Site Search

762 results for visit page here PROBLEMGO.com husband locked up need him out fast cash

-

Important cybersecurity readiness guidance

As an advisor, you collect and store clients’ sensitive personal information. Protecting this information is essential. In July 2023, the Canadian Insurance Services Regulatory Organization (CISRO) released a guide on Cybersecurity Readiness. It includes tips on keeping this sensitive client data and your business systems safe.

Please read the guide in full. Also, check your own practices to be cyber ready and reduce your risk of an incident.

Some key tips in the guide include:

1. Make cybersecurity a priority: Stay alert to cyber threats. These can be suspicious emails, texts or calls. Make sure your team knows how to keep your data and systems safe and has clear, documented processes to follow.

2. Know what to protect: Understand what data and business systems need to be protected.

3. Identify the risks: Spot the risks in your practice and those from third-party service providers.

4. Implement security measures: Take steps to protect your data and business systems.

5. Be ready to respond: Know how to spot and react to cyber incidents. The guide has useful tips on creating a Cyber Incident Response Plan.

And lastly – if you receive client instructions electronically (by email, text, or messaging apps), always confirm these over the phone to ensure it’s really the client sending the instructions.

Keep your business and important client data safe by staying informed and alert. We encourage you to read the full Cybersecurity Readiness document to learn more about how to prepare for cyber threats.

In our industry, protecting clients’ sensitive data and systems is essential. Thank you for your commitment to cybersecurity!

® or TM denotes a trademark of The Equitable Life Insurance Company of Canada. -

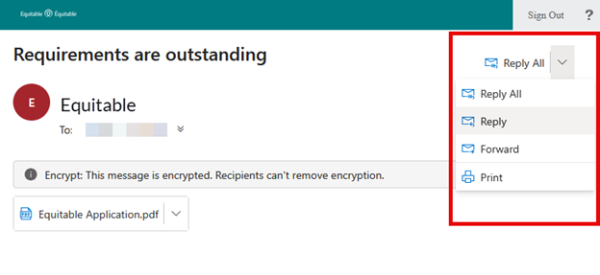

New secure encryption process for outstanding Equitable S&R business requirements

The Equitable® Savings and Retirement Operations team is improving how they send secure email messages to advisors. These emails are sent when there are outstanding requirements for an application or missing information for requests.

Previously, advisors had to manually password protect or unlock PDF documents. This caused delays and difficulties for recipients. The new encryption process will remove that confusion and make it easier for advisors to send and receive secure, encrypted messages.

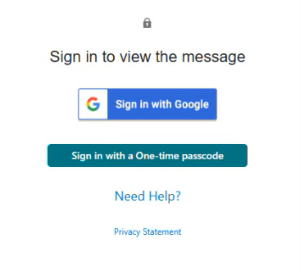

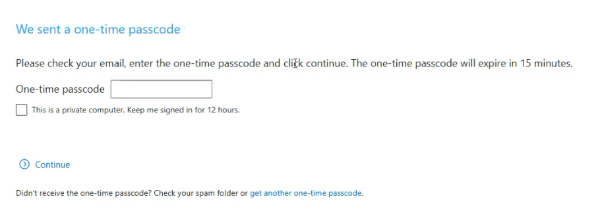

Advisors will now receive secure, encrypted emails from the QA annuity operations mailbox. These emails will use an encrypt option to protect personal client information, such as attachments or requests for personal documents. Recipients will get an email with a subject line saying they have a secure private message. They will need to sign in to view the message or choose to get a one-time passcode (OTP).

Please ensure to check the SPAM folder for the OTP option as it will expire in 15 minutes. Enter the OTP in the secure message

portal.

Emails are sent in both English and French, with automatic translation based on browser settings. Recipients must click the view button to access the message in the secure web portal where they can see the encrypted attachment.

Make sure to click Reply in the top right corner of the encrypted message to keep communications within the secure portal.

For more information or assistance, please contact your Director, Investment Sales.

Date posted: May 22, 2025 -

Insights from a pandemic: COVID-19 and group benefits plans

We’ve received numerous questions about the impact of COVID-19 and what it will mean for benefits plans in the months ahead. Below is a summary of what we’re seeing so far. In the coming weeks, we’ll explore each of these topics in greater depth.

Disability

Initially, as COVID-19 started to spread, we saw STD claims ramp up quickly. Since then, we’ve seen the number of COVID-19-related STD claims slow significantly. As for LTD, we believe both the incidence and duration of those claims will increase in both the short term and medium term due to COVID-19.

Health and Dental Claims

We saw an overall spike in the volume and paid amounts for drug claims in March as plan members rushed to stock up on their medications. This was followed by a drop in April after most provinces put 30-day refill limits in place. One exception was claims for asthma drugs which surged in March but had no drop in April. Overall, the April plunge will be short-lived; drug costs have already begun to rise in May.

While paramedical and dental claims are down, we are seeing an increase in claims for virtual treatments and emergency dental services. We expect that claims will spike once the current pandemic restrictions are lifted. We’ve already started to see claims rise in provinces that are allowing health providers to re-open.

Despite the shift to more virtual services, we haven’t seen an increase in fraudulent activity. But we continue to be vigilant. Our investigative practices – verifying with the plan member that they received the treatment and have a valid receipt, and that the practitioner has treatment notes – remain the same whether treatment is provided in person or virtually.

Technology

During this time of physical distancing, people are looking for ways to interact with their providers virtually. Fortunately, our business model is almost entirely electronic, and we have several convenient digital options available for plan members and plan sponsors. Our focus in recent weeks has been to remind clients and plan members about these tools and make it as easy as possible for them to activate and use them. And we are continually adding functionality that will allow us to serve our customers even better.

Mental Health/Wellness

Usage of i-Volve, Homewood’s online cognitive behavioural therapy tool, increased significantly in March before levelling back down in April and May. And while EFAP cases fell in April and early-May, the number of cases has begun to climb in recent weeks, particularly for anxiety. In the coming weeks and months, we expect an eventual increase in marital and family issues, as well as depression. We’ve also seen an increase in mental-health-related prescriptions.

Plan Design

It’s too early to predict how the COVID-19 pandemic will impact benefits plan design and how it will change in the coming months. We would love to get your feedback and insights about how benefit plans will evolve and what new features or provisions they should include.

Please share your thoughts and suggestions with your Group Account Executive or myFlex Marketing Manager. Or, you can email your ideas to GroupCommunications@equitable.ca.

- About

-

Levelizing taxes on fixed income investments

A smart strategy to promote with clients

Many clients choose fixed income investments because they are more stable and predictable than other investment types. However, there is a downside to this approach that many don’t think about – taxes, which increase as the investment grows. As an advisor, you can help clients reduce some of the money they pay in taxes by suggesting a different approach.

In most cases, fixed income investments are taxed yearly. To pay these taxes, clients usually take out some of the interest income earned, and leave the rest invested. This in turn increases the tax that must be paid on the interest earned the next year. As a result, a large amount of the investment income earned each year goes straight to taxes with a growing amount of tax that must be paid each year. You can show clients a solution that can help lower total taxes they pay on their fixed income investments.

The tax challenge

Using participating whole life (WL) insurance as part of a financial solution, you can help clients levelize their annual tax payment. And lower the cumulative tax they must pay on their fixed income investments.

The solution: levelize the tax

Each year the client takes out the full amount of the interest earned on the fixed income investment. They leave only the principal amount. Part of the interest income withdrawn is used to pay the taxes on the fixed income investment. The remaining amount is used to pay premiums for a participating WL policy. Because the client is leaving only the principal amount invested, the tax they pay each year is a levelized amount. This reduces the cumulative taxes they pay over the life of the fixed income investment.

How it works

With this solution, the value of the fixed income investment along with the potential value provided by the participating WL policy, can mean a higher estate value. And a lower cumulative tax bill than what can be achieved through only the fixed income investment.

The participating life insurance not only provides valuable life insurance coverage, but also offers tax-advantaged growth and the potential for dividends.

To help explain this concept to individual clients, feel free to share Levelize the tax on your fixed income investments with participating whole life (1799).

This concept also works with corporate owned participating whole life policies. Feel free to share Levelize the tax on fixed income investments with corporately-owned participating whole life (1874).

This solution isn’t just about lowering taxes. It’s about helping clients grow their money, plan for their future, and protect what matters most. As an advisor, guiding clients toward solutions that address both immediate and future needs can set you apart and help build trust.

Why it matters

Contact your wholesaler to learn more. - [pdf] Equitable Guaranteed Investment Funds – Protection Class

- EquiNet-FAQ-FINAL_fr

- [pdf] MGA Information in EZcomplete

- [pdf] Aviation Questionnaire

- [pdf] Financial Questionnaire - Business