Site Search

594 results for access source MAKEMUR.COM Paying to get out of pretrial detention Alcatraz Federal Penitentiary

- [pdf] Dollar Cost Averaging

-

ALERT! Temporary Suspension of Ground Service – British Columbia

The British Columbia government has declared a provincial state of emergency following severe flooding and landslides, causing widespread damage and road closures preventing ground access into and out of the province.

Please be advised that we are not accepting courier shipments traveling by ground into and out of British Columbia. Any printed materials ordered from Equitable Life will be held until the situation in BC is resolved. In the meantime, please feel free to use our digital copies.

If you have any questions or concerns, please contact your Regional Sales Manager.

-

Responding to Alberta's Biosimilar Initiative

Beginning March 15, 2021, we are changing coverage for some biologic drugs in Alberta in response to the province’s Biosimilar Initiative. These changes will help protect your clients from additional drug costs that may result from this new government policy while still providing access to equally safe and effective biosimilars.

What is Alberta’s Biosimilar Initiative?

Alberta’s Biosimilar Initiative will end provincial coverage of several originator biologic drugs for some or all conditions beginning on Jan. 15, 2021. Patients 18 and over who are using these drugs for the affected conditions will be required to switch to biosimilar versions of the drugs to maintain coverage under the province’s government drug plan.

What is the impact on private drug plans?

Industry response to Alberta’s Biosimilar Initiative has the potential to significantly impact your clients’ drug plan costs. If other insurance carriers follow suit with the province and delist the originator biologics, it could expose a plan that doesn’t delist them to significant coordination of benefits risk. (See Case Study below.)

How is Equitable Life responding?

To protect your clients’ plans from paying additional and avoidable drug costs, we are changing coverage in Alberta for most biologic drugs included in the provincial initiative.

As of March 15, 2021, several originator biologic drugs will no longer be covered for plan members of all ages in Alberta. Plan members taking these biologics will be required to switch to the biosimilar versions of these drugs to maintain eligibility under their Equitable Life plan.

What drugs and conditions are affected?

The following table outlines the drugs and conditions that will be affected by this change. The list of affected drugs or conditions is dynamic and will change as Alberta includes more biologic drugs in its Biosimilar Initiative, as new biosimilars come onto the market, and as we make changes in drug eligibility.

Drug name Originator biologic

These drugs will no longer be covered in Alberta for the conditions listed in this table.Biosimilar

Plan members will need to switch to these medications to maintain coverage under their Equitable Life plan.

Affected health conditions

The changes in coverage apply to these conditions.Etanercept Enbrel Brenzys

ErelziAnkylosing Spondylitis

Rheumatoid Arthritis

Polyarticular juvenile idiopathic arthritis (JIA)

Psoriatic Arthritis

Plaque Psoriasis (adults and children)Infliximab Remicade Inflectra

Renflexis

AvsolaAnkylosing Spondylitis

Plaque Psoriasis

Psoriatic Arthritis

Rheumatoid Arthritis

Crohn's Disease (adults and children)

Ulcerative Colitis (adults and children)Insulin glargine Lantus Basaglar Diabetes (Type 1 and 2) Filgrastim Neupogen Grastofil

NivestymNeutropenia Pegfilgrastim Neulasta Lapelga

Fulphila

ZiextenzoNeutropenia Glatiramer* Copaxone Glatect

TEVA-Glatiramer AcetateMultiple Sclerosis *Glatiramer is a non-biologic complex drug.

How will Equitable Life communicate this change to plan members?

We will be communicating with affected claimants in January 2021 to allow them ample time to change their prescriptions and avoid any interruptions in their treatment or their coverage.

Can my client maintain coverage of these biologic drugs?

Traditional groups who wish to opt out of this change and maintain coverage of these originator biologics for Alberta plan members can submit a policy amendment. Amendments must be submitted no later than January 15, 2021. Advisors with myFlex Benefits clients who wish to maintain coverage of these originator biologics for Alberta plan members should speak to their myFlex Sales Manager to confirm their eligibility to opt out of this change.

Will this change impact my clients’ rates?

The rate impact of this change in coverage will be relatively insignificant. Any cost savings associated with the change will be factored in at renewal.

If plan sponsors opt out of these changes and maintain coverage for the originator biologics, it may result in a rate increase. Any rate adjustment will be applied at renewal.

What is the difference between biologics and biosimilars?

Biologics are drugs that are engineered using living organisms like yeast and bacteria. The first version of a biologic developed is also known as the “originator” biologic. Biosimilars are also biologics. They are highly similar to the originator drug they are based on and have been shown to have no clinically meaningful differences in safety or efficacy.

Questions?

If you have any questions about this change, please contact your Group Account Executive or myFlex Sales Manager.

CASE STUDY: The Alberta Biosimilar Initiative and Coordination of Benefits (CoB) risk

CoB risk is real and can be significant, even if a pharmaceutical savings program exists.

The industry response to Alberta’s Biosimilar Initiative has the potential to significantly impact your clients’ drug plan costs. Some insurers may follow the province’s lead and delist these originator biologics. Others may cut back coverage to the cost of the biosimilars or maintain coverage of the originators. These differences could expose a plan that doesn’t delist the originator biologics to significant coordination of benefits risk. Here’s how:

Let’s assume there are two private drug plans – Plan A and Plan B. Both plans are open plans with no deductible. Plan A has 80% co-insurance and Plan B has 100% co-insurance.

BEFORE Alberta’s Biosimilar Initiative

Before Alberta’s Biosimilar Initiative, both plans cover the originator biologics listed above.

Plan A is the first private payer for an Alberta plan member taking an originator biologic drug for Rheumatoid Arthritis. Plan B is the second private payer. The cost of the originator biologic for the plan member is $30,000 annually. Here’s how the coordination of benefits would look before Alberta’s Biosimilar Initiative.

AFTER Alberta’s Biosimilar InitiativeIn response to Alberta’s Biosimilar Initiative, the insurer for Plan A delists the originator biologic and requires plan members to switch to the biosimilar. The insurer for Plan B maintains coverage of the originator biologic. Under this scenario, if the plan member doesn’t switch, Plan B essentially becomes the first payer and sees their annual cost increase by 400% (from $6,000 to $30,000).

Even if the insurer for Plan B cuts back coverage to the cost of the biosimilar or adjusts the paid amount because they have a savings program in place with the drug manufacturer, the impact could be significant. For example, if the insurer cuts back coverage to 50% (or $15,000 annually), Plan B would see a 150% annual cost increase (from $6,000 to $15,000):

-

February 2023 eNews

Responding to Nova Scotia’s biosimilar switch initiative

We are changing coverage for some biologic drugs in Nova Scotia in response to the province’s biosimilar initiative. These changes will help protect your clients’ plans from additional drug costs that may result from this new government policy while providing access to equally safe and effective lower-cost biosimilars.Nova Scotia’s provincial biosimilar initiative

Announced in February 2022, the Nova Scotia Biosimilar Initiative ends coverage of seven biologic drugs for residents enrolled in Pharmacare programs.

Pharmacare patients in the province using these drugs will be required to switch to biosimilar versions of these drugs by February 3, 2023, in order to maintain their Nova Scotia Pharmacare coverage.Equitable Life’s response

To ensure this provincial change doesn’t result in your clients’ plans paying additional and avoidable drug costs, we are changing coverage in Nova Scotia for most biologic drugs included in the provincial initiative.

Beginning June 1, 2023, plan members in the province will no longer be eligible for most originator biologic drugs if they have a condition for which Health Canada has approved a lower cost biosimilar version of the drug.** These plan members will be required to switch to a biosimilar version of the drug to maintain coverage under their Equitable Life plan.Can my client maintain coverage of these biologic drugs?

Traditional groups who wish to opt out of this change and maintain coverage of these originator biologics for Nova Scotia plan members can submit a policy amendment. Amendments must be submitted no later than April 1, 2023. Advisors with myFlex Benefits clients who wish to maintain coverage of these originator biologics for Nova Scotia plan members should speak to their myFlex Sales Manager to confirm their eligibility to opt out of this change.

Groups that choose to maintain coverage of these originator biologics for existing claimants will also maintain coverage for any originator biologics that we subsequently add to our Nova Scotia biosimilar initiative.Will this change impact my clients’ rates?

The rate impact of this change in coverage will be relatively insignificant. Any cost savings associated with the change will be factored in at renewal.

If plan sponsors opt out of these changes and maintain coverage for the originator biologics, it may result in a rate increase. Any rate adjustment will be applied at renewal.Communicating this change to plan members

We will inform any affected plan members in April of the need to switch their medications so that they have ample time to change their prescriptions and avoid any interruptions in treatment or coverage.What is the difference between biologics and biosimilars?

Biologics are drugs that are engineered using living organisms like yeast and bacteria. The first version of a biologic developed is known as the “originator” biologic. Biosimilars are highly similar to the drugs they are based on and Health Canada considers them to be equally safe and effective for approved conditions.Questions?

If you have any questions about this change, please contact your Group Account Executive or myFlex Sales Manager.

**The list of affected drugs is dynamic and will change as Nova Scotia includes more biologic drugs in its biosimilar initiative, as new biosimilars come onto the market, and as we make changes in drug eligibility.

Changes to New Brunswick drug interchangeability rules

We are introducing changes to help ensure that your clients with voluntary or mandatory generic pricing for their drug plans will benefit more from the cost savings of these two features, regardless of the province where the drugs are dispensed.

Currently, when determining whether a lower-cost alternative is available for a brand-name drug, most insurers only consider drugs that the provincial drug plan identifies as interchangeable.

However, the public drug plan in New Brunswick does not identify a drug as interchangeable if the drug is not listed on its formulary – even if Health Canada has deemed the drug interchangeable.

As a result, plans with mandatory or voluntary generic pricing have continued to reimburse some drugs in New Brunswick based on the cost of the brand-name drug, even if a lower-cost generic alternative is available.

Effective March 20, 2023, if your clients have drug plans with mandatory or voluntary generic pricing, we will adjudicate any drug claims in New Brunswick using the lowest cost alternative that Health Canada approves as bioequivalent. This will occur even if the public drug plan has not identified the drug as interchangeable.

To benefit from this more robust drug plan control, plan sponsors must have mandatory or voluntary generic pricing in place.

For more information about this change or about implementing mandatory or voluntary generic pricing for your clients, please contact your Group Account Executive or myFlex Sales Manager.

New template: plan members eligible for additional coverage

Often, based on salary, some plan members may become eligible to apply for extra Life, Accidental Death & Dismemberment (AD&D), Short Term Disability or Long Term Disability coverage. If this occurs, your clients receive a notification from Group Benefits Administration. We have now developed a template that your clients can provide to applicable plan members if they become eligible for extra coverage. The template makes it simpler for your clients to pass on these details to their plan members efficiently.

The new template is available for download under the Quick Links section of EquitableHealth.ca. It is a fillable PDF form that your clients can complete and provide to their plan members when necessary. The document is called Over the Non-Evidence Limit for Plan Members Notification.

If you have any questions about the template, please contact your Group Account Executive or myFlex Sales Manager. -

Helping you deliver more value to clients

In this issue:

Mid-year update: Helping you deliver more value to clients

Coming soon: Easier access to vision and dental coverage details*

*Indicates content we will share with your clients

Mid-year update: Helping you deliver more value to clientsIn this mid-year video update, Marc Avaria, Executive Vice President, Group Insurance, shares key progress and priorities that are driving our group benefits business. Find out what they mean for you, your clients and plan members.

Coming soon: Easier access to vision and dental coverage details

Equitable® group benefits plans that include dental or vision coverage will soon give plan members easy access to key benefit details at their fingertips. Plan members with vision or dental benefits will be able to easily access coverage information about dental check-ups and fillings, as well as eye exams and eyewear right from the EquitableHealth.ca® home page. The page also includes information on when the plan member is eligible for their next covered dental checkup or eye exam.

Earlier this year, we introduced quick access to paramedical coverage information and spending account balances on the home page. These updates made it easier for plan members to find important benefits information in one convenient place.

Plan members can continue to access helpful resources from the home page, including their digital benefits cards and plan booklet.

See these new features in the video below:

More enhancements coming soon

These updates are part of our ongoing journey to enhance the digital experience for our plan members. More self-service features will be added soon to make it even easier for plan members to manage their benefits.

To learn more about how we’re making the home page effortless for plan members, contact your Group Account Executive or visit Equitable.ca/effortless.

-

Help your clients this tax season with Equitable Life

It is tax time, and your clients should be receiving tax slips and deposit receipts by now. Check out the Tax Slips: A Quick Reference Guide which gives a taxation breakdown by product. Review Insights into Non-Registered Taxation that offers a detailed explanation on investment income, and why T3 tax slips generate on non-registered segregated funds. Does your client have questions about contribution limits? Retirement Income Fund minimums? or Canada pension maximums? Check out Equitable’s handy 2022 Facts & Figures guide.

Did your clients sign up for tax slips on Equitable Client Access before December 31, 2021?

If so, your clients can download or print their tax slips quickly and easily from their Equitable Client Access Inbox.

For questions, contact Equitable's Advisor Services Team Monday to Friday, 8:30 a.m. – 7:30 p.m. ET at 1.866.884.7427 or by email at savingsretirement@equitable.ca. or your Regional Investment Sales Manager. -

Tax Slips – What you need to know

It is tax time, and clients should be receiving tax slips and deposit receipts by now. Check out the Tax Slips: A Quick Reference Guide for a taxation breakdown by product and Insights into Non-Registered Taxation for a detailed explanation on investment income, and why T3 tax slips are generated on non-registered segregated funds.

Clients who registered for tax slips on Equitable Client Access before December 31, 2022, can download or print tax slips quickly and easily from their Equitable® Client Access Inbox. Advisors can download tax receipts on Document Lookup on EquiNet®.

For questions about contribution limits, Retirement Income Fund minimums and Canada pension maximums check out Equitable Life®’s helpful 2023 Facts & Figures guide.

Equitable's Advisor Services Team is available Monday to Friday, 8:30 a.m. – 7:30 p.m. ET at 1.866.884.7427 or by email at savingsretirement@equitable.ca. You can also contact your Regional Investment Sales Manager.

® denotes a trademark of The Equitable Life Insurance Company of Canada.

Posted: February 15, 2023 - [pdf] Personalized Brochure - Benefits of segregated funds in a Tax-free Savings Account

-

EAMG Market Commentary April 2024

April 2024

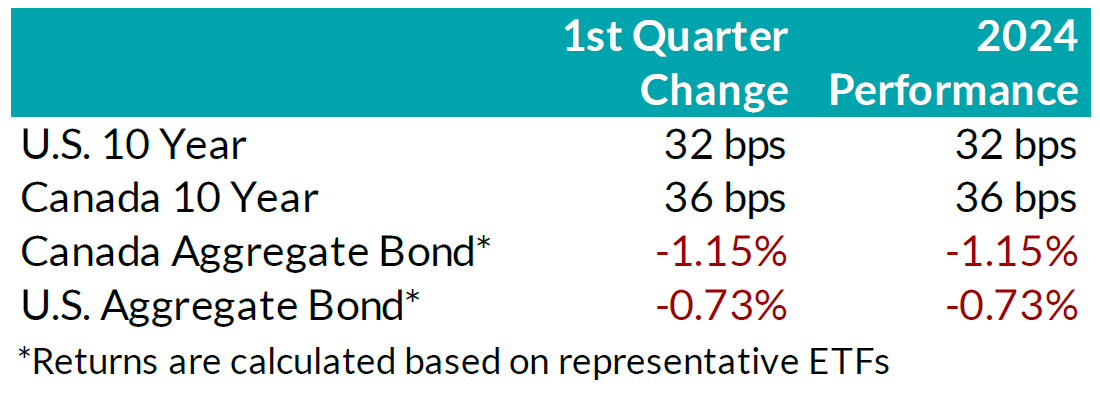

Rates & Credit – Interest rates increased in Q1 2024, giving back half of the decline experienced in Q4 2023 amid consistently positive surprises in U.S. economic data. The positive economic news also drove a strong risk-on tone to the market, with the risk premium on corporate bonds tightening as economic prospects improved. In Canada, corporate bonds outperformed government bonds and the broader FTSE Canada Universe Index (FTSE) with a slightly positive 0.07% return, verses a loss of 1.66% in government bonds and a loss of 1.22% for the overall index. More interest rate sensitive long-term bonds experienced the largest decline, which was partially offset in corporate bonds by the risk-on tone to corporate bond spreads. On a 6-month and 1-year basis, the FTSE remained positive at 6.94% and 2.10%, respectively. Within corporate bonds, lower-rated BBBs outperformed higher-rated A bonds, while industries with higher interest rate exposure such as infrastructure, energy, and communications underperformed those with less exposure (notably financials and securitization).

.png?width=850&height=303 "chart1-(4).png")

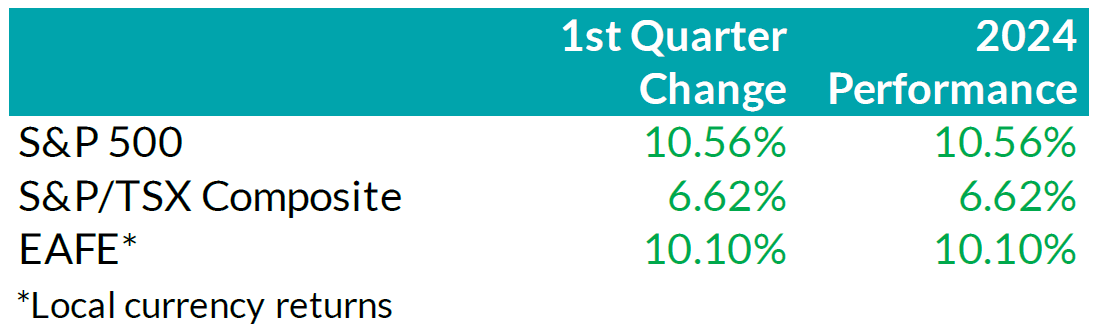

Equity Overview – Throughout Q1 2024, concerns about a recession gradually eased as central bankers adopted a more accommodative outlook on monetary policy. Their growing dovishness reflected confidence that the restrictive monetary measures were effectively curbing inflation as anticipated. Underpinned by prospects of an economic soft-landing, global equity markets rallied to start the year with most major North American indices soaring to new all-time highs during the quarter. U.S. equities continued to outperform other major international markets with the S&P 500 returning 10.6% in USD terms. Major developed economies from Europe, Australasia, and the Far East (EAFE) gained 10.1% in local currency terms, while the TSX added 6.6%. Furthermore, the U.S. economy continued to prove more resilient than most major developed economies, with strong employment and robust output data. As such, foreign investors of U.S. denominated securities achieved enhanced returns, benefitting from a stronger Greenback.

.png?width=850&height=260 "chart2-(1).png")

U.S. Fundamentals – Corporate earnings beat expectations in Q4 2023, triggering a wave of upward earnings revision. Stable operating margins, cash flows and debt loads continue to attract investors into equities. Investors appear focused on the company’s ability to sustain debt levels ahead of renewing debt obligations. We observed that the number of major companies that expect improving financial performance shrunk to ~19%. This suggests that concentration risks are likely brewing in the equity market, yet again.

U.S. Quant Factors

Optimistic run-up in equity valuations were mostly driven by the momentum factor. A basket of companies with positive price trends intensified concentration risk in the equity market. We note that momentum factor’ performance sharply contrasted fundamental factors, making us cautious on the market’s complacency. For context, high quality companies, which is typically defined by high Return on Equity (ROE), stable earnings variability, and low financial leverage, placed second in our risk-adjusted performance rankings, and is dwarfed by the ~ 17.9% return observed from the momentum factor.

Canadian Fundamentals – Against the backdrop of underwhelming financial results, ROE – a gauge of how efficiently a corporation generates profits – rebounded in Q4, 2023, after declining throughout most of the year. The improved efficiency metric provided a positive catalyst for dividend investors as the inverse movements of ROE relative to financing costs over 2023 kept investors on the sidelines. In addition, the CRB Raw Industrials Index, a measure of price changes of basic commodities, broke out of recent ranges, providing a tailwind for Canada’s energy and materials sector. Concerns with earnings contraction and macro-economic conditions have subsided.

Canadian Quant Factors – Crude prices soared higher in Q1 2024, with ongoing production cuts from OPEC+ and ramifications of geopolitical conflicts keeping oil markets undersupplied. As such, energy companies benefitted, surging higher and outperforming the broader index, while the low volatility basket – with lower exposure to cyclically sensitive business – underperformed into quarter end. Furthermore, Canadian banks underperformed to start the quarter, giving back some of the sharp outperformance witnessed into the end of Q4 2023. That said, soft inflation data increased expectations of impending rate cuts from the Bank of Canada and, as such, banks performed in line with the broader market throughout most of the quarter. Underpinned by expectations of a dovish switch in monetary policy, investors rewarded dividend payers with a history of increasing dividends, boosting confidence in their ability to support future dividend growth. It is important to note that investors should not let dividend growth’s outperformance overshadow high dividend paying companies’ underperformance; more specifically, investors remain attentive to the businesses’ ability to create value relative to financing costs.

Views From the Frontline

Rates – Interest rates in both Canada and the U.S. increased across all bond tenors in Q1 2024. U.S. inflation data surprised to the upside, remaining stubbornly higher than hoped, while labour market and consumer indicators underscored the economy's continued strength. In Canada, inflation data fell below forecasts, but early 2024 GDP readings exceeded expectations. The market now anticipates a 'soft landing' for the U.S. economy; however, the Canadian economy continues to slow. North American central banks have signaled that we are at the peak for policy rates. The market is currently pricing in approximately two-to-three, 25 basis point interest rate cuts by the U.S. Federal Reserve in the second half of 2024, much fewer than the six-to-seven 25 basis point interest rate cuts that the market had been anticipating even just three months ago. As the Swiss central bank led the way with the first rate cut among developed countries, central banks in major developed economies will closely monitor upcoming data and market developments to determine the timing and pace for rate cuts.

Credit – The risk premium for corporate bonds (versus government bonds) continued to tighten over the quarter, with a strong risk-on tone to the market as investors priced in renewed economic growth in 2024 as compared to previous expectations. Corporate bond supply was robust, with $38.2bn in new issuance, the second strongest first quarter on record. On the balance, we do not think the current risk premium adequately compensates for downside risk, particularly in longer-dated corporate bonds, and have a bias towards shorter-dated credit where we view the risk / reward dynamic as being more favourable.

Equity – We favour a combination of the Dow Jones and the S&P500 for our broad market exposure. The Dow, a price-weighted index, should have some value and low volatility tilt as it tracks mature large companies. As explained above, concentration risks are brewing in the equity market, and during Q1 this risk was exacerbated by investors rushing into a basket of companies with positive price trends, thereby pushing valuation metrics further into the expensive territory. In our view, it is well-suited to use a combination of the Dow Jones Industrial Average and the S&P 500 for broad U.S. market exposure given the heightened concentration risk. Looking forward, we expect companies to exhibit stable operating margins and therefore, we are shifting our focus toward the balance between upcoming corporate debt refinancing requirements and reinvestment in projects intended to drive future growth. In plain words, we are tactically adding to companies with stable cash flows and decreased debt loads outside of the mega-cap group. In Canada, we expect a modest earnings growth and remain attentive to how efficiently a corporation generates profits relative to their financing cost. We caution against the overly optimistic, commodity driven, “catch-up” trade vs. our southern neighbour. Therefore, we tweaked our investment strategy by rotating out of the low volatility factor and adding to higher yielding quality companies in Canada.

Downloadable Copy

Mark Warywoda, CFA VP, Public Portfolio Management Ian Whiteside, CFA, MBA AVP, Public Portfolio Management Johanna Shaw, CFA Director, Portfolio Management Jin Li

Director, Equity Portfolio ManagementTyler Farrow, CFA

Senior Analyst, EquityAndrew Vermeer

Senior Analyst, CreditElizabeth Ayodele

Analyst, CreditFrancie Chen

Analyst, Rates

ADVISOR USE ONLY

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

- [pdf] Corporate Preferred Estate Transfer using universal life