Site Search

324 results for open quick MAKEMUR.COM pay a judge to replace my prison sentence with house arrest or a fine

- [pdf] Pivotal Select Application - FHSA

- [pdf] Daily/Guaranteed Interest Account Application - FHSA

-

Equitable Life Group Benefits Bulletin – September 2021

In this issue:

- Right drug, right dose*

- Responding to New Brunswick’s Biosimilar Initiative*

- Helping plan members access our convenient digital options*

- Reminder: Please access forms on EquitableHealth.ca*

- Over-age dependents losing coverage?*

Right drug, right dose

Equitable Life partners with Personalized Prescribing Inc. to help plan members avoid treatment trial and error

Patients suffering from mental health conditions often need to try several medications before they find one that works for them. This is frustrating and can result in negative side-effects, a longer recovery, lost productivity, or a delayed return to work.

To help plan members avoid this treatment trial and error, we have partnered with Personalized Prescribing Inc. to provide easier access to pharmacogenomic testing for plan members with mental health conditions.

Pharmacogenomics 101

Pharmacogenomics is the study of how an individual’s genes influence their response to medications. Pharmacogenomic testing can help determine how compatible a patient’s body may be to a particular drug, and helps their physician prescribe the most appropriate medication. The goal is to ensure the right drug is prescribed to deliver the most positive outcome with the fewest side effects.

Easier access to pharmacogenomic testing

Through our partnership with Personalized Prescribing Inc., any Equitable Life plan member diagnosed with a mental health condition can purchase a pharmacogenomic test for a discounted price of $399 plus HST – a 20% savings.

We are also introducing the option for plan sponsors to add coverage of pharmacogenomic tests provided by Personalized Prescribing Inc. for mental health conditions.

With this coverage, plan members are eligible for pharmacogenomic testing if:- They have been diagnosed with a mental health condition;

- They are currently taking or have stopped taking a medication for a mental health condition that does not work or has side effects; and

- The pharmacogenomic test is conducted by Personalized Prescribing Inc.

Getting a test is easy. The plan member starts by visiting www.personalizedprescribing.com/equitablelife to request a test kit.

Once they receive their test kit from Personalized Prescribing Inc., they simply provide a saliva sample and send it back (postage is pre-paid). Within 7-10 business days, they receive an Rx Report™ that they can share with their doctor. This report includes details to help their doctor prescribe the right drug and the right dose for them.

Benefits for plan members:- The plan member and their physician receive a full report that is easy to understand;

- The report identifies the most compatible medications for the plan member’s condition and the medications to avoid;

- The physician is able to prescribe the most appropriate medication with the fewest side effects; and

- The plan member avoids medication trial and error.

- Pharmacogenomic testing can be an effective prevention strategy to help employees stay healthy and potentially avoid a mental health-related work absence; and

- Employees suffering from mental health conditions may be more productive when they are on the right medication for them.

Responding to New Brunswick’s Biosimilar Initiative

We are changing coverage for some biologic drugs in New Brunswick in response to the province’s Biosimilar Initiative. These changes will help protect your clients from additional drug costs while still providing access to equally safe and effective biosimilars.

What is New Brunswick’s Biosimilar Initiative?

New Brunswick’s Biosimilar Initiative will end provincial coverage of several originator biologic drugs for some or all conditions beginning on December 1, 2021. Patients who are using these drugs for the affected conditions will be required to switch to biosimilar versions of the drugs to maintain coverage under the province’s government drug plan.

What is the impact on private drug plans?

The most significant risk to plan sponsors who maintain coverage of originator biologics is coordination of benefits (CoB) risk. If other insurance carriers follow suit with the province and delist the originator biologics, it could expose a plan that doesn’t delist them to significant coordination of benefits risk.

For example, consider a patient who is covered under two private plans – their employer plan and a spousal plan. If their employer plan was the first payer for the originator biologic but delists the drug, the spousal plan now becomes the first payor. If the spousal plan continues to cover the cost of the originator, it now pays most or all of the cost of the drug.

How is Equitable Life responding?

To protect your clients’ plans from paying additional and avoidable drug costs, we are changing coverage in New Brunswick for most biologic drugs included in the provincial initiative.

Beginning Feb. 1, 2022, plan members in New Brunswick will no longer be eligible for coverage of Humira, Lantus, Humalog and Copaxone if they have a condition for which Health Canada has approved a lower cost biosimilar version of the drug. These plan members will be required to switch to a biosimilar version of those drugs to maintain coverage under their Equitable Life plan.

How will Equitable Life communicate this change to plan members?

We will be communicating with affected claimants in early-December 2021 to allow them ample time to change their prescriptions and avoid any interruptions in their treatment or their coverage.

Can my client maintain coverage of these biologic drugs?

All groups, except myFlex clients, who wish to opt out of this change and maintain coverage of these originator biologics for New Brunswick plan members can submit a policy amendment. Amendments must be submitted no later than Nov. 30, 2021.

Advisors with myFlex Benefits clients who wish to maintain coverage of these originator biologics for New Brunswick plan members should speak to their myFlex Sales Manager to confirm their eligibility to opt out of this change.

Groups that opt out of this change are also opting out of any future changes to our New Brunswick biosimilar initiative. Their drug plans will continue to cover any additional originator biologics that we subsequently add to the program.

Will this change impact my clients’ rates?

The rate impact of this change and any cost savings associated with the change will be factored in at renewal.

If plan sponsors opt out of these changes and maintain coverage for the originator biologics, it may result in a rate increase. Any rate adjustment will be applied at renewal.

What is the difference between biologics and biosimilars?

Biologics are drugs that are engineered using living organisms like yeast and bacteria. The first version of a biologic developed is also known as the “originator” biologic. Biosimilars are also biologics. They are highly similar to the originator drug they are based on and have been shown to have no clinically meaningful differences in safety or efficacy.

Questions?

If you have any questions about this change, please contact your Group Account Executive or myFlex Sales Manager.

Helping plan members access our convenient digital options

Some of your clients’ plan members aren’t benefitting from our secure and convenient digital options to access and use their Group Benefits. They can sign up to submit claims electronically for faster claim payments, get claim payments deposited directly to their bank accounts, easily review their coverage details, quickly access their Group Benefits plan booklet, benefits card and more. We’ve made it easier than ever to sign up, with more resources all conveniently located at Equitable.ca/go/digital.

Your clients’ plan members can visit this link to view:- A brochure with all the high-level instructions they need to get started on EquitableHealth.ca and the EZClaim mobile app

- A full video guide on how to access and navigate EquitableHealth.ca

Reminder: Please access forms on EquitableHealth.ca*

We routinely update our Plan Administrator forms on EquitableHealth.ca based on their feedback and to stay compliant with legal and/or regulatory requirements. If your clients need a form, they should always pull the most recent version from EquitableHealth.ca instead of reusing forms they have saved on their computer. Using an old or outdated form may result in processing delays.

Your clients can access the Plan Administrator forms by following these steps:- Login to EquitableHealth.ca

- Select “Documents”

- Toggle between English and French forms

- Click on the document name to download a PDF copy

Over-age dependents losing coverage?*

Some of your clients’ plan members may have dependents who are reaching the maximum age for eligibility under their group benefits plan.

If they are attending school full-time or are disabled, they may be eligible for continued coverage. Plan members with over-age dependents can simply complete the Application for Coverage of Dependent Child Over Age 21 (Form #441) and submit it through our online document submission tool. They can access the tool by logging into their Group Benefits account at www.equitablehealth.ca and clicking My Resources.

If they are not attending school full-time or disabled, they will no longer be covered under the plan. However, they may be eligible for Coverage2go®. It allows individuals who are losing their group coverage to purchase personal month-to-month health and dental coverage that is affordable, reliable and works like their previous group benefits plan. They can choose the level of coverage and protection that suits their personal situation.

There are no medical questions – they simply need to apply within 60 days of losing their health coverage under their group benefits plan.*

Help your clients’ plan members and their dependents who are losing coverage by letting them know about Coverage2go. They can visit our website to learn more about Coverage2go and to get a quote.

*Quebec residents are not eligible for Coverage2go - Continuing Education

- [pdf] FHSA to RSP/RIF Conversion

-

Market Commentary July 2025

Key Takeaways

• Markets were very volatile in April to start Q2 but calmed as the quarter progressed. Volatility was driven mostly by headlines about tariffs, but other fiscal policy developments also had an impact.

• Equity markets sold off sharply at the start of the quarter, continuing Q1’s weakness. Markets rebounded sharply once worst-case fears over tariffs eased. The markets continued to rally through the quarter as trade negotiations progressed. Stronger-thanexpected corporate earnings also boosted markets. Despite the shaky start to the quarter, most global equity markets set new all-time highs in Q2.

• Canadian bond markets delivered slightly negative returns in Q2. Weak performance was driven by rising interest rates, which outweighed the impact of tighter credit spreads. Higher interest rates hurt the performance of longer-term bonds most.

• Both the Bank of Canada and the U.S. Federal Reserve adopted a wait-and-see approach. They each held rates steady during Q2, awaiting greater clarity on the impacts of tariffs on both growth and inflation before considering further cuts.

Economic and Market UpdateEconomic Summary: Most indicators of economic activity in the U.S. continued to expand at a decent pace. However, GDP data for the first quarter came in weaker than expected, as higher imports ahead of anticipated tariffs and weaker spending by consumers weighed on Q1 GDP. That said, GDP growth is expected to bounce back in Q2. Tariffs will likely continue to be an evolving story, with potential impacts on both economic growth and inflation. Those impacts will remain uncertain until trade agreements have been finalized.

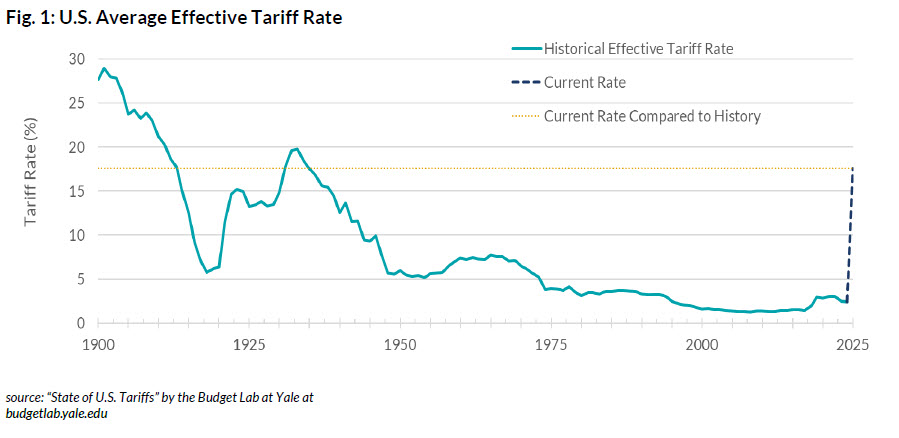

In early April, President Trump announced larger-than-expected reciprocal tariffs, with the impact most notable on trade with China. However, progress followed with a 90-day pause in tariff implementation. The U.S. then reached trade agreements with the UK, China, and Vietnam. Negotiations with other major trade partners are ongoing. The conflict between Israel and Iran raised inflation concerns, due mostly to the possibility of higher oil prices. Those concerns eased following a ceasefire. Congress passed Trump’s tax cut and spending bill, raising concerns about its potential impact on the U.S. fiscal burden. Meanwhile, U.S. labour market conditions remain resilient, with the unemployment rate remaining low. Inflation has eased slightly but remains above the Federal Reserve’s target. Amid heightened uncertainty, the Federal Reserve held interest rates steady at 4.25%–4.50% at both of its meetings in Q2. Chair Jerome Powell stated that the Fed is “well positioned to wait for greater clarity before considering any adjustments to our policy stance.”

.jpg "Fig-One-(1).jpg")

In Canada, tariffs and trade-related uncertainty continue to weigh on the economy. A pullforward of exports and inventory accumulation ahead of tariffs helped keep first-quarter GDP firm, but growth is expected to slow in the second quarter. The labour market has weakened, particularly in trade-sensitive sectors. Inflation remains within the Bank of Canada’s 1–3% preferred range. However, core CPI remains above the Bank’s preferred 2% target. Canada’s fiscal deficit is expected to widen as Prime Minister Mark Carney aims to fast-track infrastructure development and increase defense spending. Amid ongoing trade uncertainty, the Bank of Canada held its policy rate at 2.75% during its April and June meetings. Governor Tiff Macklem signaled the Bank’s readiness to cut rates further if economic conditions deteriorate.

.jpg "Fig-Two-(1).jpg")

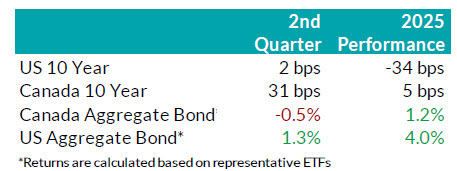

Bond Markets: During Q2, the FTSE Canada Universe Bond Index returned -0.6%. Yields for Canadian bonds rose across all maturities over the quarter. That reflected reduced expectations for rate cuts by the Bank of Canada and a higher risk premium on long-term debt. The impact of higher yields on government bonds was offset in part by tightening of credit spreads on provincial and corporate bonds. Overall corporate bonds saw a positive return for the quarter and outperformed government bonds, in part due to the strong recovery in credit spreads that started in late

April. While corporate issuance slowed considerably in April due to increased trade policy uncertainty, issuance in the Canadian bond markets during May and June were robust. There were 83 deals during Q2 that combined to raise $37 billion for issuers. June 2025 was the 3rd busiest month for issuance on record. We continue to expect higher credit spreads as the U.S. tariffs impact global growth. As such, we have maintained our conservative view with a bias towards shorter corporate bonds but remain ready to invest in longer corporate bonds as valuations become

attractive.

.jpg "Fig-Three-(1).jpg")

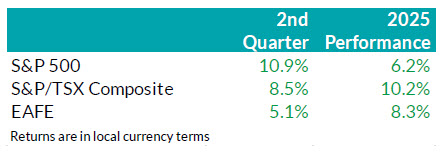

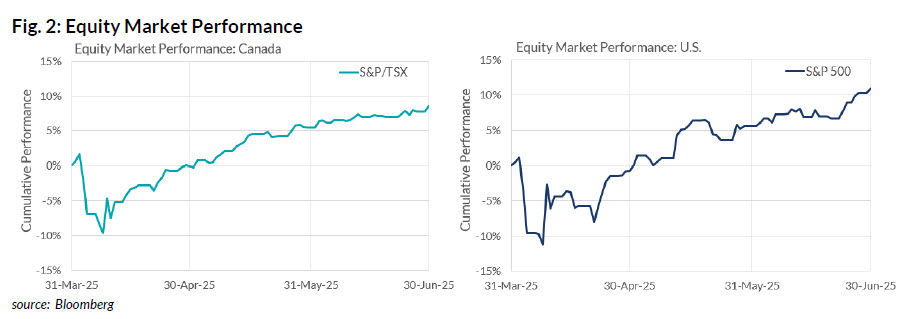

Stock Markets – Overview: Having done a round-trip following April tariff announcements, technology, consumer discretionary and industrial companies propelled the U.S. equity market to another record high. The S&P 500 ended the quarter up about 11%, outperforming Canadian and international markets. Canadian equities gained 8.5% in Q2, buoyed by front-loaded demand that benefited the Materials sector, while Financials recovered from a poor Q1. Meanwhile, as risk sentiment stabilized following the 90-day tariff pause and U.S. equities regained momentum, the appeal of the “Sell America” trade diminished. As a result, Europe, Australasia, and the Far East (EAFE) markets finished the quarter with a more modest gain of just over 5%, lagging the sharper

recovery seen in North America.

.jpg "Fig-Four-(1).jpg")

U.S. Equities: The U.S. equity market staged a V-shaped recovery on strong company earnings data in the second quarter. A stable job market and muted inflation reinforced the view of a resilient U.S. economy. At a company level, we observed positive corporate earnings surprises, steady profit margins and better-than-expected forward earnings guidance. Together they underpinned the equity market’s sharp reversal to the upside. Market breadth also improved over the quarter, with strength extending beyond Technology to include Industrials and Financials. That signalled that the market rally was supported by investors’ confidence in the U.S. economy. Furthermore, structural investment trends in artificial intelligence (AI) continued to accelerate, highlighted by rising enterprise capex in data centres. Beyond AI, Circle, a blockchain-based platform that supports stablecoin issuance, tokenized assets, and digital payment infrastructure, conducted a successful IPO. Its share price jumped 485% from its listing price as of quarter-end. On June 17, the U.S. Senate passed the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act, a regulatory framework for use of tokenized assets. While investors wait for the House’s decision, equity price actions suggest that the policy environment is increasingly supportive of blockchain innovation and digital efficiency.

Canadian Equities: Canadian equities posted solid gains in Q2, with Financials overtaking Materials to lead the market higher. Momentum from the Materials sector, which benefited from the pull-forward demand related to U.S. tariff uncertainty, faded toward quarter-end. Meanwhile, cooling inflation and muted domestic growth pushed investors towards highquality, high-dividend-paying companies. Notably, banks significantly outperformed the broader market, as investors favoured their stable corporate fundamentals. Energy surged briefly amid escalating geopolitical tensions, but those gains proved short-lived. In recap, investors in the Canadian market faced slowing resource demand and a stalling domestic economy, which fueled increased interest in high-quality, high-dividend-paying companies. That is a trend we expect to continue going forward.

Bottom line: Markets remain heavily influenced by sentiment, with U.S. policy developments and ongoing tariff negotiations continuing to cause periodic volatility. However, there is little

evidence of deterioration in the hard data to date. As such, we continue to anchor our positioning on underlying data rather than market narratives. Looking ahead, the combination of a structurally higher-for-longer interest rate environment and increasingly pro-growth policy backdrop presents selective opportunities. In the U.S., this favours highquality growth stocks, particularly within Technology, where strong balance sheets and long-term thematic tailwinds remain intact. In Canada, Financials, especially the relatively inexpensive banks, present a more compelling opportunity as earlier tailwinds from pullforward demand are beginning to wane. While we remain constructive, we are mindful of elevated equity valuations and continue to closely monitor macro conditions and policy developments for signs of inflection.

Downloadable Copy

Mark Warywoda, CFA

VP, Public InvestmentsIan Whiteside, CFA, MBA

AVP, Public InvestmentsJohanna Shaw, CFA

Director, Public InvestmentsJin Li

Director, Equity Investments

Wanyi Chen, CFA, FRM

Sr. Quantitative Analyst

Andrew Vermeer, CFA

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Edward Ng Cheng Hi

Analyst, Credit

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

-

Market Commentary July 2025

Key Takeaways

• Markets were very volatile in April to start Q2 but calmed as the quarter progressed. Volatility was driven mostly by headlines about tariffs, but other fiscal policy developments also had an impact.

• Equity markets sold off sharply at the start of the quarter, continuing Q1’s weakness. Markets rebounded sharply once worst-case fears over tariffs eased. The markets continued to rally through the quarter as trade negotiations progressed. Stronger-thanexpected corporate earnings also boosted markets. Despite the shaky start to the quarter, most global equity markets set new all-time highs in Q2.

• Canadian bond markets delivered slightly negative returns in Q2. Weak performance was driven by rising interest rates, which outweighed the impact of tighter credit spreads. Higher interest rates hurt the performance of longer-term bonds most.

• Both the Bank of Canada and the U.S. Federal Reserve adopted a wait-and-see approach. They each held rates steady during Q2, awaiting greater clarity on the impacts of tariffs on both growth and inflation before considering further cuts.

Economic and Market UpdateEconomic Summary: Most indicators of economic activity in the U.S. continued to expand at a decent pace. However, GDP data for the first quarter came in weaker than expected, as higher imports ahead of anticipated tariffs and weaker spending by consumers weighed on Q1 GDP. That said, GDP growth is expected to bounce back in Q2. Tariffs will likely continue to be an evolving story, with potential impacts on both economic growth and inflation. Those impacts will remain uncertain until trade agreements have been finalized.

In early April, President Trump announced larger-than-expected reciprocal tariffs, with the impact most notable on trade with China. However, progress followed with a 90-day pause in tariff implementation. The U.S. then reached trade agreements with the UK, China, and Vietnam. Negotiations with other major trade partners are ongoing. The conflict between Israel and Iran raised inflation concerns, due mostly to the possibility of higher oil prices. Those concerns eased following a ceasefire. Congress passed Trump’s tax cut and spending bill, raising concerns about its potential impact on the U.S. fiscal burden. Meanwhile, U.S. labour market conditions remain resilient, with the unemployment rate remaining low. Inflation has eased slightly but remains above the Federal Reserve’s target. Amid heightened uncertainty, the Federal Reserve held interest rates steady at 4.25%–4.50% at both of its meetings in Q2. Chair Jerome Powell stated that the Fed is “well positioned to wait for greater clarity before considering any adjustments to our policy stance.”

In Canada, tariffs and trade-related uncertainty continue to weigh on the economy. A pullforward of exports and inventory accumulation ahead of tariffs helped keep first-quarter GDP firm, but growth is expected to slow in the second quarter. The labour market has weakened, particularly in trade-sensitive sectors. Inflation remains within the Bank of Canada’s 1–3% preferred range. However, core CPI remains above the Bank’s preferred 2% target. Canada’s fiscal deficit is expected to widen as Prime Minister Mark Carney aims to fast-track infrastructure development and increase defense spending. Amid ongoing trade uncertainty, the Bank of Canada held its policy rate at 2.75% during its April and June meetings. Governor Tiff Macklem signaled the Bank’s readiness to cut rates further if economic conditions deteriorate.

Bond Markets: During Q2, the FTSE Canada Universe Bond Index returned -0.6%. Yields for Canadian bonds rose across all maturities over the quarter. That reflected reduced expectations for rate cuts by the Bank of Canada and a higher risk premium on long-term debt. The impact of higher yields on government bonds was offset in part by tightening of credit spreads on provincial and corporate bonds. Overall corporate bonds saw a positive return for the quarter and outperformed government bonds, in part due to the strong recovery in credit spreads that started in late

April. While corporate issuance slowed considerably in April due to increased trade policy uncertainty, issuance in the Canadian bond markets during May and June were robust. There were 83 deals during Q2 that combined to raise $37 billion for issuers. June 2025 was the 3rd busiest month for issuance on record. We continue to expect higher credit spreads as the U.S. tariffs impact global growth. As such, we have maintained our conservative view with a bias towards shorter corporate bonds but remain ready to invest in longer corporate bonds as valuations become

attractive.

Stock Markets – Overview: Having done a round-trip following April tariff announcements, technology, consumer discretionary and industrial companies propelled the U.S. equity market to another record high. The S&P 500 ended the quarter up about 11%, outperforming Canadian and international markets. Canadian equities gained 8.5% in Q2, buoyed by front-loaded demand that benefited the Materials sector, while Financials recovered from a poor Q1. Meanwhile, as risk sentiment stabilized following the 90-day tariff pause and U.S. equities regained momentum, the appeal of the “Sell America” trade diminished. As a result, Europe, Australasia, and the Far East (EAFE) markets finished the quarter with a more modest gain of just over 5%, lagging the sharper

recovery seen in North America.

U.S. Equities: The U.S. equity market staged a V-shaped recovery on strong company earnings data in the second quarter. A stable job market and muted inflation reinforced the view of a resilient U.S. economy. At a company level, we observed positive corporate earnings surprises, steady profit margins and better-than-expected forward earnings guidance. Together they underpinned the equity market’s sharp reversal to the upside. Market breadth also improved over the quarter, with strength extending beyond Technology to include Industrials and Financials. That signalled that the market rally was supported by investors’ confidence in the U.S. economy. Furthermore, structural investment trends in artificial intelligence (AI) continued to accelerate, highlighted by rising enterprise capex in data centres. Beyond AI, Circle, a blockchain-based platform that supports stablecoin issuance, tokenized assets, and digital payment infrastructure, conducted a successful IPO. Its share price jumped 485% from its listing price as of quarter-end. On June 17, the U.S. Senate passed the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act, a regulatory framework for use of tokenized assets. While investors wait for the House’s decision, equity price actions suggest that the policy environment is increasingly supportive of blockchain innovation and digital efficiency.

Canadian Equities: Canadian equities posted solid gains in Q2, with Financials overtaking Materials to lead the market higher. Momentum from the Materials sector, which benefited from the pull-forward demand related to U.S. tariff uncertainty, faded toward quarter-end. Meanwhile, cooling inflation and muted domestic growth pushed investors towards highquality, high-dividend-paying companies. Notably, banks significantly outperformed the broader market, as investors favoured their stable corporate fundamentals. Energy surged briefly amid escalating geopolitical tensions, but those gains proved short-lived. In recap, investors in the Canadian market faced slowing resource demand and a stalling domestic economy, which fueled increased interest in high-quality, high-dividend-paying companies. That is a trend we expect to continue going forward.

Bottom line: Markets remain heavily influenced by sentiment, with U.S. policy developments and ongoing tariff negotiations continuing to cause periodic volatility. However, there is little

evidence of deterioration in the hard data to date. As such, we continue to anchor our positioning on underlying data rather than market narratives. Looking ahead, the combination of a structurally higher-for-longer interest rate environment and increasingly pro-growth policy backdrop presents selective opportunities. In the U.S., this favours highquality growth stocks, particularly within Technology, where strong balance sheets and long-term thematic tailwinds remain intact. In Canada, Financials, especially the relatively inexpensive banks, present a more compelling opportunity as earlier tailwinds from pullforward demand are beginning to wane. While we remain constructive, we are mindful of elevated equity valuations and continue to closely monitor macro conditions and policy developments for signs of inflection.

Downloadable Copy

Mark Warywoda, CFA

VP, Public InvestmentsIan Whiteside, CFA, MBA

AVP, Public InvestmentsJohanna Shaw, CFA

Director, Public InvestmentsJin Li

Director, Equity Investments

Wanyi Chen, CFA, FRM

Sr. Quantitative Analyst

Andrew Vermeer, CFA

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Edward Ng Cheng Hi

Analyst, Credit

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

-

Market Commentary October 2025

Key Takeaways

• Market sentiment improved significantly in Q3 as economic uncertainties eased.

• Both U.S. and Canadian stock markets posted strong gains. The rally was supported by sector-specific earnings strength and structural growth drivers in AI and digital infrastructure. Equity valuations remain elevated, which could become a potential headwind for future performance.

• Canadian bond markets delivered positive returns in Q3. Returns were largely from underlying interest income, supported by modestly lower interest rates and continued strong performance from tighter credit spreads.

• Both the Bank of Canada and the U.S. Federal Reserve restarted easing in Q3. Each central bank cut rates by 25 basis points in September, responding to rising risks to labour markets.

Economic and Market UpdateEconomic Summary: In the U.S., economic activity has remained relatively steady through 2025. However, while business investment remained robust, the pace of hiring slowed. Inflation has increased in recent months, but overall price pressures appear contained. Trade uncertainty eased in the third quarter as the U.S. reached agreements on tariffs with several key trading partners. Countries such as Japan, South Korea, and Indonesia, as well as the European Union, negotiated compromise deals. These deals typically involved U.S. tariffs in the range of 15% to 20% in exchange for market access or investment commitments. However, other nations faced higher tariffs of 30-50% following failed negotiations. Mexico and China are currently in a 90-day pause on tariff hikes, which will expire on October 29 and November 10, respectively. At its September meeting, the U.S. Federal Reserve (the “Fed”) lowered its policy rate by 25 basis points to a range of 4.00%– 4.25%. The Fed also signaled that additional interest rate cuts will likely be required to support the economy. Chair Jerome Powell highlighted increasing risks to the labour market and decreasing risks to inflation. He emphasized that the Fed remains data dependent and that interest rate decisions will be made “meeting-by-meeting”. The October 1 shutdown of the U.S. government added further uncertainty to the economic outlook. Key data releases are expected to be delayed, and the White House has warned of mass layoffs of federal workers.

The Canadian economy experienced a modest rebound in July following weak growth in the second quarter. However, U.S. tariffs and ongoing trade policy uncertainty continue to present risks to the economy. The labour market continues to weaken while inflationary pressures have eased in recent months. On July 31, the U.S. increased tariffs on Canadian imports from 25% to 35% for those products not exempted under USMCA. In addition, the U.S. has expanded its list of sector-specific tariffs. This is expected to place further strain on Canadian exporters. In response to these developments, the Bank of Canada cut its policy rate by 25 basis points to 2.50% during its September meeting. Governor Tiff Macklem indicated that the Bank is prepared to take further action if the balance of risks shifts to weaker growth.

Bond Markets: During Q3, the FTSE Canada Universe Bond Index returned 1.5%. Yields on Canadian bonds with maturities of 10 years or less declined. That reflected increased expectations for interest rate cuts by the Bank of Canada. Yields on bonds with maturities of greater than 10 years increased moderately, as investors continued to demand a higher risk premium for long-term debt.

Overall, corporate bonds saw a positive return for the quarter and outperformed government bonds. This outperformance was due to the higher interest rate on corporate bonds relative to government bonds, with an assist from modestly tighter credit spreads. Corporate issuance was robust during the quarter with strong investor demand, as investors were willing to look past U.S. tariffs and their potential impact to global growth. There were 99 corporate bond issuances during Q3 that combined to raise $45 billion for issuers, a new record. Indeed, the new issuance market is tracking ahead of last year, the previous high-water mark for issuance.

Notwithstanding the continued strong performance from corporate bonds, we have maintained a bias towards shorter corporate bonds where the risk and reward are better balanced. We remain ready to invest in longer corporate bonds as valuations become attractive.

Stock Markets: Equity markets posted strong gains in Q3. The S&P 500 returned 8.1% for the quarter, led by Information Technology and Communication Services. Investors focused on the expansion of AI infrastructure and a more favourable regulatory environment for blockchain technology. These themes supported risk appetite despite valuations remaining high relative to historical averages. The Canadian market returned 12.5% in Q3, outperforming the U.S. by more than 4%. This was driven mainly by strong returns in the Materials sector. Meanwhile, the Europe, Australasia, and Far East Index (EAFE) returned 5.4%, as international investors re-evaluated the “Sell America” trade trend.

U.S. Equities: In Q3, U.S. equities rose on strong momentum in AI infrastructure investment and growing interest in blockchain innovation. Mega-cap tech stocks led the rally. Major announcements such as NVIDIA’s $100 billion investment in OpenAI and Oracle’s $300 billion multi-year cloud deal highlighted the rapid growth of hyperscale data centers and the deepening commitment to AI development. A more supportive regulatory environment for blockchain technology also boosted investor interest in digital assets. This was reflected in robust IPO activity from crypto-focused companies such as Figure Technology and Gemini. Both stocks saw sharp gains following their public market debuts. That said, the S&P 500 continues to trade at nearly 23 times its forward earnings, roughly 20% above its 10-year average.

Canadian Equities: Canadian equities rose on better-than-expected economic data and sector-driven earnings, outperforming the U.S. by more than 4% in Q3. The Materials sector drove the rally, contributing nearly half of the gain for the TSX in Q3, as the price of gold surged past US$3850/oz (+45% YTD). The Technology sector also posted solid results, highlighted by Shopify’s continued strong performance. Shopify’s AI-driven product expansion and scalable digital commerce growth pushed the stock to trade around 85 times its forward earnings over the next twelve months. Positive sentiment extended to the Financials sector, where better-than-expected provisions for credit losses helped support a revaluation of bank stocks.

Overall, Q3 marked a risk-on environment across North American equities, underpinned by sector-specific earnings strength and structural growth drivers. In the U.S., enthusiasm around AI and digital infrastructure continued to dominate. In Canada, the rally was driven by surging gold prices and better-than-expected bank earnings. These catalysts helped sustain broad-based market strength across both markets.

Bottom line: Overall market sentiment improved in the third quarter following the volatility earlier in the year caused by tariffs. Investors benefited from resilient performance in North American equities and positive performance in fixed income. In the U.S., the Federal Reserve resumed its rate-cutting cycle, while strong consumer demand and continued capex-spending acted as key drivers for the market strength. In Canada, gold prices continued to surge amid persistent safe-haven demand driven by geopolitical risks. Looking ahead, we will continue to closely monitor valuation levels and underlying economic data for signals of inflection as the cycle progresses.

Downloadable Copy

Mark Warywoda, CFA

VP, Public InvestmentsIan Whiteside, CFA, MBA

AVP, Public InvestmentsJohanna Shaw, CFA

Director, Public InvestmentsJin Li

Director, Equity Investments

Wanyi Chen, CFA, FRM

Sr. Quantitative Analyst

Andrew Vermeer, CFA

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Edward Ng Cheng Hin

Analyst, Credit

Kate (Huyen) Vinh

Analyst, Equity

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy. - [pdf] Application for Fundserv Contract (segregated funds only) - Dealer and Advisor