Site Search

570 results for enter portal MAKEMUR.COM contact judge to dismiss case for money Missouri

-

Group Benefits - Premium relief for Dental and Extended Health Care benefits

We know this is a difficult time for Canadian employers and that many of your clients are facing financial hardship as a result of the COVID-19 pandemic. We continue to look for ways to help employers manage while still supporting their employees.

With many health practitioners closing their offices due to the pandemic restrictions, plan member use of dental benefits and some health benefits has declined.

So, we are pleased to announce that we are offering premium relief for all Traditional and myFlex insured non-refund customers for Health and Dental benefits, as follows:

- A 50% reduction on Dental premiums; and

- A 20% reduction on vision and extended healthcare rates (excluding prescription drugs), which equates to an 8% reduction on Health premiums.

These reductions are retroactive to April 1, 2020 and will appear as a credit against the next available billing. We will assess the situation monthly and expect to continue with monthly refunds for as long as the current crisis period continues.

We expect that claims experience and premiums will return to normal once the current pandemic restrictions are lifted.

In the meantime, plan members will continue to have full access to their benefits coverage throughout the pandemic. In many cases, dental offices remain open for emergency services, and a variety of healthcare providers are available virtually.

Commissions

We know the pandemic has put financial strain on your business as well, so we will continue to pay full compensation. Although your overall commission will be unaffected by these premium reduction adjustments, you may see a temporary reduction in your commission payments if you are on a pay-as-earned basis while we put through mass changes. If so, we will then make an additional top-up payment to cover that shortfall as soon as we are able.

Communication

We will be communicating this premium relief program to your clients April 21st at 8:00am EST.

A PDF of the communication is also available here.Questions?

If you have any questions, please contact your Group Account Executive or myFlex Sales Manager. In the meantime, we have provided some Questions and Answers below.

Will the premium reduction on Health and Dental benefits have an impact on the renewals that were deferred?

No. Renewals will proceed as normal, with rate adjustments based only on months where full premium was paid. For most clients, we anticipate “normal” rate adjustments at renewal compared to rates paid prior to refunds taking effect.

Does this adjustment apply equally to clients who have had their renewal deferred?

Yes, these adjustments apply to all Traditional and myFlex insured, non-refund customers for Health and Dental benefits.

How does this affect clients who have terminated or amended a plan?

If a benefit is in-force during the month of April, the adjustment will be credited to the next available billing. For clients who have temporarily terminated all benefits, this will be applied against the first bill once benefits have been reinstated. No cash refunds will be paid.

Will you recover any of the adjustment at a future point in time?

No, we will not recover this adjustment.

Instead of this premium reduction adjustment, can a client cancel or adjust some of the benefits on their plan?

Yes, you and your clients always have the option of changing the coverage on a plan, such as reducing or removing a benefit to help control costs. Please speak to your Group Account Executive or myFlex Sales Manager about the options available.

Are TPAs and self-administered groups eligible for the premium reduction?

Yes. TPAs and self-administered groups are eligible for the premium reduction. However, timing for the credit will be dependent on the billing practices of the TPA or self-administered group. We will apply these credits as soon as we are able. -

January 2023 eNews

Responding to Saskatchewan’s biosimilar switch initiative*

We are changing coverage for some biologic drugs in Saskatchewan in response to the province’s biosimilar initiative. These changes will help protect your clients’ plans from additional drug costs that may result from this new government policy while providing access to equally safe and effective lower-cost biosimilars.

Saskatchewan’s provincial biosimilar initiative

Announced in October 2022, the Saskatchewan Biosimilars Initiative ends coverage of ten biologic drugs beginning on April 30, 2023.

Patients in the province who are using these drugs will be required to switch to biosimilar versions of these drugs by April 30, 2023, in order to maintain their Saskatchewan Drug Plan coverage.

Equitable Life’s response

To ensure this provincial change doesn’t result in your clients’ plans paying additional and avoidable drug costs, we are changing coverage in Saskatchewan for most biologic drugs included in the provincial initiative.

Beginning April 30, 2023, plan members in the province will no longer be eligible for most originator biologic drugs if they have a condition for which Health Canada has approved a lower cost biosimilar version of the drug.** These plan members will be required to switch to a biosimilar version of the drug to maintain coverage under their Equitable Life plan.

Communicating this change to plan members

We will inform any affected plan members in early February of the need to switch their medications so that they have ample time to change their prescriptions and avoid any interruptions in treatment or coverage.

What is the difference between biologics and biosimilars?

Biologics are drugs that are engineered using living organisms like yeast and bacteria. The first version of a biologic developed is known as the “originator” biologic. Biosimilars are highly similar to the drugs they are based on and Health Canada considers them to be equally safe and effective for approved conditions.

Questions?

If you have any questions about this change, please contact your Group Account Executive or myFlex Sales Manager.

**The list of affected drugs is dynamic and will change as Saskatchewan includes more biologic drugs in its biosimilar initiative, as new biosimilars come onto the market, and as we make changes in drug eligibility.

Ontario announces 2023 biosimilar switch program*

The government of Ontario recently announced the launch of a biosimilar initiative to switch patients from eight originator biologic drugs to biosimilar versions of the drugs.

Patients in Ontario using affected originator biologic drugs will have until December 29, 2023 to switch to a biosimilar version of their medications in order to maintain coverage under the province’s public drug plans.

We are actively monitoring and investigating the impact of this new policy on private drug plans in Ontario. We plan to implement changes to coverage of biologic drugs in the province in 2023 to help prevent this change from resulting in additional costs for our clients’ drug plans. We will provide more details in the coming months.

If you have any questions, please contact your Group Account Executive or myFlex Sales Manager.

Dental fee guide updates*

Each year, Provincial and Territorial Dental Associations publish fee guides. Equitable Life® uses these guides to help determine the reimbursement limits for dental procedures. For your reference, below is the list of the average dental fee increases for general practitioners that will be used by Equitable Life for 2023.***Dental fee guide increases over 2022***

***Data for all provinces and territories was not available at the time of publication. This chart will be updated on EquitableHealth.ca as more information becomes available.

Equitable Life ranks high with Canadian group advisors*

Equitable Life ranked second nationally and first in Ontario among major insurers in a recent survey of Canadian group benefits advisors.

NMG Consulting, a leading global consulting firm, conducted in-depth interviews with 130 leading group consultants, brokers and third-party administrators across the country between May and August 2022 for its annual Canadian Group Benefits Study. Based on these interviews, NMG ranked group insurers in six categories, ranging from operational management to technology.

Nationally, Equitable Life ranked either first or second in four of the six main categories:

Advisors in Ontario, in particular, scored Equitable Life very favourably. We ranked #1 overall in the province, finishing first in four of the six overall categories, including: Relationship Management, Operational Management, Underwriting and Claims Management and Technology.

“The fact that advisors regard us so highly in so many categories is a testament to our mutual status and our ability to focus exclusively on our clients and advisors,” said Marc Avaria, Senior Vice President of Group. “We are truly working together to build strong, enduring and aligned partnerships.”

“While we are happy with these results, we won’t rest on our laurels,” added Avaria. “We will continue to dedicate ourselves to providing our clients and advisors with a better benefits experience.”

Here are more of the highlights from this year’s results:

Nationally, we ranked first in all 10 subcategories in Operational Management, including:- Overall service to intermediaries,

- Overall service to plan sponsors,

- New quote process,

- Plan implementation,

- Renewal process,

- Information shared at renewal,

- Accuracy and timeliness of reporting and billing,

- Administration quality and responsiveness,

- Taking ownership and

- Management information quality and availability.

- Company relationship management,

- Ease of doing business,

- Account executive capability,

- Market knowledge,

- Visit/call quality,

- Effective coordination and

- Advice.

- Fairness and timeliness of disability claims (1st)

- Fairness and timeliness of health claims (2nd)

- Fraud management (2nd)

- Competitiveness of pooling charges (2nd)

- Group underwriting flexibility (3rd)

- Health and dental TLR competitiveness (3rd)

- Overall technology – Intermediary (2nd)

- Member experience (2nd)

- [pdf] Alternative Identification Requirements

-

Market Commentary January 2025

Key Takeaways

Full year 2024:

-

Despite reductions of policy-setting interest rates by central banks, yields on longer-term bonds finished the year higher than they started the year.

-

Positive risk appetite helped corporate bonds perform well, led by lower-quality issuers.

-

Global equity markets posted robust returns, with U.S. equities outperforming other developed markets, driven by heavy concentration into the ‘Magnificent 7’ stocks.

Fourth Quarter:

-

Central banks continued to ease monetary policy in Q4, with the Bank of Canada cutting its policy interest rate more aggressively than did the U.S. Federal Reserve.

-

The Republican victory across both the executive and legislative branches in the U.S. ignited expectations of economic growth, pushing bond yields and stock prices higher.

-

Risk sentiment helped corporate bonds continue to outperform government bonds.

-

Markets remained volatile: while North American stock markets continued to outperform most international indices, Canadian stocks managed to outperform U.S. stocks in Q4, as sources of returns in the U.S. narrowed into year-end.

Economic and Market Update

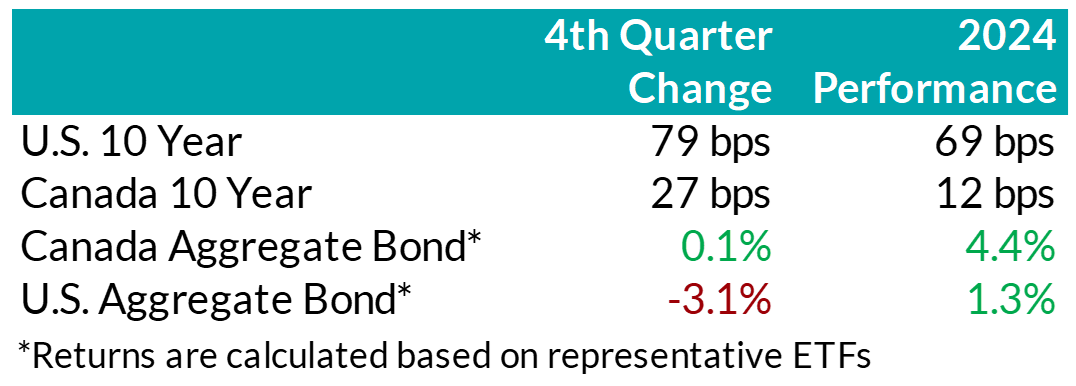

Economic Summary: In the U.S., economic activity continued to expand at a solid pace in Q4. The rate of inflation continued to slow but remained above the central bank’s 2% objective. The labour market in the U.S. remained resilient, as the unemployment rate has remained low compared to historical norms. A decisive victory for Donald Trump and the Republican Party further boosted expectations for continued growth. The return of the President-elect’s old tactics of threatening tariffs to influence trade, security, and drug control re-introduced some economic uncertainty, particularly regarding the potential return of inflationary pressures. Those concerns prompted the Federal Reserve to slow the pace of its policy easing, as it lowered rates by just 0.25% at each of its two meetings in Q4, following the 0.50% cut in September. Throughout 2024, the Fed reduced rates by a total of 100 basis points, from 5.50% to 4.50%. Nonetheless, bond yields were significantly higher for most maturity terms during the fourth quarter as the market priced in not just a stronger economy than had been the expectation during Q3, implying less interest rate cuts by the Fed, but also growing concerns about the government deficit.

In Canada, growth remained positive during 2024 and improved a bit to close the year, but continued to fall short of the Bank of Canada’s expectations. Similarly, inflation came in lower than expected and below the Bank’s 2% target. The labour market continued to soften for much of the year, with employment growth falling short of labour force growth. The weakness in the labour market and economy, along with tamed inflation, prompted the Central Bank to cut rates at the pace of 50 basis points at each of its two meetings in Q4. For the full year, the Bank of Canada ended up lowering its policy rate by a total of 175 basis points, from 5% to 3.25%. The market has been expecting the Bank of Canada to need to continue cutting rates due to slower economic growth in Canada, but the fear of a possible trade war with the U.S. has made the economic outlook somewhat murkier.

.png "Chart1-(1).png")

Bond Markets: During the quarter, yields on mid- to long-term bonds in Canada rose in sympathy with rising bond yields in the U.S. However, bond yields in Canada rose to a lesser extent, and yields on shorter-term bonds were actually little changed over the quarter. The FTSE Canada Universe Bond Index was basically flat during Q4 and posted a return of 4.2% for the full year. Although interest rates rose, credit spreads (i.e. the extra yield on corporate bonds versus government bonds to compensate for their extra risk) continued to grind lower, helping corporate bonds post positive overall returns in the quarter. Tightening credit spreads reflected the generally positive risk-on tone to the market, despite some volatility. Lower-rated BBB bonds generally performed better than higher-quality A-rated bonds. Credit spreads have now generally fallen back to levels similar to those experienced in 2021, when markets did quite well after the pandemic. The on-going appetite of investors for the extra yield offered by corporate bonds over government bonds is indicated not just by falling credit spreads, but also by investors’ enthusiasm to support the primary issuance market. Corporate bond supply continued to be very robust in the quarter, with $30 billion in new issuance, resulting in a record-breaking year with $141 billion of new issuance in 2024. Nonetheless, on balance, we do not think the current risk premium adequately compensates for downside risk, particularly in longer-dated corporate bonds, and have a bias towards shorter-dated credit where we view the risk / reward trade-off as being more favourable.

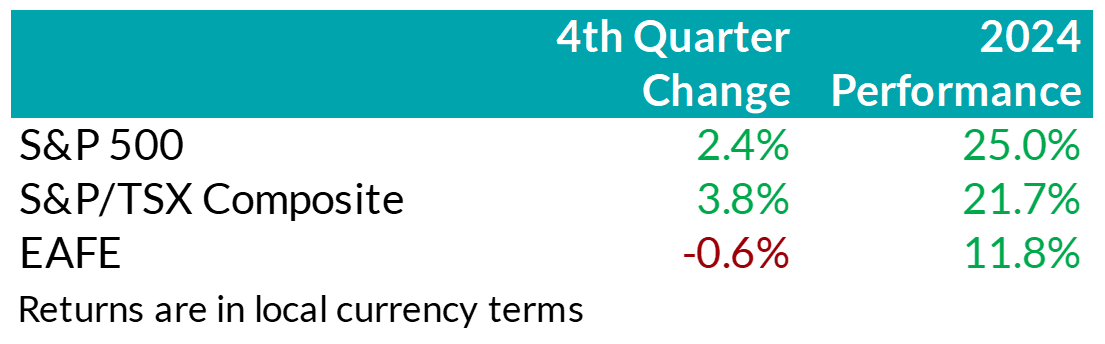

.png "Chart2-(1).png") Stock Markets – Overview: Trump’s presidential victory and the Republican party’s ‘red sweep’ in the Senate and House of Representatives sparked optimism surrounding economic growth and a new era of U.S. exceptionalism. As a result, North American equity markets extended their rally in Q4, capping off a year of robust returns. The S&P 500 returned 2.4%, bringing its year-to-date return to 25%. Within the U.S., the broadening of returns paused during the quarter as the chase for growth intensified, with mega-cap growth names like Tesla driving performance. Canadian equities surprisingly outperformed the U.S. market over the quarter, returning 3.8% in Q4, despite threats of widespread tariff negotiations looming on the horizon that could negatively impact Canadian corporate fundamentals. At a sector level, strength in the technology, financials, and energy sectors more than offset weakness in telecommunication companies as well as in the materials sector. Elsewhere, major developed markets from Europe and Asia (EAFE) underperformed last quarter as deteriorating Chinese growth prospects and weak economic growth in the Eurozone weighed on equities. Notably, foreign investors of U.S. denominated securities benefitted from a rebounding U.S. dollar with the dollar index adding over 7.6% in Q4.

Stock Markets – Overview: Trump’s presidential victory and the Republican party’s ‘red sweep’ in the Senate and House of Representatives sparked optimism surrounding economic growth and a new era of U.S. exceptionalism. As a result, North American equity markets extended their rally in Q4, capping off a year of robust returns. The S&P 500 returned 2.4%, bringing its year-to-date return to 25%. Within the U.S., the broadening of returns paused during the quarter as the chase for growth intensified, with mega-cap growth names like Tesla driving performance. Canadian equities surprisingly outperformed the U.S. market over the quarter, returning 3.8% in Q4, despite threats of widespread tariff negotiations looming on the horizon that could negatively impact Canadian corporate fundamentals. At a sector level, strength in the technology, financials, and energy sectors more than offset weakness in telecommunication companies as well as in the materials sector. Elsewhere, major developed markets from Europe and Asia (EAFE) underperformed last quarter as deteriorating Chinese growth prospects and weak economic growth in the Eurozone weighed on equities. Notably, foreign investors of U.S. denominated securities benefitted from a rebounding U.S. dollar with the dollar index adding over 7.6% in Q4.

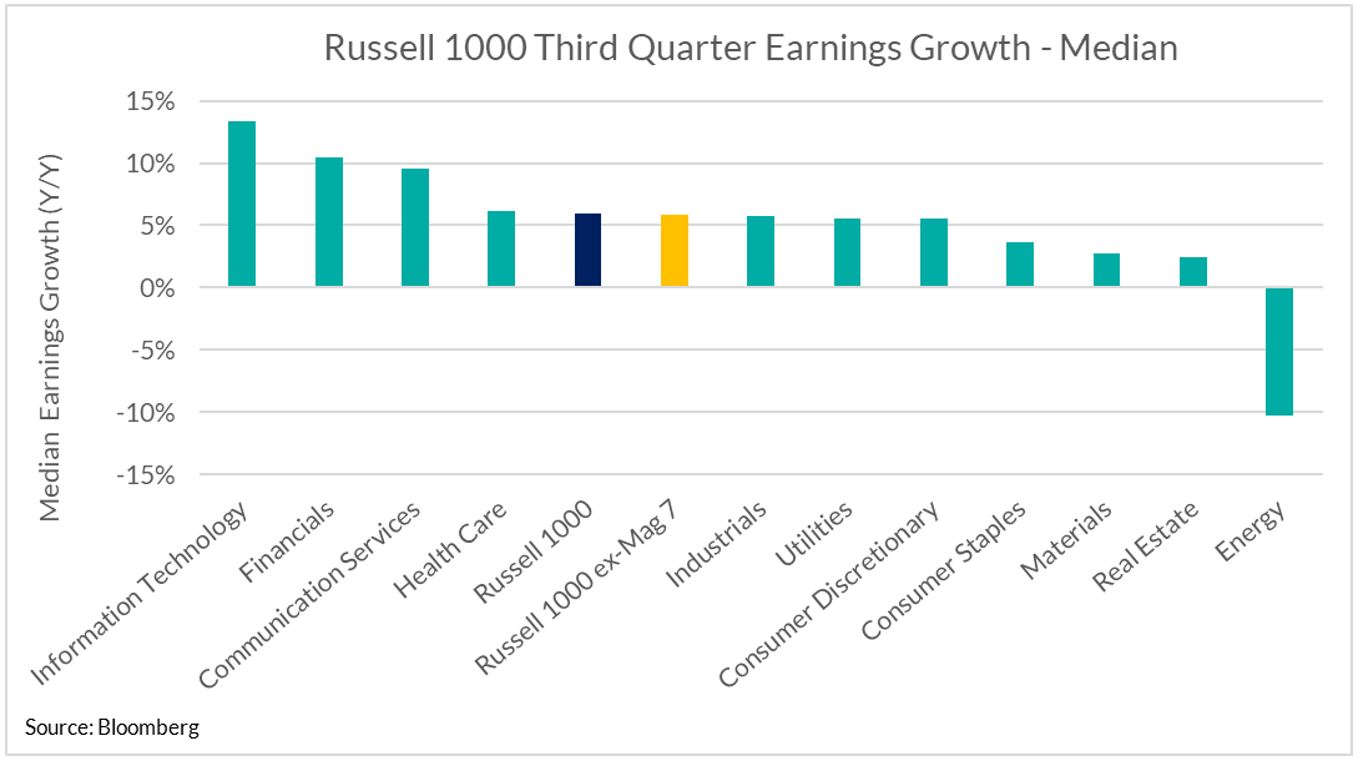

.png "Chart3-(1).png") U.S. Equities: U.S. equities remain supported by resilient margins and strong corporate earnings growth with over 70% of businesses surpassing bottom-line expectations last quarter. We remain attentive to the broadening of earnings performance and note that this trend has continued, albeit at a normalized pace versus prior quarters. More specifically, our work shows that members of the Russell 1000, excluding the Magnificent 7, posted median earnings growth of 6% last quarter, down from nearly 9% in Q3 but comparable to Q2 (6%). Looking forward to 2025, analysts continue to forecast U.S. exceptionalism, with forecasts of ~12% earnings growth.

U.S. Equities: U.S. equities remain supported by resilient margins and strong corporate earnings growth with over 70% of businesses surpassing bottom-line expectations last quarter. We remain attentive to the broadening of earnings performance and note that this trend has continued, albeit at a normalized pace versus prior quarters. More specifically, our work shows that members of the Russell 1000, excluding the Magnificent 7, posted median earnings growth of 6% last quarter, down from nearly 9% in Q3 but comparable to Q2 (6%). Looking forward to 2025, analysts continue to forecast U.S. exceptionalism, with forecasts of ~12% earnings growth.

Following Trump’s presidential victory, stocks with greater sensitivity to the U.S. economy, such as small cap businesses, benefitted from expectations of domestically focused growth initiatives. However, stubborn inflation and expectations of fewer interest rate cuts by the Federal Reserve saw the trend of broadening sources of returns pause into the end of the year. Instead, market concentration reaccelerated with investors rushing back towards mega-cap growth stocks. In fact, Tesla – which is approximately 2% of the S&P 500 Index by market cap – contributed approximately one-third of the total index return in Q4, while the Mag 7 as a group contributed over 100% of total returns. In other words, U.S. large cap companies excluding the Magnificent 7 declined in aggregate last quarter.

Canadian Equities: Against the backdrop of cooling inflation and below-trend growth, the Bank of Canada continued to loosen monetary policy. As a result, Canadian companies

showed signs of improving efficiency with return on equity – a gauge of corporate profitability – improving versus prior quarters. Under these conditions, investors remained focused on higher quality, high-dividend paying companies – particularly within the financial sector. Relative to prior quarters, this group witnessed greater contribution out of non-bank financials (such as asset managers and insurance companies), as the premium investors were willing to pay for Canadian banks remained elevated. Across other sectors, the energy sector had a positive quarter as the price of oil stabilized, but falling prices for raw industrials pushed the materials sector lower.

Bottom line: U.S. political developments and subsequent growth expectations dominated market sentiment last quarter. As a result, investors dialed back rate cut expectations and bond yields moved higher. In equity markets, the potential for an era of higher-for-longer rates prompted a resumption of investors crowding into growth stocks. Going forward, we remain cautious of elevated valuations and continue to prioritize diversified sources of returns with a long-term outlook. Nonetheless, despite rich valuations, our base case remains that investors’ enthusiasm for equities will persist in the near-term and stocks should continue to outperform bonds.

Downloadable Copy

ADVISOR USE ONLYMark Warywoda, CFA

VP, Public Portfolio ManagementIan Whiteside, CFA, MBA

AVP, Public Portfolio ManagementJohanna Shaw, CFA

Director, Portfolio ManagementJin Li

Director, Equity Portfolio Management

Tyler Farrow, CFA

Senior Analyst, Equity

Andrew Vermeer

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Francie Chen

Analyst, Rates

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

-

-

Market Commentary July 2025

Key Takeaways

• Markets were very volatile in April to start Q2 but calmed as the quarter progressed. Volatility was driven mostly by headlines about tariffs, but other fiscal policy developments also had an impact.

• Equity markets sold off sharply at the start of the quarter, continuing Q1’s weakness. Markets rebounded sharply once worst-case fears over tariffs eased. The markets continued to rally through the quarter as trade negotiations progressed. Stronger-thanexpected corporate earnings also boosted markets. Despite the shaky start to the quarter, most global equity markets set new all-time highs in Q2.

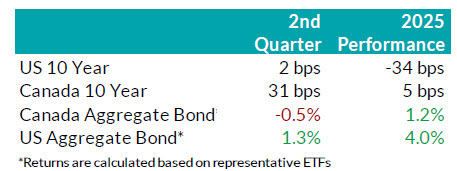

• Canadian bond markets delivered slightly negative returns in Q2. Weak performance was driven by rising interest rates, which outweighed the impact of tighter credit spreads. Higher interest rates hurt the performance of longer-term bonds most.

• Both the Bank of Canada and the U.S. Federal Reserve adopted a wait-and-see approach. They each held rates steady during Q2, awaiting greater clarity on the impacts of tariffs on both growth and inflation before considering further cuts.

Economic and Market UpdateEconomic Summary: Most indicators of economic activity in the U.S. continued to expand at a decent pace. However, GDP data for the first quarter came in weaker than expected, as higher imports ahead of anticipated tariffs and weaker spending by consumers weighed on Q1 GDP. That said, GDP growth is expected to bounce back in Q2. Tariffs will likely continue to be an evolving story, with potential impacts on both economic growth and inflation. Those impacts will remain uncertain until trade agreements have been finalized.

In early April, President Trump announced larger-than-expected reciprocal tariffs, with the impact most notable on trade with China. However, progress followed with a 90-day pause in tariff implementation. The U.S. then reached trade agreements with the UK, China, and Vietnam. Negotiations with other major trade partners are ongoing. The conflict between Israel and Iran raised inflation concerns, due mostly to the possibility of higher oil prices. Those concerns eased following a ceasefire. Congress passed Trump’s tax cut and spending bill, raising concerns about its potential impact on the U.S. fiscal burden. Meanwhile, U.S. labour market conditions remain resilient, with the unemployment rate remaining low. Inflation has eased slightly but remains above the Federal Reserve’s target. Amid heightened uncertainty, the Federal Reserve held interest rates steady at 4.25%–4.50% at both of its meetings in Q2. Chair Jerome Powell stated that the Fed is “well positioned to wait for greater clarity before considering any adjustments to our policy stance.”

.jpg "Fig-One-(1).jpg")

In Canada, tariffs and trade-related uncertainty continue to weigh on the economy. A pullforward of exports and inventory accumulation ahead of tariffs helped keep first-quarter GDP firm, but growth is expected to slow in the second quarter. The labour market has weakened, particularly in trade-sensitive sectors. Inflation remains within the Bank of Canada’s 1–3% preferred range. However, core CPI remains above the Bank’s preferred 2% target. Canada’s fiscal deficit is expected to widen as Prime Minister Mark Carney aims to fast-track infrastructure development and increase defense spending. Amid ongoing trade uncertainty, the Bank of Canada held its policy rate at 2.75% during its April and June meetings. Governor Tiff Macklem signaled the Bank’s readiness to cut rates further if economic conditions deteriorate.

.jpg "Fig-Two-(1).jpg")

Bond Markets: During Q2, the FTSE Canada Universe Bond Index returned -0.6%. Yields for Canadian bonds rose across all maturities over the quarter. That reflected reduced expectations for rate cuts by the Bank of Canada and a higher risk premium on long-term debt. The impact of higher yields on government bonds was offset in part by tightening of credit spreads on provincial and corporate bonds. Overall corporate bonds saw a positive return for the quarter and outperformed government bonds, in part due to the strong recovery in credit spreads that started in late

April. While corporate issuance slowed considerably in April due to increased trade policy uncertainty, issuance in the Canadian bond markets during May and June were robust. There were 83 deals during Q2 that combined to raise $37 billion for issuers. June 2025 was the 3rd busiest month for issuance on record. We continue to expect higher credit spreads as the U.S. tariffs impact global growth. As such, we have maintained our conservative view with a bias towards shorter corporate bonds but remain ready to invest in longer corporate bonds as valuations become

attractive.

.jpg "Fig-Three-(1).jpg")

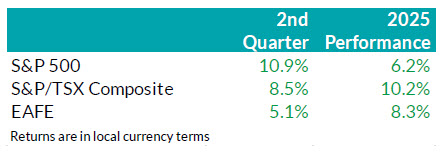

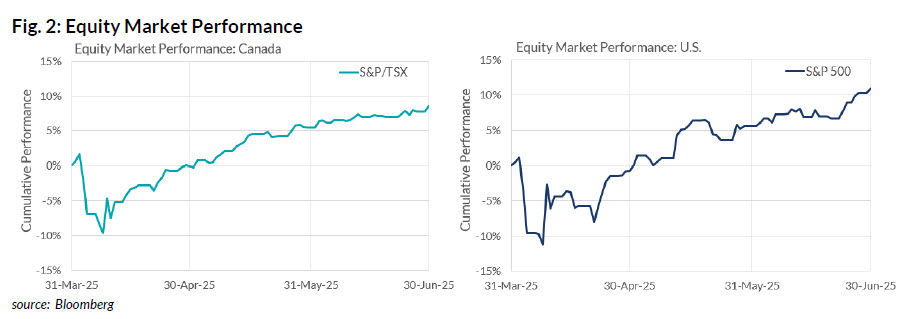

Stock Markets – Overview: Having done a round-trip following April tariff announcements, technology, consumer discretionary and industrial companies propelled the U.S. equity market to another record high. The S&P 500 ended the quarter up about 11%, outperforming Canadian and international markets. Canadian equities gained 8.5% in Q2, buoyed by front-loaded demand that benefited the Materials sector, while Financials recovered from a poor Q1. Meanwhile, as risk sentiment stabilized following the 90-day tariff pause and U.S. equities regained momentum, the appeal of the “Sell America” trade diminished. As a result, Europe, Australasia, and the Far East (EAFE) markets finished the quarter with a more modest gain of just over 5%, lagging the sharper

recovery seen in North America.

.jpg "Fig-Four-(1).jpg")

U.S. Equities: The U.S. equity market staged a V-shaped recovery on strong company earnings data in the second quarter. A stable job market and muted inflation reinforced the view of a resilient U.S. economy. At a company level, we observed positive corporate earnings surprises, steady profit margins and better-than-expected forward earnings guidance. Together they underpinned the equity market’s sharp reversal to the upside. Market breadth also improved over the quarter, with strength extending beyond Technology to include Industrials and Financials. That signalled that the market rally was supported by investors’ confidence in the U.S. economy. Furthermore, structural investment trends in artificial intelligence (AI) continued to accelerate, highlighted by rising enterprise capex in data centres. Beyond AI, Circle, a blockchain-based platform that supports stablecoin issuance, tokenized assets, and digital payment infrastructure, conducted a successful IPO. Its share price jumped 485% from its listing price as of quarter-end. On June 17, the U.S. Senate passed the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act, a regulatory framework for use of tokenized assets. While investors wait for the House’s decision, equity price actions suggest that the policy environment is increasingly supportive of blockchain innovation and digital efficiency.

Canadian Equities: Canadian equities posted solid gains in Q2, with Financials overtaking Materials to lead the market higher. Momentum from the Materials sector, which benefited from the pull-forward demand related to U.S. tariff uncertainty, faded toward quarter-end. Meanwhile, cooling inflation and muted domestic growth pushed investors towards highquality, high-dividend-paying companies. Notably, banks significantly outperformed the broader market, as investors favoured their stable corporate fundamentals. Energy surged briefly amid escalating geopolitical tensions, but those gains proved short-lived. In recap, investors in the Canadian market faced slowing resource demand and a stalling domestic economy, which fueled increased interest in high-quality, high-dividend-paying companies. That is a trend we expect to continue going forward.

Bottom line: Markets remain heavily influenced by sentiment, with U.S. policy developments and ongoing tariff negotiations continuing to cause periodic volatility. However, there is little

evidence of deterioration in the hard data to date. As such, we continue to anchor our positioning on underlying data rather than market narratives. Looking ahead, the combination of a structurally higher-for-longer interest rate environment and increasingly pro-growth policy backdrop presents selective opportunities. In the U.S., this favours highquality growth stocks, particularly within Technology, where strong balance sheets and long-term thematic tailwinds remain intact. In Canada, Financials, especially the relatively inexpensive banks, present a more compelling opportunity as earlier tailwinds from pullforward demand are beginning to wane. While we remain constructive, we are mindful of elevated equity valuations and continue to closely monitor macro conditions and policy developments for signs of inflection.

Downloadable Copy

Mark Warywoda, CFA

VP, Public InvestmentsIan Whiteside, CFA, MBA

AVP, Public InvestmentsJohanna Shaw, CFA

Director, Public InvestmentsJin Li

Director, Equity Investments

Wanyi Chen, CFA, FRM

Sr. Quantitative Analyst

Andrew Vermeer, CFA

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Edward Ng Cheng Hi

Analyst, Credit

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

- [pdf] Non-Face to Face Meetings ID Verification

-

Market Commentary July 2025

Key Takeaways

• Markets were very volatile in April to start Q2 but calmed as the quarter progressed. Volatility was driven mostly by headlines about tariffs, but other fiscal policy developments also had an impact.

• Equity markets sold off sharply at the start of the quarter, continuing Q1’s weakness. Markets rebounded sharply once worst-case fears over tariffs eased. The markets continued to rally through the quarter as trade negotiations progressed. Stronger-thanexpected corporate earnings also boosted markets. Despite the shaky start to the quarter, most global equity markets set new all-time highs in Q2.

• Canadian bond markets delivered slightly negative returns in Q2. Weak performance was driven by rising interest rates, which outweighed the impact of tighter credit spreads. Higher interest rates hurt the performance of longer-term bonds most.

• Both the Bank of Canada and the U.S. Federal Reserve adopted a wait-and-see approach. They each held rates steady during Q2, awaiting greater clarity on the impacts of tariffs on both growth and inflation before considering further cuts.

Economic and Market UpdateEconomic Summary: Most indicators of economic activity in the U.S. continued to expand at a decent pace. However, GDP data for the first quarter came in weaker than expected, as higher imports ahead of anticipated tariffs and weaker spending by consumers weighed on Q1 GDP. That said, GDP growth is expected to bounce back in Q2. Tariffs will likely continue to be an evolving story, with potential impacts on both economic growth and inflation. Those impacts will remain uncertain until trade agreements have been finalized.

In early April, President Trump announced larger-than-expected reciprocal tariffs, with the impact most notable on trade with China. However, progress followed with a 90-day pause in tariff implementation. The U.S. then reached trade agreements with the UK, China, and Vietnam. Negotiations with other major trade partners are ongoing. The conflict between Israel and Iran raised inflation concerns, due mostly to the possibility of higher oil prices. Those concerns eased following a ceasefire. Congress passed Trump’s tax cut and spending bill, raising concerns about its potential impact on the U.S. fiscal burden. Meanwhile, U.S. labour market conditions remain resilient, with the unemployment rate remaining low. Inflation has eased slightly but remains above the Federal Reserve’s target. Amid heightened uncertainty, the Federal Reserve held interest rates steady at 4.25%–4.50% at both of its meetings in Q2. Chair Jerome Powell stated that the Fed is “well positioned to wait for greater clarity before considering any adjustments to our policy stance.”

In Canada, tariffs and trade-related uncertainty continue to weigh on the economy. A pullforward of exports and inventory accumulation ahead of tariffs helped keep first-quarter GDP firm, but growth is expected to slow in the second quarter. The labour market has weakened, particularly in trade-sensitive sectors. Inflation remains within the Bank of Canada’s 1–3% preferred range. However, core CPI remains above the Bank’s preferred 2% target. Canada’s fiscal deficit is expected to widen as Prime Minister Mark Carney aims to fast-track infrastructure development and increase defense spending. Amid ongoing trade uncertainty, the Bank of Canada held its policy rate at 2.75% during its April and June meetings. Governor Tiff Macklem signaled the Bank’s readiness to cut rates further if economic conditions deteriorate.

Bond Markets: During Q2, the FTSE Canada Universe Bond Index returned -0.6%. Yields for Canadian bonds rose across all maturities over the quarter. That reflected reduced expectations for rate cuts by the Bank of Canada and a higher risk premium on long-term debt. The impact of higher yields on government bonds was offset in part by tightening of credit spreads on provincial and corporate bonds. Overall corporate bonds saw a positive return for the quarter and outperformed government bonds, in part due to the strong recovery in credit spreads that started in late

April. While corporate issuance slowed considerably in April due to increased trade policy uncertainty, issuance in the Canadian bond markets during May and June were robust. There were 83 deals during Q2 that combined to raise $37 billion for issuers. June 2025 was the 3rd busiest month for issuance on record. We continue to expect higher credit spreads as the U.S. tariffs impact global growth. As such, we have maintained our conservative view with a bias towards shorter corporate bonds but remain ready to invest in longer corporate bonds as valuations become

attractive.

Stock Markets – Overview: Having done a round-trip following April tariff announcements, technology, consumer discretionary and industrial companies propelled the U.S. equity market to another record high. The S&P 500 ended the quarter up about 11%, outperforming Canadian and international markets. Canadian equities gained 8.5% in Q2, buoyed by front-loaded demand that benefited the Materials sector, while Financials recovered from a poor Q1. Meanwhile, as risk sentiment stabilized following the 90-day tariff pause and U.S. equities regained momentum, the appeal of the “Sell America” trade diminished. As a result, Europe, Australasia, and the Far East (EAFE) markets finished the quarter with a more modest gain of just over 5%, lagging the sharper

recovery seen in North America.

U.S. Equities: The U.S. equity market staged a V-shaped recovery on strong company earnings data in the second quarter. A stable job market and muted inflation reinforced the view of a resilient U.S. economy. At a company level, we observed positive corporate earnings surprises, steady profit margins and better-than-expected forward earnings guidance. Together they underpinned the equity market’s sharp reversal to the upside. Market breadth also improved over the quarter, with strength extending beyond Technology to include Industrials and Financials. That signalled that the market rally was supported by investors’ confidence in the U.S. economy. Furthermore, structural investment trends in artificial intelligence (AI) continued to accelerate, highlighted by rising enterprise capex in data centres. Beyond AI, Circle, a blockchain-based platform that supports stablecoin issuance, tokenized assets, and digital payment infrastructure, conducted a successful IPO. Its share price jumped 485% from its listing price as of quarter-end. On June 17, the U.S. Senate passed the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act, a regulatory framework for use of tokenized assets. While investors wait for the House’s decision, equity price actions suggest that the policy environment is increasingly supportive of blockchain innovation and digital efficiency.

Canadian Equities: Canadian equities posted solid gains in Q2, with Financials overtaking Materials to lead the market higher. Momentum from the Materials sector, which benefited from the pull-forward demand related to U.S. tariff uncertainty, faded toward quarter-end. Meanwhile, cooling inflation and muted domestic growth pushed investors towards highquality, high-dividend-paying companies. Notably, banks significantly outperformed the broader market, as investors favoured their stable corporate fundamentals. Energy surged briefly amid escalating geopolitical tensions, but those gains proved short-lived. In recap, investors in the Canadian market faced slowing resource demand and a stalling domestic economy, which fueled increased interest in high-quality, high-dividend-paying companies. That is a trend we expect to continue going forward.

Bottom line: Markets remain heavily influenced by sentiment, with U.S. policy developments and ongoing tariff negotiations continuing to cause periodic volatility. However, there is little

evidence of deterioration in the hard data to date. As such, we continue to anchor our positioning on underlying data rather than market narratives. Looking ahead, the combination of a structurally higher-for-longer interest rate environment and increasingly pro-growth policy backdrop presents selective opportunities. In the U.S., this favours highquality growth stocks, particularly within Technology, where strong balance sheets and long-term thematic tailwinds remain intact. In Canada, Financials, especially the relatively inexpensive banks, present a more compelling opportunity as earlier tailwinds from pullforward demand are beginning to wane. While we remain constructive, we are mindful of elevated equity valuations and continue to closely monitor macro conditions and policy developments for signs of inflection.

Downloadable Copy

Mark Warywoda, CFA

VP, Public InvestmentsIan Whiteside, CFA, MBA

AVP, Public InvestmentsJohanna Shaw, CFA

Director, Public InvestmentsJin Li

Director, Equity Investments

Wanyi Chen, CFA, FRM

Sr. Quantitative Analyst

Andrew Vermeer, CFA

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Edward Ng Cheng Hi

Analyst, Credit

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

- [pdf] Building a Stronger Investment Portfolio

- [pdf] Custom Quote - Payout Annuity

- New Applications & Transaction Authorization Requirements