Site Search

805 results for access website quick PROBLEMGO.com release from jail before court date cash

-

EAMG Market Commentary July 2023

Posted July 27, 2023

July 17, 2023

Rates & Credit - The rates market was volatile in Q2 as investors focused on inflation, central bank interest rate decisions, and recession probabilities. Persistent strength in U.S. consumer spending and labour markets have surprised investors and prompted further interest rate tightening from central banks. In Canada, corporate bonds outperformed government bonds and the broader FTSE Canada Universe Index during the quarter, with a total return of 0.2%, versus a loss of 1.0% for government bonds and 0.7% for the overall Index. The corporate bond outperformance was driven by a broad risk-on tone to the market, most notably in April as the market recovered from the banking sector liquidity crisis that developed during March. That said, the market tone remained cautious, with the improved risk premium on corporate bonds tempered by lingering concerns around sticky inflation, high interest rates, and the potential for slower economic growth into the latter half of the year.

Dominance of U.S. Equities – U.S. equity markets posted another strong quarter with the S&P 500 returning 8.7%, outperforming Canada and other major international equity markets. The S&P/TSX Composite, returned 1.2% in CAD. Major developed economies from Europe, Australasia, and Far East (EAFE) returned 3.2% in local currency terms. The highly anticipated re-opening of the Chinese economy has failed to materialize with economic data indicating less strength than previously forecasted. Amid sluggish Chinese growth, closely interconnected economic partners such as the European Union, as well as commodity-driven markets like Canada, have all underperformed the U.S. on a relative basis.

U.S. Fundamentals – Earnings continued to contract versus prior year, albeit at a slower pace than forecasted. Forward earnings guidance improved quarter-over-quarter with corporate sentiment returning to neutral levels. Based on our analysis, we observed that 31% of major companies expect deteriorating financial performance, while 33% expect improved performance, with the remaining expecting no material change. Overall, major U.S. companies remain well capitalized with strong operating margins. However, company guidance indicates a prioritization of cost controls amid increased consumer indebtedness and concerns about the health of the consumer.

Artificial Intelligence (AI) Mania – Despite concerns that the U.S. economy is at a late stage in its economic cycle, that monetary tightening by central banks could go too far, and the fact that earnings contracted on a year-over-year basis, equity markets became more expensive during the quarter with price-to-earnings multiples expanding. This expansion was driven by investors crowding into AI focused technology companies, with the seven largest AI/technology themed companies averaging a 26% return while the other 493 members gained only 3%. Investors rewarded businesses with contributions to AI development (hardware and software components), as well as those with the ability to implement synergies from leveraging the technology. A crowded market surge is not uncommon at this point in the economic cycle, where positive economic surprises, in this instance, strong employment and consumer spending can lead to an upswelling in investor confidence.

U.S. Quant Factors – Using our investment framework, we currently favour exposures to large cash-rich companies with innovative product offerings, which we believe offer the strongest risk-adjusted returns in the current market environment. While the valuation of AI companies seems to defy traditional rationales, the momentum has continued to push the group higher. Consequently, the Quality factor (companies with higher return-on-equity, strong operating performance, and healthy leverage levels) participated in the AI trend and consistently outperformed throughout the quarter. The Low Volatility factor (stocks with lower sensitivity to broad market movement, and lower price volatility) underperformed through the quarter. While the Low Volatility factor typically performs well at this stage of the economic cycle, the fact that a small number of stocks were responsible for much of the market’s return hurt this factor. Lastly, the Momentum factor (stocks with a recent history of price appreciation) initially underperformed during the quarter before rebounding in June. This factor’s recent outperformance suggests that the market is becoming complacent and possibly signals that rotations within the market are slowing as current trends remain in favour.

Canadian Fundamentals – Top line revenue missed forecasts while bottom line earnings were consistent with expectations. Softer-than-expected results out of Canadian financials, as well as underwhelming results from the materials sector, dragged on the aggregate index performance. Earnings forecasts for the rest of the year have been revised downward with analyst expecting index aggregate earnings to detract 2% to 3%. Meanwhile, the Bank of Canada raised its overnight interest rate by 25 basis points, bringing it to 4.75% on the backdrop of robust economic data releases including Q1 GDP and April CPI.

Canadian Quant Factors – The most notable dislocation in Canada was the convergence of the dividend yield of High-Dividend ETFs and Equal-Weight Bank ETFs. We believe that the drag from Canadian banks following the U.S. regional banking concerns in March resulted in a discount of the Quality factor as the performance of the group is sensitive to the movements of banks. While banks did recover around 35% of their SVB-induced underperformance, the nature of banking has attracted investor scrutiny given the view that we are in the late-stage of the economic cycle. That said, this environment is an attractive environment to add variants of the Quality factor, which would gain exposure to a rebounding industry that offers a similar dividend yield to the high dividend stocks.

Views From the Frontline

Rates – On an outright basis, bond yields across the curve continue to look attractive. Economic data remains strong however we are beginning to see the first signs of weakness in spending, jobs and inflation. Slower growth, a more balanced labour market, declining inflation, and tighter credit conditions will likely drive interest rates lower throughout 2023. Market participants remain focused on the extent of interest rate hikes and the duration of a pause required to bring inflation back to the 2% target. With inflation remaining more persistent than previously expected forecasts around the timing, pace and extent of the removal of monetary policy have been pushed into 2024.

Credit – The uncertain economic outlook and risks around slower economic growth later this year merit caution about corporate bonds and a bias towards higher-quality, shorter-dated credit where we think the risk / reward dynamic are more favourable. That said, the “soft-landing” narrative, now more pervasive in the market, could continue to provide support to risk assets, which we view as an opportunity to further pare down higher beta exposure.

Equities – Given the direction of the current economic and company fundamental data, we continue to favour high quality growth segments of the market with strong operating margins. As such, the late cycle conditions in the market reinforce our preference for large cap stocks over smaller, more U.S. domestically focused businesses. The U.S. Low Volatility factor’s underperformance is unlikely to reverse in the short term given the resilience of the U.S. economy. Furthermore, after a steep decline last quarter, we expect that cyclical value will find support in the near term, echoing the increased chance of slowing inflation without stalling economic growth. In Canada, equities are typically more cyclical in nature, which coupled with the potential for an earnings contraction, makes us view the Low Volatility factor as more likely to outperform. Like the U.S., we prefer Canadian high-quality companies to navigate through the late cycle environment. On the heels of poor Chinese economic data and underwhelming stimulus, we are maintaining our overweight to the U.S. relative to Canada and EAFE.

Downloadable Copy

ADVISOR USE ONLY

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable Life of Canada® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy. -

EAMG Market Commentary July 2024

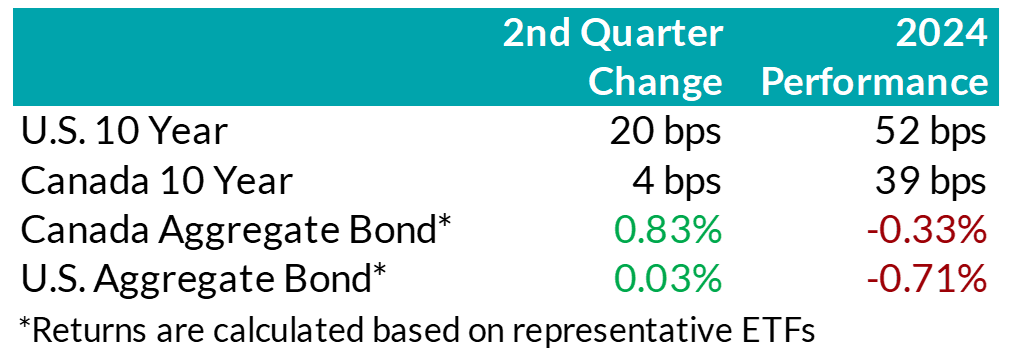

.png "Picture1-(3).png") Rates & Credit – In Q2 2024, U.S. inflation and economic growth data was mixed, leading to moderately higher interest rates in the U.S. Meanwhile, in Canada, long-end interest rates were little changed during the quarter, but short-term interest rates fell. That was due to the weaker economic outlook, as well as the Bank of Canada’s decision to reduce its overnight interest rate in June, with anticipation of further monetary policy easing to come. Canadian corporate bonds returned 1.1%, outperforming the 0.8% return of government bonds as well as the 0.9% return for the overall FTSE Canada Universe Bond index. Shorter-dated bonds outperformed longer-dated bonds. Within corporate bonds, lower-rated BBBs outperformed higher-rated A bonds, while industries that have shorter-dated debt (e.g. real estate and financials) outperformed those that tend to have longer-dated debt (e.g. communications and infrastructure).

Rates & Credit – In Q2 2024, U.S. inflation and economic growth data was mixed, leading to moderately higher interest rates in the U.S. Meanwhile, in Canada, long-end interest rates were little changed during the quarter, but short-term interest rates fell. That was due to the weaker economic outlook, as well as the Bank of Canada’s decision to reduce its overnight interest rate in June, with anticipation of further monetary policy easing to come. Canadian corporate bonds returned 1.1%, outperforming the 0.8% return of government bonds as well as the 0.9% return for the overall FTSE Canada Universe Bond index. Shorter-dated bonds outperformed longer-dated bonds. Within corporate bonds, lower-rated BBBs outperformed higher-rated A bonds, while industries that have shorter-dated debt (e.g. real estate and financials) outperformed those that tend to have longer-dated debt (e.g. communications and infrastructure).

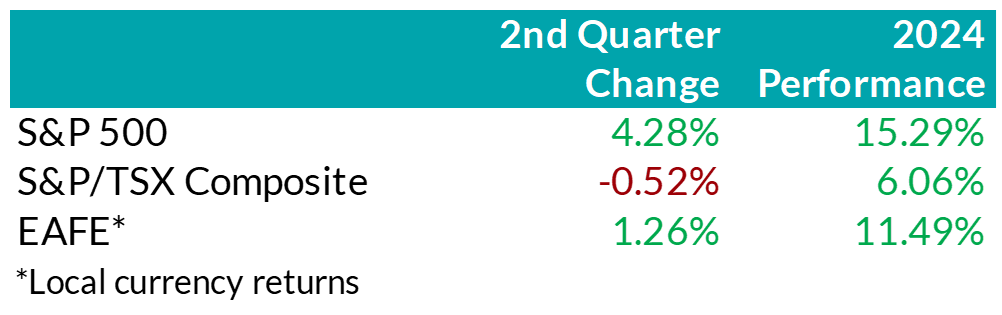

.png "Picture2-(2).png") Equity Overview – Against the backdrop of volatile inflation data and a lack of indication from the Federal Reserve that it was prepared to start cutting interest rates yet, U.S. equity markets decoupled from other regions. Crowding into AI-focused, mega-cap names accelerated in Q2. More specifically, investors defaulted toward the Magnificent 7 to navigate the current period, overlooking broadening earnings breadth and less expensive valuations from the remaining S&P 493. Outside the U.S., equity returns were generally mundane in dollar terms. That said, emerging markets proved to be a bright spot for investors seeking value, as the rebound in heavily discounted Chinese equities helped push frontier markets higher.

Equity Overview – Against the backdrop of volatile inflation data and a lack of indication from the Federal Reserve that it was prepared to start cutting interest rates yet, U.S. equity markets decoupled from other regions. Crowding into AI-focused, mega-cap names accelerated in Q2. More specifically, investors defaulted toward the Magnificent 7 to navigate the current period, overlooking broadening earnings breadth and less expensive valuations from the remaining S&P 493. Outside the U.S., equity returns were generally mundane in dollar terms. That said, emerging markets proved to be a bright spot for investors seeking value, as the rebound in heavily discounted Chinese equities helped push frontier markets higher.

U.S. Fundamentals – Corporate earnings continued to surpass expectations last quarter with stable operating margins helping businesses report better-than-expected bottom line results. Investors remain focused on the ability of companies to sustain debt levels ahead of renewing debt obligations, rewarding businesses with a strong ability to generate stable cash flows. Moreover, while prior quarters have witnessed earnings growth that was largely driven by highly profitable mega-cap technology stocks, U.S. markets are witnessing a broadening trend in earnings strength, with previously stunted segments of the market recovering. Our work shows that members of the Russell 1000 index, excluding the Magnificent 7, posted a median earnings growth of about 6% last quarter, with nearly 60% of companies increasing earnings versus the year prior. Furthermore, we observed an increase in the number of major companies that expect improving financial performance to approximately 27%, suggesting that the recovery in earnings breadth may persist.

U.S. Quant Factors – As mentioned, concentration in the equity market drove a surge in valuations as investors continued to chase specific mega-cap technology stocks. In fact, within the Russell 1000 growth factor – which screens for companies whose earnings are expected to grow at an above-average rate relative to the market – the Magnificent 7 totaled nearly 55% of the entire index by quarter-end. In addition, the Nasdaq 100 – which is generally viewed as a technology-biased index – saw the weight of the Magnificent 7 rise to almost 43% of the entire index by the end of the quarter. Furthermore, the equal-weighted S&P 500 underperformed the cap-weighted index by nearly 7% last quarter, bringing the year-to-date divergence to about 10%. With concentration accelerating, the cap-weighted index outperformance has soared past Covid-era levels, a period that saw investors rapidly crowd into profitable technology names due to panic and economic uncertainty. We remain cautious of a severely crowded market that trades near all-time highs as strong performance from 5-7 names distorts the overall stature of market conditions.

Canadian Fundamentals – Although Canadian companies exceeded bleak forecasts, earnings continue to contract on a year-over-year basis. Furthermore, earnings revisions have grinded lower with easing monetary conditions unable to offset concerns of a slowing economic environment. We note the sharp contrast versus the U.S. as the bifurcation of earnings performance widens. The CRB Raw Industrials Index, a measure of price changes of basic commodities, broke out of recent ranges as metals rallied higher despite a stronger U.S. dollar and elevated interest rates. The mining industry benefited from a sustained elevation in prices, helping the materials sector outperform over the quarter. Returns from the heavily-weighted Canadian banks were constrained last quarter with company-specific drivers – including regulatory challenges from TD, and underwhelming U.S. results from BMO – limiting performance. More broadly, the banks continue to build prudent credit provisions to mitigate uncertain economic forecasts and remain well capitalized.

Canadian Quant Factors – With investors remaining attentive to businesses’ ability to create value relative to financing costs, we see value in high quality, dividend-paying companies with strong earnings sustainability and a healthy degree of leverage. Based on our work, investors of the Canadian banks appear well compensated, with the current premium between value creation and current yield remaining compressed. In our opinion, the market has modest expectations regarding prospects for value generation from the banks and, therefore, we believe the industry stands to benefit if the premium reverts closer to historical norms. We also continue to see sources of quality dividend opportunities within certain areas of the energy sector. More specifically, we believe companies that have taken steps to improve their balance sheets through deleveraging efforts, and with improved operating leverage, offer attractive prospects given their stable and high-yielding composition.

Views From the Frontline

Rates – During the first half of the second quarter, interest rates in both Canada and the U.S. increased, continuing the upward momentum from Q1. Higher-than-expected inflation data in the U.S. along with mixed economic growth data caused investors to push out expectations for when the U.S. Federal Reserve would start lowering its interest rate. This trend shifted in the second half of Q2, as positive economic momentum slowed in the U.S. economy and inflation data began to soften. Interest rates in Canada declined more rapidly than in the U.S. due to more benign inflation, a weaker job market, and economic growth remaining below population growth. This economic weakening provided the confidence required for the Bank of Canada to cut rates by 25 basis points in June to 4.75%. The Bank also signaled that if inflation continues to ease and the Bank’s confidence grows that inflation would continue to trend toward its 2% inflation target, it is reasonable to expect further cuts. The second quarter marked a pivotal point for the global policy easing cycle. Sweden, Canada, and the European Central Bank all began lowering their policy rates, and Switzerland made a second rate cut, following one in Q1. The market continues to speculate on the timing of the U.S. Federal Reserve’s first rate cut. Interest rate cut expectations are largely unchanged in Canada since last quarter, with a total of three rate cuts expected throughout 2024. Expectations for the rate cuts by the U.S. Federal Reserve declined slightly, however, to two cuts in 2024.

Credit – The risk premium for corporate bonds (versus government bonds) was largely flat over the quarter, with spreads approaching the tight post-pandemic levels experienced in 2021. Corporate bond supply continues to be very robust, with $41bn in new issuance. Year-to-date, corporate issuance has set a new record, with an impressive $80bn in issuance. On balance, we do not think the current risk premium adequately compensates for downside risk, particularly in longer-dated corporate bonds, and have a bias towards shorter-dated credit where we view the risk / reward trade-off as being more favourable.

Equity – On the backdrop of a heavily concentrated U.S. market rally, we remain cautious of the distortion to market returns from high-flying technology stocks. As a result, we continue to favour a combination of the Dow Jones Industrial Average and the S&P 500 for our broad U.S. market exposure. The Dow provides a more diversified exposure to 30 prominent large-cap companies and less concentration in technology relative to the S&P. Broadening earnings strength presents an opportunity for previously out-of-favour names to “catch-up”. In our view, companies outside the Magnificent 7 that have demonstrated robust earnings growth, strong cash flow generation, along with decreased debt loads, are well-positioned to benefit from internal market rotations. As such, we gain exposure to these companies through the quality factor – companies with higher return-on-equity, strong operating performance, and healthy leverage levels – and the dividend growth factor – businesses with a lengthy and established history of increasing dividends.

In Canada, we remain attentive to how efficiently corporations are generating profits relative to financing costs. Looking forward, we continue to monitor the ability of businesses to generate profits given a decline in capital spending. More specifically, we are focused on businesses’ ability to grow and sustain dividends amid the lag between easing monetary conditions and consumption. Due to this, we observe value in higher yielding companies that are higher on the spectrum of quality. Geographically, we maintain our overweight U.S. exposure, underpinned by encouraging U.S. inflation data trends, broadening corporate earnings growth, and normalizing consumption. In addition, sluggish Chinese data and the lack of positive earnings revisions from EAFE tilt the risk-adjusted return profile in favour of the U.S. Lastly, as a Canadian investor, fluctuations in the Loonie’s relative value versus other major currencies continues to present tactical trading opportunities within our investment mandate.

Downloadable Copy

Mark Warywoda, CFA

VP, Public Portfolio ManagementIan Whiteside, CFA, MBA

AVP, Public Portfolio ManagementJohanna Shaw, CFA

Director, Portfolio ManagementJin Li

Director, Equity Portfolio Management

Tyler Farrow, CFA

Senior Analyst, Equity

Andrew Vermeer

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

-

March 2026 eNews

In this issue:

Equitable is adding nutrition app to all group benefits plans*

Coming soon: One-time passcodes will be added to account login process*

Standardized CLHIA disability form is now part of our disability claims submission package*

Reminder: Review manual allocations for HCSAs and/or TSAs*

Protecting clients’ plans from benefits fraud*

*Indicates content that will be shared with your clients.

Equitable is adding nutrition app to all group benefits plans

Equitable is making healthy eating easier and more accessible for all group benefits plan members. Beginning in April, access to the RxFood mobile app will be added to every Equitable group benefits plan—at no extra cost.

This will put personalized nutrition insights, practical tips and tailored recommendations at every plan member’s fingertips—helping them make more informed food choices that can either help prevent or manage chronic conditions, such as diabetes, high cholesterol and heart disease.

What is RxFood?

RxFood is Canada’s first clinically validated nutrition platform that’s used and trusted by leading health care institutions across the country, including SickKids Hospital, Diabetes Canada, Children’s Hospital of Eastern Ontario (CHEO) and more, to support better health outcomes through nutrition.

While we can track many aspects of our daily health—steps, heart rate, sleep, and blood sugar—food is often overlooked. RxFood helps close that gap by using technology that’s powered by artificial intelligence (AI) to turn everyday meals into meaningful health insights.

How it works

A plan member takes photos of their meals with their smartphone. RxFood will analyze what's on their plate, from nutritional quality to portion sizes, then provide personalized feedback, easy-to-follow suggestions and recipes with ingredient options tailored to their budget.

After a few days of logging, they’ll receive a comprehensive nutrition summary showing how their eating patterns align with their personal health goals, and where to go from there.

Check out the following video to learn more about RxFood— and how Equitable is putting the power to eat healthy in the hands of plan members.

Coming soon: One-time passcodes will be added to account login process

This spring, Equitable will launch a new multi-factor authentication (MFA) security measure to further enhance our digital security. When our new feature takes effect, anyone logging in to EquitableHealth.ca® and the Equitable EZClaim® mobile app with an email address and password may be required to enter a one-time passcode they receive via email. This will further safeguard their account access and personal data.

Keep it simple – create a passkey

If you don’t want to enter a one-time passcode when logging into your account, you can skip this extra step all together by creating a passkey on your mobile device or computer.

Passkeys are safe and provide a quicker, easier way to log in while also enhancing account security. They use either biometrics–your face or fingerprint–or a PIN authenticator to confirm your identity.

If you create and use a passkey to log in, you won’t need to enter a one-time passcode.

Learn more about passkeys. The set-up process is simple. The two videos below guide you through creating a passkey on both your mobile device and computer.

Client and plan member communications

We will share this information with clients and group benefits plan members before we introduce our new security measure. Please reach out to your Group Account Executive if you have any questions.

If you use the same email address to log in to your accounts on EquitableHealth.ca, EquiNet® and Equitable Client Access®, you can use the same passkey. Equitable Client Access is our secure site for Individual Insurance and Individual Wealth clients.

If you use the same email address to log in to your accounts on EquitableHealth.ca, EquiNet® and Equitable Client Access®, you can use the same passkey. Equitable Client Access is our secure site for Individual Insurance and Individual Wealth clients.

Standardized CLHIA disability form is now part of our disability claims submission packageClients with employees who are submitting short-term or long-term disability claims should be aware that we’ve changed one of the required forms in our disability claim submission package.

The Canadian Life and Health Insurance Association’s (CLHIA) Initial Disability Insurance Medical Statement has replaced our Attending Physician’s Statement (APS) form.

Our disability claim application packages on Equitable.ca and EquitableHealth.ca now include the CLHIA standardized form instead of our APS form. Our old form is no longer available on our websites.

We will continue accepting our previous APS form for initiating disability claims for now. However, we’re encouraging clients to begin using the standardized form as soon as possible. Using a standardized form for disability claims across the group insurance industry helps reduce the administrative burden on physicians by simplifying the disability application process.

If you have any questions, please contact your Group Account Executive.

Reminder: Review manual allocations for HCSAs and/or TSAs

If your client’s Health Care Spending Account (HCSA) and/or Taxable Spending Account (TSA) has manual allocations, they need to allocate these amounts to plan members each year.

Plan administrators can update these amounts on EquitableHealth.ca. Here are the steps:- Select View certificate

- Select Health Care Spending Account or Taxable Spending Account

- Select Update Allocation in Task Center

- Enter amount in Revised Allocation Amount

- Override Reason – Plan Administrator Request

- Select Save

- Select Reports

- Select New

- Select Next

- Select HCSA or TSA Totals by Plan Member

- Select Next

- Enter end date of 12/31/2026

- Select Next

- Select Finish

- View Report

Protecting clients’ plans from benefits fraud

March is Fraud Prevention month – the perfect time for clients to educate their plan members on the consequences of benefits fraud.

According to the Canadian Life and Health Insurance Association (CLHIA), benefits fraud costs millions each year and can contribute to higher premiums for plan sponsors.

These resources can help clients and plan members prevent benefits fraud:- CLHIA’s free 15-minute Protect Your Benefits online course for plan administrators and their members

- CLHIA’s Fraud is Fraud program, including their FAQs on benefits fraud

- CLHIA's 10 tips to 'Protect your benefits' for plan members

How we protect against benefits fraud

Our Investigative Claims Unit (ICU) uses a range of techniques, including CLHIA‑led tools, to detect and prevent benefits fraud:- Joint Provider Fraud Investigation Program: Allows insurers to collaborate on fraud investigations that affect multiple insurers.

- Data Pooling Program: Pools data between insurers and uses advanced artificial intelligence (AI) to further identify and reduce benefits fraud.

- Provider Alert Registry: Allows insurers to view the results of other insurers’ anti-fraud investigations into specific practitioners.

To learn more, contact your Group Account Executive. - [pdf] Daily/Guaranteed Interest Account Contract

- [pdf] UL Transfers & Allocations How To

-

Market Comments - October 2024

Key Takeaways for Q3· Central banks eased monetary policy by reducing their target interest rates.

· Bond markets performed very well during the quarter as interest rates fell.

· Risk markets experienced some volatility, but stock markets had robust returns.

· Canadian stocks outperformed U.S. stocks in Q3, while the sources of returns in the U.S. market were more balanced and diversified than in the first half of the year.

Views From the Frontline

Bond Markets: During the third quarter, interest rates in both Canada and the U.S. moved significantly lower as markets anticipated that the Bank of Canada would continue – and the Federal Reserve would start – cutting rates. Additionally, the expectation became that the central banks would end up lowering rates more aggressively than previously assumed. That’s because inflation data has softened sufficiently to give the central banks the scope to ease policy, and other economic data, especially from the labour market, indicated the need for them to ease policy in order to prevent economic activity from cooling too much. For instance, in Canada, inflation slowed to the Bank of Canada’s 2% target, while the labour market showed warning signs with the unemployment rate rising to 6.6%. The Bank of Canada cut its target interest rate by 0.25% at each of its July and September meetings. Governor Macklem indicated that if growth does not materialize as expected, “it could be appropriate to move faster on interest rates”. In the U.S., the Federal Reserve kicked off its easing cycle by cutting its target rate by 0.50% in September. The growing signs of a cooling labour market amidst slowing inflation motivated the larger-than-typical move. That said, consumer spending in the U.S. continued to be strong, and GDP is still tracking a healthy growth rate.

While interest rates fell, bonds returns were also boosted by solid behaviour of corporate bonds. Credit spreads (i.e. the risk premium for corporate bonds versus government bonds) continued to grind lower over the quarter. Tightening credit spreads reflected the generally positive risk-on tone to the market, despite some volatility. Lower-rated BBB bonds performed better than higher-quality A-rated bonds. Credit spreads have now generally fallen back to levels that are largely consistent with the tight post-pandemic levels experienced in 2021. The on-going appetite of investors for the extra yield offered by corporate bonds over government bonds is indicated not just by falling credit spreads, but also by investors’ enthusiasm to support the primary issuance market. Corporate bond supply continues to be very robust, with $29B (billion) in new issuance during the quarter, resulting in an impressive $119B issued year-to-date, a new record. Nonetheless, on balance, we do not think the current risk premium adequately compensates for downside risk, particularly in longer-dated corporate bonds, and have a bias towards shorter-dated credit where we view the risk / reward trade-off as being more favourable.

Stock Markets: In the U.S., we continue to caution against heavily concentrated sources of market returns and emphasize a diversified portfolio. Last quarter, diversification proved essential as a multitude of factors heightened market volatility. These factors – which included the unwind of the yen carry trade, investor reactions to mixed mega-cap earnings, and concerns of a slowing labour market – drove investors away from mega-cap technology names and into defensive areas of the market. Following the Federal Reserve’s decision to reduce interest rates by 0.5%, sources of investment returns continued to broaden as investors rotated into economically-sensitive baskets. Underpinned by decelerating inflation and easing monetary policy, we believe the rotation away from the mega-cap tech names is likely to persist and we continue to emphasize portfolio diversification. In Canada, high-quality, high-yielding businesses – composed of the financial sector and non-financial dividend payers – outperformed over the quarter as investors rewarded companies that demonstrated a strong ability to sustain dividends, as well as greater efficiency generating profits. While we continue to favour these businesses, we have taken profit on our financial sector dividend exposure after a sharp reversion in the premium between value creation and current yield. In addition, Chinese officials introduced a wave of stimulus to revitalize growth, bringing life back to the metals and luxury goods sectors. Accordingly, Canadian and European equities have benefitted recently.

Market Update

Rates & Credit: In Q3, interest rates in both Canada and the U.S. decreased significantly, with front-end interest rates declining faster than long-end interest rates amid cooling inflation and a weakening labour market. As a result, the FTSE Canada Universe Index posted a positive return of 4.7%. Coincidentally, Canadian corporate bonds and government bonds each also generated returns of 4.7%, totally in-line with the Universe index. On the other hand, despite short-term interest rates falling much more than long-term interest rates, the higher price sensitivity of long-dated bonds had them outperform shorter-dated bonds, with the Long-Term bond index up 5.8% while the Short-Term bond index gained 3.4%. Similarly, within corporate bonds, industries that have longer-dated debt (e.g. energy and infrastructure) outperformed those that tend to have shorter-dated debt (e.g. real estate and financials).

Rates & Credit: In Q3, interest rates in both Canada and the U.S. decreased significantly, with front-end interest rates declining faster than long-end interest rates amid cooling inflation and a weakening labour market. As a result, the FTSE Canada Universe Index posted a positive return of 4.7%. Coincidentally, Canadian corporate bonds and government bonds each also generated returns of 4.7%, totally in-line with the Universe index. On the other hand, despite short-term interest rates falling much more than long-term interest rates, the higher price sensitivity of long-dated bonds had them outperform shorter-dated bonds, with the Long-Term bond index up 5.8% while the Short-Term bond index gained 3.4%. Similarly, within corporate bonds, industries that have longer-dated debt (e.g. energy and infrastructure) outperformed those that tend to have shorter-dated debt (e.g. real estate and financials).

Equity Overview: Underpinned by decelerating inflation data and easing monetary policy – including the outsize 50-basis cut from the Federal Reserve – prospects for an economic soft landing increased over the quarter. That favourable outlook spurred global equity markets to all-time highs, with previously lagging areas of the market narrowing the performance gap compared to the U.S. mega-cap technology names that had led returns in the first half of the year. Canadian equities outperformed their U.S. counterpart last quarter, rising 10.5% as strength in the banking and materials sectors pushed the index higher. Major developed markets from Europe, Australasia, and the Far East (EAFE) were more subdued, gaining 0.9% (in local currency terms) last quarter. That said, grand expectations for further interest rate cuts in the U.S. pushed the greenback to its lowest level in over a year, boosting EAFE returns to over 7% in U.S. dollar terms. Within the U.S., sources of market returns broadened as well, with investors rotating out of concentrated AI companies and into more economically sensitive businesses.

Equity Overview: Underpinned by decelerating inflation data and easing monetary policy – including the outsize 50-basis cut from the Federal Reserve – prospects for an economic soft landing increased over the quarter. That favourable outlook spurred global equity markets to all-time highs, with previously lagging areas of the market narrowing the performance gap compared to the U.S. mega-cap technology names that had led returns in the first half of the year. Canadian equities outperformed their U.S. counterpart last quarter, rising 10.5% as strength in the banking and materials sectors pushed the index higher. Major developed markets from Europe, Australasia, and the Far East (EAFE) were more subdued, gaining 0.9% (in local currency terms) last quarter. That said, grand expectations for further interest rate cuts in the U.S. pushed the greenback to its lowest level in over a year, boosting EAFE returns to over 7% in U.S. dollar terms. Within the U.S., sources of market returns broadened as well, with investors rotating out of concentrated AI companies and into more economically sensitive businesses.

U.S. Fundamentals: Outside of the Magnificent 7, investors are interpreting downside earnings surprises as a normalization of financial performance rather than a deterioration. For example, McDonald’s share price rallied over 17% into quarter-end following its earnings release despite announcing declining sales and contracting earnings per share. Within the AI-ecosystem, investors are beginning to look for opportunities beyond chip manufacturers, such as nuclear energy providers. At an index level, our work shows that members of the Russell 1000 index, excluding the Mag-7, posted a median earnings growth of nearly 9% year-over-year, expanding from the ~6% witnessed in Q2. Furthermore, the number of companies from this group reporting positive earnings growth grew to approximately 67%, up from 60% in the prior quarter. In our view, the ongoing broadening of earnings strength outside of the Mag-7 can provide tailwinds to current market rotations into previously left-behind companies. Within the mega-cap tech space, investors have become more discriminant than in prior quarters, rewarding businesses with greater success monetizing their AI-investments. This trend was evident through the divergence of returns from IBM and Alphabet (Google’s parent company) following their quarterly earnings.

U.S. Quant Factors: Decelerating U.S. inflation data prompted a rotation out of highly concentrated areas of the market (growth) and into more economically-sensitive companies (value). Then, concerns of a slowing U.S. labour market and the unwind of the yen carry trade increased market volatility, leading investors to shelter their positions by reallocating to low volatility. As the quarter progressed, expectations of easing monetary policy and stabilizing employment data helped calm return to the market and the rotation from mega-cap tech sector resumed, albeit at a lesser pace. Notably, this “catch-up” trade also benefitted dividend-paying companies, particularly those with a lengthy and established history of increasing dividends, as investors favoured those more mature operations.

Canadian Fundamentals: Investors returned to the Canadian market after Canadian companies showed signs of recovery last quarter with earnings expanding by more than expected. With inflation showing clearer signs of deceleration and the outlook regarding the path of monetary policy increasingly implying lower interest rates going forward, investors are allocating toward high-quality, dividend-paying companies. From a sector level, surging gold prices provided a tailwind for Canadian miners, helping the materials sector outperform over the quarter. More recently, the materials sector has benefitted from elevated base metal prices following the arrival of Chinese stimulus. In contrast, oil prices declined over 16% last quarter as fears of an oversupplied market swelled following speculation that OPEC+ would look to dial back production cuts. As a result, investors looked past lingering geopolitical risks and the energy sector underperformed.

Canadian Quant Factors: Amid an improving Canadian macroeconomic backdrop and clearer outlook on the trajectory of monetary policy, dividend-yielding businesses became sought after. More specifically, investors continued to emphasize dividend sustainability last quarter, rewarding dividend-paying businesses that demonstrated strong financial performance and the ability to support future payouts. For example, the major Canadian banks sharply outperformed in Q3 after reporting earnings growth that mostly exceeded expectations. In essence, investors have become more constructive on this high-yielding group as their ability to create value relative to financing costs improves.

Downloadable Copy

ADVISOR USE ONLYMark Warywoda, CFA

VP, Public Portfolio ManagementIan Whiteside, CFA, MBA

AVP, Public Portfolio ManagementJohanna Shaw, CFA

Director, Portfolio ManagementJin Li

Director, Equity Portfolio Management

Tyler Farrow, CFA

Senior Analyst, Equity

Andrew Vermeer

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Francie Chen

Analyst, Rates

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

- Client Access

- [pdf] Daily/Guaranteed Interest Account Client Brochure

- Introducing Empathy – Compassion and care at time of loss

-

New “Update Payment” feature for banking changes has launched!

Great news! Equitable® has launched a new self-serve "Update Payment" feature in Client Access and on EquiNet®. This new online process enables clients and advisors to easily submit key banking change requests for eligible insurance policies*, with no need to complete a physical form.

What’s new?

A new "Update Payment" feature is now available on Client Access and on EquiNet under Policy Inquiry. It allows clients (and advisors) to easily submit requests for the following three transactions online:

1. STOP pre-authorized payments.

2. RESUME pre-authorized payments on overdue accounts.

3. CHANGE which bank we withdraw money from.

The new "Update Payment" feature replaces the previous "Edit" button in Client Access. The old banking change options are still available in the client’s Profile section. They can be used to request a change to the payment withdrawal date, as that option is not yet available with the new Update Payment feature.

How it works!

When a change is requested using the new Update Payment feature, our Operations team receives it online. They will review and process the changes within three business days, as per Equitable’s current service standards.

The Update Payment feature in Client Access is a self-serve process. However, if a client prefers, their advisor or an Equitable Customer Service associate can assist them by submitting the request on their behalf. Clients will be asked to sign to approve any such requests that are submitted by someone other than the owner of the policy.

*The Update Payment transactions are only available for eligible policies: those that have not lapsed, are not on Automatic Premium Loan, and are not owned by a corporation or other entity.

We trust that these digital enhancements will help make the client and advisor experience even simpler and more efficient.

Need more information? Please contact your Equitable wholesaler.

® or TM denotes a trademark of The Equitable Life Insurance Company of Canada.