Site Search

698 results for browse official page MAKEMUR.COM Paying to get my daughter out of jail now pay later West Virginia

-

Enhancing the Transfer Process: Equitable's New Signature Guarantee Service

Equitable® is making transfers even easier with EZcomplete®.

This enhancement will help advisors and clients by reducing the number of rejections from other institutions that need a signature guarantee. Reducing transfer rejections means less time and effort for advisors, and faster transfers from other institutions.

Signature Guarantees

Equitable will now offer signature guarantees on most transfers requested through EZcomplete.

When is a signature guarantee not available?

• For entity owned accounts

• If a Power of Attorney is signing on behalf of an owner

• If the transferring account has an irrevocable beneficiary

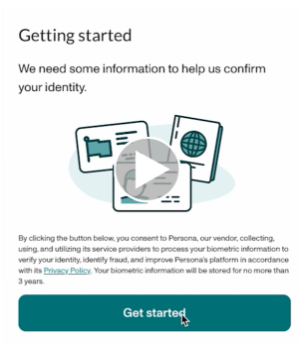

Watch the quick Identity Check with Persona video or read through instructions below.

To offer a signature guarantee, Equitable first needs to check the identity of all owners using Persona, a third-party service provider.

The advisor starts by selecting a signature guarantee in EZcomplete. An email link is sent to all proposed owners.

Clients can click the link within the email to Persona's verification process.

They will be prompted to take a picture of their photo ID and a selfie, turning their head slightly left and right by following the prompts.

Their identity can then be confirmed in seconds.

Sending Transfer Forms:

• If all owners' identities are verified, Equitable will send the transfer form with a signature guarantee stamp and the e-signature audit log to the transferring institution.

• If ID verification fails, clients will be prompted to try up to three times. If still unsuccessful, the transfer form and e-signature audit log is sent to the transferring institution without the signature guarantee stamp.

Handling Issues:

• Advisors’ obligations to verify ID is not affected by this process; ID verification is still required.

• If the client times out or loses the email to access Persona, the advisor can resend the link.

• If the client’s name or email changes after ID verification, the advisor will need to redo the ID verification with the updated information to get a signature guarantee.

This update strives to make processes smoother and more efficient for everyone. Just another reason to do business with Equitable. When we work together, success is mutual.

For more information or assistance, please contact your Director, Investment Sales.

Date published: May 7, 2025 - [pdf] Annuity Settlement Option

-

EZcomplete now displays Critical Illness insurance premiums

We have exciting news about EquiLiving® Critical Illness EZcomplete® applications. Effective April 22, 2023, EZcomplete will calculate and display critical illness insurance premiums automatically! This will save you time during the application process.

EZcomplete will calculate and show both the yearly and monthly premium amounts as you complete the application – this is similar to other Equitable Life insurance products. This means you do not need to run a separate illustration to determine and input the premium amount into EZcomplete anymore.

To learn more about Critical Illness, the Equitable way, visit our Critical Illness page on EquiNet or contact your local wholesaler.

® and TM denote trademarks of The Equitable Life Insurance Company of Canada.

-

December 2023 eNews

Insights on EZBenefits from our Executive Vice-President, Group Insurance

When it comes to advising small business owners, it can be tough to find the right group benefits solution. Offering a competitive benefits plan is more important than ever to help small business owners attract and retain talent. They need an affordable solution that’s easy to implement, renew and maintain.

That’s why we launched EZBenefits for small business earlier this year. It’s a unique group benefits solution designed with you and your small business clients in mind.Marc Avaria, Executive Vice-President, Group Insurance, explains:

Find out more

Visit info.equitable.ca/EZBenefits for more details or to request a quote. If you have questions, contact your Equitable Group Account Executive.

Now that cold and flu season is here, many Canadians will start calling in sick or missing work to visit their doctor – if they can get an appointment. Now’s the time to remind your clients that Equitable offers Dialogue Virtual Healthcare. It can be added to any Equitable plan for an additional cost.

Supporting plan members through cold and flu season with Dialogue Virtual Healthcare*

Eligible plan members and dependants receive fast, on-demand access to virtual primary medical care—24/7, 365 days a year. Available for a variety of non-urgent health concerns, Dialogue Virtual Healthcare can make it easier to navigate cold and flu season by providing:- Access to the largest, most experienced bilingual medical team in Canada,

- In-app prescription renewals and refills,

- Personalized follow-ups after each consultation, and

- An all-in-one patient journey to address health issues. This reduces long waits and means less time away for doctor appointments.

Benefits of Virtual Healthcare for plan sponsors

When your clients provide Virtual Healthcare for their plan members, they can help:- Drive employee engagement;

- Reduce absenteeism related to in-person medical appointments;

- Manage chronic health issues;

- Attract and retain top talent; and

- Build a healthier workforce.

Learn how it works

Adding Dialogue Virtual Healthcare to your clients' plans

To learn more about adding Virtual Healthcare to your clients’ benefits plans, contact your Group Account Executive or myFlex® Account Executive. You can also share this resource from Dialogue on managing cold and flu season.

The Canada Employment Insurance Commission and Canada Revenue Agency have announced the 2024 changes to Maximum Insurable Earnings, and premiums for employment insurance. The following changes to Employment Insurance (EI) will take effect January 1, 2024:

Changes to Short-Term Disability benefits calculations*

How does this affect your clients?

To comply with client policy provisions, Equitable will revise Short-Term Disability (STD) benefits with the updated maximums based on the percentage of EI Maximum Weekly Insurance Earnings for policies that meet these conditions:- Policies that include a STD benefit that is tied to the EI Maximum Weekly Insurable Earnings, and

- Policies with a classification of employees that has less than a $668 maximum.

- The additional premium for any increase from their previous STD amounts and new STD amounts will be shown on your clients’ January 2024 Group Insurance Billings (as applicable).

If your clients wish to provide direction regarding revising their STD maximum, or have questions about the process, they can email Kari Gough, Manager, Group Issue and Special Projects.

*Indicates content that will be shared with your clients. - [pdf] Pivotal Select Application - Registered/Non-Registered

- [pdf] Payout Annuity Advisor Guide

-

Backdating of insurance applications – New rule now in effect

Great news! We are making it even easier for you to do business with Equitable Life®. We now allow backdating of life insurance applications by up to 364 days. Previously, the maximum backdating period was six (6) months.

Backdating can result in lower total premiums for the client over the life of a policy based on their younger age at time of application. But clients must pay all the premiums due for the backdated period up front. Thus, backdating is only beneficial when the total premium savings over the life of the policy are greater than the premium due for the backdated period.

To request backdating beyond six (6) months (up to 364 days)

No special approval is needed. Simply add a note to the Advisor Sheet requesting backdating or contact us at any time prior to policy issue. This step is only necessary when backdating beyond six (6) months as the application will automatically prompt to save age within the 6-month period.

Note: The maximum backdating period for critical illness (CI) applications remains unchanged at three (3) months.

Questions? Please contact your Equitable Life Regional Sales Manager for more information.

-

Crunch The Numbers With Equitable Life’s Savings Calculator

Whether helping your client determine net worth or reviewing to see if your client’s retirement plan is on track, Equitable Life® is here to help with our online calculators. These number crunching tools can help you answer some of those challenging questions you get asked by your clients. From an RSP loan calculator to home budgeting to even figuring out if your client will be a future millionaire, check out our latest tools.

Each week in March, we will be sharing an online calculator from our list.

Share calculators using your Facebook, Twitter or LinkedIn account.-------------------------------------------------------------------------------------------------------

Amina is going to get in the habit of saving by putting $25 a month into her RRSP. Her friends don’t think it is worth the effort. Does it matter how much you contribute?

Did you know?

Consistent investments over several years can be an effective strategy to accumulate wealth. Check out Equitable Life’s Savings Calculator.

- [pdf] Benefits of segregated funds in a TFSA

-

Equitable Life Group Benefits Bulletin – February 2022

In this issue:

- Update: Alberta biosimilar coverage changes*

- Preferred Biosimilar Program*

- Responding to Quebec’s biosimilar policy*

- Dental fee guide updates*

- Reminder: Review manual allocations for HCSAs and/or TSAs*

- Mental health resources for plan members*

Update: Alberta biosimilar coverage changes*

In 2022, Alberta’s provincial drug plan is adding four originator biologics to its Biosimilar Initiative. It has ended or will end provincial coverage of these drugs for some or all conditions, as follows:

Four originator biologics added to Alberta Biosimilar Initiative- Lovenox: Jan. 10, 2022

- Humalog: Feb. 1, 2022

- NovoRapid: April 1, 2022

- Humira: May 1, 2022

Patients 18 and over who are using these drugs for the affected conditions will be required to switch to biosimilar versions of the drugs to maintain coverage under the province’s government drug plan.

How we are responding to protect our clients

To help prevent this change from resulting in additional costs for our clients’ drug plans while still providing plan members with access to safe and effective medications, we will no longer cover these originator biologic drugs for plan members in Alberta.

Effective May 1, 2022, claimants currently taking these drugs will be required to switch to a biosimilar version of the drug to maintain coverage under their Equitable Life plan.

This is a continuation of the Alberta biosimilar switch program we launched last March, when the province first introduced its Biosimilar Initiative.

Do my clients need to take any action?

No action is required by plan sponsors. Plan members taking these targeted originator biologics will be contacted directly to allow them ample time to transition to a biosimilar. Any cost savings associated with the change will be factored in at renewal.

Groups that opted out of the biologic coverage changes we made last March will automatically be opted out of these coverage changes, as well as any future changes to our Alberta biosimilar switch program. This means that their drug plans will continue to provide coverage to existing claimants for any originator biologics we stop covering as part of our biosimilar program.

Advisors with clients who wish to opt out of our Alberta biosimilar program, or who previously opted out and want to opt back in, should speak to their Group Account Executive or myFlex Sales Manager.

Communication to plan members

We will be communicating these coverage changes with affected claimants in early March to allow them ample time to change their prescriptions and avoid any interruptions in their treatment or their coverage. Thus far, the transition to biosimilars, has been smooth and continues to be successful.

What is the difference between biologics and biosimilars?

Biologics are drugs that are engineered using living organisms like yeast and bacteria. The first version of a biologic developed is known as the “originator” biologic. Biosimilars are also biologics. Biosimilars are highly similar to the drugs they are based on and Health Canada considers them to be equally safe and effective for approved conditions.

Questions?

If you have any questions about this change, please contact your Group Account Executive or myFlex Sales Manager.Preferred Biosimilar Program*

As part of our ongoing efforts to help ensure the sustainability of your clients’ drug plans, we continue to engage in strategic partnerships with pharmaceutical manufacturers.

We are pleased to announce a partnership to make Hyrimoz our preferred biosimilar for Humira. This partnership will generate additional savings for plan sponsors.

Plan members will still have the choice to use Humira biosimilars other than Hyrimoz. However, in the absence of alternative sources of reimbursement, this may increase their out-of-pocket amount.

The Preferred Biosimilar Program will take effect March 1, 2022 for all new claimants across Canada who start using a Humira biosimilar. It will take effect May 1 for existing claimants in Alberta who switch to a Humira biosimilar, to align with changes to the provincial plan.

Questions?

If you have any questions about this change, please contact your Group Account Executive or myFlex Sales Manager.Responding to Quebec’s biosimilar policy

Last year, the Quebec government announced it is phasing out coverage of biologic drugs. Beginning April 13, 2022, patients in Quebec using originator biologics will be required to switch to the corresponding biosimilar covered on the province’s public plan in order to maintain coverage.

The following populations are excepted from this new policy:- Pregnant women, who should be transitioned to biosimilars in the 12 months after childbirth.

- Pediatric patients, who should be transitioned to biosimilars in the 12 months after their 18th birthdays.

- Patients who have experienced two or more therapeutic failures while being treated with a biologic drug for the same chronic disease.

We are actively investigating the impact of this new policy on private drug plans in Quebec. We plan to implement further enhancements to our biosimilar programs in Quebec later this year to help prevent this change from resulting in additional costs for our clients’ drug plans. We will provide more details in the coming months.Dental fee guide updates

Each year, Provincial and Territorial Dental Associations publish fee guides. Equitable Life uses these guides to help determine the reimbursement limits for dental procedures. For your reference, below is the list of the average dental fee increases for general practitioners that will be used by Equitable Life for 2022.*

Dental fee guide increases over 2021*

*Data for all provinces and territories was not available at the time of publication. This chart will be updated on EquitableHealth.ca as more information becomes available.Province/Territory Average Fee Increase Alberta 3.9% British Columbia 7.35% Manitoba 5.79% New Brunswick 5.9% Newfoundland and Labrador 5% Nova Scotia 7.05% Northwest Territories 3% Nunavut 3.1% Ontario 4.75% Prince Edward Island 4.75% Quebec 5% Saskatchewan 5.99%

Reminder: Review manual allocations for HCSAs and/or TSAs*

If your client’s Health Care Spending Account (HCSA) and/or Taxable Spending Account (TSA) has manual allocations, they need to allocate these amounts to plan members each year. Please review all your plan members’ profiles on EquitableHealth.ca to ensure they have received their allocation(s) for the current benefit year.

If your clients have Plan Administrator update access on EquitableHealth.ca, they can update these amounts online by doing the following:- Select “View certificate”

- Select “Health Care Spending Account” or “Taxable Spending Account”

- Select “Update Allocation” in Task Center

- Enter amount in “Revised Allocation Amount”

- Override Reason – “Plan Administrator Request”

- Select “Save”

- Select “Reports”

- Select “New”

- Select “Next”

- Select “HCSA” or “TSA Totals by Plan Member”

- Select “Next”

- Enter end date of “12/31/2020”

- Select “Next”

- Select “Finish”

- View “Report”

Mental health resources for plan members*

As the COVID-19 pandemic continues to evolve, many Canadians are experiencing increased levels of stress, anxiety, and depression. Through our partnership with Homewood Health®, all of our clients and their plan members have access to a number of health and wellness resources designed to provide guidance and support. These resources include a number of webinars which discuss various COVID-19 and mental health-related topics. The webinars are pre-recorded so plan members can stream them at their convenience.

Understanding the Impact of COVID-19 on Your Mental Health

English webinar

French webinar

COVID-19: Loneliness & Isolation Fatigue - Self-Care Strategies

English webinar

French webinar

COVID-19: Dealing with Seasonal Affective Disorder

English webinar

French webinar

Reducing Anxiety & Managing the Transition Back to the Classroom - for Teachers

English webinar

French webinar

COVID-19: Specialized Mental Health Support for Health Care Professionals

English webinar

French webinar

COVID-19: Supporting Children’s Mental Health

English webinar

French webinar

Additional resources, including articles, tools, videos and podcasts, are available at Homeweb.ca/Equitable. Please encourage your clients to share these resources with their plan members.