S. equity market staged a V-shaped recovery on strong company earnings data in the second quarter. A stable job market and muted inflation reinforced the view of a resilient U.S. economy. At a company level, we observed positive corporate earnings surprises, steady profit margins and better-than-expected forward earnings guidance. Together they underpinned the equity market’s sharp reversal to the upside. Market breadth also improved over the quarter, with strength extending beyond Technology to include Industrials and Financials. That signalled that the market rally was supported by investors’ confidence in the U.S. economy. Furthermore, structural investment trends in artificial intelligence (AI) continued to accelerate, highlighted by rising enterprise capex in data centres. Beyond AI, Circle, a blockchain-based platform that supports stablecoin issuance, tokenized assets, and digital payment infrastructure, conducted a successful IPO. Its share price jumped 485% from its listing price as of quarter-end. On June 17, the U.S. Senate passed the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act, a regulatory framework for use of tokenized assets. While investors wait for the House’s decision, equity price actions suggest that the policy environment is increasingly supportive of blockchain innovation and digital efficiency.

Canadian Equities: Canadian equities posted solid gains in Q2, with Financials overtaking Materials to lead the market higher. Momentum from the Materials sector, which benefited from the pull-forward demand related to U.S. tariff uncertainty, faded toward quarter-end. Meanwhile, cooling inflation and muted domestic growth pushed investors towards highquality, high-dividend-paying companies. Notably, banks significantly outperformed the broader market, as investors favoured their stable corporate fundamentals. Energy surged briefly amid escalating geopolitical tensions, but those gains proved short-lived. In recap, investors in the Canadian market faced slowing resource demand and a stalling domestic economy, which fueled increased interest in high-quality, high-dividend-paying companies. That is a trend we expect to continue going forward.

Bottom line: Markets remain heavily influenced by sentiment, with U.S. policy developments and ongoing tariff negotiations continuing to cause periodic volatility. However, there is little

evidence of deterioration in the hard data to date. As such, we continue to anchor our positioning on underlying data rather than market narratives. Looking ahead, the combination of a structurally higher-for-longer interest rate environment and increasingly pro-growth policy backdrop presents selective opportunities. In the U.S., this favours highquality growth stocks, particularly within Technology, where strong balance sheets and long-term thematic tailwinds remain intact. In Canada, Financials, especially the relatively inexpensive banks, present a more compelling opportunity as earlier tailwinds from pullforward demand are beginning to wane. While we remain constructive, we are mindful of elevated equity valuations and continue to closely monitor macro conditions and policy developments for signs of inflection.

Downloadable Copy

Mark Warywoda, CFA

VP, Public InvestmentsIan Whiteside, CFA, MBA

AVP, Public InvestmentsJohanna Shaw, CFA

Director, Public InvestmentsJin Li

Director, Equity Investments

Wanyi Chen, CFA, FRM

Sr. Quantitative Analyst

Andrew Vermeer, CFA

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Edward Ng Cheng Hi

Analyst, Credit

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

-

Tune in to our latest Equitable Insights Videos on EquiNet

Our new Equitable Insights Video Series page on EquiNet® hosts all of our latest videos in one convenient place, including:

● Our Large Case Experts, featuring Scott Morrow, Individual Insurance Sales Vice President, MGA East, Equitable Life

● EZcomplete Makes Submission to Commission Easy, featuring Chris Marrese, Individual Operations Vice-President, Equitable Life

● Our Investment Approach featuring David Irwin, Director, Portfolio Management and Client relations

● Our Financial Strength, featuring Sheila Hart, Chief Financial Officer, Equitable Life

Watch our Equitable Insights Video Series to learn more about Equitable Life and the solutions we offer to meet our customers’ needs. - [pdf] Advisors Edge Insurance for Children Article

- [pdf] G3NU-Application for Non-Underwriting Change