Site Search

580 results for enter now access PROBLEMGO.com Buying a guarantee that customs wont open my box Norrkoping

- Chinese Markets

- [pdf] Equitable Guaranteed Investment Funds Understanding sales charge options

- [pdf] Personalized Ads - What does your retirement bucket list include?

- On-Demand Webcasts

- [pdf] Introducing EZBenefits: A better benefits experience for small business

-

EAMG Market Commentary July 2024

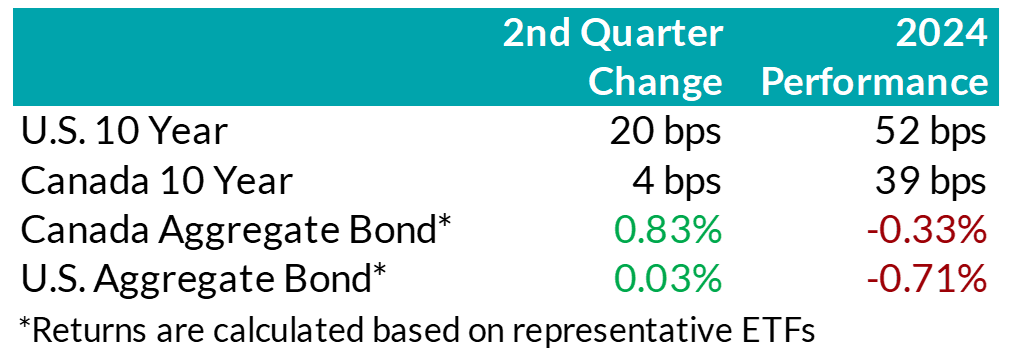

.png "Picture1-(3).png") Rates & Credit – In Q2 2024, U.S. inflation and economic growth data was mixed, leading to moderately higher interest rates in the U.S. Meanwhile, in Canada, long-end interest rates were little changed during the quarter, but short-term interest rates fell. That was due to the weaker economic outlook, as well as the Bank of Canada’s decision to reduce its overnight interest rate in June, with anticipation of further monetary policy easing to come. Canadian corporate bonds returned 1.1%, outperforming the 0.8% return of government bonds as well as the 0.9% return for the overall FTSE Canada Universe Bond index. Shorter-dated bonds outperformed longer-dated bonds. Within corporate bonds, lower-rated BBBs outperformed higher-rated A bonds, while industries that have shorter-dated debt (e.g. real estate and financials) outperformed those that tend to have longer-dated debt (e.g. communications and infrastructure).

Rates & Credit – In Q2 2024, U.S. inflation and economic growth data was mixed, leading to moderately higher interest rates in the U.S. Meanwhile, in Canada, long-end interest rates were little changed during the quarter, but short-term interest rates fell. That was due to the weaker economic outlook, as well as the Bank of Canada’s decision to reduce its overnight interest rate in June, with anticipation of further monetary policy easing to come. Canadian corporate bonds returned 1.1%, outperforming the 0.8% return of government bonds as well as the 0.9% return for the overall FTSE Canada Universe Bond index. Shorter-dated bonds outperformed longer-dated bonds. Within corporate bonds, lower-rated BBBs outperformed higher-rated A bonds, while industries that have shorter-dated debt (e.g. real estate and financials) outperformed those that tend to have longer-dated debt (e.g. communications and infrastructure).

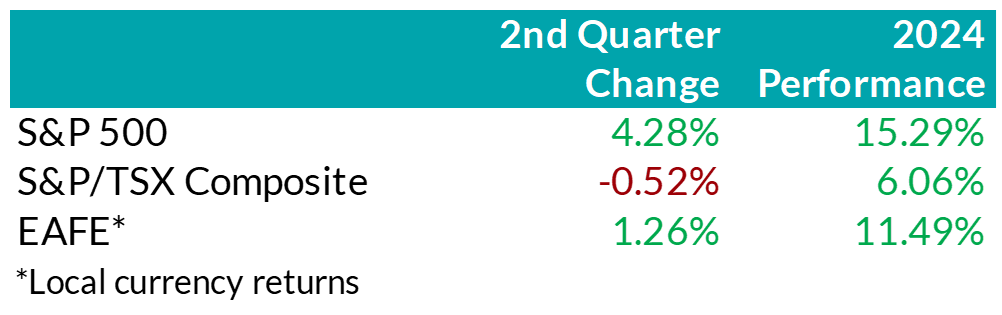

.png "Picture2-(2).png") Equity Overview – Against the backdrop of volatile inflation data and a lack of indication from the Federal Reserve that it was prepared to start cutting interest rates yet, U.S. equity markets decoupled from other regions. Crowding into AI-focused, mega-cap names accelerated in Q2. More specifically, investors defaulted toward the Magnificent 7 to navigate the current period, overlooking broadening earnings breadth and less expensive valuations from the remaining S&P 493. Outside the U.S., equity returns were generally mundane in dollar terms. That said, emerging markets proved to be a bright spot for investors seeking value, as the rebound in heavily discounted Chinese equities helped push frontier markets higher.

Equity Overview – Against the backdrop of volatile inflation data and a lack of indication from the Federal Reserve that it was prepared to start cutting interest rates yet, U.S. equity markets decoupled from other regions. Crowding into AI-focused, mega-cap names accelerated in Q2. More specifically, investors defaulted toward the Magnificent 7 to navigate the current period, overlooking broadening earnings breadth and less expensive valuations from the remaining S&P 493. Outside the U.S., equity returns were generally mundane in dollar terms. That said, emerging markets proved to be a bright spot for investors seeking value, as the rebound in heavily discounted Chinese equities helped push frontier markets higher.

U.S. Fundamentals – Corporate earnings continued to surpass expectations last quarter with stable operating margins helping businesses report better-than-expected bottom line results. Investors remain focused on the ability of companies to sustain debt levels ahead of renewing debt obligations, rewarding businesses with a strong ability to generate stable cash flows. Moreover, while prior quarters have witnessed earnings growth that was largely driven by highly profitable mega-cap technology stocks, U.S. markets are witnessing a broadening trend in earnings strength, with previously stunted segments of the market recovering. Our work shows that members of the Russell 1000 index, excluding the Magnificent 7, posted a median earnings growth of about 6% last quarter, with nearly 60% of companies increasing earnings versus the year prior. Furthermore, we observed an increase in the number of major companies that expect improving financial performance to approximately 27%, suggesting that the recovery in earnings breadth may persist.

U.S. Quant Factors – As mentioned, concentration in the equity market drove a surge in valuations as investors continued to chase specific mega-cap technology stocks. In fact, within the Russell 1000 growth factor – which screens for companies whose earnings are expected to grow at an above-average rate relative to the market – the Magnificent 7 totaled nearly 55% of the entire index by quarter-end. In addition, the Nasdaq 100 – which is generally viewed as a technology-biased index – saw the weight of the Magnificent 7 rise to almost 43% of the entire index by the end of the quarter. Furthermore, the equal-weighted S&P 500 underperformed the cap-weighted index by nearly 7% last quarter, bringing the year-to-date divergence to about 10%. With concentration accelerating, the cap-weighted index outperformance has soared past Covid-era levels, a period that saw investors rapidly crowd into profitable technology names due to panic and economic uncertainty. We remain cautious of a severely crowded market that trades near all-time highs as strong performance from 5-7 names distorts the overall stature of market conditions.

Canadian Fundamentals – Although Canadian companies exceeded bleak forecasts, earnings continue to contract on a year-over-year basis. Furthermore, earnings revisions have grinded lower with easing monetary conditions unable to offset concerns of a slowing economic environment. We note the sharp contrast versus the U.S. as the bifurcation of earnings performance widens. The CRB Raw Industrials Index, a measure of price changes of basic commodities, broke out of recent ranges as metals rallied higher despite a stronger U.S. dollar and elevated interest rates. The mining industry benefited from a sustained elevation in prices, helping the materials sector outperform over the quarter. Returns from the heavily-weighted Canadian banks were constrained last quarter with company-specific drivers – including regulatory challenges from TD, and underwhelming U.S. results from BMO – limiting performance. More broadly, the banks continue to build prudent credit provisions to mitigate uncertain economic forecasts and remain well capitalized.

Canadian Quant Factors – With investors remaining attentive to businesses’ ability to create value relative to financing costs, we see value in high quality, dividend-paying companies with strong earnings sustainability and a healthy degree of leverage. Based on our work, investors of the Canadian banks appear well compensated, with the current premium between value creation and current yield remaining compressed. In our opinion, the market has modest expectations regarding prospects for value generation from the banks and, therefore, we believe the industry stands to benefit if the premium reverts closer to historical norms. We also continue to see sources of quality dividend opportunities within certain areas of the energy sector. More specifically, we believe companies that have taken steps to improve their balance sheets through deleveraging efforts, and with improved operating leverage, offer attractive prospects given their stable and high-yielding composition.

Views From the Frontline

Rates – During the first half of the second quarter, interest rates in both Canada and the U.S. increased, continuing the upward momentum from Q1. Higher-than-expected inflation data in the U.S. along with mixed economic growth data caused investors to push out expectations for when the U.S. Federal Reserve would start lowering its interest rate. This trend shifted in the second half of Q2, as positive economic momentum slowed in the U.S. economy and inflation data began to soften. Interest rates in Canada declined more rapidly than in the U.S. due to more benign inflation, a weaker job market, and economic growth remaining below population growth. This economic weakening provided the confidence required for the Bank of Canada to cut rates by 25 basis points in June to 4.75%. The Bank also signaled that if inflation continues to ease and the Bank’s confidence grows that inflation would continue to trend toward its 2% inflation target, it is reasonable to expect further cuts. The second quarter marked a pivotal point for the global policy easing cycle. Sweden, Canada, and the European Central Bank all began lowering their policy rates, and Switzerland made a second rate cut, following one in Q1. The market continues to speculate on the timing of the U.S. Federal Reserve’s first rate cut. Interest rate cut expectations are largely unchanged in Canada since last quarter, with a total of three rate cuts expected throughout 2024. Expectations for the rate cuts by the U.S. Federal Reserve declined slightly, however, to two cuts in 2024.

Credit – The risk premium for corporate bonds (versus government bonds) was largely flat over the quarter, with spreads approaching the tight post-pandemic levels experienced in 2021. Corporate bond supply continues to be very robust, with $41bn in new issuance. Year-to-date, corporate issuance has set a new record, with an impressive $80bn in issuance. On balance, we do not think the current risk premium adequately compensates for downside risk, particularly in longer-dated corporate bonds, and have a bias towards shorter-dated credit where we view the risk / reward trade-off as being more favourable.

Equity – On the backdrop of a heavily concentrated U.S. market rally, we remain cautious of the distortion to market returns from high-flying technology stocks. As a result, we continue to favour a combination of the Dow Jones Industrial Average and the S&P 500 for our broad U.S. market exposure. The Dow provides a more diversified exposure to 30 prominent large-cap companies and less concentration in technology relative to the S&P. Broadening earnings strength presents an opportunity for previously out-of-favour names to “catch-up”. In our view, companies outside the Magnificent 7 that have demonstrated robust earnings growth, strong cash flow generation, along with decreased debt loads, are well-positioned to benefit from internal market rotations. As such, we gain exposure to these companies through the quality factor – companies with higher return-on-equity, strong operating performance, and healthy leverage levels – and the dividend growth factor – businesses with a lengthy and established history of increasing dividends.

In Canada, we remain attentive to how efficiently corporations are generating profits relative to financing costs. Looking forward, we continue to monitor the ability of businesses to generate profits given a decline in capital spending. More specifically, we are focused on businesses’ ability to grow and sustain dividends amid the lag between easing monetary conditions and consumption. Due to this, we observe value in higher yielding companies that are higher on the spectrum of quality. Geographically, we maintain our overweight U.S. exposure, underpinned by encouraging U.S. inflation data trends, broadening corporate earnings growth, and normalizing consumption. In addition, sluggish Chinese data and the lack of positive earnings revisions from EAFE tilt the risk-adjusted return profile in favour of the U.S. Lastly, as a Canadian investor, fluctuations in the Loonie’s relative value versus other major currencies continues to present tactical trading opportunities within our investment mandate.

Downloadable Copy

Mark Warywoda, CFA

VP, Public Portfolio ManagementIan Whiteside, CFA, MBA

AVP, Public Portfolio ManagementJohanna Shaw, CFA

Director, Portfolio ManagementJin Li

Director, Equity Portfolio Management

Tyler Farrow, CFA

Senior Analyst, Equity

Andrew Vermeer

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

- [pdf] Collateral Loan Suitable Candidate Profile

- [pdf] Building a Stronger Investment Portfolio

-

January 2023 eNews

Responding to Saskatchewan’s biosimilar switch initiative*

We are changing coverage for some biologic drugs in Saskatchewan in response to the province’s biosimilar initiative. These changes will help protect your clients’ plans from additional drug costs that may result from this new government policy while providing access to equally safe and effective lower-cost biosimilars.

Saskatchewan’s provincial biosimilar initiative

Announced in October 2022, the Saskatchewan Biosimilars Initiative ends coverage of ten biologic drugs beginning on April 30, 2023.

Patients in the province who are using these drugs will be required to switch to biosimilar versions of these drugs by April 30, 2023, in order to maintain their Saskatchewan Drug Plan coverage.

Equitable Life’s response

To ensure this provincial change doesn’t result in your clients’ plans paying additional and avoidable drug costs, we are changing coverage in Saskatchewan for most biologic drugs included in the provincial initiative.

Beginning April 30, 2023, plan members in the province will no longer be eligible for most originator biologic drugs if they have a condition for which Health Canada has approved a lower cost biosimilar version of the drug.** These plan members will be required to switch to a biosimilar version of the drug to maintain coverage under their Equitable Life plan.

Communicating this change to plan members

We will inform any affected plan members in early February of the need to switch their medications so that they have ample time to change their prescriptions and avoid any interruptions in treatment or coverage.

What is the difference between biologics and biosimilars?

Biologics are drugs that are engineered using living organisms like yeast and bacteria. The first version of a biologic developed is known as the “originator” biologic. Biosimilars are highly similar to the drugs they are based on and Health Canada considers them to be equally safe and effective for approved conditions.

Questions?

If you have any questions about this change, please contact your Group Account Executive or myFlex Sales Manager.

**The list of affected drugs is dynamic and will change as Saskatchewan includes more biologic drugs in its biosimilar initiative, as new biosimilars come onto the market, and as we make changes in drug eligibility.

Ontario announces 2023 biosimilar switch program*

The government of Ontario recently announced the launch of a biosimilar initiative to switch patients from eight originator biologic drugs to biosimilar versions of the drugs.

Patients in Ontario using affected originator biologic drugs will have until December 29, 2023 to switch to a biosimilar version of their medications in order to maintain coverage under the province’s public drug plans.

We are actively monitoring and investigating the impact of this new policy on private drug plans in Ontario. We plan to implement changes to coverage of biologic drugs in the province in 2023 to help prevent this change from resulting in additional costs for our clients’ drug plans. We will provide more details in the coming months.

If you have any questions, please contact your Group Account Executive or myFlex Sales Manager.

Dental fee guide updates*

Each year, Provincial and Territorial Dental Associations publish fee guides. Equitable Life® uses these guides to help determine the reimbursement limits for dental procedures. For your reference, below is the list of the average dental fee increases for general practitioners that will be used by Equitable Life for 2023.***Dental fee guide increases over 2022***

***Data for all provinces and territories was not available at the time of publication. This chart will be updated on EquitableHealth.ca as more information becomes available.

Equitable Life ranks high with Canadian group advisors*

Equitable Life ranked second nationally and first in Ontario among major insurers in a recent survey of Canadian group benefits advisors.

NMG Consulting, a leading global consulting firm, conducted in-depth interviews with 130 leading group consultants, brokers and third-party administrators across the country between May and August 2022 for its annual Canadian Group Benefits Study. Based on these interviews, NMG ranked group insurers in six categories, ranging from operational management to technology.

Nationally, Equitable Life ranked either first or second in four of the six main categories:

Advisors in Ontario, in particular, scored Equitable Life very favourably. We ranked #1 overall in the province, finishing first in four of the six overall categories, including: Relationship Management, Operational Management, Underwriting and Claims Management and Technology.

“The fact that advisors regard us so highly in so many categories is a testament to our mutual status and our ability to focus exclusively on our clients and advisors,” said Marc Avaria, Senior Vice President of Group. “We are truly working together to build strong, enduring and aligned partnerships.”

“While we are happy with these results, we won’t rest on our laurels,” added Avaria. “We will continue to dedicate ourselves to providing our clients and advisors with a better benefits experience.”

Here are more of the highlights from this year’s results:

Nationally, we ranked first in all 10 subcategories in Operational Management, including:- Overall service to intermediaries,

- Overall service to plan sponsors,

- New quote process,

- Plan implementation,

- Renewal process,

- Information shared at renewal,

- Accuracy and timeliness of reporting and billing,

- Administration quality and responsiveness,

- Taking ownership and

- Management information quality and availability.

- Company relationship management,

- Ease of doing business,

- Account executive capability,

- Market knowledge,

- Visit/call quality,

- Effective coordination and

- Advice.

- Fairness and timeliness of disability claims (1st)

- Fairness and timeliness of health claims (2nd)

- Fraud management (2nd)

- Competitiveness of pooling charges (2nd)

- Group underwriting flexibility (3rd)

- Health and dental TLR competitiveness (3rd)

- Overall technology – Intermediary (2nd)

- Member experience (2nd)

- [pdf] FeelingBetterNow