Site Search

766 results for browse now MAKEMUR.COM early release from jail payment options

- [pdf] Application for Term Conversion (Guide)

- [pdf] Equitable GIF Advisor Guide

- Navigating the current market

-

EAMG Market Commentary April 2024

April 2024

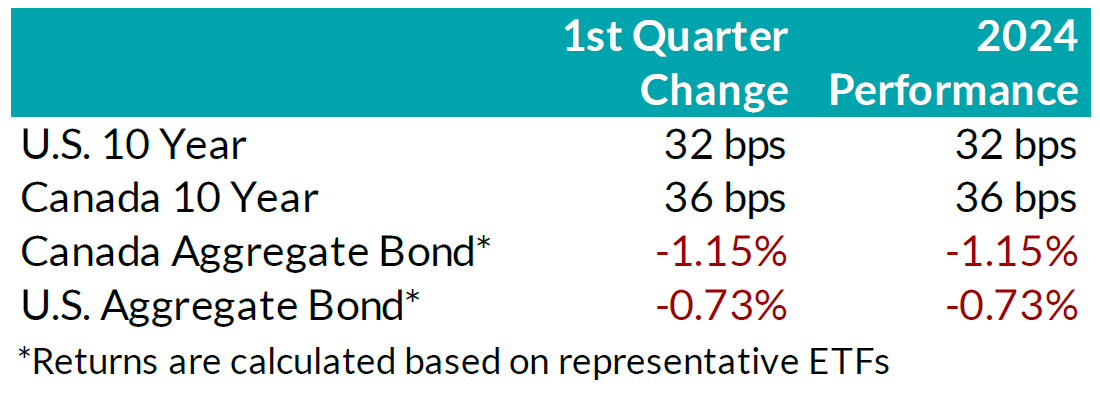

Rates & Credit – Interest rates increased in Q1 2024, giving back half of the decline experienced in Q4 2023 amid consistently positive surprises in U.S. economic data. The positive economic news also drove a strong risk-on tone to the market, with the risk premium on corporate bonds tightening as economic prospects improved. In Canada, corporate bonds outperformed government bonds and the broader FTSE Canada Universe Index (FTSE) with a slightly positive 0.07% return, verses a loss of 1.66% in government bonds and a loss of 1.22% for the overall index. More interest rate sensitive long-term bonds experienced the largest decline, which was partially offset in corporate bonds by the risk-on tone to corporate bond spreads. On a 6-month and 1-year basis, the FTSE remained positive at 6.94% and 2.10%, respectively. Within corporate bonds, lower-rated BBBs outperformed higher-rated A bonds, while industries with higher interest rate exposure such as infrastructure, energy, and communications underperformed those with less exposure (notably financials and securitization).

.png?width=850&height=303 "chart1-(4).png")

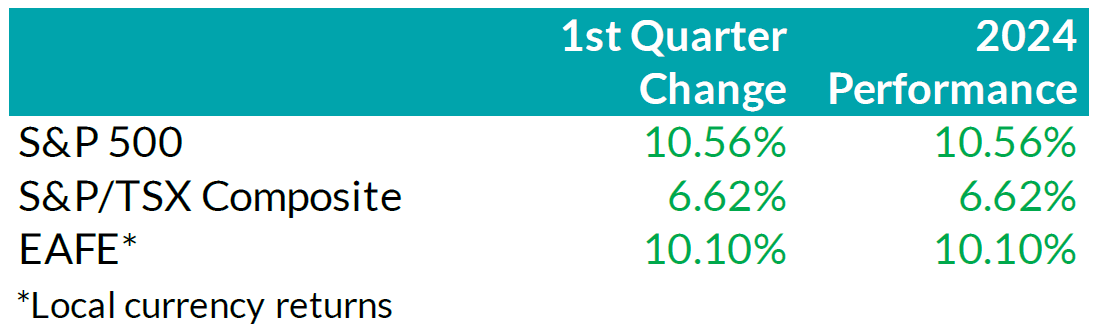

Equity Overview – Throughout Q1 2024, concerns about a recession gradually eased as central bankers adopted a more accommodative outlook on monetary policy. Their growing dovishness reflected confidence that the restrictive monetary measures were effectively curbing inflation as anticipated. Underpinned by prospects of an economic soft-landing, global equity markets rallied to start the year with most major North American indices soaring to new all-time highs during the quarter. U.S. equities continued to outperform other major international markets with the S&P 500 returning 10.6% in USD terms. Major developed economies from Europe, Australasia, and the Far East (EAFE) gained 10.1% in local currency terms, while the TSX added 6.6%. Furthermore, the U.S. economy continued to prove more resilient than most major developed economies, with strong employment and robust output data. As such, foreign investors of U.S. denominated securities achieved enhanced returns, benefitting from a stronger Greenback.

.png?width=850&height=260 "chart2-(1).png")

U.S. Fundamentals – Corporate earnings beat expectations in Q4 2023, triggering a wave of upward earnings revision. Stable operating margins, cash flows and debt loads continue to attract investors into equities. Investors appear focused on the company’s ability to sustain debt levels ahead of renewing debt obligations. We observed that the number of major companies that expect improving financial performance shrunk to ~19%. This suggests that concentration risks are likely brewing in the equity market, yet again.

U.S. Quant Factors

Optimistic run-up in equity valuations were mostly driven by the momentum factor. A basket of companies with positive price trends intensified concentration risk in the equity market. We note that momentum factor’ performance sharply contrasted fundamental factors, making us cautious on the market’s complacency. For context, high quality companies, which is typically defined by high Return on Equity (ROE), stable earnings variability, and low financial leverage, placed second in our risk-adjusted performance rankings, and is dwarfed by the ~ 17.9% return observed from the momentum factor.

Canadian Fundamentals – Against the backdrop of underwhelming financial results, ROE – a gauge of how efficiently a corporation generates profits – rebounded in Q4, 2023, after declining throughout most of the year. The improved efficiency metric provided a positive catalyst for dividend investors as the inverse movements of ROE relative to financing costs over 2023 kept investors on the sidelines. In addition, the CRB Raw Industrials Index, a measure of price changes of basic commodities, broke out of recent ranges, providing a tailwind for Canada’s energy and materials sector. Concerns with earnings contraction and macro-economic conditions have subsided.

Canadian Quant Factors – Crude prices soared higher in Q1 2024, with ongoing production cuts from OPEC+ and ramifications of geopolitical conflicts keeping oil markets undersupplied. As such, energy companies benefitted, surging higher and outperforming the broader index, while the low volatility basket – with lower exposure to cyclically sensitive business – underperformed into quarter end. Furthermore, Canadian banks underperformed to start the quarter, giving back some of the sharp outperformance witnessed into the end of Q4 2023. That said, soft inflation data increased expectations of impending rate cuts from the Bank of Canada and, as such, banks performed in line with the broader market throughout most of the quarter. Underpinned by expectations of a dovish switch in monetary policy, investors rewarded dividend payers with a history of increasing dividends, boosting confidence in their ability to support future dividend growth. It is important to note that investors should not let dividend growth’s outperformance overshadow high dividend paying companies’ underperformance; more specifically, investors remain attentive to the businesses’ ability to create value relative to financing costs.

Views From the Frontline

Rates – Interest rates in both Canada and the U.S. increased across all bond tenors in Q1 2024. U.S. inflation data surprised to the upside, remaining stubbornly higher than hoped, while labour market and consumer indicators underscored the economy's continued strength. In Canada, inflation data fell below forecasts, but early 2024 GDP readings exceeded expectations. The market now anticipates a 'soft landing' for the U.S. economy; however, the Canadian economy continues to slow. North American central banks have signaled that we are at the peak for policy rates. The market is currently pricing in approximately two-to-three, 25 basis point interest rate cuts by the U.S. Federal Reserve in the second half of 2024, much fewer than the six-to-seven 25 basis point interest rate cuts that the market had been anticipating even just three months ago. As the Swiss central bank led the way with the first rate cut among developed countries, central banks in major developed economies will closely monitor upcoming data and market developments to determine the timing and pace for rate cuts.

Credit – The risk premium for corporate bonds (versus government bonds) continued to tighten over the quarter, with a strong risk-on tone to the market as investors priced in renewed economic growth in 2024 as compared to previous expectations. Corporate bond supply was robust, with $38.2bn in new issuance, the second strongest first quarter on record. On the balance, we do not think the current risk premium adequately compensates for downside risk, particularly in longer-dated corporate bonds, and have a bias towards shorter-dated credit where we view the risk / reward dynamic as being more favourable.

Equity – We favour a combination of the Dow Jones and the S&P500 for our broad market exposure. The Dow, a price-weighted index, should have some value and low volatility tilt as it tracks mature large companies. As explained above, concentration risks are brewing in the equity market, and during Q1 this risk was exacerbated by investors rushing into a basket of companies with positive price trends, thereby pushing valuation metrics further into the expensive territory. In our view, it is well-suited to use a combination of the Dow Jones Industrial Average and the S&P 500 for broad U.S. market exposure given the heightened concentration risk. Looking forward, we expect companies to exhibit stable operating margins and therefore, we are shifting our focus toward the balance between upcoming corporate debt refinancing requirements and reinvestment in projects intended to drive future growth. In plain words, we are tactically adding to companies with stable cash flows and decreased debt loads outside of the mega-cap group. In Canada, we expect a modest earnings growth and remain attentive to how efficiently a corporation generates profits relative to their financing cost. We caution against the overly optimistic, commodity driven, “catch-up” trade vs. our southern neighbour. Therefore, we tweaked our investment strategy by rotating out of the low volatility factor and adding to higher yielding quality companies in Canada.

Downloadable Copy

Mark Warywoda, CFA VP, Public Portfolio Management Ian Whiteside, CFA, MBA AVP, Public Portfolio Management Johanna Shaw, CFA Director, Portfolio Management Jin Li

Director, Equity Portfolio ManagementTyler Farrow, CFA

Senior Analyst, EquityAndrew Vermeer

Senior Analyst, CreditElizabeth Ayodele

Analyst, CreditFrancie Chen

Analyst, Rates

ADVISOR USE ONLY

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

-

Market Commentary July 2025

Key Takeaways

• Markets were very volatile in April to start Q2 but calmed as the quarter progressed. Volatility was driven mostly by headlines about tariffs, but other fiscal policy developments also had an impact.

• Equity markets sold off sharply at the start of the quarter, continuing Q1’s weakness. Markets rebounded sharply once worst-case fears over tariffs eased. The markets continued to rally through the quarter as trade negotiations progressed. Stronger-thanexpected corporate earnings also boosted markets. Despite the shaky start to the quarter, most global equity markets set new all-time highs in Q2.

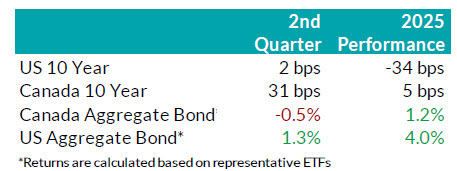

• Canadian bond markets delivered slightly negative returns in Q2. Weak performance was driven by rising interest rates, which outweighed the impact of tighter credit spreads. Higher interest rates hurt the performance of longer-term bonds most.

• Both the Bank of Canada and the U.S. Federal Reserve adopted a wait-and-see approach. They each held rates steady during Q2, awaiting greater clarity on the impacts of tariffs on both growth and inflation before considering further cuts.

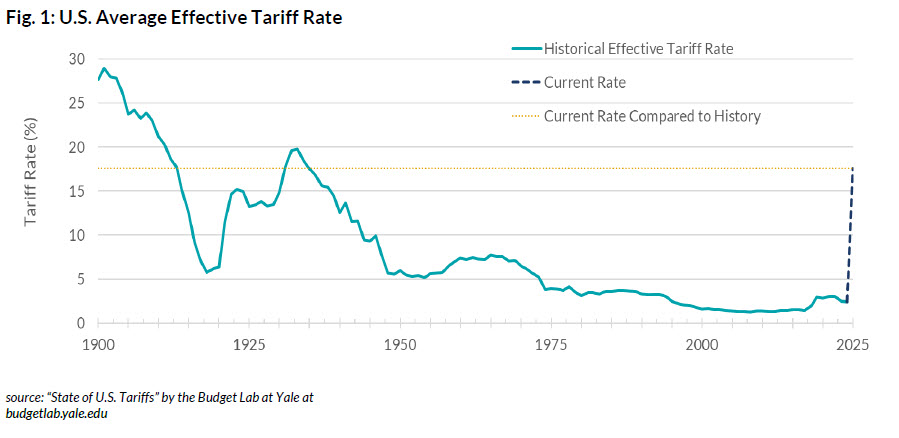

Economic and Market UpdateEconomic Summary: Most indicators of economic activity in the U.S. continued to expand at a decent pace. However, GDP data for the first quarter came in weaker than expected, as higher imports ahead of anticipated tariffs and weaker spending by consumers weighed on Q1 GDP. That said, GDP growth is expected to bounce back in Q2. Tariffs will likely continue to be an evolving story, with potential impacts on both economic growth and inflation. Those impacts will remain uncertain until trade agreements have been finalized.

In early April, President Trump announced larger-than-expected reciprocal tariffs, with the impact most notable on trade with China. However, progress followed with a 90-day pause in tariff implementation. The U.S. then reached trade agreements with the UK, China, and Vietnam. Negotiations with other major trade partners are ongoing. The conflict between Israel and Iran raised inflation concerns, due mostly to the possibility of higher oil prices. Those concerns eased following a ceasefire. Congress passed Trump’s tax cut and spending bill, raising concerns about its potential impact on the U.S. fiscal burden. Meanwhile, U.S. labour market conditions remain resilient, with the unemployment rate remaining low. Inflation has eased slightly but remains above the Federal Reserve’s target. Amid heightened uncertainty, the Federal Reserve held interest rates steady at 4.25%–4.50% at both of its meetings in Q2. Chair Jerome Powell stated that the Fed is “well positioned to wait for greater clarity before considering any adjustments to our policy stance.”

.jpg "Fig-One-(1).jpg")

In Canada, tariffs and trade-related uncertainty continue to weigh on the economy. A pullforward of exports and inventory accumulation ahead of tariffs helped keep first-quarter GDP firm, but growth is expected to slow in the second quarter. The labour market has weakened, particularly in trade-sensitive sectors. Inflation remains within the Bank of Canada’s 1–3% preferred range. However, core CPI remains above the Bank’s preferred 2% target. Canada’s fiscal deficit is expected to widen as Prime Minister Mark Carney aims to fast-track infrastructure development and increase defense spending. Amid ongoing trade uncertainty, the Bank of Canada held its policy rate at 2.75% during its April and June meetings. Governor Tiff Macklem signaled the Bank’s readiness to cut rates further if economic conditions deteriorate.

.jpg "Fig-Two-(1).jpg")

Bond Markets: During Q2, the FTSE Canada Universe Bond Index returned -0.6%. Yields for Canadian bonds rose across all maturities over the quarter. That reflected reduced expectations for rate cuts by the Bank of Canada and a higher risk premium on long-term debt. The impact of higher yields on government bonds was offset in part by tightening of credit spreads on provincial and corporate bonds. Overall corporate bonds saw a positive return for the quarter and outperformed government bonds, in part due to the strong recovery in credit spreads that started in late

April. While corporate issuance slowed considerably in April due to increased trade policy uncertainty, issuance in the Canadian bond markets during May and June were robust. There were 83 deals during Q2 that combined to raise $37 billion for issuers. June 2025 was the 3rd busiest month for issuance on record. We continue to expect higher credit spreads as the U.S. tariffs impact global growth. As such, we have maintained our conservative view with a bias towards shorter corporate bonds but remain ready to invest in longer corporate bonds as valuations become

attractive.

.jpg "Fig-Three-(1).jpg")

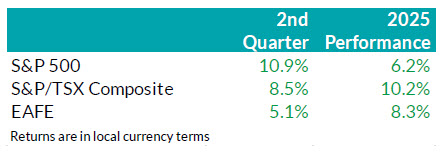

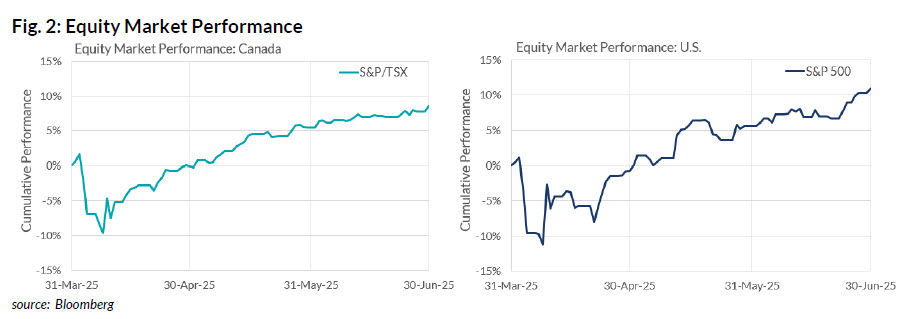

Stock Markets – Overview: Having done a round-trip following April tariff announcements, technology, consumer discretionary and industrial companies propelled the U.S. equity market to another record high. The S&P 500 ended the quarter up about 11%, outperforming Canadian and international markets. Canadian equities gained 8.5% in Q2, buoyed by front-loaded demand that benefited the Materials sector, while Financials recovered from a poor Q1. Meanwhile, as risk sentiment stabilized following the 90-day tariff pause and U.S. equities regained momentum, the appeal of the “Sell America” trade diminished. As a result, Europe, Australasia, and the Far East (EAFE) markets finished the quarter with a more modest gain of just over 5%, lagging the sharper

recovery seen in North America.

.jpg "Fig-Four-(1).jpg")

U.S. Equities: The U.S. equity market staged a V-shaped recovery on strong company earnings data in the second quarter. A stable job market and muted inflation reinforced the view of a resilient U.S. economy. At a company level, we observed positive corporate earnings surprises, steady profit margins and better-than-expected forward earnings guidance. Together they underpinned the equity market’s sharp reversal to the upside. Market breadth also improved over the quarter, with strength extending beyond Technology to include Industrials and Financials. That signalled that the market rally was supported by investors’ confidence in the U.S. economy. Furthermore, structural investment trends in artificial intelligence (AI) continued to accelerate, highlighted by rising enterprise capex in data centres. Beyond AI, Circle, a blockchain-based platform that supports stablecoin issuance, tokenized assets, and digital payment infrastructure, conducted a successful IPO. Its share price jumped 485% from its listing price as of quarter-end. On June 17, the U.S. Senate passed the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act, a regulatory framework for use of tokenized assets. While investors wait for the House’s decision, equity price actions suggest that the policy environment is increasingly supportive of blockchain innovation and digital efficiency.

Canadian Equities: Canadian equities posted solid gains in Q2, with Financials overtaking Materials to lead the market higher. Momentum from the Materials sector, which benefited from the pull-forward demand related to U.S. tariff uncertainty, faded toward quarter-end. Meanwhile, cooling inflation and muted domestic growth pushed investors towards highquality, high-dividend-paying companies. Notably, banks significantly outperformed the broader market, as investors favoured their stable corporate fundamentals. Energy surged briefly amid escalating geopolitical tensions, but those gains proved short-lived. In recap, investors in the Canadian market faced slowing resource demand and a stalling domestic economy, which fueled increased interest in high-quality, high-dividend-paying companies. That is a trend we expect to continue going forward.

Bottom line: Markets remain heavily influenced by sentiment, with U.S. policy developments and ongoing tariff negotiations continuing to cause periodic volatility. However, there is little

evidence of deterioration in the hard data to date. As such, we continue to anchor our positioning on underlying data rather than market narratives. Looking ahead, the combination of a structurally higher-for-longer interest rate environment and increasingly pro-growth policy backdrop presents selective opportunities. In the U.S., this favours highquality growth stocks, particularly within Technology, where strong balance sheets and long-term thematic tailwinds remain intact. In Canada, Financials, especially the relatively inexpensive banks, present a more compelling opportunity as earlier tailwinds from pullforward demand are beginning to wane. While we remain constructive, we are mindful of elevated equity valuations and continue to closely monitor macro conditions and policy developments for signs of inflection.

Downloadable Copy

Mark Warywoda, CFA

VP, Public InvestmentsIan Whiteside, CFA, MBA

AVP, Public InvestmentsJohanna Shaw, CFA

Director, Public InvestmentsJin Li

Director, Equity Investments

Wanyi Chen, CFA, FRM

Sr. Quantitative Analyst

Andrew Vermeer, CFA

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Edward Ng Cheng Hi

Analyst, Credit

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

-

Market Commentary July 2025

Key Takeaways

• Markets were very volatile in April to start Q2 but calmed as the quarter progressed. Volatility was driven mostly by headlines about tariffs, but other fiscal policy developments also had an impact.

• Equity markets sold off sharply at the start of the quarter, continuing Q1’s weakness. Markets rebounded sharply once worst-case fears over tariffs eased. The markets continued to rally through the quarter as trade negotiations progressed. Stronger-thanexpected corporate earnings also boosted markets. Despite the shaky start to the quarter, most global equity markets set new all-time highs in Q2.

• Canadian bond markets delivered slightly negative returns in Q2. Weak performance was driven by rising interest rates, which outweighed the impact of tighter credit spreads. Higher interest rates hurt the performance of longer-term bonds most.

• Both the Bank of Canada and the U.S. Federal Reserve adopted a wait-and-see approach. They each held rates steady during Q2, awaiting greater clarity on the impacts of tariffs on both growth and inflation before considering further cuts.

Economic and Market UpdateEconomic Summary: Most indicators of economic activity in the U.S. continued to expand at a decent pace. However, GDP data for the first quarter came in weaker than expected, as higher imports ahead of anticipated tariffs and weaker spending by consumers weighed on Q1 GDP. That said, GDP growth is expected to bounce back in Q2. Tariffs will likely continue to be an evolving story, with potential impacts on both economic growth and inflation. Those impacts will remain uncertain until trade agreements have been finalized.

In early April, President Trump announced larger-than-expected reciprocal tariffs, with the impact most notable on trade with China. However, progress followed with a 90-day pause in tariff implementation. The U.S. then reached trade agreements with the UK, China, and Vietnam. Negotiations with other major trade partners are ongoing. The conflict between Israel and Iran raised inflation concerns, due mostly to the possibility of higher oil prices. Those concerns eased following a ceasefire. Congress passed Trump’s tax cut and spending bill, raising concerns about its potential impact on the U.S. fiscal burden. Meanwhile, U.S. labour market conditions remain resilient, with the unemployment rate remaining low. Inflation has eased slightly but remains above the Federal Reserve’s target. Amid heightened uncertainty, the Federal Reserve held interest rates steady at 4.25%–4.50% at both of its meetings in Q2. Chair Jerome Powell stated that the Fed is “well positioned to wait for greater clarity before considering any adjustments to our policy stance.”

In Canada, tariffs and trade-related uncertainty continue to weigh on the economy. A pullforward of exports and inventory accumulation ahead of tariffs helped keep first-quarter GDP firm, but growth is expected to slow in the second quarter. The labour market has weakened, particularly in trade-sensitive sectors. Inflation remains within the Bank of Canada’s 1–3% preferred range. However, core CPI remains above the Bank’s preferred 2% target. Canada’s fiscal deficit is expected to widen as Prime Minister Mark Carney aims to fast-track infrastructure development and increase defense spending. Amid ongoing trade uncertainty, the Bank of Canada held its policy rate at 2.75% during its April and June meetings. Governor Tiff Macklem signaled the Bank’s readiness to cut rates further if economic conditions deteriorate.

Bond Markets: During Q2, the FTSE Canada Universe Bond Index returned -0.6%. Yields for Canadian bonds rose across all maturities over the quarter. That reflected reduced expectations for rate cuts by the Bank of Canada and a higher risk premium on long-term debt. The impact of higher yields on government bonds was offset in part by tightening of credit spreads on provincial and corporate bonds. Overall corporate bonds saw a positive return for the quarter and outperformed government bonds, in part due to the strong recovery in credit spreads that started in late

April. While corporate issuance slowed considerably in April due to increased trade policy uncertainty, issuance in the Canadian bond markets during May and June were robust. There were 83 deals during Q2 that combined to raise $37 billion for issuers. June 2025 was the 3rd busiest month for issuance on record. We continue to expect higher credit spreads as the U.S. tariffs impact global growth. As such, we have maintained our conservative view with a bias towards shorter corporate bonds but remain ready to invest in longer corporate bonds as valuations become

attractive.

Stock Markets – Overview: Having done a round-trip following April tariff announcements, technology, consumer discretionary and industrial companies propelled the U.S. equity market to another record high. The S&P 500 ended the quarter up about 11%, outperforming Canadian and international markets. Canadian equities gained 8.5% in Q2, buoyed by front-loaded demand that benefited the Materials sector, while Financials recovered from a poor Q1. Meanwhile, as risk sentiment stabilized following the 90-day tariff pause and U.S. equities regained momentum, the appeal of the “Sell America” trade diminished. As a result, Europe, Australasia, and the Far East (EAFE) markets finished the quarter with a more modest gain of just over 5%, lagging the sharper

recovery seen in North America.

U.S. Equities: The U.S. equity market staged a V-shaped recovery on strong company earnings data in the second quarter. A stable job market and muted inflation reinforced the view of a resilient U.S. economy. At a company level, we observed positive corporate earnings surprises, steady profit margins and better-than-expected forward earnings guidance. Together they underpinned the equity market’s sharp reversal to the upside. Market breadth also improved over the quarter, with strength extending beyond Technology to include Industrials and Financials. That signalled that the market rally was supported by investors’ confidence in the U.S. economy. Furthermore, structural investment trends in artificial intelligence (AI) continued to accelerate, highlighted by rising enterprise capex in data centres. Beyond AI, Circle, a blockchain-based platform that supports stablecoin issuance, tokenized assets, and digital payment infrastructure, conducted a successful IPO. Its share price jumped 485% from its listing price as of quarter-end. On June 17, the U.S. Senate passed the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act, a regulatory framework for use of tokenized assets. While investors wait for the House’s decision, equity price actions suggest that the policy environment is increasingly supportive of blockchain innovation and digital efficiency.

Canadian Equities: Canadian equities posted solid gains in Q2, with Financials overtaking Materials to lead the market higher. Momentum from the Materials sector, which benefited from the pull-forward demand related to U.S. tariff uncertainty, faded toward quarter-end. Meanwhile, cooling inflation and muted domestic growth pushed investors towards highquality, high-dividend-paying companies. Notably, banks significantly outperformed the broader market, as investors favoured their stable corporate fundamentals. Energy surged briefly amid escalating geopolitical tensions, but those gains proved short-lived. In recap, investors in the Canadian market faced slowing resource demand and a stalling domestic economy, which fueled increased interest in high-quality, high-dividend-paying companies. That is a trend we expect to continue going forward.

Bottom line: Markets remain heavily influenced by sentiment, with U.S. policy developments and ongoing tariff negotiations continuing to cause periodic volatility. However, there is little

evidence of deterioration in the hard data to date. As such, we continue to anchor our positioning on underlying data rather than market narratives. Looking ahead, the combination of a structurally higher-for-longer interest rate environment and increasingly pro-growth policy backdrop presents selective opportunities. In the U.S., this favours highquality growth stocks, particularly within Technology, where strong balance sheets and long-term thematic tailwinds remain intact. In Canada, Financials, especially the relatively inexpensive banks, present a more compelling opportunity as earlier tailwinds from pullforward demand are beginning to wane. While we remain constructive, we are mindful of elevated equity valuations and continue to closely monitor macro conditions and policy developments for signs of inflection.

Downloadable Copy

Mark Warywoda, CFA

VP, Public InvestmentsIan Whiteside, CFA, MBA

AVP, Public InvestmentsJohanna Shaw, CFA

Director, Public InvestmentsJin Li

Director, Equity Investments

Wanyi Chen, CFA, FRM

Sr. Quantitative Analyst

Andrew Vermeer, CFA

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Edward Ng Cheng Hi

Analyst, Credit

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

- Reinstatements

-

Faster claims processing on Equitable EZClaim Mobile

Equitable Life now provides real-time processing of massage therapy, physiotherapy and chiropractor claims submitted via the EZClaim® Mobile app.

That means plan members will be able to find out the status of their claim almost instantaneously. And, for approved claims, they will receive payment even sooner – often in as little as 24 hours.

Equitable Life plan members can submit all types of health and dental claims via EZClaim Mobile, including co-ordination of benefits and Health Care Spending Account claims. Currently, 43% of all claims are submitted through the user-friendly app.

“We know plan members love the speed and convenience of EZClaim Mobile,” says Norma Crouse, Assistant Vice-President of Claims and Administration at Equitable Life. “With these enhancements, some claims submitted through the app will be processed and paid even faster.”

We’re also adding biometric login functionality to allow plan members to sign in to the app using their face or fingerprint. And we’ve redesigned our landing page on the mobile app to make it easier for plan members to navigate the various features of the app.

- [pdf] Annuity Settlement Option