Site Search

601 results for PROBLEMGO.COM pay to make criminal case vanish dark web enter portal instant freedom now

- [pdf] Daily/Guaranteed Interest Account Advisor Guide

- [pdf] Dialogue Virtual Healthcare Overview

-

Equitable Life Group Benefits Bulletin – February 2022

In this issue:

- Update: Alberta biosimilar coverage changes*

- Preferred Biosimilar Program*

- Responding to Quebec’s biosimilar policy*

- Dental fee guide updates*

- Reminder: Review manual allocations for HCSAs and/or TSAs*

- Mental health resources for plan members*

Update: Alberta biosimilar coverage changes*

In 2022, Alberta’s provincial drug plan is adding four originator biologics to its Biosimilar Initiative. It has ended or will end provincial coverage of these drugs for some or all conditions, as follows:

Four originator biologics added to Alberta Biosimilar Initiative- Lovenox: Jan. 10, 2022

- Humalog: Feb. 1, 2022

- NovoRapid: April 1, 2022

- Humira: May 1, 2022

Patients 18 and over who are using these drugs for the affected conditions will be required to switch to biosimilar versions of the drugs to maintain coverage under the province’s government drug plan.

How we are responding to protect our clients

To help prevent this change from resulting in additional costs for our clients’ drug plans while still providing plan members with access to safe and effective medications, we will no longer cover these originator biologic drugs for plan members in Alberta.

Effective May 1, 2022, claimants currently taking these drugs will be required to switch to a biosimilar version of the drug to maintain coverage under their Equitable Life plan.

This is a continuation of the Alberta biosimilar switch program we launched last March, when the province first introduced its Biosimilar Initiative.

Do my clients need to take any action?

No action is required by plan sponsors. Plan members taking these targeted originator biologics will be contacted directly to allow them ample time to transition to a biosimilar. Any cost savings associated with the change will be factored in at renewal.

Groups that opted out of the biologic coverage changes we made last March will automatically be opted out of these coverage changes, as well as any future changes to our Alberta biosimilar switch program. This means that their drug plans will continue to provide coverage to existing claimants for any originator biologics we stop covering as part of our biosimilar program.

Advisors with clients who wish to opt out of our Alberta biosimilar program, or who previously opted out and want to opt back in, should speak to their Group Account Executive or myFlex Sales Manager.

Communication to plan members

We will be communicating these coverage changes with affected claimants in early March to allow them ample time to change their prescriptions and avoid any interruptions in their treatment or their coverage. Thus far, the transition to biosimilars, has been smooth and continues to be successful.

What is the difference between biologics and biosimilars?

Biologics are drugs that are engineered using living organisms like yeast and bacteria. The first version of a biologic developed is known as the “originator” biologic. Biosimilars are also biologics. Biosimilars are highly similar to the drugs they are based on and Health Canada considers them to be equally safe and effective for approved conditions.

Questions?

If you have any questions about this change, please contact your Group Account Executive or myFlex Sales Manager.Preferred Biosimilar Program*

As part of our ongoing efforts to help ensure the sustainability of your clients’ drug plans, we continue to engage in strategic partnerships with pharmaceutical manufacturers.

We are pleased to announce a partnership to make Hyrimoz our preferred biosimilar for Humira. This partnership will generate additional savings for plan sponsors.

Plan members will still have the choice to use Humira biosimilars other than Hyrimoz. However, in the absence of alternative sources of reimbursement, this may increase their out-of-pocket amount.

The Preferred Biosimilar Program will take effect March 1, 2022 for all new claimants across Canada who start using a Humira biosimilar. It will take effect May 1 for existing claimants in Alberta who switch to a Humira biosimilar, to align with changes to the provincial plan.

Questions?

If you have any questions about this change, please contact your Group Account Executive or myFlex Sales Manager.Responding to Quebec’s biosimilar policy

Last year, the Quebec government announced it is phasing out coverage of biologic drugs. Beginning April 13, 2022, patients in Quebec using originator biologics will be required to switch to the corresponding biosimilar covered on the province’s public plan in order to maintain coverage.

The following populations are excepted from this new policy:- Pregnant women, who should be transitioned to biosimilars in the 12 months after childbirth.

- Pediatric patients, who should be transitioned to biosimilars in the 12 months after their 18th birthdays.

- Patients who have experienced two or more therapeutic failures while being treated with a biologic drug for the same chronic disease.

We are actively investigating the impact of this new policy on private drug plans in Quebec. We plan to implement further enhancements to our biosimilar programs in Quebec later this year to help prevent this change from resulting in additional costs for our clients’ drug plans. We will provide more details in the coming months.Dental fee guide updates

Each year, Provincial and Territorial Dental Associations publish fee guides. Equitable Life uses these guides to help determine the reimbursement limits for dental procedures. For your reference, below is the list of the average dental fee increases for general practitioners that will be used by Equitable Life for 2022.*

Dental fee guide increases over 2021*

*Data for all provinces and territories was not available at the time of publication. This chart will be updated on EquitableHealth.ca as more information becomes available.Province/Territory Average Fee Increase Alberta 3.9% British Columbia 7.35% Manitoba 5.79% New Brunswick 5.9% Newfoundland and Labrador 5% Nova Scotia 7.05% Northwest Territories 3% Nunavut 3.1% Ontario 4.75% Prince Edward Island 4.75% Quebec 5% Saskatchewan 5.99%

Reminder: Review manual allocations for HCSAs and/or TSAs*

If your client’s Health Care Spending Account (HCSA) and/or Taxable Spending Account (TSA) has manual allocations, they need to allocate these amounts to plan members each year. Please review all your plan members’ profiles on EquitableHealth.ca to ensure they have received their allocation(s) for the current benefit year.

If your clients have Plan Administrator update access on EquitableHealth.ca, they can update these amounts online by doing the following:- Select “View certificate”

- Select “Health Care Spending Account” or “Taxable Spending Account”

- Select “Update Allocation” in Task Center

- Enter amount in “Revised Allocation Amount”

- Override Reason – “Plan Administrator Request”

- Select “Save”

- Select “Reports”

- Select “New”

- Select “Next”

- Select “HCSA” or “TSA Totals by Plan Member”

- Select “Next”

- Enter end date of “12/31/2020”

- Select “Next”

- Select “Finish”

- View “Report”

Mental health resources for plan members*

As the COVID-19 pandemic continues to evolve, many Canadians are experiencing increased levels of stress, anxiety, and depression. Through our partnership with Homewood Health®, all of our clients and their plan members have access to a number of health and wellness resources designed to provide guidance and support. These resources include a number of webinars which discuss various COVID-19 and mental health-related topics. The webinars are pre-recorded so plan members can stream them at their convenience.

Understanding the Impact of COVID-19 on Your Mental Health

English webinar

French webinar

COVID-19: Loneliness & Isolation Fatigue - Self-Care Strategies

English webinar

French webinar

COVID-19: Dealing with Seasonal Affective Disorder

English webinar

French webinar

Reducing Anxiety & Managing the Transition Back to the Classroom - for Teachers

English webinar

French webinar

COVID-19: Specialized Mental Health Support for Health Care Professionals

English webinar

French webinar

COVID-19: Supporting Children’s Mental Health

English webinar

French webinar

Additional resources, including articles, tools, videos and podcasts, are available at Homeweb.ca/Equitable. Please encourage your clients to share these resources with their plan members.

-

Equitable Life Group Benefits Bulletin - October 2022

Introducing new Gender Affirmation Coverage for group benefits plans

Providing an inclusive benefits plan can play a critical role in fostering a workplace culture that welcomes diversity and helps employees thrive. While most provinces cover the cost of gender-affirming surgery, each person has unique needs. Some may require procedures that are not publicly covered.

That’s why we’re pleased to introduce a new coverage option for gender affirmation surgical procedures that are not covered by provincial health plans. Gender Affirmation Coverage helps plan sponsors to close the gap where provincial health coverage ends.Coverage details and eligibility

Gender Affirmation Coverage can be added to any Equitable Life plan with an in-force Extended Health Care plan. It provides coverage for gender-affirming procedures that are not covered by provincial health plans. This might include tracheal (Adam’s apple) shaving and voice surgery. It will also cover some additional procedures to further align the plan member’s features to the transitioned gender, such as facial bone reduction and cheek augmentation. This makes a wider variety of gender-affirming surgeries accessible to plan members and helps minimize their out-of-pocket costs.

Plan members are eligible for coverage with a diagnosis of gender dysphoria from a qualified health care professional.Offering a more inclusive benefits plan

The coverage provides one more way for your clients to offer more inclusive coverage and to offer holistic support to their plan members undergoing a gender transition. We have developed this coverage as a complement to our existing coverage options, including Health Care Spending Accounts (HCSAs), Taxable Spending Accounts (TSAs), Extended Health Care and drug coverage, and Employee and Family Assistance Programs, all of which can provide support to plan members undergoing gender affirmation.

We regularly review our products to ensure that they’re meeting your clients’ needs, and we’re committed to offering products that support diversity, equity and inclusion.

We also continue to review our forms, documents and processes to make them more inclusive. This includes reviewing our online plan member enrolment (OPME) tool to allow for more flexibility with the way plan members identify their gender.Gender affirmation and mental well-being

Gender affirmation procedures can lead to improved mental health outcomes for those with gender dysphoria, as most report an improvement in their quality of life following the procedures. Gender dysphoria may occur when a person’s assigned sex at birth does not match their identity, and people experiencing gender dysphoria typically report psychological and emotional distress, including symptoms of depression or anxiety. By offering coverage where provincial health coverage ends, your clients can support plan members as they seek procedures that align their body presentation with their self-identified gender.

Advantages at a glance

Advantages for plan members include:- Reimbursement for some procedures and expenses, leading to fewer out-of-pocket costs

- May experience improved mental health outcomes after surgery

- A benefits plan that promotes a culture of diversity, equity and inclusion, which may build employee loyalty

- Support for plan member mental health to help those with gender dysphoria thrive

The Benefits Canada 2022 Health Care Survey results are in!

Equitable Life is proud to be a Platinum sponsor for The Benefits Canada 2022 Health Care Survey, Canada’s leading survey on workplace benefits plans. This year’s survey report highlights many fascinating insights across a wide variety of benefits topics, including:- A focus on mental health for both plan sponsors and plan members

- The repercussions of the "shadow" pandemic due to health care delays

- Trends in plan members' overall perceptions of their health benefits plans

- The types of benefits getting more attention from plan members

- The role of remote work in plan member satisfaction

We’re committed to helping you and your clients navigate the evolving landscape of employee benefits in Canada by contributing to this vibrant industry community. To read the full report, visit Benefits Canada.

HCSA and TSA manual allocation reminder

If your clients’ Health Care Spending Account (HCSA) and/or Taxable Spending Account (TSA) have manual allocations, they need to allocate these amounts to plan members each year. Clients should review their plan members’ profiles on EquitableHealth.ca to ensure they have received their allocation(s) for the current benefit year. Your clients may also order HCSA and TSA forfeiture reports on EquitableHealth.ca.

If your clients have Plan Administrator update access on EquitableHealth.ca, they can update these amounts online by doing the following:- Select View certificate

- Select Health Care Spending Account or Taxable Spending Account

- Select Update Allocation in Task Center

- Enter amount in Revised Allocation Amount

- Override Reason – Plan Administrator Request

- Select Save

- Select Reports

- Select New

- Select Next

- Select HCSA or TSA Totals by Plan Member

- Select Next

- Enter end date of 12/31/2022

- Select Next

- Select Finish

- View Report

- Individual Wealth Marketing Materials

-

NEW MARKETING MATERIAL! Equimax Participating Whole Life, Strong and Stable Dividends

Participating whole life policyholders can get some of the participating account earnings back as dividends.1

Dividend scales change over time. This new marketing piece shows how the actual values of policies look like against those that were estimated. It looks at two sample policies and compares them to the original sales illustrations. One example shows an Equimax Estate Builder® policy. The other example shows an Equimax® Wealth Accumulator® policy.

We are proud of our strong and stable dividend results. We have paid dividends to our participating policyholders every year since 1936. And we’re still going strong!

We want to make sure that we can continue to provide long-term income and growth to support the dividend scale and meet the product guarantees. We do this with constant focus on how we invest and manage risk to support the participating account.

As a mutual life insurance company, we are owned by our policyholders who count on us and our services. Their trust in our knowledge, experience, and financial strength helps us keep our commitments to them—now and in the future.

Dividend scales may change.2 But with a balanced approach, Equitable Life’s Equimax® Participating Whole Life continues to deliver excellent value. It gives guaranteed life insurance protection with the potential for earnings.

Want to learn more? Check out our new marketing piece: Equimax Participating Whole Life, Strong and Stable Dividends (2075).

For more information, reach out to your local wholesaler.

® and TM denote trademarks of The Equitable Life Insurance Company of Canada.

1 Dividends are not guaranteed and are paid at the sole discretion of the Board of Directors. Dividends may be subject to taxation. Dividends will vary based on the actual investment returns in the participating account as well as mortality, expenses, lapse, claims experience, taxes, and other experience of the participating block of policies.

2 If low interest rates continue, investment returns will be lower, and this may mean decreases in the dividend scale in the future. Dividend payments are not guaranteed, but they will never be negative. -

Announcing Equitable Life's National Biosimilar Program

Beginning March 1, 2024, we are expanding our biosimilar switch program nationally** to protect all our clients and to make our coverage consistent across Canada.

Our national biosimilar initiative will simplify drug plan coverage, replacing our provincial programs with one program across the country.

Why now?

Over the past few years, most provinces have introduced policies to delist some originator biologic drugs. They require most patients to switch to biosimilar versions of those drugs to be eligible for coverage under their public drug plans. Soon, it is expected that all provincial drug plans will cover only biosimilars.

In response, we have implemented biosimilar switch initiatives in BC, Alberta, Saskatchewan, Ontario, Quebec, New Brunswick and Nova Scotia to align with these provincial changes. Our initiatives are designed to protect our clients from additional drug costs that may result from these government policies while providing access to equally safe and effective lower cost biosimilars.

How will this affect clients’ drug plans?

Because we have already introduced biosimilar switch initiatives in most provinces, the impact of this change will be minimal. It will primarily affect plan members in provinces or territories where we haven’t already required the switch to biosimilars, and plan members who are taking biosimilars that were not originally included in the switch initiative for their province.

Regardless of where they live, plan members across Canada will no longer be eligible for most originator biologic drugs if they have a condition for which Health Canada has approved a lower cost biosimilar version of the drug. Plan members already taking the originator biologic will be required to switch to a biosimilar version of the drug to maintain coverage under their Equitable plan. We will support their transition with education, personalized communication, and resources.

Will this change affect clients' rates?

Any cost savings associated with the change will be factored in at renewal.

Biologics are drugs that are engineered using living organisms like yeast and bacteria. The first version of a biologic developed is known as the “originator” biologic. Biosimilars are highly similar to the drugs they are based on, and Health Canada considers them to be equally safe and effective for approved conditions.

What is the difference between biologics and biosimilars?

Advance notice

We will be communicating with affected claimants in early December to allow them ample time to change their prescription and avoid any interruptions in their treatment or their coverage.

If you have any questions about this change, please contact your Group Account Executive or myFlex Account Executive.

**Excludes plan members in Quebec who participate in a separate provincial program. -

Streamline your transactions with EZtransact

Skip the forms and submit more transactions digitally with EZtransact® to see how Equitable® has continued to make it easier for you to do business with us.

What’s new with these updates?

One-time PAD functionality for Daily/Guaranteed Interest AccountWith the recent addition of DIA/GIA PAD to EZcomplete, you can now utilize EZtransact for one-time pre-authorized debits. This means faster processing with one-time deposits for investment instructions to either a DIA and/or GIA (multiple terms) with end-of-term instructions.

Key benefits of these enhancements include:

• enhanced rate guarantees to secure the best rates available for clients,

• daily updated interest rate guide informs you of the latest rates,

• interest rate guarantee valid for three business days, for direct deposits from clients.

Be sure to use EZtransact on your next DIA/GIA one-time deposit request to experience these improvements.

.png")

Reduce RSP to RIF conversion timeReduce time and effort submitting Retirement Savings Plan (RSP) to Retirement Income Fund (RIF) conversion requests. EZtransact is continuing to reduce the amount of time it takes advisors to submit conversion requests.

Features include:

• RSP/Spousal RSP to RIF Conversion to effortlessly submit request digitally.

• RIF Calculator to easily calculate your conversions.

Save time with our enhanced digital experience.

Sort & Filter Enhancements

We’ve taken your feedback and made it easier than ever to find the contracts and clients you’re searching for. This improved advisor experience ensures you can:

• Filter “My Clients” By Product Type/ Registration Type

• Sort “My Clients” By Contract Number/ Client Name

• Filter “Transactions” By Transactions Status/ Transaction Type

• Sort “Transactions” By Date.png")

You asked, and we listened! Keep providing us with your feedback on our digital tools. When we grow together, success is mutual.

Get to know EZtransact and accelerate your sales! If you have any questions, please contact your Director, Investment Sales.

Date posted: April 3, 2025 -

Enhancing the Transfer Process: Equitable's New Signature Guarantee Service

Equitable® is making transfers even easier with EZcomplete®.

This enhancement will help advisors and clients by reducing the number of rejections from other institutions that need a signature guarantee. Reducing transfer rejections means less time and effort for advisors, and faster transfers from other institutions.

Signature Guarantees

Equitable will now offer signature guarantees on most transfers requested through EZcomplete.

When is a signature guarantee not available?

• For entity owned accounts

• If a Power of Attorney is signing on behalf of an owner

• If the transferring account has an irrevocable beneficiary

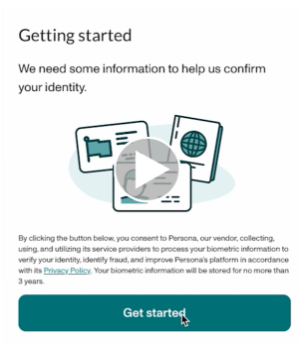

Watch the quick Identity Check with Persona video or read through instructions below.

To offer a signature guarantee, Equitable first needs to check the identity of all owners using Persona, a third-party service provider.

The advisor starts by selecting a signature guarantee in EZcomplete. An email link is sent to all proposed owners.

Clients can click the link within the email to Persona's verification process.

They will be prompted to take a picture of their photo ID and a selfie, turning their head slightly left and right by following the prompts.

Their identity can then be confirmed in seconds.

Sending Transfer Forms:

• If all owners' identities are verified, Equitable will send the transfer form with a signature guarantee stamp and the e-signature audit log to the transferring institution.

• If ID verification fails, clients will be prompted to try up to three times. If still unsuccessful, the transfer form and e-signature audit log is sent to the transferring institution without the signature guarantee stamp.

Handling Issues:

• Advisors’ obligations to verify ID is not affected by this process; ID verification is still required.

• If the client times out or loses the email to access Persona, the advisor can resend the link.

• If the client’s name or email changes after ID verification, the advisor will need to redo the ID verification with the updated information to get a signature guarantee.

This update strives to make processes smoother and more efficient for everyone. Just another reason to do business with Equitable. When we work together, success is mutual.

For more information or assistance, please contact your Director, Investment Sales.

Date published: May 7, 2025 -

This year’s RSP deadline is March 2, 2026

RRSP deposits to be considered for the 2025 tax year must be:

• Dated March 2, 2026, or before

• Must be submitted to Head Office in good order by March 6, 2026, by 4:00 p.m. ET

RRSP applications to be considered for 2025 contribution year must be submitted in good order by:

• March 2, 2026, 11:59 p.m. ET

RRSP B2B Loans:

• RRSP loan deposits must be received from B2B by March 13, 2026, by 4:00 p.m. ET

Note: Transactions submitted after these dates will not receive a 2025 contribution receipt

Please note that all requirements must be received in Head Office by the above dates to guarantee settlement for year end.

Have you started talking to your clients about their Registered Retirement Savings Plan (RRSP) contributions yet? Equitable® has a range of RRSP solutions that can help meet their needs, including:- Daily/Guaranteed Interest Account

- Equitable Guaranteed Investment Funds™, available in:

- o Investment Class (75/75)

- o Estate Class (75/100)

- o Protection Class (100/100)

Most clients genuinely want to save for retirement, but intentions alone aren’t enough—they need a plan. As their trusted advisor, you can help them understand why making their RRSP a priority is an important step toward long‑term financial security.

To support those conversations

Most clients genuinely want to save for retirement, but intentions alone aren’t enough—they need a plan. As their trusted advisor, you can help them understand why making their RRSP a priority is an important step toward long‑term financial security.

To support those conversations, we’ve pulled together helpful tools and marketing materials that show how an Equitable RRSP can make a meaningful difference in reaching their retirement goals. Resources include:- Investment calculators

- A retirement savings plan is just a relevant now as it was over 60 years ago

- Borrowing money to save money

From January 1 to March 2, 2026, when clients open or add money to an Equitable TFSA or RRSP, they’ll automatically be entered into Equitable’s Snowball Your Savings contest. Two lucky clients will win — and their advisors get to celebrate too!