Site Search

795 results for check site now MAKEMUR.COM Buying early release from jail with payment plans

-

EAMG Market Commentary July 2024

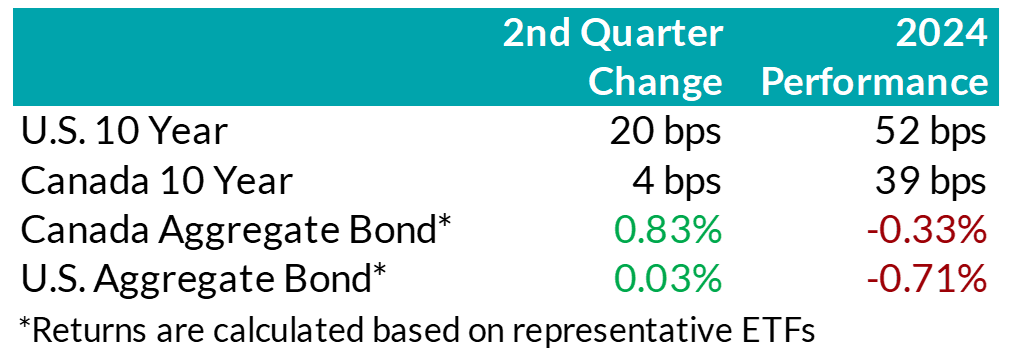

.png "Picture1-(3).png") Rates & Credit – In Q2 2024, U.S. inflation and economic growth data was mixed, leading to moderately higher interest rates in the U.S. Meanwhile, in Canada, long-end interest rates were little changed during the quarter, but short-term interest rates fell. That was due to the weaker economic outlook, as well as the Bank of Canada’s decision to reduce its overnight interest rate in June, with anticipation of further monetary policy easing to come. Canadian corporate bonds returned 1.1%, outperforming the 0.8% return of government bonds as well as the 0.9% return for the overall FTSE Canada Universe Bond index. Shorter-dated bonds outperformed longer-dated bonds. Within corporate bonds, lower-rated BBBs outperformed higher-rated A bonds, while industries that have shorter-dated debt (e.g. real estate and financials) outperformed those that tend to have longer-dated debt (e.g. communications and infrastructure).

Rates & Credit – In Q2 2024, U.S. inflation and economic growth data was mixed, leading to moderately higher interest rates in the U.S. Meanwhile, in Canada, long-end interest rates were little changed during the quarter, but short-term interest rates fell. That was due to the weaker economic outlook, as well as the Bank of Canada’s decision to reduce its overnight interest rate in June, with anticipation of further monetary policy easing to come. Canadian corporate bonds returned 1.1%, outperforming the 0.8% return of government bonds as well as the 0.9% return for the overall FTSE Canada Universe Bond index. Shorter-dated bonds outperformed longer-dated bonds. Within corporate bonds, lower-rated BBBs outperformed higher-rated A bonds, while industries that have shorter-dated debt (e.g. real estate and financials) outperformed those that tend to have longer-dated debt (e.g. communications and infrastructure).

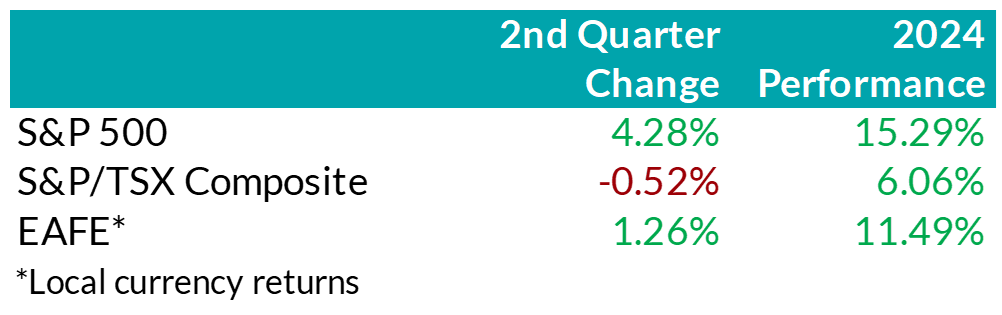

.png "Picture2-(2).png") Equity Overview – Against the backdrop of volatile inflation data and a lack of indication from the Federal Reserve that it was prepared to start cutting interest rates yet, U.S. equity markets decoupled from other regions. Crowding into AI-focused, mega-cap names accelerated in Q2. More specifically, investors defaulted toward the Magnificent 7 to navigate the current period, overlooking broadening earnings breadth and less expensive valuations from the remaining S&P 493. Outside the U.S., equity returns were generally mundane in dollar terms. That said, emerging markets proved to be a bright spot for investors seeking value, as the rebound in heavily discounted Chinese equities helped push frontier markets higher.

Equity Overview – Against the backdrop of volatile inflation data and a lack of indication from the Federal Reserve that it was prepared to start cutting interest rates yet, U.S. equity markets decoupled from other regions. Crowding into AI-focused, mega-cap names accelerated in Q2. More specifically, investors defaulted toward the Magnificent 7 to navigate the current period, overlooking broadening earnings breadth and less expensive valuations from the remaining S&P 493. Outside the U.S., equity returns were generally mundane in dollar terms. That said, emerging markets proved to be a bright spot for investors seeking value, as the rebound in heavily discounted Chinese equities helped push frontier markets higher.

U.S. Fundamentals – Corporate earnings continued to surpass expectations last quarter with stable operating margins helping businesses report better-than-expected bottom line results. Investors remain focused on the ability of companies to sustain debt levels ahead of renewing debt obligations, rewarding businesses with a strong ability to generate stable cash flows. Moreover, while prior quarters have witnessed earnings growth that was largely driven by highly profitable mega-cap technology stocks, U.S. markets are witnessing a broadening trend in earnings strength, with previously stunted segments of the market recovering. Our work shows that members of the Russell 1000 index, excluding the Magnificent 7, posted a median earnings growth of about 6% last quarter, with nearly 60% of companies increasing earnings versus the year prior. Furthermore, we observed an increase in the number of major companies that expect improving financial performance to approximately 27%, suggesting that the recovery in earnings breadth may persist.

U.S. Quant Factors – As mentioned, concentration in the equity market drove a surge in valuations as investors continued to chase specific mega-cap technology stocks. In fact, within the Russell 1000 growth factor – which screens for companies whose earnings are expected to grow at an above-average rate relative to the market – the Magnificent 7 totaled nearly 55% of the entire index by quarter-end. In addition, the Nasdaq 100 – which is generally viewed as a technology-biased index – saw the weight of the Magnificent 7 rise to almost 43% of the entire index by the end of the quarter. Furthermore, the equal-weighted S&P 500 underperformed the cap-weighted index by nearly 7% last quarter, bringing the year-to-date divergence to about 10%. With concentration accelerating, the cap-weighted index outperformance has soared past Covid-era levels, a period that saw investors rapidly crowd into profitable technology names due to panic and economic uncertainty. We remain cautious of a severely crowded market that trades near all-time highs as strong performance from 5-7 names distorts the overall stature of market conditions.

Canadian Fundamentals – Although Canadian companies exceeded bleak forecasts, earnings continue to contract on a year-over-year basis. Furthermore, earnings revisions have grinded lower with easing monetary conditions unable to offset concerns of a slowing economic environment. We note the sharp contrast versus the U.S. as the bifurcation of earnings performance widens. The CRB Raw Industrials Index, a measure of price changes of basic commodities, broke out of recent ranges as metals rallied higher despite a stronger U.S. dollar and elevated interest rates. The mining industry benefited from a sustained elevation in prices, helping the materials sector outperform over the quarter. Returns from the heavily-weighted Canadian banks were constrained last quarter with company-specific drivers – including regulatory challenges from TD, and underwhelming U.S. results from BMO – limiting performance. More broadly, the banks continue to build prudent credit provisions to mitigate uncertain economic forecasts and remain well capitalized.

Canadian Quant Factors – With investors remaining attentive to businesses’ ability to create value relative to financing costs, we see value in high quality, dividend-paying companies with strong earnings sustainability and a healthy degree of leverage. Based on our work, investors of the Canadian banks appear well compensated, with the current premium between value creation and current yield remaining compressed. In our opinion, the market has modest expectations regarding prospects for value generation from the banks and, therefore, we believe the industry stands to benefit if the premium reverts closer to historical norms. We also continue to see sources of quality dividend opportunities within certain areas of the energy sector. More specifically, we believe companies that have taken steps to improve their balance sheets through deleveraging efforts, and with improved operating leverage, offer attractive prospects given their stable and high-yielding composition.

Views From the Frontline

Rates – During the first half of the second quarter, interest rates in both Canada and the U.S. increased, continuing the upward momentum from Q1. Higher-than-expected inflation data in the U.S. along with mixed economic growth data caused investors to push out expectations for when the U.S. Federal Reserve would start lowering its interest rate. This trend shifted in the second half of Q2, as positive economic momentum slowed in the U.S. economy and inflation data began to soften. Interest rates in Canada declined more rapidly than in the U.S. due to more benign inflation, a weaker job market, and economic growth remaining below population growth. This economic weakening provided the confidence required for the Bank of Canada to cut rates by 25 basis points in June to 4.75%. The Bank also signaled that if inflation continues to ease and the Bank’s confidence grows that inflation would continue to trend toward its 2% inflation target, it is reasonable to expect further cuts. The second quarter marked a pivotal point for the global policy easing cycle. Sweden, Canada, and the European Central Bank all began lowering their policy rates, and Switzerland made a second rate cut, following one in Q1. The market continues to speculate on the timing of the U.S. Federal Reserve’s first rate cut. Interest rate cut expectations are largely unchanged in Canada since last quarter, with a total of three rate cuts expected throughout 2024. Expectations for the rate cuts by the U.S. Federal Reserve declined slightly, however, to two cuts in 2024.

Credit – The risk premium for corporate bonds (versus government bonds) was largely flat over the quarter, with spreads approaching the tight post-pandemic levels experienced in 2021. Corporate bond supply continues to be very robust, with $41bn in new issuance. Year-to-date, corporate issuance has set a new record, with an impressive $80bn in issuance. On balance, we do not think the current risk premium adequately compensates for downside risk, particularly in longer-dated corporate bonds, and have a bias towards shorter-dated credit where we view the risk / reward trade-off as being more favourable.

Equity – On the backdrop of a heavily concentrated U.S. market rally, we remain cautious of the distortion to market returns from high-flying technology stocks. As a result, we continue to favour a combination of the Dow Jones Industrial Average and the S&P 500 for our broad U.S. market exposure. The Dow provides a more diversified exposure to 30 prominent large-cap companies and less concentration in technology relative to the S&P. Broadening earnings strength presents an opportunity for previously out-of-favour names to “catch-up”. In our view, companies outside the Magnificent 7 that have demonstrated robust earnings growth, strong cash flow generation, along with decreased debt loads, are well-positioned to benefit from internal market rotations. As such, we gain exposure to these companies through the quality factor – companies with higher return-on-equity, strong operating performance, and healthy leverage levels – and the dividend growth factor – businesses with a lengthy and established history of increasing dividends.

In Canada, we remain attentive to how efficiently corporations are generating profits relative to financing costs. Looking forward, we continue to monitor the ability of businesses to generate profits given a decline in capital spending. More specifically, we are focused on businesses’ ability to grow and sustain dividends amid the lag between easing monetary conditions and consumption. Due to this, we observe value in higher yielding companies that are higher on the spectrum of quality. Geographically, we maintain our overweight U.S. exposure, underpinned by encouraging U.S. inflation data trends, broadening corporate earnings growth, and normalizing consumption. In addition, sluggish Chinese data and the lack of positive earnings revisions from EAFE tilt the risk-adjusted return profile in favour of the U.S. Lastly, as a Canadian investor, fluctuations in the Loonie’s relative value versus other major currencies continues to present tactical trading opportunities within our investment mandate.

Downloadable Copy

Mark Warywoda, CFA

VP, Public Portfolio ManagementIan Whiteside, CFA, MBA

AVP, Public Portfolio ManagementJohanna Shaw, CFA

Director, Portfolio ManagementJin Li

Director, Equity Portfolio Management

Tyler Farrow, CFA

Senior Analyst, Equity

Andrew Vermeer

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

-

EAMG Market Commentary January 2024

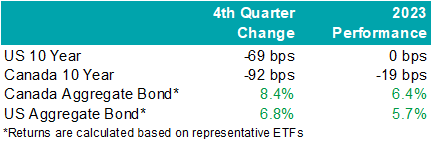

Rates & Credit – Interest rates decreased sharply in Q4 as the market priced in aggressive interest rate cuts by central banks in 2024. The prospect of lower interest rates also drove a strong risk-on tone to the market, with the risk premium on corporate bonds grinding tighter as prospects for a “soft landing” improved. The rally in interest rates resulted in the best quarter for bonds over the past 15 years, with the FTSE Canada Universe Index returning 8.3%. Corporate bonds modestly underperformed the Universe Index with a return of 7.3%. The lower return for corporate bonds was primarily driven by the fact that the corporate bond index is less sensitive to interest rate movements (as compared to the government index), partially offset by the risk-on tone to the market. Within corporate bonds, lower-rated BBBs outperformed higher-rated A bonds. Industries with higher interest rate exposure such as infrastructure, energy, and communications outperformed those with less exposure (notably financials and securitization), consistent with the overall shift in the yield curve.

.png "image1-(1).png")

Santa Came to Town – Moving in sync with bonds, global equities jolted higher into the end of the year with cooling inflation data and dovish comments from central bankers. The U.S. market outperformed most regions last quarter with the S&P 500 returning 11.7% in USD terms, bringing the total return in 2023 to 26.3%. The TSX added 8.1% in Q4, boosting the total annual return to 11.8%. Meanwhile, major developed economies from Europe, Australasia, and the Far East (EAFE) gained 5.0% in local currency terms over the quarter, helping the region produce a 16.8% return from the year prior. Prospects of interest rate cuts by the Federal Reserve saw the Loonie rally into year-end and resultantly, investors of Canadian dollar securities witnessed enhanced returns. Strong domestic U.S. economic data helped value pockets of the market outperform. That said, this was not a synchronized trend as China’s economic disappointment weighed on the performance of EAFE.

U.S. Fundamentals – Our work shows that investors are shifting their focus away from operating margins and towards the ability to sustain debt levels ahead of renewing debt obligations. Corporate earnings beat modest expectations last quarter, contracting by less-than-expected on a year-over-year basis. Resilient operating margins continue to attract investors into equities. After three consecutive quarters of improving forward earnings guidance, we observed that the number of major companies expecting deteriorating financial performance grew to ~35%. We note that this is a sharp contrast relative to the optimistic run-up in equity valuations. In general, corporate pessimism has been underpinned by concerns for the health of the consumer, increasing wage pressures, and inflation.

U.S. Quant Factors – While mega-cap technology stocks gave back some ground in the second half, crowding into the magnificent 7 remains noticeable with the cap weighted S&P 500 outperforming the equal weighted index by 12.5% last year. That said, value areas of the market – which underperformed through the first three quarters of the year – were top performing companies last quarter as the prospects for an economic “soft-landing” improved with U.S. inflation continuing to ease without substantial deteriorations of employment or output data. Quality-growth businesses initially outperformed as the higher-for-longer narrative continued to drive investors toward large cash-rich companies with stable margins. That said, this basket of companies gave back relative returns into quarter-end as weakness in operating margins persisted, making fundamentals appear stretched. Low volatility stocks (i.e. stocks with lower sensitivity to broad market movement and lower price volatility) rallied to start the quarter before dovish comments from central bankers improved risk-sentiment and ultimately pushed this basket lower on a relative basis. Lastly, dividend growth companies, which include businesses with a lengthy and established history of increasing dividends, underperformed the broader index as market participants punished businesses that slowed capital growth projects during the rising interest rate environment. While operating margins have declined, the basket’s strong cash flow and low debt burden may be advantageous if the market’s anticipation of impending interest rate cuts proves to be incorrect or mistimed.

Canadian Fundamentals – Although Canadian companies exceeded bleak forecasts last quarter, earnings continue to contract on a year-over-year basis. Return on equity (ROE) – a gauge of how efficiently a corporation generates profits – continued to decline last quarter while corporate costs of capital remain elevated. In essence, Canadian companies are generating less value relative to their financing cost. Value creation underpins the sustainability of dividend payments, which are a unique and desirable attribute of the Canadian market. Meanwhile, the Bank of Canada held its overnight interest rate unchanged with market participants forecasting a higher probability of interest rate cuts in 2024. On the expectations of easing monetary conditions, dividend yields compressed while earnings forecasts improved with analysts predicting that index aggregate earnings will grow 6% to 8% in 2024. At a sector level, the energy industry’s financial performance normalized – in line with expectations – as weakening oil demand expectations overshadowed geopolitical conflict in the Middle East, ultimately pushing crude prices ~21% lower last quarter. The industrials and financials sectors beat expectations, helping offset softer-than-expected results from the consumer staples and technology sectors.

Canadian Quant Factors – The Canadian banks underperformed for most of the year as they reported increasing provisions for nonperforming loans, reflecting forecasts of worsening economic conditions. That said, expectations of interest rate cuts in 2024 helped tame recession fears and eased concerns of slowing loan growth, propelling banks higher in the fourth quarter as they appeared more stable and therefore favourable than prior estimates. The high-quality basket underperformed last quarter as improving risk sentiment in the market reduced the attractiveness of secure companies with lower earnings variability. Furthermore, high dividend payers with solid growth prospects outperformed in the fourth quarter as market participants rewarded companies that demonstrated a strong ability to support future dividends and punished high yielding businesses with less certain financial capabilities.

Views From the Frontline Rates – Interest rates declined sharply in Q4 as inflation continued to trend lower, fears of excess bond supply declined, and the Federal Open Market Committee signaled that the next change to their overnight policy interest rate would likely be lower. Labour market and consumer spending data remain resilient however businesses have indicated slowing across industries, more price-sensitive consumers, rising delinquencies, and concerns about the high cost of debt. Central banks remain committed to achieving their 2% inflation target and most acknowledge that interest rates have likely peaked.

Credit – The risk premium for corporate bonds (versus government bonds) tightened materially over the quarter, with a strong risk on tone to the market as investors priced in lower interest rates in 2024 and a “soft-landing” to economic concerns. Corporate bond supply was well received by the market. On the balance, we do not think the current risk premium adequately compensates for downside risk, and as such, we remain cautious on corporate bonds and have a bias towards higher-quality, shorter-dated credit where we view the risk / reward dynamic as being more favourable.

Equity – In the U.S., we allocated exposure to value names which outperformed over the quarter as the macroeconomic outlook improved on the backdrop of rate cut expectations. Looking forward, we expect that margins will continue to normalize as Covid-induced pent up demand fades. While we do not forecast margins to compress at an alarming rate, we believe sticky wage and input costs will continue to pressure businesses while consumers exhibit further exhaustion. As such, we are shifting our focus toward the balance between company reinvestment in capital projects and upcoming debt refinancing requirements. In line with this view, we favour businesses with stable cash flows and decreased debt loads as we believe they present an attractive contrarian opportunity if soft-landing projections prove to be overstated. Within Canada, we remain attentive to the inverse movements of ROE relative to financing costs over 2023. With the excess between ROE and financing costs compressing, businesses’ ability to create value appears more stretched than earlier in 2023. Therefore, we continue to favour high quality companies in Canada, which is typically defined by high ROE, stable earnings variability, and low financial leverage. Geographically, the U.S. economy appears to be in healthier condition with inflation easing while employment and output data remain stable and hence, our focus will be on capital expenditures. EAFE – which is generally more economically linked to China than North America – contains a large bucket of stable, high-quality businesses that may benefit from any upside economic surprises out of China. Lastly, through the lens of a Canadian investor, the Loonie’s relative value versus other major currencies presents another resource in our investment mandate to derive excess return.Downloadable Copy

Mark Warywoda, CFA

VP, Public Portfolio ManagementIan Whiteside, CFA, MBA

AVP, Public Portfolio ManagementJohanna Shaw, CFA

Director, Portfolio ManagementJin Li

Director, Equity Portfolio Management

Tyler Farrow, CFA

Senior Analyst, Equity

Andrew Vermeer

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

ADVISOR USE ONLY

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

- [pdf] Equitable GIF Fees and Fund Codes

-

Tax impacts of the Canadian Dental Care Plan for your clients

Tax impacts of the Canadian Dental Care Plan for your clients*

Earlier this year, the government shared its progress on the Canadian Dental Care Plan (CDCP).

The CDCP will be available to Canadians with an annual family income of less than $90,000 who do not have dental benefits. Co-pays will be waived for eligible Canadians with a family income of less than $70,000.

Canadians who have access to private dental coverage are not eligible for the CDCP. This means that your clients must now report on T4s/T4As if dental coverage** was available on December 31 of the reporting tax year for:- Employees,

- Employees’ spouses and/or dependents,

- Former employees, and

- Spouses of deceased employees.

This new tax reporting requirement is mandatory starting with the 2023 tax year. Employee tax slips will include new boxes for employers to complete:- Box 45 (T4): Employer Offered Dental Benefits. This new box will be mandatory.

- Box 015 (T4A): Payer Offered Dental Benefits. This new box will be mandatory if plan sponsors report in Box 016, Pension or Superannuation. The box will otherwise be optional.

- Code 1: The plan member has no access to dental care insurance or coverage of dental services of any kind.

- Code 2: Only the plan member has access to any dental care insurance, or coverage of dental services of any kind.

- Code 3: The plan member, their spouse and their dependents have access to any dental care insurance, or coverage of dental services of any kind.

- Code 4: Only the plan member and their spouse have access to any dental care insurance, or coverage of dental services of any kind.

- Code 5: Only the plan member and their dependents have access to any dental care insurance, or coverage of dental services of any kind.

Reports for dependents

We have a report available for plan members who have enrolled their dependents in benefits coverage. Your clients can contact their local service team representative to receive a copy of the report. We are working to make it available on our Advisor and PA websites.

Questions

For guidance on your tax slips and reporting obligations, please encourage your clients to contact their accountant, payroll provider or tax advisor.

Supporting plan members affected by the Israeli-Palestinian conflict*

Traumatic events continue to unfold in the Middle East. Enduring ongoing news of conflict and suffering could challenge many Canadians. During this difficult time, Equitable encourages affected clients and plan members to access the mental health support they need.

Large-scale traumatic news events can cause people to experience intense reactions. This puts a lot of strain on their mental health. Having coping mechanisms to deal with the current crisis can be a huge help. Any Equitable Life plan member who needs mental health support can visit Homeweb.ca/equitable to access online resources or contact Homewood at 1.888.707.2115.

Support available to all Equitable plan members

Support available to plan members with the Homewood Health EFAP

For your clients that have purchased Homewood Health’s Employee and Family Assistance Program (EFAP), remind them that their plan members also have access to confidential counselling services. The EFAP provides plan members with 24/7 access to confidential counselling through a national network of mental health professionals. Whether it’s face-to-face, by phone, email, chat or video, plan members and their dependent family members will receive appropriate, timely support for the issue they’re dealing with.

Questions?

If you need more information, contact your Group Account Executive or myFlex account executive.

*Indicates content that will be shared with your clients. - [pdf] Financial Questionnaire - Personal

-

National Pharmacare (Plan NP) takes effect in B.C. on March 1

In this issue:

National Pharmacare (Plan NP) takes effect in B.C. on March 1

Travel coverage details plan members should know if they’re in or going to Mexico*

*Indicates content we will share with your clients.

National Pharmacare (Plan NP) takes effect in B.C. on March 1

The Province of British Columbia (B.C.) will implement the first phase of the National Pharmacare Act, also known as Bill C64 (Act), on March 1, 2026.

The new program will be called National Pharmacare (Plan NP). The province joins Manitoba and Prince Edward Island, who have already implemented the first phase of their own programs. All three provinces, along with Yukon, signed bilateral pharmacare agreements with the federal government last year.

National Pharmacare (Plan NP) coverage details

The federal government has agreed to provide universal coverage for many diabetes drugs and contraceptives, including deductibles, during the first phase of implementation of the Act. Equitable will no longer cover drugs that are eligible for coverage under Plan NP.

Diabetes devices and supplies are not included in the first phase of plan implementation. However, expanded coverage for certain diabetes-related devices and supplies is expected to begin in B.C. on April 1, 2026.

Since B.C. already offers universal coverage of contraceptives through its provincial pharmacare program, the province is using that portion of the federal funding to cover menopausal hormone therapy (MHT), also called hormone replacement therapy (HRT).

Many diabetes medications such as metformin, insulin, sulfonylureas and SGLT-2 inhibitors will be fully covered under Plan NP.

Some diabetes medications and MHTs will only be partially covered when the program takes effect. As well, many diabetes medications will continue to require Special Authority through the province.

What will Equitable plan members need to do?Coverage will be provided automatically at the pharmacy counter. Plan members simply need to present a prescription for a covered medication and their Medical Services Plan of B.C. (MSP) card to their pharmacist. If a plan member isn’t fully enrolled in the MSP yet, their pharmacist will help them secure coverage under Plan NP.

The pharmacist will charge the provincial plan directly for the relevant medications. There will be no direct impact to plan members or their experience at the pharmacy for fully covered drugs.

Where do GLP-1 drugs fit in?

GLP-1 agonist drugs will not be covered under Plan NP. Equitable plan members who are prescribed this type of drug to treat diabetes must try a first-line diabetic treatment before we can deem them eligible for coverage of the GLP-1 agonist.

Plan members who are already taking a GLP-1 agonist to treat diabetes will continue to be eligible for coverage. New plan members or plan members with new prescriptions for GLP-1 agonists must provide us proof that shows they’ve tried a first-line diabetic treatment to confirm eligibility—unless we already have a previous record of their insulin use. Proof can be either a past receipt or a claim statement.

Our priority is supporting the best outcomes for plan sponsors and their members. We are working with TELUS Health, our pharmacy benefits manager, to keep you updated as more details become available.

Travel coverage details plan members should know if they’re in or going to Mexico

Plan members with Travel Assist medical emergency coverage included in their benefits plan should keep the following information in mind if they’re planning travel to Mexico or if they’re in the country now.

Due to recent violence in Mexico, the Government of Canada has issued the following travel advice to anyone in or planning to visit the country.

Plan members are not covered if they receive out-of-province services where the Canadian government had issued a warning to avoid all or non‑essential travel before they entered the country.

Plan members should contact Trident Global Assistance, the company that administers our Travel Assist benefits, before departing if they have questions about their coverage or to confirm if they’re covered for travel to their specific destination.

Here’s how plan members can reach the Trident Global Assistance toll-free 24-hour emergency hotline:

-

In Canada or the U.S: 1-800-321-9998

-

Elsewhere: Call collect at 519-742-3287

They should be prepared to provide the following information:

-

Name

-

Group policy number

-

Certificate number

-

Government health insurance plan number

If a plan member arrived in Mexico before the travel advisory was issued and are past their day allowance, they should call Trident if they need to have their day maximum extended past the allowable period.

Equitable’s Travel Assist medical emergency coverage does not include any trip cancellation or trip interruption benefits.

Communicating to plan members

We are making every effort to share this information with affected plan members. Please encourage your clients who have Travel Assist coverage included in their benefits plan to share this message with their plan members.

-

- Policy Change and Conversions eDelivery - Quick Tips and Tricks

-

Introducing Equitable EZBenefits: A better group benefits solution for your small business clients

If you serve small business owners, chances are they’re looking for a group benefits solution that’s affordable, sustainable and easy to manage. That’s why we introduced Equitable EZBenefits™. It’s a unique group benefits solution designed with you and your small business clients in mind.

Options to fit every need

Available to organizations with between 2 and 25 employees, EZBenefits offers a range of plan design options to match different needs and budgets. * Whether your client owns start-up or a growing company, we’ve got them covered. Plan options include a mix of Life, Health and Dental coverage. ** Clients can also add Long-Term Disability (LTD) coverage or a Health Care Spending Account (HCSA).

Embedded services to support health and wellness

To provide employees with added support for both their physical and mental wellbeing, all our plan design options include:- Anytime, online access to medical professionals through our Virtual Healthcare solution from Dialogue,

- Access to professional counselors – via the telephone, the web or in-person – through our Employee and Family Assistance Program from Homewood Health®, and

- Online resources to help manage health, financial and family challenges through Homeweb, Homewood Health’s online wellness portal.

EZBenefits also comes with built-in HR support through Equitable Life’s partnership with HRdownloads® This takes the heavy lifting out of common human resource tasks with HR support tools and services, including:- HR Technology: An award-winning cloud-based human resource information system to provide help from onboarding to offboarding and everything in between.

- HR Content: Access to a library of over 3,000 HR documents, templates, compliance resources and articles, with 25 free document downloads.

- HR Training: A free Workplace Diversity and Inclusion online training course.

- HR Support: One free Live HR Advice call with a seasoned HR expert.

We know that advising small business clients can be challenging. We’ve created a streamlined benefits process that provides rapid quotes, hassle-free plan implementation, simplified renewals and that is easy to administer. That way, you can spend more time advising your clients and building your business – and less time with administrative back and forth.

Pricing stability for long-term stability

When it comes to attracting and retaining talent, we know your small business clients are competing with larger organizations that have big budgets and lots of resources. That’s why we’ve designed EZBenefits to provide long-term pricing stability for health and dental benefits.

Find out more

Watch this video to learn how EZBenefits can help you and your clients. You can also visit info.equitable.ca/ezbenefits for more details or to request a quote. If you have questions, contact your Equitable Life Group Account Executive. If you don't have an Equitable Life Group Account Executive, email us at EZBenefits@equitable.ca.

* Not available in Quebec.

** Dental coverage is not included with the Bronze plan design option. -

Explore Equitable EZBenefits™

A better group benefits solution for your small business clients

Running a small business isn't easy, especially for companies with smaller budgets and fewer resources. It can be tough to find a competitively priced benefits plan with the features that clients want. That’s why we created Equitable EZBenefits™, a benefits solution designed with the needs of small businesses in mind.

Options to fit every need

Available to organizations with between 2 and 25 employees, EZBenefits offers a range of plan design options to match different needs and budgets. * Whether your client owns start-up or a growing company, we’ve got them covered. Plan options include a mix of Life, Health and Dental coverage. ** Clients can also add Long-Term Disability (LTD) coverage or a Health Care Spending Account (HCSA).

Embedded services to support health and wellness

To provide employees with added support for both their physical and mental wellbeing, all our plan design options include:

● Anytime, online access to medical professionals through our Virtual Healthcare solution from Dialogue,

● Access to professional counselors – via the telephone, the web or in-person – through our Employee and Family Assistance Program from Homewood Health®, and

● Online resources to help manage health, financial and family challenges through Homeweb, Homewood Health’s online wellness portal.

Extra HR support for EZBenefits clients

EZBenefits also comes with built-in HR support through Equitable’s partnership with Citation Canada® (formerly HRdownloads). It takes the heavy lifting out of common human resource tasks with HR support tools and services. Features include:

● an award-winning cloud-based human resource information system (HRIS) to provide help from onboarding to offboarding and everything in between,

● access to a library of over 3,000 HR documents, templates, compliance resources and articles, with 25 free document downloads,

● a free Workplace Diversity and Inclusion online training course, and

● one free Life HR advice call with a seasoned HR expert.

A streamlined process to optimize your time

We know that advising small business clients can be challenging. We’ve created a streamlined benefits process that provides rapid quotes, hassle-free plan implementation, simplified renewals and that is easy to administer. That way, you can spend more time advising your clients and building your business – and less time with administrative back and forth.

Pricing stability for long-term stability

When it comes to attracting and retaining talent, we know your small business clients are competing with larger organizations that have big budgets and lots of resources. That’s why we’ve designed EZBenefits to provide long-term pricing stability for health and dental benefits.

Find out more

To learn more about EZBenefits, watch our video to learn more or view our brochure. You can also visit info.equitable.ca/ezbenefits for more details or to request a quote. If you have questions, contact your Equitable Life Group Account Executive. If you don't have an Equitable Life Group Account Executive, email us at EZBenefits@equitable.ca.

* Not available in Quebec.

** Dental coverage is not included with the Bronze plan design option.

- What is the process to change the agent on record for a policy?