Site Search

354 results for view portal now MAKEMUR.com bribe a judge for a lighter sentence in court

-

NEW MARKETING MATERIAL! Equimax Participating Whole Life, Strong and Stable Dividends

Participating whole life policyholders can get some of the participating account earnings back as dividends.1

Dividend scales change over time. This new marketing piece shows how the actual values of policies look like against those that were estimated. It looks at two sample policies and compares them to the original sales illustrations. One example shows an Equimax Estate Builder® policy. The other example shows an Equimax® Wealth Accumulator® policy.

We are proud of our strong and stable dividend results. We have paid dividends to our participating policyholders every year since 1936. And we’re still going strong!

We want to make sure that we can continue to provide long-term income and growth to support the dividend scale and meet the product guarantees. We do this with constant focus on how we invest and manage risk to support the participating account.

As a mutual life insurance company, we are owned by our policyholders who count on us and our services. Their trust in our knowledge, experience, and financial strength helps us keep our commitments to them—now and in the future.

Dividend scales may change.2 But with a balanced approach, Equitable Life’s Equimax® Participating Whole Life continues to deliver excellent value. It gives guaranteed life insurance protection with the potential for earnings.

Want to learn more? Check out our new marketing piece: Equimax Participating Whole Life, Strong and Stable Dividends (2075).

For more information, reach out to your local wholesaler.

® and TM denote trademarks of The Equitable Life Insurance Company of Canada.

1 Dividends are not guaranteed and are paid at the sole discretion of the Board of Directors. Dividends may be subject to taxation. Dividends will vary based on the actual investment returns in the participating account as well as mortality, expenses, lapse, claims experience, taxes, and other experience of the participating block of policies.

2 If low interest rates continue, investment returns will be lower, and this may mean decreases in the dividend scale in the future. Dividend payments are not guaranteed, but they will never be negative. -

Announcing Equitable Life's National Biosimilar Program

Beginning March 1, 2024, we are expanding our biosimilar switch program nationally** to protect all our clients and to make our coverage consistent across Canada.

Our national biosimilar initiative will simplify drug plan coverage, replacing our provincial programs with one program across the country.

Why now?

Over the past few years, most provinces have introduced policies to delist some originator biologic drugs. They require most patients to switch to biosimilar versions of those drugs to be eligible for coverage under their public drug plans. Soon, it is expected that all provincial drug plans will cover only biosimilars.

In response, we have implemented biosimilar switch initiatives in BC, Alberta, Saskatchewan, Ontario, Quebec, New Brunswick and Nova Scotia to align with these provincial changes. Our initiatives are designed to protect our clients from additional drug costs that may result from these government policies while providing access to equally safe and effective lower cost biosimilars.

How will this affect clients’ drug plans?

Because we have already introduced biosimilar switch initiatives in most provinces, the impact of this change will be minimal. It will primarily affect plan members in provinces or territories where we haven’t already required the switch to biosimilars, and plan members who are taking biosimilars that were not originally included in the switch initiative for their province.

Regardless of where they live, plan members across Canada will no longer be eligible for most originator biologic drugs if they have a condition for which Health Canada has approved a lower cost biosimilar version of the drug. Plan members already taking the originator biologic will be required to switch to a biosimilar version of the drug to maintain coverage under their Equitable plan. We will support their transition with education, personalized communication, and resources.

Will this change affect clients' rates?

Any cost savings associated with the change will be factored in at renewal.

Biologics are drugs that are engineered using living organisms like yeast and bacteria. The first version of a biologic developed is known as the “originator” biologic. Biosimilars are highly similar to the drugs they are based on, and Health Canada considers them to be equally safe and effective for approved conditions.

What is the difference between biologics and biosimilars?

Advance notice

We will be communicating with affected claimants in early December to allow them ample time to change their prescription and avoid any interruptions in their treatment or their coverage.

If you have any questions about this change, please contact your Group Account Executive or myFlex Account Executive.

**Excludes plan members in Quebec who participate in a separate provincial program. -

Celebrating our most popular Pivotal Select funds

In August 2022, Equitable® launched 12 new segregated funds in Pivotal Select’s Investment Class (75/75). We wanted to bring some new innovative solutions to the product, including six sustainable investment funds. To say the launch of these funds was successful would be an understatement.

The funds are quickly becoming some of the most popular funds in Pivotal Select™, and their performance in 2023 was impressive. Equitable wants to celebrate these funds and encourage clients to consider them for their portfolios.

As of February 29, 2024, nine out of the 12 funds received a 1st quartile ranking for their 1-year return and two more were 2nd quartile. The table below shows the new funds that ranked in the top two quartiles for their 1-year returns.

Access additional fund performance information

If you haven’t looked at these funds yet, now is the time. Speak to clients about their investment options and see if these funds fit within their investment portfolio.

Talk to your Director, Investment Sales today for more information.Disclaimer

Any amount that is allocated to a segregated fund is invested at the risk of the contractholder and may increase or decrease in value. Segregated fund values change frequently, and past performance does not guarantee future results. Investors do not purchase an interest in underlying securities or funds, but rather, an individual variable insurance contract issued by The Equitable Life Insurance Company of Canada. There are risks involved with investing in segregated funds. Please read the Contract and Information Folder before investing for a description of risks relevant to each segregated fund and for a complete description of product features and guarantees. Copies of the Contract and Information Folder are available on equitable.ca.

Management Expense Ratios (MERs) are based on figures as of February 29, 2024, and are unaudited. MERs may vary at any time. The MER is the combination of the management fee, insurance fee, operating expenses, HST, and any other applicable non-income tax for the fund and for the underlying fund. For clients with larger contract values, a Management Fee Reduction may be available through the Preferred Pricing Program. For details, please see the Pivotal Select Contract and Information Folder.

® and TM denote trademarks of The Equitable Life Insurance Company of Canada.

Posted April 18, 2024

-

Streamline your transactions with EZtransact

Skip the forms and submit more transactions digitally with EZtransact® to see how Equitable® has continued to make it easier for you to do business with us.

What’s new with these updates?

One-time PAD functionality for Daily/Guaranteed Interest AccountWith the recent addition of DIA/GIA PAD to EZcomplete, you can now utilize EZtransact for one-time pre-authorized debits. This means faster processing with one-time deposits for investment instructions to either a DIA and/or GIA (multiple terms) with end-of-term instructions.

Key benefits of these enhancements include:

• enhanced rate guarantees to secure the best rates available for clients,

• daily updated interest rate guide informs you of the latest rates,

• interest rate guarantee valid for three business days, for direct deposits from clients.

Be sure to use EZtransact on your next DIA/GIA one-time deposit request to experience these improvements.

.png")

Reduce RSP to RIF conversion timeReduce time and effort submitting Retirement Savings Plan (RSP) to Retirement Income Fund (RIF) conversion requests. EZtransact is continuing to reduce the amount of time it takes advisors to submit conversion requests.

Features include:

• RSP/Spousal RSP to RIF Conversion to effortlessly submit request digitally.

• RIF Calculator to easily calculate your conversions.

Save time with our enhanced digital experience.

Sort & Filter Enhancements

We’ve taken your feedback and made it easier than ever to find the contracts and clients you’re searching for. This improved advisor experience ensures you can:

• Filter “My Clients” By Product Type/ Registration Type

• Sort “My Clients” By Contract Number/ Client Name

• Filter “Transactions” By Transactions Status/ Transaction Type

• Sort “Transactions” By Date.png")

You asked, and we listened! Keep providing us with your feedback on our digital tools. When we grow together, success is mutual.

Get to know EZtransact and accelerate your sales! If you have any questions, please contact your Director, Investment Sales.

Date posted: April 3, 2025 -

Enhancing the Transfer Process: Equitable's New Signature Guarantee Service

Equitable® is making transfers even easier with EZcomplete®.

This enhancement will help advisors and clients by reducing the number of rejections from other institutions that need a signature guarantee. Reducing transfer rejections means less time and effort for advisors, and faster transfers from other institutions.

Signature Guarantees

Equitable will now offer signature guarantees on most transfers requested through EZcomplete.

When is a signature guarantee not available?

• For entity owned accounts

• If a Power of Attorney is signing on behalf of an owner

• If the transferring account has an irrevocable beneficiary

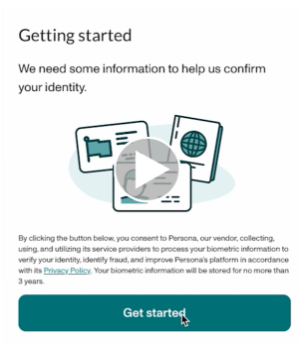

Watch the quick Identity Check with Persona video or read through instructions below.

To offer a signature guarantee, Equitable first needs to check the identity of all owners using Persona, a third-party service provider.

The advisor starts by selecting a signature guarantee in EZcomplete. An email link is sent to all proposed owners.

Clients can click the link within the email to Persona's verification process.

They will be prompted to take a picture of their photo ID and a selfie, turning their head slightly left and right by following the prompts.

Their identity can then be confirmed in seconds.

Sending Transfer Forms:

• If all owners' identities are verified, Equitable will send the transfer form with a signature guarantee stamp and the e-signature audit log to the transferring institution.

• If ID verification fails, clients will be prompted to try up to three times. If still unsuccessful, the transfer form and e-signature audit log is sent to the transferring institution without the signature guarantee stamp.

Handling Issues:

• Advisors’ obligations to verify ID is not affected by this process; ID verification is still required.

• If the client times out or loses the email to access Persona, the advisor can resend the link.

• If the client’s name or email changes after ID verification, the advisor will need to redo the ID verification with the updated information to get a signature guarantee.

This update strives to make processes smoother and more efficient for everyone. Just another reason to do business with Equitable. When we work together, success is mutual.

For more information or assistance, please contact your Director, Investment Sales.

Date published: May 7, 2025 - Exchanges

-

New Year, New Opportunities—Explore Equitable’s Competitive Term Life Solution

The new year brings new opportunities to help clients feel confident about their financial future. Equitable’s term rates are among the best on LifeGuide in key markets*, combined with our flexibility and support, making us a great choice for clients. Run an illustration now!

Why choose Equitable for term life insurance?

• Great rates – we’ve recently repriced! On average, we reduced our monthly term rates by 5%. Check out our great term rates for yourself. Tip! For best term rates, choose monthly premiums.

• Flexibility to change the term plan** – life is always changing, and so do life insurance needs. Offer clients the flexibility to:

• Exchange term plans: from Term 10 to Term 20 or Term 30/65. They can also exchange from Term 20 to Term 30/65.

• Convert to permanent coverage: Offer clients the security of changing their term plan to any of our permanent plans without underwriting.

• Partial term conversion with term rider carryover: Convert part of the term coverage into permanent protection and carry over the remaining coverage as any term rider plan.

• Extra support when it matters most – our KIND® program offers a suite of benefits for clients and their families. This reflects our deep commitment to standing by them when it matters most.

Build client relationships with trusted protection

This year, and every year, strengthen your client relationships by choosing Equitable for term life protection. With our flexible solutions, innovative features, and unwavering support, you can help clients move forward with confidence.

Start the year off by helping clients meet their insurance needs with a term plan.

Run a quote today!

Contact your Equitable wholesaler today to learn more!

*Effective November 22, 2025. Our monthly term rates are ranked among the best on LifeGuide when compared against top carriers in key markets.

** Administrative rules and age limits apply to exchanges and conversions. Please see the policy for details. The policy governs in all cases.

-

This year’s RSP deadline is March 2, 2026

RRSP deposits to be considered for the 2025 tax year must be:

• Dated March 2, 2026, or before

• Must be submitted to Head Office in good order by March 6, 2026, by 4:00 p.m. ET

RRSP applications to be considered for 2025 contribution year must be submitted in good order by:

• March 2, 2026, 11:59 p.m. ET

RRSP B2B Loans:

• RRSP loan deposits must be received from B2B by March 13, 2026, by 4:00 p.m. ET

Note: Transactions submitted after these dates will not receive a 2025 contribution receipt

Please note that all requirements must be received in Head Office by the above dates to guarantee settlement for year end.

Have you started talking to your clients about their Registered Retirement Savings Plan (RRSP) contributions yet? Equitable® has a range of RRSP solutions that can help meet their needs, including:- Daily/Guaranteed Interest Account

- Equitable Guaranteed Investment Funds™, available in:

- o Investment Class (75/75)

- o Estate Class (75/100)

- o Protection Class (100/100)

Most clients genuinely want to save for retirement, but intentions alone aren’t enough—they need a plan. As their trusted advisor, you can help them understand why making their RRSP a priority is an important step toward long‑term financial security.

To support those conversations

Most clients genuinely want to save for retirement, but intentions alone aren’t enough—they need a plan. As their trusted advisor, you can help them understand why making their RRSP a priority is an important step toward long‑term financial security.

To support those conversations, we’ve pulled together helpful tools and marketing materials that show how an Equitable RRSP can make a meaningful difference in reaching their retirement goals. Resources include:- Investment calculators

- A retirement savings plan is just a relevant now as it was over 60 years ago

- Borrowing money to save money

From January 1 to March 2, 2026, when clients open or add money to an Equitable TFSA or RRSP, they’ll automatically be entered into Equitable’s Snowball Your Savings contest. Two lucky clients will win — and their advisors get to celebrate too! -

Universal life (UL) enhanced – more options to reach more clients

Great News!

Explore the latest enhancements to Equitable Generations™ UL insurance, offering clients greater flexibility to meet their needs.

What’s new for Equitable Generations UL:

• Level cost of insurance (COI) option.* Available for new sales to offer even more choice for clients. Here is how these rates compare to Equation Generation IV Level COI:

• Non-smoker rates have decreased on average by 4% across all ages and bands (Smoker rates have increased on average by 1%).

• New rate bands. $1M and $5M for Level COI**, making our UL solution more attractive to a wide range of clients. * For Level COI, only Account Value Protector is offered as a death benefit option.

**The rate bands for Level COI are $25,000, $100,000, $250,000, $500,000, $1 million and $5 million. The rate bands for YRT remain $25,000, $50,000, $100,000, $250,000 and $500,000.

These enhancements offer a more competitive solution to grow your UL business. See for yourself – run a quote today!

Equation Generation® IV UL is retired. Equation Generation IV is no longer being offered for new sales effective March 21, 2026.

We now have the essential UL features in one powerful solution, Equitable Generations UL.

Video available French and Chinese.

Please refer to the Transition Rules for all the details on processing your applications.

Visit our splash page for full product details

More reasons to choose Equitable® for your UL business

• Wide range of investment choices through some of Canada’s most prominent fund managers (including sustainable investment options).

• We are the only UL carrier to offer target-date investment options.

• Guaranteed Investment Bonus. An annual rate of 0.75% is added to the policy’s account value starting in year 1.

• No policy administration fees. No Linked Interest Option (LIO) administration fees (except for LIOs that track indices).

• Caring claim support through our KINDTM program.

Need more information? Please contact your Equitable wholesaler.

03/23/26 -

EAMG market commentary

March 11, 2022

Since Russia first invaded the Ukraine, there’s been no shortage of headlines and commentaries trying to make sense of the situation. This is a tragedy that from a humanitarian standpoint that can’t be made sense of and our hearts go out to the people of Ukraine and those impacted. From a market standpoint, the common thinking is that geopolitical risks, aka war, historically haven’t been associated with significant corrections in the market. So far, the market reaction has been consistent with the historical experience, with the S&P 500 down only about 1% since the start of the conflict and the S&P/TSX Composite Index up close to 4%, despite the heightened daily volatility.

Given the obvious challenges of predicting how these types of conflicts play out, we look to financial market indicators to give us a better sense of the potential risks in the market. And in this respect, the most obvious indicator is oil. Since the start of the Russian invasion, oil has rallied roughly 18%, which is even more impressive considering it had already rallied 21% from the start of the year to the beginning of the conflict.

While we don’t know what will happen to energy markets over the coming weeks, we do know that oil shocks can result in higher inflation and sometimes lower growth. Inflation was already rising, although strategists generally viewed this as temporary on the expectation that the covid related supply chain disruptions and reopening pressures were the primary causes that would eventually self-correct. But as the Russian-Ukraine conflict intensifies, consensus views are moving towards inflation becoming more structural in nature. There are growing risks this will change consumer behaviour, causing inflation to be longer lasting than initially expected. Much of this has to do with the fact that as the world’s 3rd largest exporter of oil, Russia has taken a material amount of oil production capacity offline, resulting in significantly higher oil and gas prices. This also explains the significant outperformance of energy equities, and the broader S&P/TSX Composite Index vs US counterparts on a YTD basis.

While there are beneficiaries to higher oil prices, the consumer certainly isn’t one of them given gas prices reflect movements in the oil market. So far in 2022 prices paid at the pump have gone up 30%, one of the fastest paces on record. This, in addition to food price increases, will put strain on the consumer as higher bills divert dollars away from discretionary spending and potentially slow economic growth.

The other factor we’re closely watching is the overall health of the European economy, to which Russia supplies about 40% of Europe’s natural gas, 25% of their oil imports and 45% of their coal imports. While the European Commission has indicated plans to cuts their dependence on Russian energy well before 2030, the short-term impacts will be costly as Europe and other global markets see higher energy prices follow. As well, food prices will likely become an issue for the region given the interruption of supply out of the Black Sea which has driven grain and oilseed prices to levels not seen since 2008. Investors to date have priced in significant risk, evidenced by the performance of the Stoxx 50 which is down 17% YTD, one of the worst performing markets across the global universe.

While commodity prices are just one indicator, we are mindful that they could be telling us inflation may be more persistent than previously expected. From a long-term perspective this hasn’t changed our view of the equity market. As a result of potential near term impacts however, we have reduced our exposure to European markets in favour of the Canadian market and as well we have added inflation and risk hedges with sector allocations to energy, consumer staples and utilities, while still maintaining our overall long-term target levels to equities. There is no direct exposure to Russia in any of the three Equitable Life Active Balanced Portfolios which includes Equitable Life Active Balanced Growth Portfolio Select, Equitable Life Active Balanced Portfolio Select and Equitable Life Active Balanced Income Portfolio Select.

Downloadable CopyAny statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable Life of Canada® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.