Site Search

495 results for PROBLEMGO.com How to pay off a parole officer for early termination HMP Wandsworth

- [pdf] New Forms to Comply with AML & CRS Changes

- [pdf] EquiNet Quick Tips

-

EAMG Market Commentary January 2024

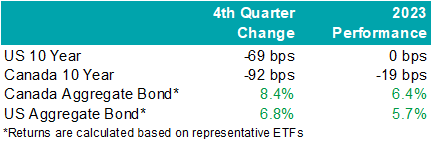

Rates & Credit – Interest rates decreased sharply in Q4 as the market priced in aggressive interest rate cuts by central banks in 2024. The prospect of lower interest rates also drove a strong risk-on tone to the market, with the risk premium on corporate bonds grinding tighter as prospects for a “soft landing” improved. The rally in interest rates resulted in the best quarter for bonds over the past 15 years, with the FTSE Canada Universe Index returning 8.3%. Corporate bonds modestly underperformed the Universe Index with a return of 7.3%. The lower return for corporate bonds was primarily driven by the fact that the corporate bond index is less sensitive to interest rate movements (as compared to the government index), partially offset by the risk-on tone to the market. Within corporate bonds, lower-rated BBBs outperformed higher-rated A bonds. Industries with higher interest rate exposure such as infrastructure, energy, and communications outperformed those with less exposure (notably financials and securitization), consistent with the overall shift in the yield curve.

.png "image1-(1).png")

Santa Came to Town – Moving in sync with bonds, global equities jolted higher into the end of the year with cooling inflation data and dovish comments from central bankers. The U.S. market outperformed most regions last quarter with the S&P 500 returning 11.7% in USD terms, bringing the total return in 2023 to 26.3%. The TSX added 8.1% in Q4, boosting the total annual return to 11.8%. Meanwhile, major developed economies from Europe, Australasia, and the Far East (EAFE) gained 5.0% in local currency terms over the quarter, helping the region produce a 16.8% return from the year prior. Prospects of interest rate cuts by the Federal Reserve saw the Loonie rally into year-end and resultantly, investors of Canadian dollar securities witnessed enhanced returns. Strong domestic U.S. economic data helped value pockets of the market outperform. That said, this was not a synchronized trend as China’s economic disappointment weighed on the performance of EAFE.

U.S. Fundamentals – Our work shows that investors are shifting their focus away from operating margins and towards the ability to sustain debt levels ahead of renewing debt obligations. Corporate earnings beat modest expectations last quarter, contracting by less-than-expected on a year-over-year basis. Resilient operating margins continue to attract investors into equities. After three consecutive quarters of improving forward earnings guidance, we observed that the number of major companies expecting deteriorating financial performance grew to ~35%. We note that this is a sharp contrast relative to the optimistic run-up in equity valuations. In general, corporate pessimism has been underpinned by concerns for the health of the consumer, increasing wage pressures, and inflation.

U.S. Quant Factors – While mega-cap technology stocks gave back some ground in the second half, crowding into the magnificent 7 remains noticeable with the cap weighted S&P 500 outperforming the equal weighted index by 12.5% last year. That said, value areas of the market – which underperformed through the first three quarters of the year – were top performing companies last quarter as the prospects for an economic “soft-landing” improved with U.S. inflation continuing to ease without substantial deteriorations of employment or output data. Quality-growth businesses initially outperformed as the higher-for-longer narrative continued to drive investors toward large cash-rich companies with stable margins. That said, this basket of companies gave back relative returns into quarter-end as weakness in operating margins persisted, making fundamentals appear stretched. Low volatility stocks (i.e. stocks with lower sensitivity to broad market movement and lower price volatility) rallied to start the quarter before dovish comments from central bankers improved risk-sentiment and ultimately pushed this basket lower on a relative basis. Lastly, dividend growth companies, which include businesses with a lengthy and established history of increasing dividends, underperformed the broader index as market participants punished businesses that slowed capital growth projects during the rising interest rate environment. While operating margins have declined, the basket’s strong cash flow and low debt burden may be advantageous if the market’s anticipation of impending interest rate cuts proves to be incorrect or mistimed.

Canadian Fundamentals – Although Canadian companies exceeded bleak forecasts last quarter, earnings continue to contract on a year-over-year basis. Return on equity (ROE) – a gauge of how efficiently a corporation generates profits – continued to decline last quarter while corporate costs of capital remain elevated. In essence, Canadian companies are generating less value relative to their financing cost. Value creation underpins the sustainability of dividend payments, which are a unique and desirable attribute of the Canadian market. Meanwhile, the Bank of Canada held its overnight interest rate unchanged with market participants forecasting a higher probability of interest rate cuts in 2024. On the expectations of easing monetary conditions, dividend yields compressed while earnings forecasts improved with analysts predicting that index aggregate earnings will grow 6% to 8% in 2024. At a sector level, the energy industry’s financial performance normalized – in line with expectations – as weakening oil demand expectations overshadowed geopolitical conflict in the Middle East, ultimately pushing crude prices ~21% lower last quarter. The industrials and financials sectors beat expectations, helping offset softer-than-expected results from the consumer staples and technology sectors.

Canadian Quant Factors – The Canadian banks underperformed for most of the year as they reported increasing provisions for nonperforming loans, reflecting forecasts of worsening economic conditions. That said, expectations of interest rate cuts in 2024 helped tame recession fears and eased concerns of slowing loan growth, propelling banks higher in the fourth quarter as they appeared more stable and therefore favourable than prior estimates. The high-quality basket underperformed last quarter as improving risk sentiment in the market reduced the attractiveness of secure companies with lower earnings variability. Furthermore, high dividend payers with solid growth prospects outperformed in the fourth quarter as market participants rewarded companies that demonstrated a strong ability to support future dividends and punished high yielding businesses with less certain financial capabilities.

Views From the Frontline Rates – Interest rates declined sharply in Q4 as inflation continued to trend lower, fears of excess bond supply declined, and the Federal Open Market Committee signaled that the next change to their overnight policy interest rate would likely be lower. Labour market and consumer spending data remain resilient however businesses have indicated slowing across industries, more price-sensitive consumers, rising delinquencies, and concerns about the high cost of debt. Central banks remain committed to achieving their 2% inflation target and most acknowledge that interest rates have likely peaked.

Credit – The risk premium for corporate bonds (versus government bonds) tightened materially over the quarter, with a strong risk on tone to the market as investors priced in lower interest rates in 2024 and a “soft-landing” to economic concerns. Corporate bond supply was well received by the market. On the balance, we do not think the current risk premium adequately compensates for downside risk, and as such, we remain cautious on corporate bonds and have a bias towards higher-quality, shorter-dated credit where we view the risk / reward dynamic as being more favourable.

Equity – In the U.S., we allocated exposure to value names which outperformed over the quarter as the macroeconomic outlook improved on the backdrop of rate cut expectations. Looking forward, we expect that margins will continue to normalize as Covid-induced pent up demand fades. While we do not forecast margins to compress at an alarming rate, we believe sticky wage and input costs will continue to pressure businesses while consumers exhibit further exhaustion. As such, we are shifting our focus toward the balance between company reinvestment in capital projects and upcoming debt refinancing requirements. In line with this view, we favour businesses with stable cash flows and decreased debt loads as we believe they present an attractive contrarian opportunity if soft-landing projections prove to be overstated. Within Canada, we remain attentive to the inverse movements of ROE relative to financing costs over 2023. With the excess between ROE and financing costs compressing, businesses’ ability to create value appears more stretched than earlier in 2023. Therefore, we continue to favour high quality companies in Canada, which is typically defined by high ROE, stable earnings variability, and low financial leverage. Geographically, the U.S. economy appears to be in healthier condition with inflation easing while employment and output data remain stable and hence, our focus will be on capital expenditures. EAFE – which is generally more economically linked to China than North America – contains a large bucket of stable, high-quality businesses that may benefit from any upside economic surprises out of China. Lastly, through the lens of a Canadian investor, the Loonie’s relative value versus other major currencies presents another resource in our investment mandate to derive excess return.Downloadable Copy

Mark Warywoda, CFA

VP, Public Portfolio ManagementIan Whiteside, CFA, MBA

AVP, Public Portfolio ManagementJohanna Shaw, CFA

Director, Portfolio ManagementJin Li

Director, Equity Portfolio Management

Tyler Farrow, CFA

Senior Analyst, Equity

Andrew Vermeer

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

ADVISOR USE ONLY

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

- [pdf] Another reason to invest with Equitable

-

Market Commentary January 2026

.png "EAMG-(1).png")

Key Takeaways

Full year 2025:

• Government policy was very impactful for markets in 2025. U.S. trade policy unsettled markets in the first half of the year, as the U.S. implemented significant tariffs and engaged in tough negotiations with major trading partners. However, by mid-year, fiscal policy provided positive support for markets, particularly with the passing in the U.S. of the One Big Beautiful Bill Act in July.

• Artificial Intelligence (“AI”) continued to attract investment, particularly in the United States. This investment provided strong support for equity market performance.

• Global equity markets delivered strong performance, most notably Canadian equities, which returned an impressive 31.7%.

• Positive risk appetite supported solid corporate bond performance, which outpaced government bonds.

Fourth Quarter:

• U.S. equities advanced at a slower pace in the fourth quarter after a strong surge in the prior two quarters. Canadian equities outperformed U.S. equities, fueled by a powerful rally in the Materials, Consumer Discretionary, and Financials sectors.

• Canadian bond markets posted slightly negative returns during the quarter as higher interest rates weighed on performance. Strong corporate bond performance partially offset weakness in government bonds.

• Both the Bank of Canada and the U.S. Federal Reserve lowered policy interest rates during the quarter, with Canada dropping its benchmark rate by 25 basis points and the U.S. dropping its policy rate by 50 basis points. Both central banks signalled a cautious approach for further easing.

Economic and Market UpdateEconomic Summary: The U.S. economy continued to expand at a moderate pace, supported by strong consumer spending and AI investment. However, job growth slowed and the unemployment rate has edged higher. Inflation remains higher than the 2% target, despite easing trends. While some U.S. trading partners have made trade agreements, uncertainty remains regarding reciprocal tariffs, with a case before the U.S. Supreme Court as to their legality. The Federal Reserve lowered its policy interest rate twice during the quarter, first in October and again in December, to reach a target rate of 3.50% to 3.75%. Chair Powell cited downside risks to employment as a key factor behind the rate cut decisions and emphasized that officials are “well positioned” to wait and assess how the economy evolves.

In Canada, U.S. tariffs on steel, aluminum, autos, and lumber have weighed heavily on these sectors. While most goods continue to enter the U.S. tariff-free due to the Canada-United States-Mexico Agreement (“CUSMA”), broader uncertainty around U.S. trade policy is dampening business investment. Third quarter GDP growth exceeded market expectations, but growth tracked weaker in the fourth quarter amid the trade disputes. The labour market showed signs of improvement in the fourth quarter after earlier weakness. Headline inflation has hovered near the 2% target, while core inflation remained persistent. The Bank of Canada lowered its policy interest rate by 25 basis points to 2.25% in October and made no changes in December. Going into 2026, trade uncertainty remains with the CUSMA up for renegotiation. The Bank of Canada reiterated its readiness to respond if new shocks or accumulating evidence materially alter the outlook.

Bond Markets: During the quarter, the FTSE Canada Universe Bond Index returned -0.3% as interest rates on Canadian bonds rose (bond prices fall as interest rates go up). The increase reflected reduced expectations for interest rate cuts by the Bank of Canada and a higher risk premium demanded by investors for long-term debt. Although interest rates increased, credit spreads (i.e. the extra yield on corporate bonds versus government bonds to compensate for their extra risk) continued to move lower. These lower credit spreads resulted in positive overall returns for corporate bonds in the quarter, despite the overall bond market recording a loss. Tightening credit spreads reflected the continued risk-on tone to the market. Despite some volatility, lower-rated BBB bonds generally performed better than higher-quality A-rated bonds. Credit spreads have now rallied back to the tightest spreads since the 2008 financial crisis, nearing the tightest spreads in history. Despite expensive levels, investors remain buyers of corporate bonds, evidenced not just by falling credit spreads, but also by investors’ enthusiasm to support the primary issuance market. Corporate bond supply continues to set new records, with an impressive $37.5 billion in new issuance in the fourth quarter helping 2025 to exceed the prior year’s issuance. All told, 2025 saw an impressive $160 billion in new issuance via 358 new bonds, versus 2024’s prior record of $139 billion from 301 new bonds.

Bond Markets: During the quarter, the FTSE Canada Universe Bond Index returned -0.3% as interest rates on Canadian bonds rose (bond prices fall as interest rates go up). The increase reflected reduced expectations for interest rate cuts by the Bank of Canada and a higher risk premium demanded by investors for long-term debt. Although interest rates increased, credit spreads (i.e. the extra yield on corporate bonds versus government bonds to compensate for their extra risk) continued to move lower. These lower credit spreads resulted in positive overall returns for corporate bonds in the quarter, despite the overall bond market recording a loss. Tightening credit spreads reflected the continued risk-on tone to the market. Despite some volatility, lower-rated BBB bonds generally performed better than higher-quality A-rated bonds. Credit spreads have now rallied back to the tightest spreads since the 2008 financial crisis, nearing the tightest spreads in history. Despite expensive levels, investors remain buyers of corporate bonds, evidenced not just by falling credit spreads, but also by investors’ enthusiasm to support the primary issuance market. Corporate bond supply continues to set new records, with an impressive $37.5 billion in new issuance in the fourth quarter helping 2025 to exceed the prior year’s issuance. All told, 2025 saw an impressive $160 billion in new issuance via 358 new bonds, versus 2024’s prior record of $139 billion from 301 new bonds.

Stock Markets: The fourth quarter marked a pivotal shift in the global equity market rally of 2025. After three quarters of a highly concentrated, tech-led rally in the U.S., cyclical and valueoriented sectors outperformed in Q4. The S&P 500 advanced at a slower 2.7% in the fourth quarter, reflecting a market that is recalibrating after an extended period of concentrated gains. Canadian equities outperformed U.S. equities as the S&P/TSX Composite returned 6.3% in the quarter, finishing the year with an impressive 31.7% return. That was its strongest annual gain since 2009. The strong returns in Canadian equities were fueled by a powerful rally in the Materials sector, supported by soaring gold and base metal prices, and reinforced by the resilience of the Consumer Discretionary and Financials sectors. Internationally, developed markets in Europe and Asia gained 6.2% for the quarter, bringing their annual return to 21.2%. This move signals a healthy rebalancing as global investors rotated into attractivelyvalued international equities to hedge against elevated U.S. valuations. Capital is now flowing toward regions and sectors offering stronger earnings visibility and defensive characteristics rather than purely speculative growth.

Stock Markets: The fourth quarter marked a pivotal shift in the global equity market rally of 2025. After three quarters of a highly concentrated, tech-led rally in the U.S., cyclical and valueoriented sectors outperformed in Q4. The S&P 500 advanced at a slower 2.7% in the fourth quarter, reflecting a market that is recalibrating after an extended period of concentrated gains. Canadian equities outperformed U.S. equities as the S&P/TSX Composite returned 6.3% in the quarter, finishing the year with an impressive 31.7% return. That was its strongest annual gain since 2009. The strong returns in Canadian equities were fueled by a powerful rally in the Materials sector, supported by soaring gold and base metal prices, and reinforced by the resilience of the Consumer Discretionary and Financials sectors. Internationally, developed markets in Europe and Asia gained 6.2% for the quarter, bringing their annual return to 21.2%. This move signals a healthy rebalancing as global investors rotated into attractivelyvalued international equities to hedge against elevated U.S. valuations. Capital is now flowing toward regions and sectors offering stronger earnings visibility and defensive characteristics rather than purely speculative growth.

U.S. Equities: U.S. equities entered the fourth quarter at elevated valuations. Despite fundamentally strong earnings growth, stock prices struggled to move higher because investor expectations were for even stronger growth. Technology remained the primary driver of earnings, but the sector faced intense pressure to prove its value. Specifically, investors questioned the pace at which companies could convert AI investments into actual revenue. Investors also worried that growth remained concentrated among too few companies rather than more broadly across the economy. Sector-wise, Communication Services emerged as the top performer for the full year due to significant margin expansion. This was driven by a wave of media-related merger activity and the successful use of AI to make digital advertising more efficient. Industrials also advanced as new tax incentives for domestic manufacturing boosted factory orders. Nevertheless, the market remains concentrated with the top ten stocks representing nearly 40% of the S&P 500 Index. This level of concentration makes the market vulnerable to sudden price swings. As inflation moderated and the Federal Reserve cut rates in December, investors shifted toward more defensive sectors and international equities. This rotation signals a preference for companies with stable cash flows over speculative growth.

Canadian Equities: The Canadian market was a global standout during the quarter, supported by lower borrowing costs, a stable Financials sector, and rally in the prices of metals (including gold, but also base metals like nickel and copper). The Materials sector led the way as a weaker U.S. dollar and geopolitical tensions pushed gold to a record of US$4,550 per ounce in late December. For major mining companies, these prices generated record cash flow allowing them to raise dividends and buy back shares. The Bank of Canada interest rate cut supported both the Consumer Discretionary and Financials sectors, reducing borrowing costs, and helping banks maintain stable net interest margins. The Big Six Canadian Banks delivered strong earnings results in Q4. These were driven by a surge in capital markets activity and better-than-expected provisions for credit losses, as the economy remained resilient. Trading at 17 times forward earnings, the Canadian market appears attractively valued, prompting investors to shift away from U.S. volatility toward more tangible assets and reliable dividends.

Bottom line: The final quarter of 2025 saw a notable shift in investor positioning. As recession fears receded, attention turned to navigating a period of moderate economic expansion. In Canada, capital flowed into profitable, cash flow-generating companies in the Financials and Material sectors. Momentum in U.S. equities slowed as investors reduced risk amid caution around AI developments. Although major indices remain highly valued, opportunities persist in sectors and regions with stable cash flows and pricing power.

Downloadable Copy

Mark Warywoda, CFA

VP, Public InvestmentsIan Whiteside, CFA, MBA

AVP, Public InvestmentsJohanna Shaw, CFA

Director, Public InvestmentsJin Li

Director, Equity Investments

Wanyi Chen, CFA, FRM

Sr. Quantitative Analyst

Andrew Vermeer, CFA

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Edward Ng Cheng Hin

Analyst, Credit

Kate (Huyen) Vinh

Analyst, Equity

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy. - [pdf] Tax-free money does exist, if you know where to look.

- [pdf] Protecting your plan

- [pdf] Guide to MGA contracting

- [pdf] Segregated Fund Semi-annual Report - June 30, 2025

- [pdf] Investment Direction Form - DIA/GIA