Site Search

534 results for access source PROBLEMGO.COM Paying a witness to not show up to court

-

Market Commentary July 2025

Key Takeaways

• Markets were very volatile in April to start Q2 but calmed as the quarter progressed. Volatility was driven mostly by headlines about tariffs, but other fiscal policy developments also had an impact.

• Equity markets sold off sharply at the start of the quarter, continuing Q1’s weakness. Markets rebounded sharply once worst-case fears over tariffs eased. The markets continued to rally through the quarter as trade negotiations progressed. Stronger-thanexpected corporate earnings also boosted markets. Despite the shaky start to the quarter, most global equity markets set new all-time highs in Q2.

• Canadian bond markets delivered slightly negative returns in Q2. Weak performance was driven by rising interest rates, which outweighed the impact of tighter credit spreads. Higher interest rates hurt the performance of longer-term bonds most.

• Both the Bank of Canada and the U.S. Federal Reserve adopted a wait-and-see approach. They each held rates steady during Q2, awaiting greater clarity on the impacts of tariffs on both growth and inflation before considering further cuts.

Economic and Market UpdateEconomic Summary: Most indicators of economic activity in the U.S. continued to expand at a decent pace. However, GDP data for the first quarter came in weaker than expected, as higher imports ahead of anticipated tariffs and weaker spending by consumers weighed on Q1 GDP. That said, GDP growth is expected to bounce back in Q2. Tariffs will likely continue to be an evolving story, with potential impacts on both economic growth and inflation. Those impacts will remain uncertain until trade agreements have been finalized.

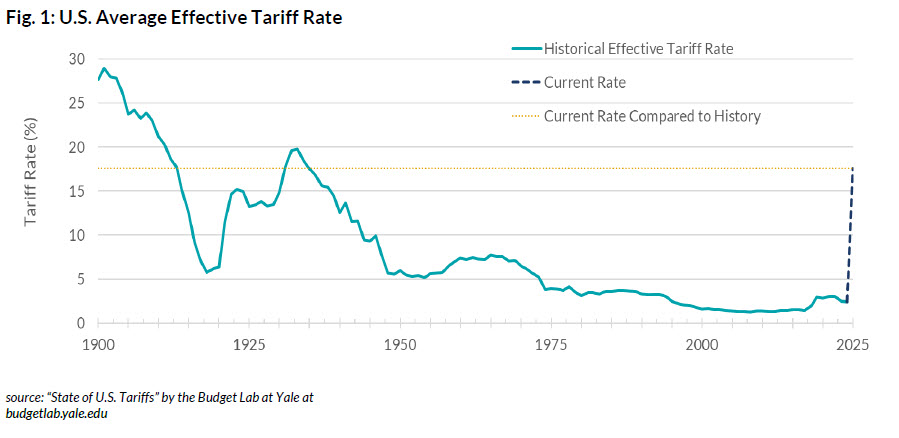

In early April, President Trump announced larger-than-expected reciprocal tariffs, with the impact most notable on trade with China. However, progress followed with a 90-day pause in tariff implementation. The U.S. then reached trade agreements with the UK, China, and Vietnam. Negotiations with other major trade partners are ongoing. The conflict between Israel and Iran raised inflation concerns, due mostly to the possibility of higher oil prices. Those concerns eased following a ceasefire. Congress passed Trump’s tax cut and spending bill, raising concerns about its potential impact on the U.S. fiscal burden. Meanwhile, U.S. labour market conditions remain resilient, with the unemployment rate remaining low. Inflation has eased slightly but remains above the Federal Reserve’s target. Amid heightened uncertainty, the Federal Reserve held interest rates steady at 4.25%–4.50% at both of its meetings in Q2. Chair Jerome Powell stated that the Fed is “well positioned to wait for greater clarity before considering any adjustments to our policy stance.”

.jpg "Fig-One-(1).jpg")

In Canada, tariffs and trade-related uncertainty continue to weigh on the economy. A pullforward of exports and inventory accumulation ahead of tariffs helped keep first-quarter GDP firm, but growth is expected to slow in the second quarter. The labour market has weakened, particularly in trade-sensitive sectors. Inflation remains within the Bank of Canada’s 1–3% preferred range. However, core CPI remains above the Bank’s preferred 2% target. Canada’s fiscal deficit is expected to widen as Prime Minister Mark Carney aims to fast-track infrastructure development and increase defense spending. Amid ongoing trade uncertainty, the Bank of Canada held its policy rate at 2.75% during its April and June meetings. Governor Tiff Macklem signaled the Bank’s readiness to cut rates further if economic conditions deteriorate.

.jpg "Fig-Two-(1).jpg")

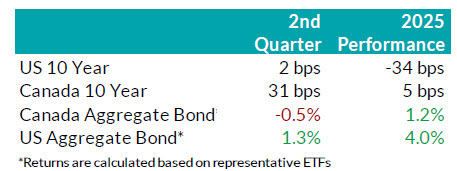

Bond Markets: During Q2, the FTSE Canada Universe Bond Index returned -0.6%. Yields for Canadian bonds rose across all maturities over the quarter. That reflected reduced expectations for rate cuts by the Bank of Canada and a higher risk premium on long-term debt. The impact of higher yields on government bonds was offset in part by tightening of credit spreads on provincial and corporate bonds. Overall corporate bonds saw a positive return for the quarter and outperformed government bonds, in part due to the strong recovery in credit spreads that started in late

April. While corporate issuance slowed considerably in April due to increased trade policy uncertainty, issuance in the Canadian bond markets during May and June were robust. There were 83 deals during Q2 that combined to raise $37 billion for issuers. June 2025 was the 3rd busiest month for issuance on record. We continue to expect higher credit spreads as the U.S. tariffs impact global growth. As such, we have maintained our conservative view with a bias towards shorter corporate bonds but remain ready to invest in longer corporate bonds as valuations become

attractive.

.jpg "Fig-Three-(1).jpg")

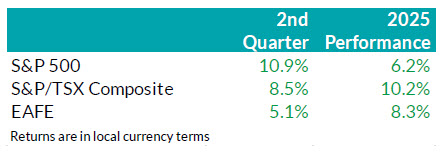

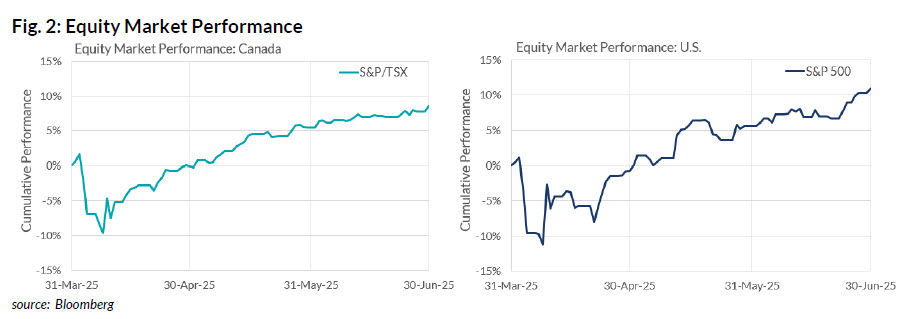

Stock Markets – Overview: Having done a round-trip following April tariff announcements, technology, consumer discretionary and industrial companies propelled the U.S. equity market to another record high. The S&P 500 ended the quarter up about 11%, outperforming Canadian and international markets. Canadian equities gained 8.5% in Q2, buoyed by front-loaded demand that benefited the Materials sector, while Financials recovered from a poor Q1. Meanwhile, as risk sentiment stabilized following the 90-day tariff pause and U.S. equities regained momentum, the appeal of the “Sell America” trade diminished. As a result, Europe, Australasia, and the Far East (EAFE) markets finished the quarter with a more modest gain of just over 5%, lagging the sharper

recovery seen in North America.

.jpg "Fig-Four-(1).jpg")

U.S. Equities: The U.S. equity market staged a V-shaped recovery on strong company earnings data in the second quarter. A stable job market and muted inflation reinforced the view of a resilient U.S. economy. At a company level, we observed positive corporate earnings surprises, steady profit margins and better-than-expected forward earnings guidance. Together they underpinned the equity market’s sharp reversal to the upside. Market breadth also improved over the quarter, with strength extending beyond Technology to include Industrials and Financials. That signalled that the market rally was supported by investors’ confidence in the U.S. economy. Furthermore, structural investment trends in artificial intelligence (AI) continued to accelerate, highlighted by rising enterprise capex in data centres. Beyond AI, Circle, a blockchain-based platform that supports stablecoin issuance, tokenized assets, and digital payment infrastructure, conducted a successful IPO. Its share price jumped 485% from its listing price as of quarter-end. On June 17, the U.S. Senate passed the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act, a regulatory framework for use of tokenized assets. While investors wait for the House’s decision, equity price actions suggest that the policy environment is increasingly supportive of blockchain innovation and digital efficiency.

Canadian Equities: Canadian equities posted solid gains in Q2, with Financials overtaking Materials to lead the market higher. Momentum from the Materials sector, which benefited from the pull-forward demand related to U.S. tariff uncertainty, faded toward quarter-end. Meanwhile, cooling inflation and muted domestic growth pushed investors towards highquality, high-dividend-paying companies. Notably, banks significantly outperformed the broader market, as investors favoured their stable corporate fundamentals. Energy surged briefly amid escalating geopolitical tensions, but those gains proved short-lived. In recap, investors in the Canadian market faced slowing resource demand and a stalling domestic economy, which fueled increased interest in high-quality, high-dividend-paying companies. That is a trend we expect to continue going forward.

Bottom line: Markets remain heavily influenced by sentiment, with U.S. policy developments and ongoing tariff negotiations continuing to cause periodic volatility. However, there is little

evidence of deterioration in the hard data to date. As such, we continue to anchor our positioning on underlying data rather than market narratives. Looking ahead, the combination of a structurally higher-for-longer interest rate environment and increasingly pro-growth policy backdrop presents selective opportunities. In the U.S., this favours highquality growth stocks, particularly within Technology, where strong balance sheets and long-term thematic tailwinds remain intact. In Canada, Financials, especially the relatively inexpensive banks, present a more compelling opportunity as earlier tailwinds from pullforward demand are beginning to wane. While we remain constructive, we are mindful of elevated equity valuations and continue to closely monitor macro conditions and policy developments for signs of inflection.

Downloadable Copy

Mark Warywoda, CFA

VP, Public InvestmentsIan Whiteside, CFA, MBA

AVP, Public InvestmentsJohanna Shaw, CFA

Director, Public InvestmentsJin Li

Director, Equity Investments

Wanyi Chen, CFA, FRM

Sr. Quantitative Analyst

Andrew Vermeer, CFA

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Edward Ng Cheng Hi

Analyst, Credit

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

-

Market Commentary July 2025

Key Takeaways

• Markets were very volatile in April to start Q2 but calmed as the quarter progressed. Volatility was driven mostly by headlines about tariffs, but other fiscal policy developments also had an impact.

• Equity markets sold off sharply at the start of the quarter, continuing Q1’s weakness. Markets rebounded sharply once worst-case fears over tariffs eased. The markets continued to rally through the quarter as trade negotiations progressed. Stronger-thanexpected corporate earnings also boosted markets. Despite the shaky start to the quarter, most global equity markets set new all-time highs in Q2.

• Canadian bond markets delivered slightly negative returns in Q2. Weak performance was driven by rising interest rates, which outweighed the impact of tighter credit spreads. Higher interest rates hurt the performance of longer-term bonds most.

• Both the Bank of Canada and the U.S. Federal Reserve adopted a wait-and-see approach. They each held rates steady during Q2, awaiting greater clarity on the impacts of tariffs on both growth and inflation before considering further cuts.

Economic and Market UpdateEconomic Summary: Most indicators of economic activity in the U.S. continued to expand at a decent pace. However, GDP data for the first quarter came in weaker than expected, as higher imports ahead of anticipated tariffs and weaker spending by consumers weighed on Q1 GDP. That said, GDP growth is expected to bounce back in Q2. Tariffs will likely continue to be an evolving story, with potential impacts on both economic growth and inflation. Those impacts will remain uncertain until trade agreements have been finalized.

In early April, President Trump announced larger-than-expected reciprocal tariffs, with the impact most notable on trade with China. However, progress followed with a 90-day pause in tariff implementation. The U.S. then reached trade agreements with the UK, China, and Vietnam. Negotiations with other major trade partners are ongoing. The conflict between Israel and Iran raised inflation concerns, due mostly to the possibility of higher oil prices. Those concerns eased following a ceasefire. Congress passed Trump’s tax cut and spending bill, raising concerns about its potential impact on the U.S. fiscal burden. Meanwhile, U.S. labour market conditions remain resilient, with the unemployment rate remaining low. Inflation has eased slightly but remains above the Federal Reserve’s target. Amid heightened uncertainty, the Federal Reserve held interest rates steady at 4.25%–4.50% at both of its meetings in Q2. Chair Jerome Powell stated that the Fed is “well positioned to wait for greater clarity before considering any adjustments to our policy stance.”

In Canada, tariffs and trade-related uncertainty continue to weigh on the economy. A pullforward of exports and inventory accumulation ahead of tariffs helped keep first-quarter GDP firm, but growth is expected to slow in the second quarter. The labour market has weakened, particularly in trade-sensitive sectors. Inflation remains within the Bank of Canada’s 1–3% preferred range. However, core CPI remains above the Bank’s preferred 2% target. Canada’s fiscal deficit is expected to widen as Prime Minister Mark Carney aims to fast-track infrastructure development and increase defense spending. Amid ongoing trade uncertainty, the Bank of Canada held its policy rate at 2.75% during its April and June meetings. Governor Tiff Macklem signaled the Bank’s readiness to cut rates further if economic conditions deteriorate.

Bond Markets: During Q2, the FTSE Canada Universe Bond Index returned -0.6%. Yields for Canadian bonds rose across all maturities over the quarter. That reflected reduced expectations for rate cuts by the Bank of Canada and a higher risk premium on long-term debt. The impact of higher yields on government bonds was offset in part by tightening of credit spreads on provincial and corporate bonds. Overall corporate bonds saw a positive return for the quarter and outperformed government bonds, in part due to the strong recovery in credit spreads that started in late

April. While corporate issuance slowed considerably in April due to increased trade policy uncertainty, issuance in the Canadian bond markets during May and June were robust. There were 83 deals during Q2 that combined to raise $37 billion for issuers. June 2025 was the 3rd busiest month for issuance on record. We continue to expect higher credit spreads as the U.S. tariffs impact global growth. As such, we have maintained our conservative view with a bias towards shorter corporate bonds but remain ready to invest in longer corporate bonds as valuations become

attractive.

Stock Markets – Overview: Having done a round-trip following April tariff announcements, technology, consumer discretionary and industrial companies propelled the U.S. equity market to another record high. The S&P 500 ended the quarter up about 11%, outperforming Canadian and international markets. Canadian equities gained 8.5% in Q2, buoyed by front-loaded demand that benefited the Materials sector, while Financials recovered from a poor Q1. Meanwhile, as risk sentiment stabilized following the 90-day tariff pause and U.S. equities regained momentum, the appeal of the “Sell America” trade diminished. As a result, Europe, Australasia, and the Far East (EAFE) markets finished the quarter with a more modest gain of just over 5%, lagging the sharper

recovery seen in North America.

U.S. Equities: The U.S. equity market staged a V-shaped recovery on strong company earnings data in the second quarter. A stable job market and muted inflation reinforced the view of a resilient U.S. economy. At a company level, we observed positive corporate earnings surprises, steady profit margins and better-than-expected forward earnings guidance. Together they underpinned the equity market’s sharp reversal to the upside. Market breadth also improved over the quarter, with strength extending beyond Technology to include Industrials and Financials. That signalled that the market rally was supported by investors’ confidence in the U.S. economy. Furthermore, structural investment trends in artificial intelligence (AI) continued to accelerate, highlighted by rising enterprise capex in data centres. Beyond AI, Circle, a blockchain-based platform that supports stablecoin issuance, tokenized assets, and digital payment infrastructure, conducted a successful IPO. Its share price jumped 485% from its listing price as of quarter-end. On June 17, the U.S. Senate passed the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act, a regulatory framework for use of tokenized assets. While investors wait for the House’s decision, equity price actions suggest that the policy environment is increasingly supportive of blockchain innovation and digital efficiency.

Canadian Equities: Canadian equities posted solid gains in Q2, with Financials overtaking Materials to lead the market higher. Momentum from the Materials sector, which benefited from the pull-forward demand related to U.S. tariff uncertainty, faded toward quarter-end. Meanwhile, cooling inflation and muted domestic growth pushed investors towards highquality, high-dividend-paying companies. Notably, banks significantly outperformed the broader market, as investors favoured their stable corporate fundamentals. Energy surged briefly amid escalating geopolitical tensions, but those gains proved short-lived. In recap, investors in the Canadian market faced slowing resource demand and a stalling domestic economy, which fueled increased interest in high-quality, high-dividend-paying companies. That is a trend we expect to continue going forward.

Bottom line: Markets remain heavily influenced by sentiment, with U.S. policy developments and ongoing tariff negotiations continuing to cause periodic volatility. However, there is little

evidence of deterioration in the hard data to date. As such, we continue to anchor our positioning on underlying data rather than market narratives. Looking ahead, the combination of a structurally higher-for-longer interest rate environment and increasingly pro-growth policy backdrop presents selective opportunities. In the U.S., this favours highquality growth stocks, particularly within Technology, where strong balance sheets and long-term thematic tailwinds remain intact. In Canada, Financials, especially the relatively inexpensive banks, present a more compelling opportunity as earlier tailwinds from pullforward demand are beginning to wane. While we remain constructive, we are mindful of elevated equity valuations and continue to closely monitor macro conditions and policy developments for signs of inflection.

Downloadable Copy

Mark Warywoda, CFA

VP, Public InvestmentsIan Whiteside, CFA, MBA

AVP, Public InvestmentsJohanna Shaw, CFA

Director, Public InvestmentsJin Li

Director, Equity Investments

Wanyi Chen, CFA, FRM

Sr. Quantitative Analyst

Andrew Vermeer, CFA

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Edward Ng Cheng Hi

Analyst, Credit

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

- [pdf] Investment Direction - Legacy

-

Market Commentary April 2026

Key Takeaways

• Markets started 2026 constructively, with positive returns in both stock and bond markets in the first two months of the year. However, the war on Iran by the U.S. and Israel drove significant changes to markets in March. The biggest driver was the spike in oil prices. Oil prices increased over 70% during the quarter to over US$100 per barrel as 20% of global oil production became trapped in the Middle East when Iran closed the Strait of Hormuz.

• Canadian equities returned 3.9% in the first quarter, outperforming U.S. equities which lost -4.3%. The Canadian market benefitted from its 40% exposure to strong performing Energy, Materials and Utilities sectors, which each gained over 10% in Q1. Conversely, the U.S. market has much less exposure to those strong performing sectors and therefore fell as geopolitical tensions weighed on performance of most other sectors.

• Canadian bonds posted modest gains as early-quarter strength was largely offset by March weakness. Rising commodity prices reignited inflation fears and prompted speculation for central bank interest rate hikes. Credit spreads widened as concerns regarding defaults and liquidity in the private credit market intensified.

• The Bank of Canada and the U.S. Federal Reserve held policy rates unchanged during the first quarter. Both central banks maintained a wait-and-see approach amid slowing labour markets, persistent inflation risks, and heightened global uncertainty.

Economic and Market UpdateEconomic Summary: The U.S. economy continued to grow at a steady pace in the first quarter. Inflation remained above the Federal Reserve’s target. The labour market showed signs of cooling as hiring slowed, but the unemployment rate remained stable. However, higher energy prices and risks to global supply chains added near term inflation pressures and weighed on the global outlook. The Federal Reserve held its policy interest rate unchanged during the quarter, maintaining the target range at 3.50% to 3.75%. Chair Powell highlighted ongoing uncertainty and reiterated that the Federal Reserve is well positioned to adjust policy as economic conditions evolve.

In Canada, economic growth remained subdued in the first quarter as excess supply persisted, and the labour market softened. Inflation stayed close to the 2.0% target, though rising global energy prices increased short term inflation risks. Trade uncertainty continued to weigh on confidence and business activity. The Bank of Canada held its policy interest rate steady at 2.25% throughout the quarter. The Governing Council noted it stands ready to respond if the economic outlook shifts materially. Bond Markets: The Canada Aggregate Bond Index returned 0.23% in the first quarter. A strong start to the year in January and February (+2.25%) was mostly offset by a weak March (-1.97%), as higher oil prices from the war in Iran led to higher interest rates on Canadian bonds (bond prices fall as interest rates go up). The increase in interest rates was most predominant in shorter term bonds, with higher oil prices driving inflation fears. These inflation fears reframed the market’s interest rate cut expectations for 2026: a 40% chance of an interest cut by the Bank of Canada has now shifted to a 70% chance of not just one, but two 25 basis point increases to the Bank of Canada overnight rate in 2026. In addition, the war in Iran has resulted in a higher risk premium for corporate bonds: credit spreads (i.e. the extra yield on corporate bonds versus government bonds to compensate for their extra risk) moved higher in March after reaching record low levels in January and February. These higher credit spreads resulted in corporate bonds modestly underperforming the overall index, albeit still with positive returns. Despite the modest risk off tone, investors remain buyers of corporate bonds as evidenced by investors’ enthusiasm to support the primary issuance market. Corporate bond supply continues to set new records, with an impressive $50 billion in new issuance in the quarter, a record start to the year and 23% higher than the same period in 2025.

Bond Markets: The Canada Aggregate Bond Index returned 0.23% in the first quarter. A strong start to the year in January and February (+2.25%) was mostly offset by a weak March (-1.97%), as higher oil prices from the war in Iran led to higher interest rates on Canadian bonds (bond prices fall as interest rates go up). The increase in interest rates was most predominant in shorter term bonds, with higher oil prices driving inflation fears. These inflation fears reframed the market’s interest rate cut expectations for 2026: a 40% chance of an interest cut by the Bank of Canada has now shifted to a 70% chance of not just one, but two 25 basis point increases to the Bank of Canada overnight rate in 2026. In addition, the war in Iran has resulted in a higher risk premium for corporate bonds: credit spreads (i.e. the extra yield on corporate bonds versus government bonds to compensate for their extra risk) moved higher in March after reaching record low levels in January and February. These higher credit spreads resulted in corporate bonds modestly underperforming the overall index, albeit still with positive returns. Despite the modest risk off tone, investors remain buyers of corporate bonds as evidenced by investors’ enthusiasm to support the primary issuance market. Corporate bond supply continues to set new records, with an impressive $50 billion in new issuance in the quarter, a record start to the year and 23% higher than the same period in 2025.

Stock Markets: The first quarter of 2026 marked a period of heightened investor caution with geopolitical tensions rising. Equity markets remained under pressure in March, as dip buyers remained cautious. Early market volatility was driven by several geopolitical developments, including Japan’s snap election, events in Venezuela, and U.S. interest in Greenland. Private credit markets also came under pressure as liquidity tightened and default risks increased, particularly in semi-liquid lending structures. The war on Iran raised concerns around demand destruction and inflation, pushing oil prices above US$100 per barrel for the first time since 2022. Gold continued to rise strongly early in the quarter. However, it later recorded its sharpest decline in years, driven by central bank selling. Despite this pullback, gold finished the quarter up 8% and continues to be viewed as a key safe-haven asset.

Stock Markets: The first quarter of 2026 marked a period of heightened investor caution with geopolitical tensions rising. Equity markets remained under pressure in March, as dip buyers remained cautious. Early market volatility was driven by several geopolitical developments, including Japan’s snap election, events in Venezuela, and U.S. interest in Greenland. Private credit markets also came under pressure as liquidity tightened and default risks increased, particularly in semi-liquid lending structures. The war on Iran raised concerns around demand destruction and inflation, pushing oil prices above US$100 per barrel for the first time since 2022. Gold continued to rise strongly early in the quarter. However, it later recorded its sharpest decline in years, driven by central bank selling. Despite this pullback, gold finished the quarter up 8% and continues to be viewed as a key safe-haven asset.

U.S. Equities: U.S. equities entered the first quarter with strong momentum, supported by robust earnings growth from technology companies. While earnings results confirmed this strength, investor sentiment weakened, particularly toward Software-as-a-Service (SaaS) companies. Rapid progress in AI agents developed by firms such as Anthropic and Google highlighted how quickly generative AI could automate core SaaS functions. As a result, software stocks sold off sharply in February, triggering a broader rotation away from largecap growth. Furthermore, tighter financial conditions and rising geopolitical tensions reduced risk tolerance and drove sharp sector rotation. The Energy sector led market performance, while Technology lagged and Financials underperformed due to stress in credit markets.

Canadian Equities: The Canadian stock market was supported by its high exposure to commodities. That structural tilt helped Canadian equities outperform U.S. equities as macro narratives shifted toward inflation concerns and supply risks. Performance during the quarter was marked by a sharp whipsaw between gold and oil, reflecting shifting investor sentiment. Investors sold gold aggressively and scrambled to source U.S. dollars as financial conditions tightened. Conversely, oil prices rose sharply on Middle East supply disruptions, lifting Energy stocks to become the strongest-performing sector of the quarter, up 29%.

Bottom line: The first quarter showed how quickly geopolitical shocks can reshape sectors’ performance. Canada outperformed U.S. growth markets due to its higher exposure to commodities, as energy prices rose and inflation concerns returned. The sharp move in gold and oil prices highlighted the market’s sensitivity to macro developments. The war against Iran forced investors to reprice both inflation expectations and Federal Reserve policy expectations. Looking ahead, geopolitical stability, energy prices, and central bank policy are likely to remain key drivers of market performance and sector leadership.

Downloadable Copy

Mark Warywoda, CFA

VP, Public InvestmentsIan Whiteside, CFA, MBA

AVP, Public InvestmentsJohanna Shaw, CFA

Director, Public InvestmentsJin Li

Director, Equity Investments

Wanyi Chen, CFA, FRM

Sr. Quantitative Analyst

Andrew Vermeer, CFA

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Edward Ng Cheng Hin

Analyst, Credit

Kate (Huyen) Vinh

Analyst, Equity

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

Except for statements of historical fact, all statements in this document are forward-looking statements. These forward-looking statements represent the portfolio manager’s current best judgment as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may be materially different from what is expressed. Furthermore, the portfolio manager’s views, opinions, or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable assumes no obligation to update any forward-looking information contained in this document. The reader is cautioned to consider these and other factors carefully and to not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy. -

September is Life Insurance Awareness Month

The perfect time to start conversations with clients.

Many people don’t think about life insurance until it’s too late. This month is a good time to remind clients why life insurance matters. Life insurance can help provide financial protection for families and businesses when they need it most.

As an advisor, you play a key role in helping clients make the right choices to protect the people and things they care about. At Equitable®, we’re committed to supporting you in guiding clients through these important decisions. To help you start conversations about life insurance, we have created resources that explain the different types of life insurance and how each can help clients meet their unique financial needs.

Use these tools during your client meetings, either in person or online. They can help you explain why life insurance matters, show the different plan options, and build trust with clients.

Let’s work TOGETHER this month to help clients PROTECT TODAY and PREPARE TOMORROW.

Contact your Equitable wholesaler today to learn more!

.jpg "1197-(3).jpg")

What kind of life insurance is right for you? (1197) - Resource Hub

- [pdf] Additional/Updated Client Information

-

Passkey: The fastest, safest way to log in to Client Access

We’ve upgraded the Client Access® portal to make access easier and more secure.

What’s new?

• Passkey: The easiest way to log in

Passkey is now available across all Equitable portals. With passkey, clients can log in quickly and securely using biometrics like face or fingerprint recognition, eliminating the need for passwords.

• Extra protection for email/password users

For clients who continue to use their email and password, extra security may be required. Clients may be prompted to enter a one-time passcode sent to their email, ensuring only authorized access.

What you need to know:

• Clients sign in to Client Access the same way you do on EquiNet, making it easier to support your clients.

• “Forgot email” is available to help clients recover the email they need to log in.

• Passkey setup is easy and safe. Just follow the prompts when you login. Watch the video to learn how to create a passkey. - eDelivery of a Contract - New Business

-

Easier group enrolment and more group benefits updates

Make enrolment easier for your clients with online plan member enrolment (OPME)

Enrolling new plan members can be overwhelming – for both you, your clients and their employees. It’s time-consuming to manually load new members and challenging to ensure they complete the necessary paperwork before the enrolment deadline.

Our Online Plan Member Enrolment (OPME) tool is available at no extra cost for all your Equitable Life clients and offers a more secure and efficient alternative to traditional paper enrolment. Using their computer or mobile device, employees can enrol in their benefits plan in just minutes.

The user-friendly tool allows plan members to easily enter all their enrolment information, including:- Dependent details

- Banking information for direct deposit of claim payments

- Details for coordination of benefits

- Beneficiary designation

The days of chasing plan members for their paper enrolment forms are gone. Once plan administrators enter a few employee details, our system automatically sends an email to each plan member, inviting them to enrol in their benefits program. And there will be no need for your clients to send reminders or follow up with employees about their benefits enrolment. It’s all done automatically.Support with using OPME

To learn more about the benefits of using OPME, check out our Online Plan Member Enrolment Flyer. We also encourage you to share more information with your clients: We also have helpful reference guides for plan members, to help them use the tool:- Online Plan Member Enrolment Quick Reference Guide

- myFlex Online Plan Member Enrolment Quick Reference Guide

Help your clients spend less time administering group benefits. Contact your Group Account Executive or myFlex Sales Manager to learn more about our online plan member enrolment.

Coming soon: A survey to help us serve your clients better*

We are committed to providing your clients and their plan members with industry-leading service. We’ve introduced several enhancements over the past year to make it easier to do business with us. And we’re continually looking for ways to improve.

This month, we will conduct a survey of your clients to help us understand how we can better serve them. Plan administrators will receive an email with a link to the survey, which will take between five and 10 minutes to complete.

Please encourage your clients to participate. Their feedback will be confidential, and their responses will help us improve our service and ensure we’re meeting their expectations. We will also allow them to provide their name so that we can follow up with them to address any concerns they’ve identified.

We know your clients’ time is valuable. So, each plan administrator who completes the survey will be entered into a random draw for a chance to win one of 3 prepaid gift cards for $200.

Improved mental assessment features for FeelingBetterNow®*

Mensante has enhanced its FeelingBetterNow® online platform to make it easier for plan members to assess the state of their mental health and talk to their health care provider about treatment options. FeelingBetterNow is part of our Equitable HealthConnector suite of wellness solutions and is available for an additional cost. It can help plan members easily identify if they are at risk for a number of common mental health issues, including depression, anxiety and substance abuse.Upgrades to the platform include:

- New features to help plan members better gauge their progress in the assessment.

- A printable Action Plan that plan members can share with their health care provider to initiate conversations about managing their mental health challenges.

- A new “follow-up” module to help plan members assess the care they’ve received from their health care provider and identify care gaps.

- An Assessment Outcome Page, which allows plan members to view their diagnostic risks across mental health disorders for a more holistic picture of their health.

Over-age dependants losing coverage?*

Your clients’ plan members may have dependants approaching the maximum age for eligibility under their group benefits plan. If so, members should be aware of their options for dependant coverage.Coverage for full-time students and dependants with disabilities

The dependants of your clients’ plan members may be eligible to continue their coverage under the current plan if:- The dependant is attending a post-secondary school full-time; or

- The dependant is disabled.

Coverage2go for over-age dependants

Dependants who aren’t eligible for continued coverage under the plan can apply for Coverage2go®, a month-to-month health and dental plan for individuals losing their group coverage.**

Coverage2go is affordable, reliable and allows the over-age dependants to choose the level of coverage and protection that suits their personal situation. With no medical questions required as long as they apply within 60 days of losing their coverage, your clients’ plan members can ensure that their over-age dependants have the coverage they need.

Plan members can receive a quote within minutes. Please direct your clients to Coverage2go on Equitable.ca to learn more.

**Quebec residents are not eligible for Coverage2go.Forfeiture reports for HCSAs and TSAs on EquitableHealth.ca*

As a reminder, your clients can access forfeiture reports for their Health Care Spending Account (HCSA) and Taxable Spending Account (TSA) usage on EquitableHealth.ca.HCSA summary by plan member

HCSA summary reports provide an overview of each plan member’s account activity and balances. These reports include the total amounts allocated, the amount claimed to date, the net balance, and the amount of funds that will be forfeited based on claims paid to date. Please note that plan members’ claim submissions will remain confidential and will not be viewable by the employer on this summary.

Your clients can provide each plan member with their HCSA summary, if they wish.HCSA account forfeiture by plan member

HCSA forfeiture reports detail the amount that each member will forfeit if they do not use it. The amount is based on claims that have been paid to date within the benefit year period.HCSA account totals by plan member

Your clients may wish to access the HCSA account totals reports, which reflect the information in each plan member’s HCSA summary report. For terminated employees, the Funds Available field will display as zero, regardless of the balance in the account when terminated.

At least three months before the end of the benefits period, your clients should remind their members to use their allocated HCSA and TSA amounts.

If your clients need help accessing these reports, they can reach out to their Regional Office Service team for assistance.

* Indicates content that will be shared with your clients.