Site Search

536 results for see official MAKEMUR.com Buying a way to make criminal charges go away Cocos (Keeling) Islands

-

What’s your saving style?

A TFSA for its flexibility or an RRSP for tax-deferred growth.

Did you know? More than 65% of people who put money into a TFSA* earn less than $80,000 a year. That’s why TFSAs are popular with middle-income Canadians. They’re simple and flexible: you don’t get a tax break when you put money in, but you don’t pay tax when you take money out. This makes them great for people who don’t get big benefits from tax deductions.

On the other hand, 54% of RRSP contributors earn more than $80,000 per year*. RRSPs often work better for higher-income earners because contributions lower taxable income. That means bigger tax savings for people in higher tax brackets.

Here’s the good news: From January 1 to March 2, 2026, when clients open or add money to an Equitable TFSA or RRSP, they’ll be entered into Equitable’s Snowball Your Savings contest. Two winners will be chosen—and their advisors will celebrate too!

How to Enter

Advisors can help clients submit contributions through EZcomplete® or process transactions using EZtransact®. Every entry is a chance to win!

Want ideas to boost contributions and help Canadians save more? Connect with your Director, Investment Sales today.

* Source: advisor.ca/news/tfsas-more-popular-than-rrsps-in-2023/

® and ™ denote trademarks of The Equitable Life Insurance Company of Canada.

Equitable’s Snowball Your Savings contest: No purchase necessary. Contest period January 1, 2026 to March 2, 2026. Enter by making a deposit to an Equitable Tax-Free Savings Account or Registered Retirement Savings Plan during the contest period or by submitting a no-purchase entry. Two prizes of $5,000 CAD to be drawn on March 23, 2026 will be awarded. The servicing advisor for the contract to which the selected entrants made the deposit is also an eligible winner and will receive a $1,000 CAD prize. For example, if an Equitable client is a winner of the $5,000 prize, the client’s servicing advisor for the relevant contract wins a $1,000 prize. Open to legal residents of Canada of the age of majority. Odds of winning depend on number of eligible entries received during the Contest Period. For full contest rules, including no-purchase method of entry, see the full contest rules. -

Equitable celebrates FundGrade A+ awards, reinforces commitment to Canadian investors

Equitable® has been recognized with two FundGrade A+® awards, an annual distinction that recognizes exceptional performance among Canadian investment funds.

The award-winning funds are available on the new Equitable Guaranteed Investment FundsTM solution:

Equitable Invesco NASDAQ 100 ESG Index ETF

Equitable Fidelity® Global Innovators

“We’re honoured to receive this recognition,” says Cam Crosbie, Executive Vice-President, Individual Wealth. “These awards reflect the hard work of many teams across our organization and, of course, our partners.”

Looking ahead, Equitable Individual Wealth remains focused on continuous improvement and innovation. “This is just the beginning,” adds Crosbie. “We deeply value the trust advisors and clients place in us every day, and we’re committed to helping Canadians reach their financial goals with more confidence.”

FundGrade A+® is used with permission from Fundata Canada Inc., all rights reserved. The annual FundGrade A+® Awards are presented by Fundata Canada Inc. to recognize the “best of the best” among Canadian investment funds. The FundGrade A+® calculation is supplemental to the monthly FundGrade ratings and is calculated at the end of each calendar year. The FundGrade rating system evaluates funds based on their risk-adjusted performance, measured by Sharpe Ratio, Sortino Ratio, and Information Ratio. The score for each ratio is calculated individually, covering all time periods from 2 to 10 years. The scores are then weighted equally in calculating a monthly FundGrade. The top 10% of funds earn an A Grade; the next 20% of funds earn a B Grade; the next 40% of funds earn a C Grade; the next 20% of funds receive a D Grade; and the lowest 10% of funds receive an E Grade. To be eligible, a fund must have received a FundGrade rating every month in the previous year. The FundGrade A+® uses a GPA-style calculation, where each monthly FundGrade from “A” to “E” receives a score from 4 to 0, respectively. A fund’s average score for the year determines its GPA. Any fund with a GPA of 3.5 or greater is awarded a FundGrade A+® Award. For more information, see www.FundGradeAwards.com. Although Fundata makes every effort to ensure the accuracy and reliability of the data contained herein, the accuracy is not guaranteed by Fundata.

Equitable and Equitable Guaranteed Investment Funds are trademarks of The Equitable Life Insurance Company of Canada. -

Universal life (UL) enhanced – more options to reach more clients

Great News!

Explore the latest enhancements to Equitable Generations™ UL insurance, offering clients greater flexibility to meet their needs.

What’s new for Equitable Generations UL:

• Level cost of insurance (COI) option.* Available for new sales to offer even more choice for clients. Here is how these rates compare to Equation Generation IV Level COI:

• Non-smoker rates have decreased on average by 4% across all ages and bands (Smoker rates have increased on average by 1%).

• New rate bands. $1M and $5M for Level COI**, making our UL solution more attractive to a wide range of clients. * For Level COI, only Account Value Protector is offered as a death benefit option.

**The rate bands for Level COI are $25,000, $100,000, $250,000, $500,000, $1 million and $5 million. The rate bands for YRT remain $25,000, $50,000, $100,000, $250,000 and $500,000.

These enhancements offer a more competitive solution to grow your UL business. See for yourself – run a quote today!

Equation Generation® IV UL is retired. Equation Generation IV is no longer being offered for new sales effective March 21, 2026.

We now have the essential UL features in one powerful solution, Equitable Generations UL.

Video available French and Chinese.

Please refer to the Transition Rules for all the details on processing your applications.

Visit our splash page for full product details

More reasons to choose Equitable® for your UL business

• Wide range of investment choices through some of Canada’s most prominent fund managers (including sustainable investment options).

• We are the only UL carrier to offer target-date investment options.

• Guaranteed Investment Bonus. An annual rate of 0.75% is added to the policy’s account value starting in year 1.

• No policy administration fees. No Linked Interest Option (LIO) administration fees (except for LIOs that track indices).

• Caring claim support through our KINDTM program.

Need more information? Please contact your Equitable wholesaler.

03/23/26 -

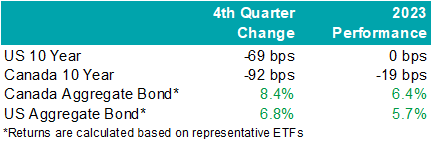

EAMG Market Commentary January 2024

Rates & Credit – Interest rates decreased sharply in Q4 as the market priced in aggressive interest rate cuts by central banks in 2024. The prospect of lower interest rates also drove a strong risk-on tone to the market, with the risk premium on corporate bonds grinding tighter as prospects for a “soft landing” improved. The rally in interest rates resulted in the best quarter for bonds over the past 15 years, with the FTSE Canada Universe Index returning 8.3%. Corporate bonds modestly underperformed the Universe Index with a return of 7.3%. The lower return for corporate bonds was primarily driven by the fact that the corporate bond index is less sensitive to interest rate movements (as compared to the government index), partially offset by the risk-on tone to the market. Within corporate bonds, lower-rated BBBs outperformed higher-rated A bonds. Industries with higher interest rate exposure such as infrastructure, energy, and communications outperformed those with less exposure (notably financials and securitization), consistent with the overall shift in the yield curve.

.png "image1-(1).png")

Santa Came to Town – Moving in sync with bonds, global equities jolted higher into the end of the year with cooling inflation data and dovish comments from central bankers. The U.S. market outperformed most regions last quarter with the S&P 500 returning 11.7% in USD terms, bringing the total return in 2023 to 26.3%. The TSX added 8.1% in Q4, boosting the total annual return to 11.8%. Meanwhile, major developed economies from Europe, Australasia, and the Far East (EAFE) gained 5.0% in local currency terms over the quarter, helping the region produce a 16.8% return from the year prior. Prospects of interest rate cuts by the Federal Reserve saw the Loonie rally into year-end and resultantly, investors of Canadian dollar securities witnessed enhanced returns. Strong domestic U.S. economic data helped value pockets of the market outperform. That said, this was not a synchronized trend as China’s economic disappointment weighed on the performance of EAFE.

U.S. Fundamentals – Our work shows that investors are shifting their focus away from operating margins and towards the ability to sustain debt levels ahead of renewing debt obligations. Corporate earnings beat modest expectations last quarter, contracting by less-than-expected on a year-over-year basis. Resilient operating margins continue to attract investors into equities. After three consecutive quarters of improving forward earnings guidance, we observed that the number of major companies expecting deteriorating financial performance grew to ~35%. We note that this is a sharp contrast relative to the optimistic run-up in equity valuations. In general, corporate pessimism has been underpinned by concerns for the health of the consumer, increasing wage pressures, and inflation.

U.S. Quant Factors – While mega-cap technology stocks gave back some ground in the second half, crowding into the magnificent 7 remains noticeable with the cap weighted S&P 500 outperforming the equal weighted index by 12.5% last year. That said, value areas of the market – which underperformed through the first three quarters of the year – were top performing companies last quarter as the prospects for an economic “soft-landing” improved with U.S. inflation continuing to ease without substantial deteriorations of employment or output data. Quality-growth businesses initially outperformed as the higher-for-longer narrative continued to drive investors toward large cash-rich companies with stable margins. That said, this basket of companies gave back relative returns into quarter-end as weakness in operating margins persisted, making fundamentals appear stretched. Low volatility stocks (i.e. stocks with lower sensitivity to broad market movement and lower price volatility) rallied to start the quarter before dovish comments from central bankers improved risk-sentiment and ultimately pushed this basket lower on a relative basis. Lastly, dividend growth companies, which include businesses with a lengthy and established history of increasing dividends, underperformed the broader index as market participants punished businesses that slowed capital growth projects during the rising interest rate environment. While operating margins have declined, the basket’s strong cash flow and low debt burden may be advantageous if the market’s anticipation of impending interest rate cuts proves to be incorrect or mistimed.

Canadian Fundamentals – Although Canadian companies exceeded bleak forecasts last quarter, earnings continue to contract on a year-over-year basis. Return on equity (ROE) – a gauge of how efficiently a corporation generates profits – continued to decline last quarter while corporate costs of capital remain elevated. In essence, Canadian companies are generating less value relative to their financing cost. Value creation underpins the sustainability of dividend payments, which are a unique and desirable attribute of the Canadian market. Meanwhile, the Bank of Canada held its overnight interest rate unchanged with market participants forecasting a higher probability of interest rate cuts in 2024. On the expectations of easing monetary conditions, dividend yields compressed while earnings forecasts improved with analysts predicting that index aggregate earnings will grow 6% to 8% in 2024. At a sector level, the energy industry’s financial performance normalized – in line with expectations – as weakening oil demand expectations overshadowed geopolitical conflict in the Middle East, ultimately pushing crude prices ~21% lower last quarter. The industrials and financials sectors beat expectations, helping offset softer-than-expected results from the consumer staples and technology sectors.

Canadian Quant Factors – The Canadian banks underperformed for most of the year as they reported increasing provisions for nonperforming loans, reflecting forecasts of worsening economic conditions. That said, expectations of interest rate cuts in 2024 helped tame recession fears and eased concerns of slowing loan growth, propelling banks higher in the fourth quarter as they appeared more stable and therefore favourable than prior estimates. The high-quality basket underperformed last quarter as improving risk sentiment in the market reduced the attractiveness of secure companies with lower earnings variability. Furthermore, high dividend payers with solid growth prospects outperformed in the fourth quarter as market participants rewarded companies that demonstrated a strong ability to support future dividends and punished high yielding businesses with less certain financial capabilities.

Views From the Frontline Rates – Interest rates declined sharply in Q4 as inflation continued to trend lower, fears of excess bond supply declined, and the Federal Open Market Committee signaled that the next change to their overnight policy interest rate would likely be lower. Labour market and consumer spending data remain resilient however businesses have indicated slowing across industries, more price-sensitive consumers, rising delinquencies, and concerns about the high cost of debt. Central banks remain committed to achieving their 2% inflation target and most acknowledge that interest rates have likely peaked.

Credit – The risk premium for corporate bonds (versus government bonds) tightened materially over the quarter, with a strong risk on tone to the market as investors priced in lower interest rates in 2024 and a “soft-landing” to economic concerns. Corporate bond supply was well received by the market. On the balance, we do not think the current risk premium adequately compensates for downside risk, and as such, we remain cautious on corporate bonds and have a bias towards higher-quality, shorter-dated credit where we view the risk / reward dynamic as being more favourable.

Equity – In the U.S., we allocated exposure to value names which outperformed over the quarter as the macroeconomic outlook improved on the backdrop of rate cut expectations. Looking forward, we expect that margins will continue to normalize as Covid-induced pent up demand fades. While we do not forecast margins to compress at an alarming rate, we believe sticky wage and input costs will continue to pressure businesses while consumers exhibit further exhaustion. As such, we are shifting our focus toward the balance between company reinvestment in capital projects and upcoming debt refinancing requirements. In line with this view, we favour businesses with stable cash flows and decreased debt loads as we believe they present an attractive contrarian opportunity if soft-landing projections prove to be overstated. Within Canada, we remain attentive to the inverse movements of ROE relative to financing costs over 2023. With the excess between ROE and financing costs compressing, businesses’ ability to create value appears more stretched than earlier in 2023. Therefore, we continue to favour high quality companies in Canada, which is typically defined by high ROE, stable earnings variability, and low financial leverage. Geographically, the U.S. economy appears to be in healthier condition with inflation easing while employment and output data remain stable and hence, our focus will be on capital expenditures. EAFE – which is generally more economically linked to China than North America – contains a large bucket of stable, high-quality businesses that may benefit from any upside economic surprises out of China. Lastly, through the lens of a Canadian investor, the Loonie’s relative value versus other major currencies presents another resource in our investment mandate to derive excess return.Downloadable Copy

Mark Warywoda, CFA

VP, Public Portfolio ManagementIan Whiteside, CFA, MBA

AVP, Public Portfolio ManagementJohanna Shaw, CFA

Director, Portfolio ManagementJin Li

Director, Equity Portfolio Management

Tyler Farrow, CFA

Senior Analyst, Equity

Andrew Vermeer

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

ADVISOR USE ONLY

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

- Path to Success Module 5

-

Update - Travel Assist Coverage*

Last Friday, we announced that plan members with Travel Assist on their benefits plan will not be eligible for coverage if they departed the country after the Government of Canada issued its Global Travel Advisory.

When the Government issued its advisory late Friday afternoon, we felt an obligation to let prospective travellers know as soon as possible so they could make informed choices about their travel. Since then, we have been made aware of a number of situations where plan members were unable to change their travel plans and need our continued support.

To provide that support, we have revised our position. We will continue to cover plan members for all eligible emergency medical expenses, including those related to COVID-19, for trips outside Canada. Given the global situation is evolving quickly, we will continue to monitor developments and update you accordingly.

In spite of this, we strongly urge your clients to advise their employees not to travel outside of the country at this time. The risk is high and the options for returning to Canada are becoming limited. Further, we urge your clients to advise their employees who are outside the country to return to Canada earlier than scheduled, if possible.

If a plan member is currently travelling abroad and is experiencing symptoms or is hospitalized with suspicion of the coronavirus, they should contact Travel Assist at the numbers listed below for assistance and to confirm their coverage.

- Toll-free Canada/USA: 1.800.321.9998

- Global call collect: 519.742.3287

- Allianz Global Assistance ID #9089

We will continue to update you as the situation develops.

We will update the announcement on our Plan Member website to reflect this change.

We apologize for any confusion or inconvenience our earlier announcement may have caused.

*Indicates content that will be shared with your clients

-

Excelerator Deposit Option – maximum payment limit changes

The Excelerator Deposit Option (EDO) gives your client the option to make additional payments, subject to specified limits and our current administrative rules and guidelines, above the required guaranteed policy premium. EDO payments can help grow the long-term values in your client’s policy. This change is regarding the maximum EDO payment limit that applies to the policy.

● NEW! If a request is received to terminate, convert, or reduce the term rider and the term rider has been in effect for 10 years or longer, the EDO maximum for the policy will not be reduced.

For Equimax policies with an Owner Signature Date of June 26, 2021 or after where a term rider has increased the maximum EDO payment limit on the policy

● If a request is received to terminate, convert, or reduce the term rider and the term rider has been in effect for less than 10 years (it has not reached the 10th policy anniversary), the EDO maximum for the policy will be reduced accordingly.

Current rules as to when underwriting is required for EDO payments continue to apply, as do current rules surrounding acceptance of EDO payments and maintaining the tax-exempt status of the policy and can be found in the Equimax Product Admin Guide.

Want more information? Contact your Regional Sales Manager for more information on these changes

-

Enhancements to ID Verification and Business Forms

We have made enhancements to some of our forms and created an additional form to help make it easier for you to do business with Equitable Life®.

The first enhancement is an update to the ID Verification section to allow for Third Party ID Verification when a client doesn’t want to provide ID documents to an Advisor. They are now given additional options to either use the Alternative Identification requirements, or consent to Equitable Life verifying their identity through a third party service provider. We’ve also clarified in the Advisor declaration that they can’t sign for their own policies as they aren’t able to validate their own ID.

The above changes have been made to the following forms:- 671OC – Ownership Change Form

- 1027 – Additional/Updated Customer Information

- 1616 – Application for Term Conversion

The second enhancement is an update to Business forms. We’ve created a new form, 2004 Signing Authorities Certificate, to help Businesses provide the Signing Authority information needed more easily! Forms 594 and 682ENT have been updated to point to the new Form 2004 and also have new “Ownership structure” requirements added in section 2.

View the below forms for details on these changes:- 2004 – Signing Authorities Certificate (NEW)

- 594 – Business Information Form

- 682ENT – Claimants’ Statement for Entities

® denotes a registered trademark of The Equitable Life Insurance Company of Canada.

-

Increased auto approval means more time to focus on your complex cases

As the year draws to a close, we are pleased to reflect back on our many enhancements geared toward improving our auto-approval rates and the notable impact they have made on our service standards.

Throughout 2021, we have invested significantly in our services and technology, including data & analytics to ensure that more of our new business applications are approved automatically without any intervention, leaving our teams available to engage in settling your complex cases. As a result of these enhancements, over the past 3 months we have improved from 8% of our new business flowing straight through to approval, to an impressive 25% of cases requiring no underwriting*.

There are a number of factors that contribute to this straight through approval success in processing applications, such as simpler cases, applicants with no medical history or medical issues, younger applicants and applications for lower face amounts. These factors, alongside our ongoing efforts to fortify our processes, has resulted in positive feedback from the field.

Advisors have mentioned you’ve felt the impact on our speed and service, and we will continue forward into 2022 with this positive momentum, with further enhancements to help make it easier for you to do business with Equitable Life.

*As of December 2021 -

The value of Equitable Life’s EZcomplete online application for Pivotal Select

Necessity is the mother of invention. And COVID-19 has taken Equitable Life’s® EZcomplete® online application to the next level. Prior to the pandemic, EZcomplete was touted as being convenient and easy to use. Well, it is. But now…it is so much more.

Whether secure in an office or safe at home, EZcomplete’s non face-to-face capabilities include an alternative to physical verification. EZcomplete simply requires verification of ID using a third-party service provider. The third-party service provider completes the verification behind the scenes using information that was already required to complete an application. By removing the physical ID requirements, the ID verification process has been automated and simplified.

EZcomplete’s electronic signature functionality is also easy and secure. To enable a remote signature, your client just provides an e-mail address. Your client will receive a link and security code that you provide. The client enters the code, reviews the application and e-signs the documents.

Step by step directions ensure you have the right details without any confusing or unnecessary questions. Highlighted fields alert you to any missing information, eliminating any extra work or effort. The immediate processing also helps make it an attractive resource.

Whether selling segregated funds face to face or from the comfort of home, Equitable Life’s EZcomplete online application and Pivotal Select™ segregated fund line up provide the solution for even the most rattled and weary investor. Learn more, visit EquiNet or contact your Regional Investment Sales Manager.