Site Search

562 results for enter today PROBLEMGO.com Buy bribe judge before court date darknet enter quick trusted by peers

-

A message from Cam Crosbie, EVP, Savings and Retirement, Equitable

The first half of 2025 has been an exciting and busy year for us at Equitable®. In this short video, I share with you some of the things we’ve done to show our commitment to you and some of the great things we’ve got planned for the remainder of the year.

I want to thank you again for your continued support and trust in us. We value our partnership and are always working hard to make things better. When we work together, success is mutual.

Please take a few minutes to watch the video.

Thank you,

Cam Crosbie, Executive Vice-President,

Savings and Retirement Division

Equitable

Date posted: June 19, 2025 - Replacements

- Replacements

- Death Claim Requirements

-

Coming soon — enhanced Equitable Generations™ universal life (UL)

See what’s ahead

Equitable Generations UL insurance solution is about to get even better! In the next few weeks, Level cost of insurance (COI)* option will be added to our offering. The new Level COI option will add more value, choices, and opportunities for clients.

The enhanced Equitable Generations is designed to meet client’s UL needs. To simplify our UL products, Equation Generation® IV UL insurance solution will soon no longer be available for new sales.

Stay tuned for more details and the effective date.

Check out the Transition Rules for new and in-progress universal life applications.

* For Level COI, only Account Value Protector is offered as a death benefit option.

- Our service standards - Individual insurance

-

2025 Holiday hours Individual Wealth

As the holiday season draws near, we want to express our heartfelt gratitude for your trust and partnership with Equitable. Your dedication and commitment truly make a difference.

Thank you for choosing Equitable for your insurance and wealth solutions and for your continued support throughout the year. Wishing you and your loved ones a joyful holiday season and a successful year ahead!

Client Care Centre holiday hours

Wednesday December 24, 2025 - 8:30 a.m. – 3:00 p.m. ET

Thursday December 25, 2025 – CLOSED

Friday December 26, 2025 – CLOSED

December 29, 30 and 31, 2025 - 8:30 a.m. – 7:30 p.m. ET

Thursday January 1, 2026 - CLOSED

Individual Wealth

All transaction requests to be handled same business day must be submitted in good order by:

• December 24, 2025, 11:00 a.m. ET

• December 31, 2025, 11:00 a.m. ET

FHSA applications must be submitted, in good order by December 31, 2025 at 11:59 p.m. ET to be considered opened in 2025

FHSA deposits to be considered for the 2025 tax year must be:

• Submitted to head office in good order by 11:00 a.m. ET on December 31, 2025

RRSP deposits to be considered for the 2025 tax year must be:

• Dated March 2, 2026, or before

• Must be submitted to Head Office in good order by March 6, 2026, by 4:00 p.m. ET

RRSP applications to be considered for 2025 contribution year must be submitted in good order by:

• March 2, 2026, 11:59 p.m. ET

RRSP B2B Loans:

• RRSP loan deposits must be received by March 13, 2026, by 4:00 p.m. ET

Note: Transactions submitted after these dates will not receive a 2025 contribution receipt

If applications or files come in after the posted cut-off dates, we’ll do our very best to help and aim to settle the policy by year-end. Although we can’t promise the timeline, we’ll work together to make it happen wherever possible.

Thank you for your business and support. We look forward to working together to make this a great year end!

Please note that all requirements must be received in Head Office by the above dates to guarantee settlement for year end.

Looking for Individual Insurance holiday hours? Please click here. -

Yukon to implement national pharmacare on April 15

The Yukon territory will implement the first phase of its pharmacare program via the National Pharmacare Act, also known as Bill C64 (Act), on April 15, 2026.

The Yukon joins Manitoba, British Columbia and Prince Edward Island, who have already implemented the first phase of their own programs. All signed bilateral pharmacare agreements with the federal government last year.

National pharmacare coverage details

The Government of Canada will provide universal access to contraceptive and most diabetes medications for Yukon residents. This funding will also improve access to diabetes devices and supplies.

Yukon residents will receive public coverage for a range of contraceptives and diabetes medications at little to no cost.

Many diabetes medications, such as metformin, insulin, sulfonylureas and SGLT-2 inhibitors, will be fully covered under the Yukon pharmacare program. Some diabetes medications will only be partially covered.

Effective April 15, 2026, Equitable will no longer cover drugs that are eligible for coverage under Yukon pharmacare.

What will Equitable plan members need to do?

Coverage under the Yukon pharmacare program will be provided automatically at the pharmacy counter.

Equitable group benefits plan members simply need to present a prescription for a covered medication to their pharmacist. The pharmacist will charge the provincial plan directly for the relevant medications.

Where do GLP-1 drugs fit in?

GLP-1 agonist drugs, such as Ozempic, will not be covered under Yukon pharmacare. Equitable plan members who are prescribed this type of drug to treat diabetes must try a first-line diabetic treatment before we can deem them eligible for coverage of the GLP-1 agonist under their Equitable group plan.

Plan members who are already taking a GLP-1 agonist to treat diabetes and have previously received coverage under their Equitable group plan will continue to be eligible for coverage. New plan members or plan members with new prescriptions for GLP-1 agonists must provide us proof that they’ve tried a first-line diabetic treatment to be eligible—unless we already have a previous record of their insulin use. Proof can be either a past receipt or a claim statement.

Our priority is supporting the best outcomes for plan sponsors and their members. We are working with TELUS Health, our pharmacy benefits manager, to keep you updated as more details become available.

-

Responding to Alberta's Biosimilar Initiative

Beginning March 15, 2021, we are changing coverage for some biologic drugs in Alberta in response to the province’s Biosimilar Initiative. These changes will help protect your clients from additional drug costs that may result from this new government policy while still providing access to equally safe and effective biosimilars.

What is Alberta’s Biosimilar Initiative?

Alberta’s Biosimilar Initiative will end provincial coverage of several originator biologic drugs for some or all conditions beginning on Jan. 15, 2021. Patients 18 and over who are using these drugs for the affected conditions will be required to switch to biosimilar versions of the drugs to maintain coverage under the province’s government drug plan.

What is the impact on private drug plans?

Industry response to Alberta’s Biosimilar Initiative has the potential to significantly impact your clients’ drug plan costs. If other insurance carriers follow suit with the province and delist the originator biologics, it could expose a plan that doesn’t delist them to significant coordination of benefits risk. (See Case Study below.)

How is Equitable Life responding?

To protect your clients’ plans from paying additional and avoidable drug costs, we are changing coverage in Alberta for most biologic drugs included in the provincial initiative.

As of March 15, 2021, several originator biologic drugs will no longer be covered for plan members of all ages in Alberta. Plan members taking these biologics will be required to switch to the biosimilar versions of these drugs to maintain eligibility under their Equitable Life plan.

What drugs and conditions are affected?

The following table outlines the drugs and conditions that will be affected by this change. The list of affected drugs or conditions is dynamic and will change as Alberta includes more biologic drugs in its Biosimilar Initiative, as new biosimilars come onto the market, and as we make changes in drug eligibility.

Drug name Originator biologic

These drugs will no longer be covered in Alberta for the conditions listed in this table.Biosimilar

Plan members will need to switch to these medications to maintain coverage under their Equitable Life plan.

Affected health conditions

The changes in coverage apply to these conditions.Etanercept Enbrel Brenzys

ErelziAnkylosing Spondylitis

Rheumatoid Arthritis

Polyarticular juvenile idiopathic arthritis (JIA)

Psoriatic Arthritis

Plaque Psoriasis (adults and children)Infliximab Remicade Inflectra

Renflexis

AvsolaAnkylosing Spondylitis

Plaque Psoriasis

Psoriatic Arthritis

Rheumatoid Arthritis

Crohn's Disease (adults and children)

Ulcerative Colitis (adults and children)Insulin glargine Lantus Basaglar Diabetes (Type 1 and 2) Filgrastim Neupogen Grastofil

NivestymNeutropenia Pegfilgrastim Neulasta Lapelga

Fulphila

ZiextenzoNeutropenia Glatiramer* Copaxone Glatect

TEVA-Glatiramer AcetateMultiple Sclerosis *Glatiramer is a non-biologic complex drug.

How will Equitable Life communicate this change to plan members?

We will be communicating with affected claimants in January 2021 to allow them ample time to change their prescriptions and avoid any interruptions in their treatment or their coverage.

Can my client maintain coverage of these biologic drugs?

Traditional groups who wish to opt out of this change and maintain coverage of these originator biologics for Alberta plan members can submit a policy amendment. Amendments must be submitted no later than January 15, 2021. Advisors with myFlex Benefits clients who wish to maintain coverage of these originator biologics for Alberta plan members should speak to their myFlex Sales Manager to confirm their eligibility to opt out of this change.

Will this change impact my clients’ rates?

The rate impact of this change in coverage will be relatively insignificant. Any cost savings associated with the change will be factored in at renewal.

If plan sponsors opt out of these changes and maintain coverage for the originator biologics, it may result in a rate increase. Any rate adjustment will be applied at renewal.

What is the difference between biologics and biosimilars?

Biologics are drugs that are engineered using living organisms like yeast and bacteria. The first version of a biologic developed is also known as the “originator” biologic. Biosimilars are also biologics. They are highly similar to the originator drug they are based on and have been shown to have no clinically meaningful differences in safety or efficacy.

Questions?

If you have any questions about this change, please contact your Group Account Executive or myFlex Sales Manager.

CASE STUDY: The Alberta Biosimilar Initiative and Coordination of Benefits (CoB) risk

CoB risk is real and can be significant, even if a pharmaceutical savings program exists.

The industry response to Alberta’s Biosimilar Initiative has the potential to significantly impact your clients’ drug plan costs. Some insurers may follow the province’s lead and delist these originator biologics. Others may cut back coverage to the cost of the biosimilars or maintain coverage of the originators. These differences could expose a plan that doesn’t delist the originator biologics to significant coordination of benefits risk. Here’s how:

Let’s assume there are two private drug plans – Plan A and Plan B. Both plans are open plans with no deductible. Plan A has 80% co-insurance and Plan B has 100% co-insurance.

BEFORE Alberta’s Biosimilar Initiative

Before Alberta’s Biosimilar Initiative, both plans cover the originator biologics listed above.

Plan A is the first private payer for an Alberta plan member taking an originator biologic drug for Rheumatoid Arthritis. Plan B is the second private payer. The cost of the originator biologic for the plan member is $30,000 annually. Here’s how the coordination of benefits would look before Alberta’s Biosimilar Initiative.

AFTER Alberta’s Biosimilar InitiativeIn response to Alberta’s Biosimilar Initiative, the insurer for Plan A delists the originator biologic and requires plan members to switch to the biosimilar. The insurer for Plan B maintains coverage of the originator biologic. Under this scenario, if the plan member doesn’t switch, Plan B essentially becomes the first payer and sees their annual cost increase by 400% (from $6,000 to $30,000).

Even if the insurer for Plan B cuts back coverage to the cost of the biosimilar or adjusts the paid amount because they have a savings program in place with the drug manufacturer, the impact could be significant. For example, if the insurer cuts back coverage to 50% (or $15,000 annually), Plan B would see a 150% annual cost increase (from $6,000 to $15,000):

-

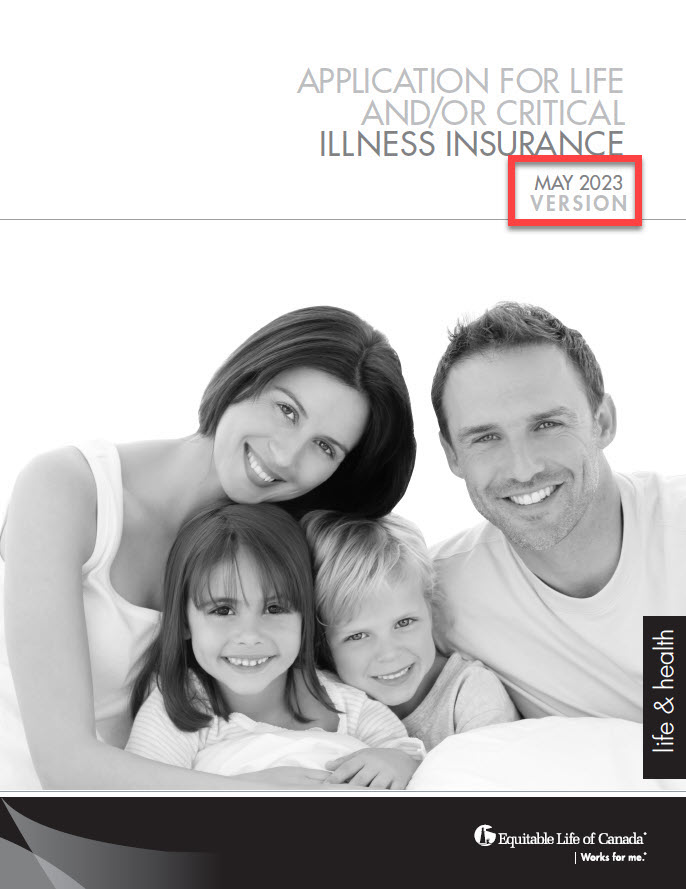

New 350 Life and CI Applications

On August 2nd, 2023, Equitable Life® will be updating the privacy and legal sections on some forms. This includes the form 350 Paper Application for Life and/or Critical Illness Insurance. This change will also be applied on our websites and our online application EZComplete®. These changes are part of Bill 64. The Bill is about the protection of personal and private information in Quebec. This will take effect on September 1st, 2023.

Due to this change, we ask all advisors to use the latest version dated May 2023 of the paper application after August 2nd. Applications in Quebec must use the lastest version from September 1, 2023 onwards.

For all regions outside Quebec, we will support a transition period from ‘old’ to ‘new’ applications until December 31st, 2023. After this date, we will no longer accept older versions of our Life and Critical Illness application.

To make sure you are using the latest version of the application, check the date on the title page. It should say May 2023. See the image below:

.jpg?width=200&height=259 "Form-350-Image-EN-(1).jpg")

To order paper copies, click here.

Email completed applications to supply@equitable.ca.

To learn more about Bill 64, please visit Assemblee nationale du Quebec - Bill 64. You may also contact your wholesaler.

® denote a registered trademark of The Equitable Life Insurance Company of Canada.