Site Search

353 results for access fast MAKEMUR.COM Paying customs to release seized items Georgia

-

Enhancing the Transfer Process: Equitable's New Signature Guarantee Service

Equitable® is making transfers even easier with EZcomplete®.

This enhancement will help advisors and clients by reducing the number of rejections from other institutions that need a signature guarantee. Reducing transfer rejections means less time and effort for advisors, and faster transfers from other institutions.

Signature Guarantees

Equitable will now offer signature guarantees on most transfers requested through EZcomplete.

When is a signature guarantee not available?

• For entity owned accounts

• If a Power of Attorney is signing on behalf of an owner

• If the transferring account has an irrevocable beneficiary

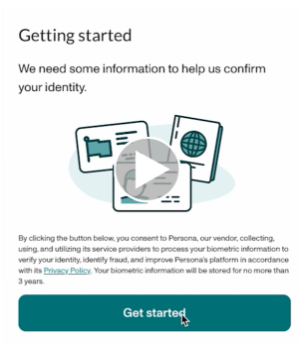

Watch the quick Identity Check with Persona video or read through instructions below.

To offer a signature guarantee, Equitable first needs to check the identity of all owners using Persona, a third-party service provider.

The advisor starts by selecting a signature guarantee in EZcomplete. An email link is sent to all proposed owners.

Clients can click the link within the email to Persona's verification process.

They will be prompted to take a picture of their photo ID and a selfie, turning their head slightly left and right by following the prompts.

Their identity can then be confirmed in seconds.

Sending Transfer Forms:

• If all owners' identities are verified, Equitable will send the transfer form with a signature guarantee stamp and the e-signature audit log to the transferring institution.

• If ID verification fails, clients will be prompted to try up to three times. If still unsuccessful, the transfer form and e-signature audit log is sent to the transferring institution without the signature guarantee stamp.

Handling Issues:

• Advisors’ obligations to verify ID is not affected by this process; ID verification is still required.

• If the client times out or loses the email to access Persona, the advisor can resend the link.

• If the client’s name or email changes after ID verification, the advisor will need to redo the ID verification with the updated information to get a signature guarantee.

This update strives to make processes smoother and more efficient for everyone. Just another reason to do business with Equitable. When we work together, success is mutual.

For more information or assistance, please contact your Director, Investment Sales.

Date published: May 7, 2025 -

Elevate your business with industry best practices and needs-based selling

Keeping your business aligned with industry best practices is vital for your success. It not only supports the fair treatment of clients – it also helps you meet certain market conduct requirements and Equitable’s expectations for needs-based selling.

The Financial Services Regulatory Authority of Ontario (FSRA) has a program that checks how well advisors follow the Insurance Act and its conduct rules. FSRA looks at how well advisors follow industry best practices and fair treatment of clients guidance (see CLHIA’s guidance document, “The Approach”). Their focus is on key areas such as giving sound advice, managing conflicts of interest, and putting clients’ needs first. FSRA selects advisors’ client files and looks for documentation that indicates needs-based selling.

In December 2024, FSRA released its latest Market Conduct Supervision Report. It highlights the need for advisors to follow certain rules and industry best practices. The report found five key areas where improvement is needed:

1. Missing notes from client meetings and calls

2. Inadequate advisor disclosure

3. Missing sales illustrations for different product options

4. Missing insurance needs analysis

5. Missing policy delivery receipts

By following industry best practices and keeping thorough records, you show your commitment to providing clients with the solutions they need. For example, taking notes during client meetings helps you track all discussions that support your recommendations. Having an insurance needs analysis shows you are providing clients with suitable advice to buy the solutions that best meet their needs.

Resources: Equitable® has resources that can help improve your business practices and help you treat clients fairly. We encourage you to check these out:

1. PPT: “Ensuring a Compliant, Needs-based Insurance Sale”. The steps to follow in needs-based selling and the records to keep.

Get CE credits! We offer the above as a self-study course that qualifies for 1 Continuing Education (CE) credit. Access it here: https://equitable-life-education.teachable.com/. (Use your contracted email to log in).

2. Client File Reference: The records to keep when selling investments, life insurance, or critical illness insurance, including key documents insurers and regulators look for during compliance audits.

3. Investor Profile Questionnaires: These will help you document your sales recommendations for:

● Universal Life (UL) sales: 1190.pdf, and

● Pivotal Select (Segregated Fund) sales: 1165.pdf

Questions? Contact your Equitable wholesaler. They are ready to support your success! - Choosing the right funds

-

Step Up Your Wealth is Back—and It’s All About You!

Equitable® is excited to bring back our Step Up Your Wealth Sales campaign for 2026! This is your opportunity to grow your business, deepen client relationships and earn rewards for doing what you do best—helping Canadians achieve financial confidence.

As an advisor, you know the value of a strong partner. At Equitable, we combine the strength of a mutual company with a full suite of competitive wealth solutions designed to help support every stage of a clients’ financial journey.

Your Advantage Starts Here

Expand Your Offering: Access a comprehensive range of products to meet diverse client needs—from accumulation to retirement income.

Build Stronger Relationships: Position yourself as a trusted advisor with solutions backed by Equitable’s proven track record.

Earn More: Receive a Growth Bonus* as our way of recognizing your commitment and success.

This campaign is designed to help you grow your book of business while delivering exceptional value to clients. Together, we can make 2026 your most successful year yet because when we grow together, success is mutual.

Ready to Step Up? Visit our website or connect with your Director, Investment Sales today for full details.

*The bonus amount will be calculated on December 31, 2026 based on net deposits to Equitable Individual Wealth products for 2026. The bonus will be paid within 90 days following December 31, 2026. Maximum bonus payable is $100,000 for re-qualifying Elite Advisors; $75,000 otherwise. Re-qualifying Elite Advisors are advisors who attained Elite status at the end of 2025 and maintain Elite status at the end of 2026. To attain Elite advisor status, an advisor must have $1,250,000 in gross deposits in at least five Equitable policies in 2026 or $10,000,000 in assets with Equitable’s Individual Wealth at the end of 2026. For re-qualifying Elite Advisors that reach $10,000,000 or more in net deposits in both 2025 and 2026, the maximum payment is $200,000. Equitable reserves the right to end or after the Step Up Your Wealth Sales campaign or the Elite Advisor Program at any time and without notice. - Total Cost Reporting: understanding what's coming next

-

Term vs permanent life insurance: helping clients choose the best solution for them

Most people understand why life insurance matters. What they’re often unsure about is which type of coverage is right for them. As an advisor, you’re in a unique position to do more than present options, you can help clients feel confident they’re making an informed choice.

Start with the client, not the product

Before discussing insurance solutions, you can start by asking three important questions:

1. What do you need to protect today?

2. What are you trying to achieve for the future?

3. What is your budget?

By asking these questions you will get a better understanding of which solution fits the client’s needs.

Matching the solution to the client

Term life insurance may be ideal for clients who have budget considerations and need coverage for:

• Helping to replace income

• Helping cover a mortgage or other debts

• Business protection

• A specific period of time (10 – 30 years)

If a client wants lifetime coverage but can’t afford it right now, term insurance is a good option. It gives them affordable coverage today that they can later choose to convert to permanent insurance when their income increases.1

Permanent life insurance (whole life and universal life) is an option for clients looking for lifelong coverage and added long-term value. It’s a good option for clients who want to:

• Build an inheritance

• Preserve their estate

• Build tax advantaged cash value growth

Permanent life insurance is also an excellent way for parents or grandparents to help give children or grandchildren some lasting financial security. It secures lifetime protection at a lower cost when the child is young and healthy. It also offers the potential for cash value growth that they can access if needed.

Helping clients make confident choices

By focusing on what the client needs now—and what they might need later—you can help them pick life insurance that fits their changing life and financial goals. Share this client‑friendly piece that outlines some of the things that clients should consider to make an informed decision:

Which life insurance solution is right for you?

Reminder: Clients’ needs can change; it’s a good idea to review their coverage regularly.

For any questions, contact your Equitable wholesaler.

1See contract for details on conversion limitations and eligibility. - EZstart

-

Equitable Life Group Benefits Bulletin – October 2020

In this issue:

- Group benefits enrolment just got a lot easier*

- Critical Illness added to myFlex Benefits® selection tool**

- ASO dental available down to 3 lives

- QDIPC updates terms and conditions for 2021*

*Indicates content that will be shared with your clients

**Indicates content that will be shared with myFlex Benefits groups onlyGroup benefits enrolment just got a lot easier*

Our Online Plan Member Enrolment tool now makes it simple to add new employees to the benefits plan.

Enrolling new plan members can be overwhelming – for both you, your clients and their employees. It’s challenging to ensure plan members complete the necessary paperwork before the enrolment deadline, and time consuming to manually load new members.

That’s why we’re updating our plan member enrolment experience. Beginning November 2nd, 2020, all Equitable Life groups will be able to easily enrol new employees in the benefits plan with our Online Plan Member Enrolment Tool.

Benefits of Online Plan Member Enrolment

Our Online Plan Member Enrolment tool offers a more secure and efficient option to traditional paper enrolment. Employees are able to enrol in their benefits plan in just minutes from their computer or mobile device.

The user-friendly interface was built with the plan member in mind. They can easily enter all their enrolment information, including dependent details, banking information for direct deposit of claim payments and details for coordination of benefits. They can even designate their beneficiary electronically.

The online enrolment tool also lessens the effort for plan administrators to onboard new hires. The tool reduces errors and rework that can occur due to spelling mistakes or missing information on paper forms. And the days of chasing plan members for their paper enrolment forms are gone. Once they enter a few employee details, our system will automatically send out an email to each plan member, inviting them to enrol in their benefits program. And there will be no need to send reminders or follow up with employees about their benefits enrolment. It’s all done automatically.

Online plan member enrolment is available to all traditional and myFlex Benefits plan administrators with update access beginning November 2nd, 2020. Plan administrators just choose “New” from the “Certificate” view in EquitableHealth.ca to get started.

This enhancement is for plan administrators who have update access on EquitableHealth.ca. If your clients are not sure if they have update access, they can contact their Equitable Life Client Relationship Specialist or myFlex Benefits Team for support.

Learn More

We’ve created Online Plan Member Enrolment User Guides to support your clients and their plan members with this new tool:

- Online Plan Member Enrolment 1-page flyer

- Plan Member Online Plan Member Enrolment Quick Reference Guide

- myFlex Plan Member Online Plan Member Enrolment Quick Reference Guide

We’re also offering a series of webinars to help your clients learn about Online Plan Member Enrolment. Plan administrators will receive an invitation with links to register for the time that best suits their schedule.

Help your clients spend less time administering group benefits. Contact your Group Account Executive or myFlex Sales Manager to learn more about our enhanced online plan member enrolment.

Critical Illness added to myFlex Benefits selection tool*

For many employers, mandatory Critical Illness (CI) coverage is an important part of their group benefits package. It provides proactive protection against life-altering illness, helping give plan members and their families a sense of security.

While CI is available on myFlex Benefits plans, it was not built into our benefits selection tool since there is no action required by the plan member.

Beginning November 2nd, 2020, we are adding a CI page to the myFlex Benefits selection tool that appears when this coverage is included as part of the plan. There are no options to choose – plan members simply review their CI coverage and carry on with the benefits selection process. It keeps the process smooth, while ensuring plan members fully appreciate their employer’s contributions.

Adding CI to the benefits selection tool also simplifies the budgeting process for employers. Now that CI is included in the selection tool, employers no longer need to break out the amount billed for CI from their contribution per employee when loading flex allocations.

To learn more about our myFlex Benefits selection tool or Critical Illness coverage for myFlex Benefits, contact your myFlex Sales Manager.

ASO dental available down to 3 lives

Beginning November 2nd, 2020, groups with as few as three full-time employees will be able to self-insure their Equitable Life dental benefits with an Administrative Services Only (ASO) funding arrangement.

Currently, dental benefits are only available on an ASO basis for groups with 20 lives or more.

In an ASO arrangement, Equitable Life administers the benefits plan but does not insure it. The plan sponsor pays for all eligible claims, as well as the expenses of administering the plan.

Why ASO?

Choosing an ASO funding arrangement allows plan sponsors to save on premiums. With a traditional insured funding arrangement, a portion of every premium dollar includes a charge for the risk that the insurer is assuming to cover the claims.

With an ASO arrangement, the plan sponsor assumes all risk, so they avoid the risk charge. And since dental claims are usually more predictable than other benefits, there is typically less risk involved in covering those claims.

For more information, contact your Group Account Executive or myFlex Sales Manager.

QDIPC updates terms and conditions for 2021*

Every year, the Quebec Drug Insurance Pooling Corporation (QDIPC) reviews the terms and conditions for the high-cost pooling system in the province. Based on its latest review, QDIPC is revising its pooling levels and fees for 2021 to reflect trends in the volume of claims submitted to the pool, particularly catastrophic claims.

Size of group (# of certificates) Threshold per certificate 2021 Annual factor (without dependents) Annual factor (with dependents) Fewer than 25 $8,000 $251.00 $691.00 25 - 49 $16,500 $165.00 $455.00 50 - 124 $32,500 $94.00 $258.00 125 - 249 $47,500 $68.00 $187.00 250 - 499 $72,000 $49.00 $135.00 500 - 999 $95,000 $40.00 $111.00 1,000 - 3,999 $120,000 $35.00 $95.00 4,000 - 5,999 $300,000 $16.00 $44.00 6,000 and over Free market - Groups not subject to Quebec Industry Pooling Free market - Groups not subject to Quebec Industry Pooling Free market - Groups not subject to Quebec Industry Pooling We will apply the new pooling levels and fees to future renewal calculations that involve Quebec plan members.

-

Equitable Life Group Benefits Bulletin – December 2021

In this issue:

- Supporting plan members affected by the flooding in Nova Scotia and Newfoundland*

- Update: Changing certificate numbers on EquitableHealth.ca*

- Help plan members take advantage of convenient digital options*

- Ontario optometrists and government to restart negotiations*

- QDIPC updates terms and conditions for 2022*

Supporting plan members affected by the flooding in Nova Scotia and Newfoundland*

The recent flooding in Nova Scotia and Newfoundland is having a devastating impact on the province’s residents.

Here are some of the ways we can help support your clients’ plan members who are affected by the flooding.

Prescription refills

Until Dec. 31, our pharmacy benefit manager, TELUS Health, will allow early refills for plan members who have been evacuated and/or lost their medication due to the flooding.

Replacement of medical or dental equipment and appliances

If plan members in Nova Scotia or Newfoundland need to replace any eligible medical or dental equipment or appliances (e.g. prescription eyeglasses, dentures, etc.) due to the flooding, they can call us at 1.800.265.4556 before incurring additional expenses to see how we can support them.

Disability or other benfit cheques

If plan members affected by the flooding are receiving disability benefits or other benefit reimbursements by cheque, they can visit www.equitable.ca/go/digital for easy instructions on how to sign up for direct deposit. It’s easy and takes just a few minutes. They can call us at 1.800.265.4556 if they need help. We can also arrange for a different mailing address or replacement cheques if necessary.

Mental Health Support

A natural disaster can also take a serious toll on people’s mental health. All of our plan members have access to the Homeweb online portal and mobile app, including numerous articles, tools and resources designed to provide guidance and support in difficult times. Homewood has put together some suggestions on how to help employees affected by a natural disaster.

For your clients with an Employee and Family Assistance Program, remind them that their plan members have 24/7 access to confidential counselling through a national network of mental health professionals. Whether it’s face-to-face, by phone, email, chat or video, plan members will receive the most appropriate, most timely support for the issue they’re dealing with.

If a client wishes to add the EFAP to their plan, we can do this quickly – often in just a few days. Simply contact your Group Account Executive or myFlex Sales Manager.

Plan Administrator support

We realize that the flooding may also be having an impact on the regular business operations of your clients in Nova Scotia and Newfoundland. If any of your clients are unable to carry out day-to-day plan administration, they can call us at 1.800.265.4556 to see how we can support them.

We know this is a challenging time for many of your clients and their plan members. We will continue to monitor the situation and provide additional updates as appropriate.

Update: Changing certificate numbers on EquitableHealth.ca*

Effective Dec. 10th, plan administrators will no longer be able to update or change plan members’ certificate numbers on EquitableHealth.ca. This change will ensure we can manage these changes more effectively to provide a smoother plan member experience.

If your clients need to update a plan member’s certificate number, please have them reach out to Group Benefits Administration for assistance at groupbenefitsadmin@equitable.ca.

Help plan members take advantage of convenient digital options*

We have several digital options available to make it easier for your clients to do business with us and for their plan members to access and use their benefits plan.

To help build awareness among plan members, we’ve created two posters that your clients can post on their intranet sites or in their office. The posters provide easy instructions on how to activate our secure, digital options.

Please click on the links below to download the posters.

EquitableHealth.ca posters: EZClaim mobile app posters:

EquitableHealth.ca English EZClaim mobile app English poster

EquitableHealth.ca French poster EZClaim mobile app French poster

Ontario optometrists and government to restart negotiations*

The Ontario Association of Optometrists (OAO) announced it has paused its job action and will restart negotiations with the Ontario Ministry of Health on funding for optometry services.

In September, Ontario optometrists began withholding services from patients covered by OHIP, including children, senior citizens and other patients with certain medical conditions, after negotiations with the Ministry of Health over compensation broke down.

Residents of Ontario between the ages of 20 to 64 who aren’t eligible for coverage of eye services under OHIP were not affected by the job action. They were able to continue to receive eye exams from their optometrist and submit eligible claims to their benefits plan.

QDIPC updates terms and conditions for 2022*

Every year, the Quebec Drug Insurance Pooling Corporation (QDIPC) reviews the terms and conditions for the high-cost pooling system in the province. Based on its latest review, QDIPC is revising its pooling levels and fees for 2022 to reflect trends in the volume of claims submitted to the pool, particularly catastrophic claims.

Size of group (# of certificates) Threshold per certificate 2022 Annual factor (without dependents Annual factor (with dependents) Fewer than 25 $8,000 $276.00 $771.00 25 – 49 $16,500 $188.00 $527.00 50 – 124 $32,500 $97.00 $328.00 125 – 249 $55,000 $66.00 $223.00 250 – 499 $80,000 $51.00 $173.00 500 – 999 $105,000 $39.00 $153.00 1,000 – 3,999 $130,000 $34.00 $133.00 4,000 – 5,999 $300,000 $18.00 $71.00 6,000 and over Free market – Groups not subject to Quebec Industry Pooling

We will apply the new pooling levels and fees to future renewal calculations that involve Quebec plan members. -

January 2024 eNews

In this issue:

- Equitable scores high marks with group advisors*

- REMINDER: Equitable's National Biosimilar Program starts in March*

- 2024 dental fee guide updates*

- Homewood Health wins HR Reporter Reader's Choice award for EFAP excellence*

Equitable scores high marks with group advisors*

Equitable ranked first for operational service among major group insurers in a recent study of Canadian group benefits advisors.

NMG Consulting, a leading global consulting firm, conducted in-depth interviews with 146 Canadian group benefits brokers, consultants, MGAs and third-party administrators between May and August 2023 for its annual Canadian Group Benefits Study. Based on these interviews, NMG ranked group insurers in six categories, ranging from operational management to technology.

Nationally, Equitable ranked among the top three in five of the six main categories, including number one for Operational Management:Category Ranking Operational management 1st Initiatives (including seminars & training) 2nd Technology 3rd Underwriting & claims management 3rd Relationship management 3rd

“Advisors regard us highly in many categories. That’s a testament to our mutual status and ability to focus exclusively on our clients and advisor partnerships,” said Marc Avaria, Executive Vice President, Group Insurance Division. “We are truly working together to build strong, enduring and aligned partnerships with our clients and advisors.”

“We’re delighted with these results and are committed to continuously advancing our delivery of a better benefits experience for our clients and advisors,” added Avaria.More highlights from the latest NMG survey

Nationally, we ranked first in seven subcategories in Operational Management, including:- Overall service to intermediaries,

- Overall service to plan sponsors,

- New quote process,

- Plan implementation,

- Renewal process,

- Accuracy and timeliness of reporting and billing, and

- Administration quality and responsiveness

And we were rated strongly in Technology, finishing in the top three for:- Overall technology for Intermediary (2nd)

- Member experience (3rd)

- Quality of technology for the plan sponsor (2nd)

- Quality of mobile application (2nd)

REMINDER: Equitable's National Biosimilar Program starts in March*

In October 2023 we announced the upcoming launch of our national biosimilar program. Starting March 1, 2024, we are expanding our biosimilar switch initiatives to provide a single, nationwide** program.

Why we’re making the switch

Over the past few years, most provinces have introduced policies to delist some originator biologic drugs. They require most patients to switch to biosimilar versions of those drugs to be eligible for coverage under their public drug plans. Soon, it is expected that all provincial drug plans will cover only biosimilars.

Equitable’s National Biosimilar Program simplifies drug plan coverage by replacing our provincial programs. It also protects clients from additional drug costs while offering access to lower-cost biosimilars deemed equally safe and effective by Health Canada.

How will this affect clients' drug plans?

Because we have already introduced biosimilar switch initiatives in most provinces, the impact of this change will be minimal. It will primarily affect plan members in provinces or territories where we haven’t already required the switch to biosimilars. It will also affect plan members who are taking biosimilars that were not originally included in the switch initiative for their province.

Regardless of where they live, plan members across Canada will no longer be eligible for most originator biologic drugs if they have a condition for which Health Canada has approved a lower-cost biosimilar version of the drug. Plan members already taking the originator biologic will be required to switch to a biosimilar version of the drug to maintain coverage under their Equitable plan. We will support their transition with education, personalized communication, and resources.

Advance notice for plan members

We contacted affected claimants in early December to give them enough time to change their prescriptions and avoid any interruptions in their treatment or their coverage.

If you have any questions about this change, please contact your Group Account Executive or myFlex Account Executive.

** Excludes plan members in Quebec who participate in a separate provincial program.

2024 dental fee guide updates*

Each year, Provincial and Territorial Dental Associations publish fee guides. Equitable uses these guides to help determine the reimbursement limits for dental procedures.

For your reference, you may wish to refer to the 2024 list of the average dental fee increases for general practitioners.

Homewood Health wins HR Reporter Reader's Choice award for EFAP excellence*

Equitable is proud to congratulate our Employee and Family Assistance Plan (EFAP) partner, Homewood Health®, for winning the Canadian HR Reporter 2023 Reader’s Choice Award in Employee Assistance Plan services. Homewood’s EFAP provides confidential support for a range of health, family, money, and work issues through face-to-face, phone, email, chat, or video counselling. The award recognizes their high standards in counselling and mental health support services.

The annual Reader’s Choice Awards identify organizations that provide outstanding expertise and services for HR professionals and employers across Canada. Those organizations provide valuable information on useful, innovative HR and employee benefits products and programs, in categories such as recruitment, mental health services, employee engagement programs, and more.

Sharing Homewood Health with your clients

Since 2019, we have worked with Homewood to provide mental health services for Equitable benefits plan members.

Your clients can access Homewood Health’s award-winning EFAP for an additional fee by adding it to their benefits plan. Services are available 24/7, 365 days a year.

All Equitable clients also have free access to Homewood Health Online in their benefits plan. Homewood Online provides a variety of helpful wellness resources, including:

- Homeweb, an online and mobile health and wellness portal,

- Health Risk Assessment, a group of assessment tools to help plan members identify and overcome health and wellness barriers, and

- Online Internet-based cognitive behavioural therapy (iCBT) through Sentio to manage symptoms of anxiety and/or depression.

Questions

To learn more about Homewood Health’s services, contact your Group Account Executive or myFlex Account Executive.