Site Search

796 results for check site now MAKEMUR.COM Buying early release from jail with payment plans

- [pdf] Dollar Cost Averaging

-

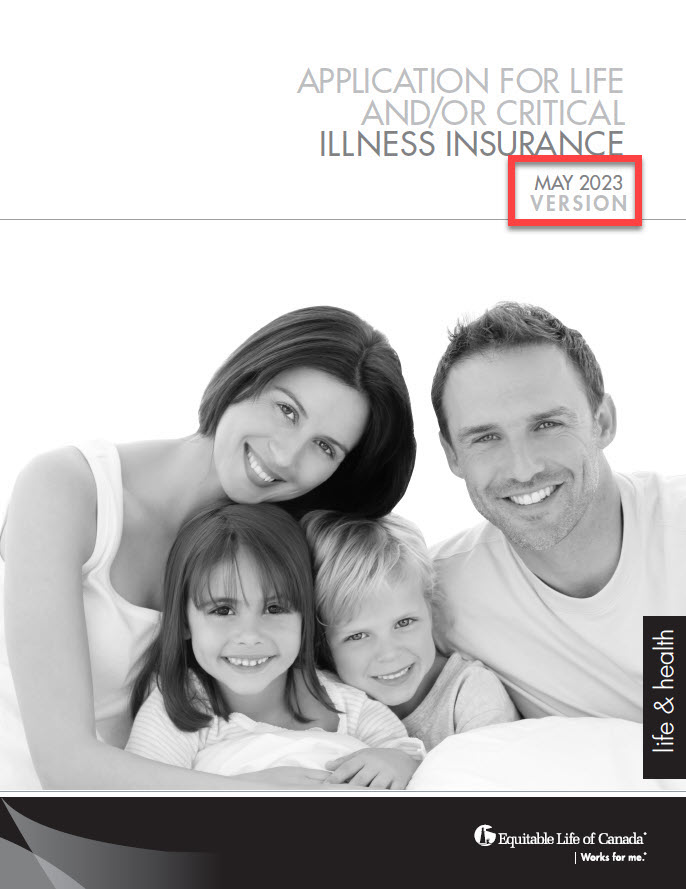

New 350 Life and CI Applications

On August 2nd, 2023, Equitable Life® will be updating the privacy and legal sections on some forms. This includes the form 350 Paper Application for Life and/or Critical Illness Insurance. This change will also be applied on our websites and our online application EZComplete®. These changes are part of Bill 64. The Bill is about the protection of personal and private information in Quebec. This will take effect on September 1st, 2023.

Due to this change, we ask all advisors to use the latest version dated May 2023 of the paper application after August 2nd. Applications in Quebec must use the lastest version from September 1, 2023 onwards.

For all regions outside Quebec, we will support a transition period from ‘old’ to ‘new’ applications until December 31st, 2023. After this date, we will no longer accept older versions of our Life and Critical Illness application.

To make sure you are using the latest version of the application, check the date on the title page. It should say May 2023. See the image below:

.jpg?width=200&height=259 "Form-350-Image-EN-(1).jpg")

To order paper copies, click here.

Email completed applications to supply@equitable.ca.

To learn more about Bill 64, please visit Assemblee nationale du Quebec - Bill 64. You may also contact your wholesaler.

® denote a registered trademark of The Equitable Life Insurance Company of Canada. - [pdf] EquiLiving 10 Year Renewable to Age 75 (For Children's Plans)

-

Responding to Alberta's Biosimilar Initiative

Beginning March 15, 2021, we are changing coverage for some biologic drugs in Alberta in response to the province’s Biosimilar Initiative. These changes will help protect your clients from additional drug costs that may result from this new government policy while still providing access to equally safe and effective biosimilars.

What is Alberta’s Biosimilar Initiative?

Alberta’s Biosimilar Initiative will end provincial coverage of several originator biologic drugs for some or all conditions beginning on Jan. 15, 2021. Patients 18 and over who are using these drugs for the affected conditions will be required to switch to biosimilar versions of the drugs to maintain coverage under the province’s government drug plan.

What is the impact on private drug plans?

Industry response to Alberta’s Biosimilar Initiative has the potential to significantly impact your clients’ drug plan costs. If other insurance carriers follow suit with the province and delist the originator biologics, it could expose a plan that doesn’t delist them to significant coordination of benefits risk. (See Case Study below.)

How is Equitable Life responding?

To protect your clients’ plans from paying additional and avoidable drug costs, we are changing coverage in Alberta for most biologic drugs included in the provincial initiative.

As of March 15, 2021, several originator biologic drugs will no longer be covered for plan members of all ages in Alberta. Plan members taking these biologics will be required to switch to the biosimilar versions of these drugs to maintain eligibility under their Equitable Life plan.

What drugs and conditions are affected?

The following table outlines the drugs and conditions that will be affected by this change. The list of affected drugs or conditions is dynamic and will change as Alberta includes more biologic drugs in its Biosimilar Initiative, as new biosimilars come onto the market, and as we make changes in drug eligibility.

Drug name Originator biologic

These drugs will no longer be covered in Alberta for the conditions listed in this table.Biosimilar

Plan members will need to switch to these medications to maintain coverage under their Equitable Life plan.

Affected health conditions

The changes in coverage apply to these conditions.Etanercept Enbrel Brenzys

ErelziAnkylosing Spondylitis

Rheumatoid Arthritis

Polyarticular juvenile idiopathic arthritis (JIA)

Psoriatic Arthritis

Plaque Psoriasis (adults and children)Infliximab Remicade Inflectra

Renflexis

AvsolaAnkylosing Spondylitis

Plaque Psoriasis

Psoriatic Arthritis

Rheumatoid Arthritis

Crohn's Disease (adults and children)

Ulcerative Colitis (adults and children)Insulin glargine Lantus Basaglar Diabetes (Type 1 and 2) Filgrastim Neupogen Grastofil

NivestymNeutropenia Pegfilgrastim Neulasta Lapelga

Fulphila

ZiextenzoNeutropenia Glatiramer* Copaxone Glatect

TEVA-Glatiramer AcetateMultiple Sclerosis *Glatiramer is a non-biologic complex drug.

How will Equitable Life communicate this change to plan members?

We will be communicating with affected claimants in January 2021 to allow them ample time to change their prescriptions and avoid any interruptions in their treatment or their coverage.

Can my client maintain coverage of these biologic drugs?

Traditional groups who wish to opt out of this change and maintain coverage of these originator biologics for Alberta plan members can submit a policy amendment. Amendments must be submitted no later than January 15, 2021. Advisors with myFlex Benefits clients who wish to maintain coverage of these originator biologics for Alberta plan members should speak to their myFlex Sales Manager to confirm their eligibility to opt out of this change.

Will this change impact my clients’ rates?

The rate impact of this change in coverage will be relatively insignificant. Any cost savings associated with the change will be factored in at renewal.

If plan sponsors opt out of these changes and maintain coverage for the originator biologics, it may result in a rate increase. Any rate adjustment will be applied at renewal.

What is the difference between biologics and biosimilars?

Biologics are drugs that are engineered using living organisms like yeast and bacteria. The first version of a biologic developed is also known as the “originator” biologic. Biosimilars are also biologics. They are highly similar to the originator drug they are based on and have been shown to have no clinically meaningful differences in safety or efficacy.

Questions?

If you have any questions about this change, please contact your Group Account Executive or myFlex Sales Manager.

CASE STUDY: The Alberta Biosimilar Initiative and Coordination of Benefits (CoB) risk

CoB risk is real and can be significant, even if a pharmaceutical savings program exists.

The industry response to Alberta’s Biosimilar Initiative has the potential to significantly impact your clients’ drug plan costs. Some insurers may follow the province’s lead and delist these originator biologics. Others may cut back coverage to the cost of the biosimilars or maintain coverage of the originators. These differences could expose a plan that doesn’t delist the originator biologics to significant coordination of benefits risk. Here’s how:

Let’s assume there are two private drug plans – Plan A and Plan B. Both plans are open plans with no deductible. Plan A has 80% co-insurance and Plan B has 100% co-insurance.

BEFORE Alberta’s Biosimilar Initiative

Before Alberta’s Biosimilar Initiative, both plans cover the originator biologics listed above.

Plan A is the first private payer for an Alberta plan member taking an originator biologic drug for Rheumatoid Arthritis. Plan B is the second private payer. The cost of the originator biologic for the plan member is $30,000 annually. Here’s how the coordination of benefits would look before Alberta’s Biosimilar Initiative.

AFTER Alberta’s Biosimilar InitiativeIn response to Alberta’s Biosimilar Initiative, the insurer for Plan A delists the originator biologic and requires plan members to switch to the biosimilar. The insurer for Plan B maintains coverage of the originator biologic. Under this scenario, if the plan member doesn’t switch, Plan B essentially becomes the first payer and sees their annual cost increase by 400% (from $6,000 to $30,000).

Even if the insurer for Plan B cuts back coverage to the cost of the biosimilar or adjusts the paid amount because they have a savings program in place with the drug manufacturer, the impact could be significant. For example, if the insurer cuts back coverage to 50% (or $15,000 annually), Plan B would see a 150% annual cost increase (from $6,000 to $15,000):

- [pdf] G3NU-Application for Non-Underwriting Change

- [pdf] G2 - Application for Non-Underwriting change

-

THREE new ways to help make your Savings & Retirement business run smoother

As of August 20, 2022, EZcomplete® will include several new features that allow applications to be completed faster and easier:

1. Prefilled Fund Transfer Form

The transfer form will be generated with the information from EZcomplete and included in the EZcomplete signing package, saving you time.

2. Client eSignature Audit History and Document Download

If you choose the e-signature option for the client, you’ll be able to download a copy of the e-signed transfer forms and the signature audit history.

3. Email the Client Contract Info and Fund Facts Before Signing

You'll now be able to email Point of Sale materials (Contract & Info Folder and Fund Facts) to clients before they provide their e-signature.

Log in to EZcomplete today!

Speak to your Regional Investment Sales Manager to learn more!

-

And the Equitable FHSA Contests winners are...

Equitable® is proud to be the first insurance company to offer a First Home Savings Account (FHSA) to Canadians.

Since launch in September 2023, we have received an incredible response to Equitable’s FHSA, available on Pivotal Select™ Investment Class (75/75) and Pivotal Select Estate Class (75/100).

As part of this historic launch, we offered contests for clients to win $8,000 towards their 2024 FHSA contribution, with their advisor winning $2,000. We’ve now completed the draws and are thrilled to announce the following winners:

January 16, 2024, draw:

Client: Jagan A., ON

Advisor: Krupa P., ON

February 13, 2024, draw:

Client: Pawandeep K., ON

Advisor: Jaskaranjit S., ON

Congratulations to our winners! It warms our hearts to know we are helping Canadians save for their first home.

From all of us at Equitable, thank you for your trust and partnership.

® or ™ denotes a trademark of The Equitable Life Insurance Company of Canada.

Date Posted: March 13, 2024 -

And the winners of Equitable’s New Year’s Resolution, New Year’s Contribution Contest are…

A big thank you for making Equitable’s New Year’s Resolution, New Year’s Contribution contest a huge success.

Clients who made a contribution between January 1 and February 29, 2024, to their Registered Retirement Savings Plan (RRSP), Tax-Free Savings Account (TFSA) or First Home Savings Account (FHSA) could win $5,000 and the advisor could win $1,000.

As a special thank you to our clients and wonderful advisor partners we’ve tripled the fun and appreciation to three prizes.

We’ve now completed the draws and are thrilled to announce the following winners:-

Client: Winnie C., Ontario

Advisor: Rebecca M., Ontario -

Client: Eunice D., Alberta

Advisor: Diamond O., Alberta -

Client: Loyda A., Alberta

Advisor: Michael V., Alberta

Congratulations to our winners!

From all of us at Equitable, thank you for your trust and partnership.

Date posted: April 24, 2024

® or ™ denotes a trademark of The Equitable Life Insurance Company of Canada. -

-

Spring update and dividend scale for 2025/2026

Good news! The Equitable® Board of Directors has approved continuing our current dividend scale for the period of July 1, 2025, to June 30, 2026.

• The interest rate* we use to decide the dividend scale will stay at 6.40%.

• Other factors used to decide the dividend scale will stay the same.

• The interest rate for policies with dividends on deposit will stay at 3.50%.

• The interest rate for most policy loans will stay at 6.50%. This applies to both new and existing policy loans, and automatic premium loans. It specifically applies to Equimax® policies with a 9-digit policy number that starts with either "3" or "8". Older policies may have different loan rates as they are based on the prime interest rate.

*The dividend scale interest rate (DSIR) is different from the participating account (PAR) rate of return. The DSIR smooths out the ups and downs of the participating account experience. The PAR rate of return is the return on the investments in the participating account over the calendar year.

Need more information?

Did you miss our Spring Update & 2025 Dividend Scale Announcement?

Watch it now: