Site Search

581 results for enter now access PROBLEMGO.com Buying a guarantee that customs wont open my box Norrkoping

-

The Equitable Gives Back Contest – Start spreading the word!

Equitable Life of Canada is celebrating our 100th Anniversary in 2020, and we’re busy planning a year of events and activities so we can celebrate this significant milestone with our employees, clients, wholesalers and advisors across Canada.

A big part of who we are as a company is our commitment to help strengthen the communities where we operate by supporting a variety of charitable initiatives that help to improve the quality of life for the people living there. We are proud to launch the Equitable Gives Back Contest. Our goal is to give $10,000 to five registered charities operating in Canada.

All it takes to enter is an original essay (not less than 100 words, not more than 500) describing the way in which a charitable organization could use $10,000 to help further their charitable purpose and improve life for Canadians.

Reach out to your clients, tell them about the contest, and encourage them to visit www.equitable100.ca to see if they are eligible! All entries must be submitted by March 31, 2020.

-

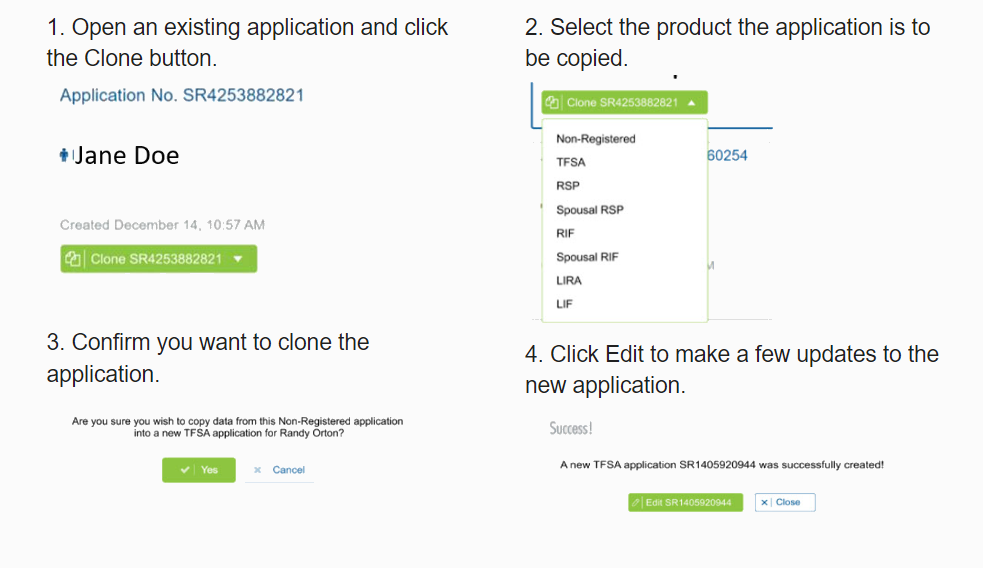

The new segregated fund EZcomplete cloning feature will save time and errors.

The new cloning feature for Savings & Retirement EZcomplete® applications means that advisors don’t need to enter the same client information when completing multiple applications for the same client.

Here's how easy it is to use.

.png "steps-(1).png")

Best of all, you can clone in progress and submitted applications.

This is just some of the information that will be automatically copied:-

Name

-

Date of birth

-

Gender

-

Occupation

-

Address

-

Phone numbers

-

Email address

-

Social Insurance Number

-

All beneficiary information

The new EZcomplete cloning feature will save advisors time and reduce errors..png?width=500&height=92 "sandbox-(3).png")

.png?width=500&height=92 "ezcomplete-(4).png")

.png?width=300&height=82 "sandboxtext-(2).png")

.png?width=300&height=39 "ezcompletetext-(1).png")

If you have any questions, contact your Regional Investment Sales Manager

® denotes a trademark of The Equitable Life Insurance Company of Canada.

Posted April 6, 2023 -

- [pdf] Additional/Updated Client Information

- [pdf] Invest with Equitable

-

Repositioned Wealth Accumulator available

Repositioned Equimax Wealth available now

As we continue to grow to meet the needs of various market segments, our product options for your high net worth (HNW) clients have also been improved. Equimax Wealth Accumulator® has been repositioned to meet the needs of your high net worth clients by providing more deposit room and competitive early cash values.

Equimax Wealth is now repositioned for your high net worth clients

Equimax Wealth Accumulator is now targeted for clients ages 45 to 65 with an insurance need but also looking for tax advantaged growth as an alternative to traditional investments. It allows your clients to achieve both while diversifying their portfolio and saving taxes, particularly for corporations.

Highlights of the repositioned Equimax Wealth Accumulator:

- More deposit room - Allows for significantly more deposit room by reducing the initial death benefit. This means more money can be paid into the policy to promote the tax-advantaged investment growth.

- Higher early cash surrender values - We are more competitive on total cash value in years 1 to 10 in the target market ages of 45-65. The higher extra deposit room and early surrender cash value allows the illustration to show an earlier premium offset, which is key for the HNW market.

- More competitive on life pay - Improvements to life pay more notable than 20 pay. Reduced premiums for most male and female non-smokers in our target market (ages 45-65) as well as 2, 3, and 4 year improvement in illustration of premium offset.

- More competitive at older ages - A shift in the target market means you can support older clients in the HNW market. The Equimax Wealth Accumulator is now more competitive at ages 45-65.

Learn more

For full details on the transition, please see our transition rules.

For more information on this product, please visit the Equimax page on Equinet.

-

Application cloning option now available on EZcomplete

As of September 10th, you will now have the option to clone any Life Insurance and Critical Illness applications that is showing on the EZcomplete dashboard. “Cloning” means the information that has been completed in the existing application is duplicated in a new application.

This feature is meant for situations where multiple applications are being completed and at least one of the parties (the policy owner or insured person) is the same. For example, a single policy owner might own policies on the lives of each of their children. Cloning the application will save re-typing the information about the policy owner into each application.

Please note the following important details regarding cloning:

- Cloning the application will duplicate all information that has been completed in the existing application into the new application.

- In the family situation described above, the information about the policy owner should be completed in the original application. The application should then be cloned before entering any information about the insured person, as there will be a different insured person for the new application.

- Cloning applications can be convenient, but it carries risk. It is imperative that the advisor review every section of the new cloned application to ensure that the information is meant to apply to the new application. If an advisor incorrectly includes information about an individual in the new application, this could give risk to a privacy breach or to liability for the advisor if the questions are answered incorrectly for that individual.

- If the application was submitted and is no longer on the dashboard you will not have the option to clone it.

- You will not be able to change the product type on a cloned application so if you need to select a different product, you will need to start a new application.

- Any documents that were attached to the previous application will not be cloned. The documentation will need to be attached again if required.

- All information from an existing application will be duplicated to the cloned app up to the Signatures step (step 8). Signatures/advisor report will need to be obtained and completed again on the new cloned application.

Resources

Please contact your Regional Sales Manager for more information

-

EXCITING NEWS! Digital Transactions for Universal Life Plans Now Available

We are happy to announce a major update to our digital systems that makes managing Equitable Universal Life (UL) policies easier than ever. Starting now, you can use digital transactions to submit your clients’ instructions to change their UL deposit allocations and transfer funds between accounts.

This update builds on the recent launch of our digital policy loan request on EquiNet® and is another step towards making your Equitable® experience easier and more convenient.

What's New?

In the past, you had to submit written requests for UL deposit allocation changes and account value transfers using the Universal Life Form 693UL (you can still use this method if you prefer).

Now, you can manage these transactions directly through the secure EquiNet advisor portal. This new process also allows clients to securely approve their requested changes by email.

To get started, simply log into your account on EquiNet and go to the Policy Inquiry tab.

We have provided a brief user guide to help you through the steps.

We trust that this digital upgrade will enhance the way you work with Equitable. Stay tuned for more digital enhancements in the near future!

Thank you for your continued support and partnership.

Questions? For more information, please reach out to your wholesaler or our customer service team.

® or TM denotes a trademark of The Equitable Life Insurance Company of Canada.

-

A bright start to July: our Dividend Scale is now active!

Effective July 1st - just in time for summer conversations!

Good news! The Equitable® Board of Directors has approved continuing our current dividend scale for the period of July 1, 2025, to June 30, 2026.

• The interest rate* we use to decide the dividend scale will stay at 6.40%.

• Other factors used to decide the dividend scale will stay the same.

• The interest rate for policies with dividends on deposit will stay at 3.50%.

• The interest rate for most policy loans will stay at 6.50%. This applies to both new and existing policy loans, and automatic premium loans. It specifically applies to Equimax® policies with a 9-digit policy number that starts with either "3" or "8". Older policies may have different loan rates as they are based on the prime interest rate.

*The dividend scale interest rate (DSIR) is different from the participating account (PAR) rate of return. The DSIR smooths out the ups and downs of the participating account experience. The PAR rate of return is the return on the investments in the participating account over the calendar year.

Need more information?

Did you miss our Spring Update & 2025 Dividend Scale Announcement?

Watch it now:

- [pdf] Introducing Equitable

-

EAMG Market Commentary July 2023

Posted July 27, 2023

July 17, 2023

Rates & Credit - The rates market was volatile in Q2 as investors focused on inflation, central bank interest rate decisions, and recession probabilities. Persistent strength in U.S. consumer spending and labour markets have surprised investors and prompted further interest rate tightening from central banks. In Canada, corporate bonds outperformed government bonds and the broader FTSE Canada Universe Index during the quarter, with a total return of 0.2%, versus a loss of 1.0% for government bonds and 0.7% for the overall Index. The corporate bond outperformance was driven by a broad risk-on tone to the market, most notably in April as the market recovered from the banking sector liquidity crisis that developed during March. That said, the market tone remained cautious, with the improved risk premium on corporate bonds tempered by lingering concerns around sticky inflation, high interest rates, and the potential for slower economic growth into the latter half of the year.

Dominance of U.S. Equities – U.S. equity markets posted another strong quarter with the S&P 500 returning 8.7%, outperforming Canada and other major international equity markets. The S&P/TSX Composite, returned 1.2% in CAD. Major developed economies from Europe, Australasia, and Far East (EAFE) returned 3.2% in local currency terms. The highly anticipated re-opening of the Chinese economy has failed to materialize with economic data indicating less strength than previously forecasted. Amid sluggish Chinese growth, closely interconnected economic partners such as the European Union, as well as commodity-driven markets like Canada, have all underperformed the U.S. on a relative basis.

U.S. Fundamentals – Earnings continued to contract versus prior year, albeit at a slower pace than forecasted. Forward earnings guidance improved quarter-over-quarter with corporate sentiment returning to neutral levels. Based on our analysis, we observed that 31% of major companies expect deteriorating financial performance, while 33% expect improved performance, with the remaining expecting no material change. Overall, major U.S. companies remain well capitalized with strong operating margins. However, company guidance indicates a prioritization of cost controls amid increased consumer indebtedness and concerns about the health of the consumer.

Artificial Intelligence (AI) Mania – Despite concerns that the U.S. economy is at a late stage in its economic cycle, that monetary tightening by central banks could go too far, and the fact that earnings contracted on a year-over-year basis, equity markets became more expensive during the quarter with price-to-earnings multiples expanding. This expansion was driven by investors crowding into AI focused technology companies, with the seven largest AI/technology themed companies averaging a 26% return while the other 493 members gained only 3%. Investors rewarded businesses with contributions to AI development (hardware and software components), as well as those with the ability to implement synergies from leveraging the technology. A crowded market surge is not uncommon at this point in the economic cycle, where positive economic surprises, in this instance, strong employment and consumer spending can lead to an upswelling in investor confidence.

U.S. Quant Factors – Using our investment framework, we currently favour exposures to large cash-rich companies with innovative product offerings, which we believe offer the strongest risk-adjusted returns in the current market environment. While the valuation of AI companies seems to defy traditional rationales, the momentum has continued to push the group higher. Consequently, the Quality factor (companies with higher return-on-equity, strong operating performance, and healthy leverage levels) participated in the AI trend and consistently outperformed throughout the quarter. The Low Volatility factor (stocks with lower sensitivity to broad market movement, and lower price volatility) underperformed through the quarter. While the Low Volatility factor typically performs well at this stage of the economic cycle, the fact that a small number of stocks were responsible for much of the market’s return hurt this factor. Lastly, the Momentum factor (stocks with a recent history of price appreciation) initially underperformed during the quarter before rebounding in June. This factor’s recent outperformance suggests that the market is becoming complacent and possibly signals that rotations within the market are slowing as current trends remain in favour.

Canadian Fundamentals – Top line revenue missed forecasts while bottom line earnings were consistent with expectations. Softer-than-expected results out of Canadian financials, as well as underwhelming results from the materials sector, dragged on the aggregate index performance. Earnings forecasts for the rest of the year have been revised downward with analyst expecting index aggregate earnings to detract 2% to 3%. Meanwhile, the Bank of Canada raised its overnight interest rate by 25 basis points, bringing it to 4.75% on the backdrop of robust economic data releases including Q1 GDP and April CPI.

Canadian Quant Factors – The most notable dislocation in Canada was the convergence of the dividend yield of High-Dividend ETFs and Equal-Weight Bank ETFs. We believe that the drag from Canadian banks following the U.S. regional banking concerns in March resulted in a discount of the Quality factor as the performance of the group is sensitive to the movements of banks. While banks did recover around 35% of their SVB-induced underperformance, the nature of banking has attracted investor scrutiny given the view that we are in the late-stage of the economic cycle. That said, this environment is an attractive environment to add variants of the Quality factor, which would gain exposure to a rebounding industry that offers a similar dividend yield to the high dividend stocks.

Views From the Frontline

Rates – On an outright basis, bond yields across the curve continue to look attractive. Economic data remains strong however we are beginning to see the first signs of weakness in spending, jobs and inflation. Slower growth, a more balanced labour market, declining inflation, and tighter credit conditions will likely drive interest rates lower throughout 2023. Market participants remain focused on the extent of interest rate hikes and the duration of a pause required to bring inflation back to the 2% target. With inflation remaining more persistent than previously expected forecasts around the timing, pace and extent of the removal of monetary policy have been pushed into 2024.

Credit – The uncertain economic outlook and risks around slower economic growth later this year merit caution about corporate bonds and a bias towards higher-quality, shorter-dated credit where we think the risk / reward dynamic are more favourable. That said, the “soft-landing” narrative, now more pervasive in the market, could continue to provide support to risk assets, which we view as an opportunity to further pare down higher beta exposure.

Equities – Given the direction of the current economic and company fundamental data, we continue to favour high quality growth segments of the market with strong operating margins. As such, the late cycle conditions in the market reinforce our preference for large cap stocks over smaller, more U.S. domestically focused businesses. The U.S. Low Volatility factor’s underperformance is unlikely to reverse in the short term given the resilience of the U.S. economy. Furthermore, after a steep decline last quarter, we expect that cyclical value will find support in the near term, echoing the increased chance of slowing inflation without stalling economic growth. In Canada, equities are typically more cyclical in nature, which coupled with the potential for an earnings contraction, makes us view the Low Volatility factor as more likely to outperform. Like the U.S., we prefer Canadian high-quality companies to navigate through the late cycle environment. On the heels of poor Chinese economic data and underwhelming stimulus, we are maintaining our overweight to the U.S. relative to Canada and EAFE.

Downloadable Copy

ADVISOR USE ONLY

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable Life of Canada® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.