Site Search

265 results for click official MAKEMUR.COM pay for clemency or pardon HMP Channings Wood

- [pdf] Collateral Loan Suitable Candidate Profile

-

February 2020 Advisor eNews

In this issue:

Provincial biosimilar update

Legislative changes for Alberta’s Coverage for Seniors program

Coming soon: enhancements to Equitable EZClaim® Online

Provincial biosimilar update

Alberta Biosimilar Initiative

On December 12, 2019, the Alberta government introduced the launch of the Alberta Biosimilar Initiative. This program will require patients using several originator biologic drugs to switch to a biosimilar, and patients using a non-biologic complex drug (NBCD) to switch to its subsequent entry version before July 1, 2020 in order to maintain coverage.

Biologics are drugs that are engineered using living organisms like yeast and bacteria. The first version of a biologic developed is also known as the “originator” drug. Biosimilars are highly similar to the originator drug they are based on and have been shown to have no clinically meaningful differences in safety or efficacy.

Alberta Health will initially cover both the originator and biosimilar or subsequent entry version of a NBCD drug as patients start the switching process.

The following table outlines the affected originator drugs, their biosimilars or subsequent entry, and the conditions affected by the program.

Biosimilar Drug Originator Biosimilar/Subsequent Entry Indications Affected etanercept Enbrel Brenzys Ankylosing Spondylitis

Rheumatoid ArthritisErelzi Ankylosing Spondylitis

Psoriatic Arthritis

Rheumatoid Arthritisinfliximab Remicade Inflectra

RenflexisAnkylosing Spondylitis

Plaque Psoriasis

Psoriatic Arthritis

Rheumatoid Arthritis

Crohn’s Disease

Ulcerative Colitisinsulin glargine Lantus Basaglar Diabetes (Type 1 and 2) Filgrastim Neupogen Grastofil Neutropenia pegfilgrastim Neulasta Lapelga Neutropenia glatiramer* Copaxone Glatect Multiple Sclerosis *Glatiramer is a non-biologic complex drug where the originator is Copaxone and the subsequent entry is Glatect.

Equitable Life is actively investigating the benefit, risk and appropriate plan changes associated with this new policy on private drug plans and will keep you informed.

For more information about the Alberta Biosimilars Initiative, consult the Alberta government website.

British Columbia

In 2019, BC Pharmacare introduced a Biosimilars Policy that impacted coverage of three biologic drugs – Remicade, Enbrel and Lantus. As of November 25, 2019, these drugs were no longer eligible in BC for most conditions for which lower cost biosimilar versions are available. Patients in the province with these conditions were required to switch to biosimilar versions of these drugs in order to maintain their coverage.

The second phase of the BC Biosimilar Policy takes effect March 6, 2020 when Remicade will be delisted for Crohn’s Disease and Ulcerative Colitis. Patients in the province with these conditions will be required to switch to Inflectra or Renflexis in order to maintain their coverage.

Biosimilar Drug Originator Biosimilar Indications Affected infliximab Remicade Inflectra

RenflexisCrohn’s Disease

Ulcerative ColitisWe have communicated with the affected plan members, informing them of the need to switch medications. If plan members have any questions or concerns, our Customer Care team is here to help and support them through the transition.

If you have any questions about this policy, please contact your Group Account Executive or myFlex Sales Manager.

Ontario

In November 2019 Ontario Minister of Health Christine Elliot indicated that the government was planning to launch consultations to explore solutions in managing biologics.

Equitable Life will continue to monitor these developments and keep you informed of any impact on private drug plans.

Legislative changes for Alberta’s Coverage for Seniors program

The government of Alberta has announced that as of March 1, 2020, seniors’ family members (such as spouses and dependents) who are younger than 65 will no longer be covered by the provincial Coverage for Seniors program. Albertans 65 years of age and older will continue to be covered under the provincial plan.

Equitable Life plan members and their dependents will continue to be covered under the parameters of their group benefits plan.

For more information, please see the Alberta Seniors Health Benefits website.

Coming soon: enhancements to Equitable EZClaim® Online

Faster vision claims processing and payment

Equitable Life will soon provide real-time processing of vision claims submitted via EZClaim Online.

This means plan members will be able to find out the status of their vision claim almost instantaneously. And, for approved claims, they will receive payment even sooner – often in as little as 24 hours.

In order to allow for instantaneous processing and faster payment, plan members will be prompted to enter some additional information including the practitioner’s name, the date of the expense, the type of expense and amount of the expense when submitting their claims for these services.

Equitable Life plan members can submit all vision claims via EZClaim, including coordination of benefits and Health Care Spending Account claims.

This enhancement will be coming to our EZClaim Mobile app in the coming months.

New printable claims extract

As part of our ongoing efforts to improve customer experience for plan members, we will also offer a claims extract in a printable format within the plan member site. Plan members will be able to select a date range and claimant, then generate and download a detailed list of health and dental claims. This is a helpful way to keep track of claims, especially when reviewing them in preparation for income tax filing.

Once these enhancements are live you will be notified in an eNews, and an announcement will be posted on the plan member section of EquitableHealth.ca.

Elimination of Out-of-Country Travellers Program in Ontario

Effective January 1, 2020, the Ontario government eliminated OHIP coverage for emergency services for Ontarians travelling outside of Canada.

Previously, the Out-of-Country Travelers Program provided some reimbursement for services required to treat conditions that are acute, unexpected, arose outside Canada and require immediate treatment. The program covered between $200 and $400 per day for inpatient services and $50 per day for outpatient and doctor services.

For groups who have out-of-country coverage from Allianz, this change will not impact the cost to your plan members, or the process plan members follow in the event of an emergency while travelling.

Plan members should still call Allianz in the event of an out of country emergency. Allianz will deal with their claim as usual and will now pay for the portion of the claim previously paid by OHIP. Plan members will not have any additional out-of-pocket costs.

We will be sharing this information with plan members as a news item on our plan member website, equitablehealth.ca.

- [pdf] FundSERV - Schedule "B" Commission Schedule

- Cost Transparency: Why Preparation Matters

-

May 2026 eNews

In this issue:

-

Save the date: Group benefits advisor roadshow is returning to a city near you

-

One-time passcodes will be added to our login experience this week*

-

Delisted service providers: What clients need to know*

-

Keeping plan member information up to date*

*Indicates content we will share with your clients.

Save the date: Group benefits advisor roadshow is returning to a city near you

Mark your calendars—our annual group benefits advisor roadshow will be travelling across Canada this fall.

Watch your inbox for an invitation with more details soon. In the meantime, here’s our full list of event dates and cities.

-

Monday, Sept. 28 – Vancouver, BC

-

Tuesday, Sept. 29 – Edmonton, AB

-

Wednesday, Sept. 30 – Calgary, AB

-

Thursday, Oct. 1 – Saskatoon, SK

-

Friday, Oct. 2 – Winnipeg, MB

-

Tuesday, Oct. 6 – Halifax, NS

-

Wednesday, Oct. 7 – Ottawa, ON

-

Thursday, Oct. 8 – Markham, ON

-

Tuesday, Oct. 20 – London, ON

-

Wednesday, Oct. 21 – Kitchener, ON

-

Thursday, Oct. 22 – Oakville, ON

One-time passcodes will be added to our login experience this week

Starting next week, anyone who logs in to EquitableHealth.ca® or the Equitable EZClaim® mobile app with an email address and password may also need to enter a one-time passcode to access their account. The one-time passcode will be provided by email.

Adding this form of multi-factor authentication (MFA) to our login process will further enhance our digital security and help safeguard your account and our clients’ personal data.

Don’t forget—you can create a passkey instead.

Passkeys are another form of MFA. They provide a quick, easy and secure way to access your account, using either biometrics—your face or fingerprint—or a PIN authenticator to confirm your identity.

Anyone who uses a passkey to log in to their account will never be required to enter a one-time passcode.

In case you get questions…

If a client asks you about these changes to our login process, consider sharing this fact sheet with them. The fact sheet highlights the value of adding MFA to the login process and describes the differences between logging in with a one-time passcode versus a passkey.

More information about one-time passcodes and passkeys is included at equitable.ca/effortless. There, you’ll also find short videos that show how easy it is to create a passkey on your mobile device and computer.

Please reach out to your Group Account Executive if you have any questions.

If you use the same email address to log in to your accounts on EquitableHealth.ca, EquiNet® and Equitable Client Access®, you can use the same passkey. Equitable Client Access is our secure site for Individual Insurance and Individual Wealth clients.

Delisted service providers: What clients need to know

Protecting clients’ group benefits plans is our priority. That’s why we regularly assess healthcare service providers, clinics, facilities and medical suppliers in our network. These reviews help ensure the claims plan members submit meet eligibility requirements.

If our review indicates a provider is not meeting those requirements, we may delist them.

Common reasons we delist providers include:

-

Billing for services that weren’t provided or aren’t medically required

-

Changing information about treatments provided (e.g., service dates or patient names)

-

Incomplete records or treatment notes

-

Lack of cooperation with an audit

-

Suspension of the provider by their licensing college or association

-

Criminal convictions

What clients need to know

If a provider is delisted, we will not accept or process claims for services or supplies they provide. However, plan members can still choose to use delisted providers at their own expense.

We provide clients instructions on where to find our current list of delisted providers in each Plan Administrator eNews announcement. We also encourage them to share the list with their plan members.

Whenever we delist a provider, we try to contact plan members, who have recently submitted claims for their services, to inform them of the change and help prevent future claim submissions. However, plan members are responsible for checking our list of delisted providers before purchasing any product or service to avoid having to pay at their expense. The list is available on EquitableHealth.ca.

If you have questions about our list of delisted service providers or our process of reviewing providers, please contact your Group Account Executive.

Keeping plan member information up to date

Keeping plan member information current helps ensure accurate benefits coverage and premium calculations.

When a plan member’s earnings or occupation changes, the plan administrator must update this information as soon as possible. Updates made before a benefits plan renewal helps ensure renewals are based on current data.

If a plan includes short-term disability (STD) or long-term disability (LTD) benefits, outdated earning information can affect disability claim payments for plan members.

We send an annual reminder to plan administrators before renewal. The email includes step-by-step instructions on how to review and update plan members’ earnings and occupation information.

Three ways to update earnings and occupation information

Plan administrators can review and update plan members’ information by either:

-

Making updates directly through the plan administrator site (update access required),

-

Generating an earnings and occupations worksheet through the plan administrator site (online reporting access required), or

-

Requesting a worksheet by emailing groupbenefitsadmin@equitable.ca.

The worksheet includes instructions on how to submit completed updates to us. If you have any questions, please contact your Client Relationship Specialist or email groupbenefitsadmin@equitable.ca.

-

- [pdf] First Home Savings Account

- [pdf] Annuity Settlement Option

- Brandes

-

Market Commentary January 2025

Key Takeaways

Full year 2024:

-

Despite reductions of policy-setting interest rates by central banks, yields on longer-term bonds finished the year higher than they started the year.

-

Positive risk appetite helped corporate bonds perform well, led by lower-quality issuers.

-

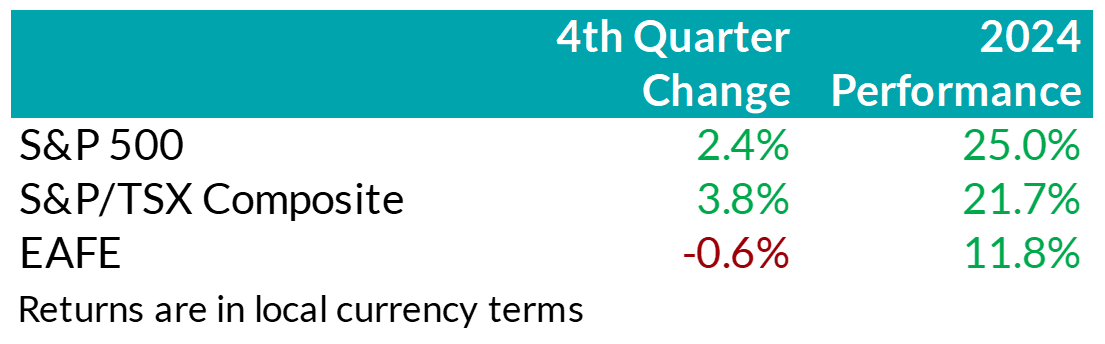

Global equity markets posted robust returns, with U.S. equities outperforming other developed markets, driven by heavy concentration into the ‘Magnificent 7’ stocks.

Fourth Quarter:

-

Central banks continued to ease monetary policy in Q4, with the Bank of Canada cutting its policy interest rate more aggressively than did the U.S. Federal Reserve.

-

The Republican victory across both the executive and legislative branches in the U.S. ignited expectations of economic growth, pushing bond yields and stock prices higher.

-

Risk sentiment helped corporate bonds continue to outperform government bonds.

-

Markets remained volatile: while North American stock markets continued to outperform most international indices, Canadian stocks managed to outperform U.S. stocks in Q4, as sources of returns in the U.S. narrowed into year-end.

Economic and Market Update

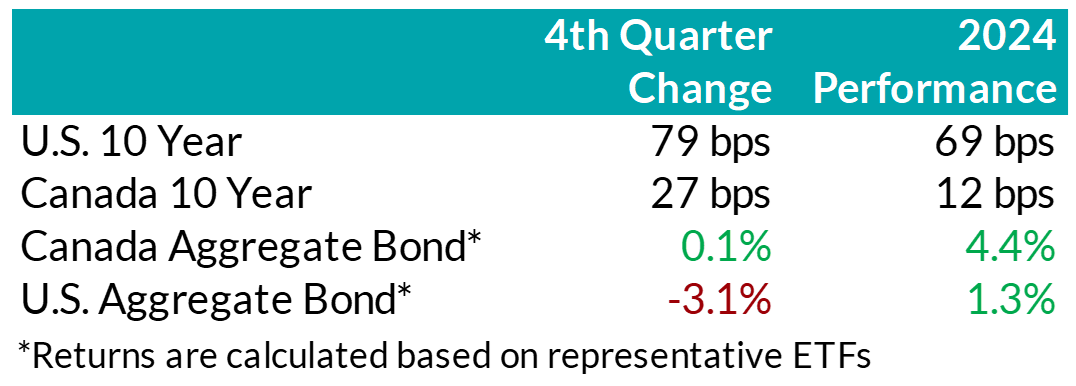

Economic Summary: In the U.S., economic activity continued to expand at a solid pace in Q4. The rate of inflation continued to slow but remained above the central bank’s 2% objective. The labour market in the U.S. remained resilient, as the unemployment rate has remained low compared to historical norms. A decisive victory for Donald Trump and the Republican Party further boosted expectations for continued growth. The return of the President-elect’s old tactics of threatening tariffs to influence trade, security, and drug control re-introduced some economic uncertainty, particularly regarding the potential return of inflationary pressures. Those concerns prompted the Federal Reserve to slow the pace of its policy easing, as it lowered rates by just 0.25% at each of its two meetings in Q4, following the 0.50% cut in September. Throughout 2024, the Fed reduced rates by a total of 100 basis points, from 5.50% to 4.50%. Nonetheless, bond yields were significantly higher for most maturity terms during the fourth quarter as the market priced in not just a stronger economy than had been the expectation during Q3, implying less interest rate cuts by the Fed, but also growing concerns about the government deficit.

In Canada, growth remained positive during 2024 and improved a bit to close the year, but continued to fall short of the Bank of Canada’s expectations. Similarly, inflation came in lower than expected and below the Bank’s 2% target. The labour market continued to soften for much of the year, with employment growth falling short of labour force growth. The weakness in the labour market and economy, along with tamed inflation, prompted the Central Bank to cut rates at the pace of 50 basis points at each of its two meetings in Q4. For the full year, the Bank of Canada ended up lowering its policy rate by a total of 175 basis points, from 5% to 3.25%. The market has been expecting the Bank of Canada to need to continue cutting rates due to slower economic growth in Canada, but the fear of a possible trade war with the U.S. has made the economic outlook somewhat murkier.

.png "Chart1-(1).png")

Bond Markets: During the quarter, yields on mid- to long-term bonds in Canada rose in sympathy with rising bond yields in the U.S. However, bond yields in Canada rose to a lesser extent, and yields on shorter-term bonds were actually little changed over the quarter. The FTSE Canada Universe Bond Index was basically flat during Q4 and posted a return of 4.2% for the full year. Although interest rates rose, credit spreads (i.e. the extra yield on corporate bonds versus government bonds to compensate for their extra risk) continued to grind lower, helping corporate bonds post positive overall returns in the quarter. Tightening credit spreads reflected the generally positive risk-on tone to the market, despite some volatility. Lower-rated BBB bonds generally performed better than higher-quality A-rated bonds. Credit spreads have now generally fallen back to levels similar to those experienced in 2021, when markets did quite well after the pandemic. The on-going appetite of investors for the extra yield offered by corporate bonds over government bonds is indicated not just by falling credit spreads, but also by investors’ enthusiasm to support the primary issuance market. Corporate bond supply continued to be very robust in the quarter, with $30 billion in new issuance, resulting in a record-breaking year with $141 billion of new issuance in 2024. Nonetheless, on balance, we do not think the current risk premium adequately compensates for downside risk, particularly in longer-dated corporate bonds, and have a bias towards shorter-dated credit where we view the risk / reward trade-off as being more favourable.

.png "Chart2-(1).png") Stock Markets – Overview: Trump’s presidential victory and the Republican party’s ‘red sweep’ in the Senate and House of Representatives sparked optimism surrounding economic growth and a new era of U.S. exceptionalism. As a result, North American equity markets extended their rally in Q4, capping off a year of robust returns. The S&P 500 returned 2.4%, bringing its year-to-date return to 25%. Within the U.S., the broadening of returns paused during the quarter as the chase for growth intensified, with mega-cap growth names like Tesla driving performance. Canadian equities surprisingly outperformed the U.S. market over the quarter, returning 3.8% in Q4, despite threats of widespread tariff negotiations looming on the horizon that could negatively impact Canadian corporate fundamentals. At a sector level, strength in the technology, financials, and energy sectors more than offset weakness in telecommunication companies as well as in the materials sector. Elsewhere, major developed markets from Europe and Asia (EAFE) underperformed last quarter as deteriorating Chinese growth prospects and weak economic growth in the Eurozone weighed on equities. Notably, foreign investors of U.S. denominated securities benefitted from a rebounding U.S. dollar with the dollar index adding over 7.6% in Q4.

Stock Markets – Overview: Trump’s presidential victory and the Republican party’s ‘red sweep’ in the Senate and House of Representatives sparked optimism surrounding economic growth and a new era of U.S. exceptionalism. As a result, North American equity markets extended their rally in Q4, capping off a year of robust returns. The S&P 500 returned 2.4%, bringing its year-to-date return to 25%. Within the U.S., the broadening of returns paused during the quarter as the chase for growth intensified, with mega-cap growth names like Tesla driving performance. Canadian equities surprisingly outperformed the U.S. market over the quarter, returning 3.8% in Q4, despite threats of widespread tariff negotiations looming on the horizon that could negatively impact Canadian corporate fundamentals. At a sector level, strength in the technology, financials, and energy sectors more than offset weakness in telecommunication companies as well as in the materials sector. Elsewhere, major developed markets from Europe and Asia (EAFE) underperformed last quarter as deteriorating Chinese growth prospects and weak economic growth in the Eurozone weighed on equities. Notably, foreign investors of U.S. denominated securities benefitted from a rebounding U.S. dollar with the dollar index adding over 7.6% in Q4.

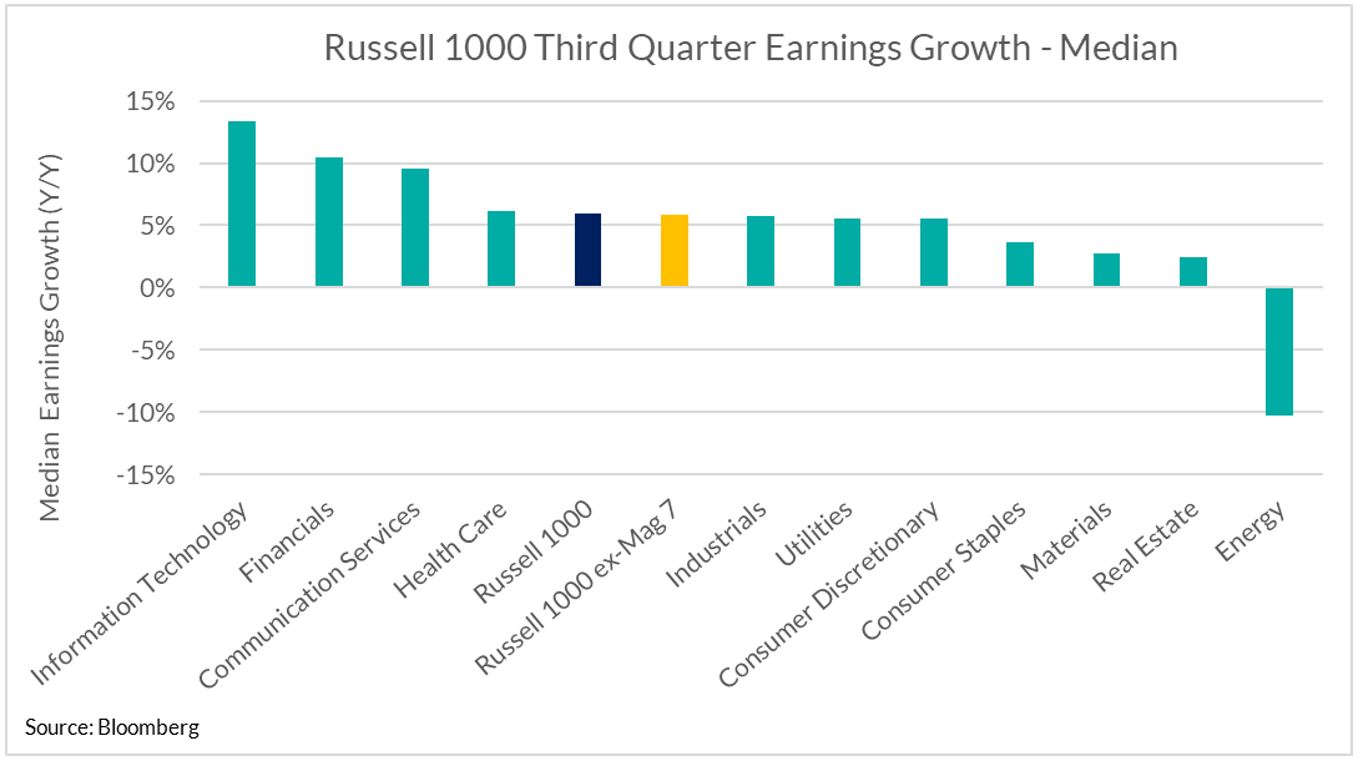

.png "Chart3-(1).png") U.S. Equities: U.S. equities remain supported by resilient margins and strong corporate earnings growth with over 70% of businesses surpassing bottom-line expectations last quarter. We remain attentive to the broadening of earnings performance and note that this trend has continued, albeit at a normalized pace versus prior quarters. More specifically, our work shows that members of the Russell 1000, excluding the Magnificent 7, posted median earnings growth of 6% last quarter, down from nearly 9% in Q3 but comparable to Q2 (6%). Looking forward to 2025, analysts continue to forecast U.S. exceptionalism, with forecasts of ~12% earnings growth.

U.S. Equities: U.S. equities remain supported by resilient margins and strong corporate earnings growth with over 70% of businesses surpassing bottom-line expectations last quarter. We remain attentive to the broadening of earnings performance and note that this trend has continued, albeit at a normalized pace versus prior quarters. More specifically, our work shows that members of the Russell 1000, excluding the Magnificent 7, posted median earnings growth of 6% last quarter, down from nearly 9% in Q3 but comparable to Q2 (6%). Looking forward to 2025, analysts continue to forecast U.S. exceptionalism, with forecasts of ~12% earnings growth.

Following Trump’s presidential victory, stocks with greater sensitivity to the U.S. economy, such as small cap businesses, benefitted from expectations of domestically focused growth initiatives. However, stubborn inflation and expectations of fewer interest rate cuts by the Federal Reserve saw the trend of broadening sources of returns pause into the end of the year. Instead, market concentration reaccelerated with investors rushing back towards mega-cap growth stocks. In fact, Tesla – which is approximately 2% of the S&P 500 Index by market cap – contributed approximately one-third of the total index return in Q4, while the Mag 7 as a group contributed over 100% of total returns. In other words, U.S. large cap companies excluding the Magnificent 7 declined in aggregate last quarter.

Canadian Equities: Against the backdrop of cooling inflation and below-trend growth, the Bank of Canada continued to loosen monetary policy. As a result, Canadian companies

showed signs of improving efficiency with return on equity – a gauge of corporate profitability – improving versus prior quarters. Under these conditions, investors remained focused on higher quality, high-dividend paying companies – particularly within the financial sector. Relative to prior quarters, this group witnessed greater contribution out of non-bank financials (such as asset managers and insurance companies), as the premium investors were willing to pay for Canadian banks remained elevated. Across other sectors, the energy sector had a positive quarter as the price of oil stabilized, but falling prices for raw industrials pushed the materials sector lower.

Bottom line: U.S. political developments and subsequent growth expectations dominated market sentiment last quarter. As a result, investors dialed back rate cut expectations and bond yields moved higher. In equity markets, the potential for an era of higher-for-longer rates prompted a resumption of investors crowding into growth stocks. Going forward, we remain cautious of elevated valuations and continue to prioritize diversified sources of returns with a long-term outlook. Nonetheless, despite rich valuations, our base case remains that investors’ enthusiasm for equities will persist in the near-term and stocks should continue to outperform bonds.

Downloadable Copy

ADVISOR USE ONLYMark Warywoda, CFA

VP, Public Portfolio ManagementIan Whiteside, CFA, MBA

AVP, Public Portfolio ManagementJohanna Shaw, CFA

Director, Portfolio ManagementJin Li

Director, Equity Portfolio Management

Tyler Farrow, CFA

Senior Analyst, Equity

Andrew Vermeer

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Francie Chen

Analyst, Rates

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

-

- [pdf] Termination for Internal Replacement