Site Search

384 results for enter secure MAKEMUR.com Looking to pay a judge for a dismissal signature

-

Message from Ron Beettam

As COVID-19 continues to spread, we want to reassure you that we remain ready and committed to support you and your clients.

We have a robust and well-tested business continuity plan in place and our business is almost 100% digital. Almost 90% of our employees are now working remotely from home and are maintaining the high level of service you have come to expect from us. We still have a fully functioning Document Services Centre that is managing our incoming and outgoing mail. Our sales and customer service teams remain open to support you and your clients.

Equitable Life’s online application process, EZcomplete®, offers non face-to-face capability and continues to be your go-to resource for managing your business virtually. We are receiving a record number of online applications and are committed to helping you maintain a certain degree of daily activity. EZcomplete® non-face-to-face works for all life, critical illness and segregated fund applications.

Advisors will be pleased to know that we have increased non-medical limits for life insurance. We are also looking at other underwriting changes, digital delivery of life insurance contracts and additional digital payment options.

Our Savings & Retirement advisors will find our new Transaction Authorization Requirements table a valuable resource for submitting forms and documents. Can’t meet with your client in person to get a signature? Not to worry. You can have your client sign a letter of direction and take a picture to authorize a number of transactions.

Transacting in a non face-to-face environment can be a challenge but we will continue to revisit existing processes and look for ways to modify requirements to help you to continue managing your business. All of us are facing an unprecedented number of urgent situations where there is no established protocol. Our commitment to you and your clients is to respond quickly, and to be flexible where we can, tailoring solutions to specific needs.

To stay up-to-date, please refer to Equitable Life’s COVID-19 information page. There you will find the latest information for all lines of business.

As the global situation continues to evolve rapidly, we ask for your patience as our solutions also evolve quickly and accordingly. Rest assured that Equitable Life is unwavering in our support, and we will be here to help you protect what matters most to Canadians.

Ron Beettam, President and CEO -

Equitable Life Group Benefits Bulletin – May 2020

In this issue:

- Digital options for your clients and their plan members*

- Alberta delaying biosimilar initiative*

- Yukon increasing insurance premium tax*

- Manitoba and New Brunswick relaxing drug limits*

- Free guide to accessing virtual healthcare*

- Homeweb for plan members who are losing coverage*

*Indicates content that will be shared with your clients

Easy and convenient digital resources for your clients and their plan membersDuring this time of physical distancing, people are looking for ways to interact with their providers virtually. We have several convenient digital tools available to make it easier for your clients and their plan members.

For plan administrators:

Plan administrator portal (EquitableHealth.ca)Our secure portal allows plan administrators to easily manage their plan anytime and anywhere. Instead of printing and mailing forms, they can make real-time updates at their convenience. The site also makes it easy to:

- View or upload forms and other important documents;

- Retrieve billing information;

- Estimate monthly premium costs; and

- View announcements, tips and reminders.

Plan administrators can visit www.equitablehealth.ca to activate their account.

Digital Welcome Kits

Instead of paper kits that can easily get lost or quickly become outdated, plan members receive personalized welcome kits via an interactive email, including instructions on how to:

- Activate their online group benefits account;

- Download their digital benefits card;

- Submit claims from their computer or mobile device;

- Review their coverage details; and

- Explore health and wellness resources.

Easy automated payments

Automated payments are a convenient way to avoid missed payments, suspended claims and disruption. Plan administrators simply complete the pre-authorized debit form and send to GroupCollections@equitable.ca. Or contact Group Collections about online banking and electronic funds transfer (EFT).

We can help

For assistance, plan administrators can contact their Client Relationship Specialist or our Web Services team at 1.800.265.4556 ext. 283 or groupbenefitsadmin@equitable.ca.

For plan members:

Plan member portal (EquitableHealth.ca)By logging into EquitableHealth.ca, plan members have secure 24/7 access to their personalized Group Benefits account. They can:

- View and submit claims;

- Review their coverage details; and

- Access health and wellness resources.

Electronic claims payment and notifications

Once plan members have activated their Group Benefits account on EquitableHealth.ca, they can easily set up receiving their claim payments via direct deposit, and their claim notifications via email.

EZClaim Mobile App

Submitting claims is fast, easy and secure with the Equitable EZClaim® mobile app for iOS and Android devices. Plan members can view and submit health and dental claims and review their coverage details.

Digital Benefits Cards

Instead of digging through their wallets, plan members can download a digital version of their benefits card to their mobile device.

We can help

We’ve created a video guide to help plan members access and use their digital resources. For further assistance, plan members can contact our Web Services team at 1.800.265.4556 ext. 283 or groupbenefitsadmin@equitable.ca.

Alberta government delaying biosimilar initiativeAs we announced in the February 2020 issue of eNews, the Alberta Biosimilar Initiative will require patients using several originator biologic drugs to switch to a biosimilar in order to maintain coverage through their Alberta government sponsored drug plan.

Due to the increased demands the COVID-19 pandemic is placing on healthcare providers, the Alberta government has postponed the switching requirement. Affected patients will now have until January 15, 2021 to switch to the biosimilar version of their drug in order to maintain provincial coverage.

We continue to investigate appropriate options to help ensure this provincial change does not unreasonably impact Equitable Life groups and patients and will keep you informed.

For more information about the Alberta Biosimilars Initiative, consult the Alberta government website.

Yukon increasing Insurance Premium TaxThe Yukon Government has announced that it plans to increase its Insurance Premium Tax rates effective January 1, 2021. The premium tax rates for group life and accident and sickness insurance are expected to increase from 2% to 4%. The new tax rates will be applied to premiums paid on or after January 1, 2021.

Manitoba and New Brunswick relaxing drug limitsIn order to protect the drug supply during the COVID-19 crisis, residents of most provinces were temporarily limited to receiving a 30-day supply of drugs when filling a prescription. Normally, doctors prescribe a 90-day supply for most maintenance-type drugs.

The Government of Manitoba and the Government of New Brunswick are now relaxing this 30-day limit for prescription drugs where shortages do not exist. They will address potential shortages of specific drugs if necessary.

As the situation continues to evolve, there may continue to be changes to provincial legislation and prescription limits. Plan members should speak to their pharmacist for the most up to date information.

Free guide to accessing virtual healthcareWith many health clinics closed and the healthcare system under strain, people are looking to access a doctor and other health providers virtually.

As we announced previously, we’ve made it easier for plan members to find the information they need using our Guide to Accessing Virtual Healthcare. This online resource provides information about and links to a range of virtual health services they need to take care of their health and the health of their family during these challenging times.

The Guide also indicates which services are covered by public health plan, so there’s no cost to the patient to access them if they provide their valid provincial health card.

We will continue to update the Guide as more virtual healthcare providers and services become available.The Guide is available on both EquitableHealth.ca and Equitable.ca.

Homeweb for plan members who are losing coverageWe know these are difficult times for Canadian employers and their employees. As businesses temporarily suspend operations, some employers have had to make the difficult decision to temporarily lay off employees or put their benefits coverage on hold.

That’s why we were pleased to announce that Homewood Health® and Equitable Life will extend access to Homeweb, a personalized online mental health and wellness portal, for up to 120 days for plan members who have temporarily lost their benefits coverage due to COVID-19.

Employees and their family members will continue to have access to the Homeweb website and mobile app, including:

- iVolve, online self-directed Cognitive Behavioural Therapy;

- Resources to support themselves and their family members through the COVID-19 pandemic;

- An interactive online Health Risk Assessment; and

- An online library of tools, assessments and e-courses.

This will allow businesses undergoing financial hardship to provide some support to employees who are temporarily without benefits coverage.

- [pdf] Pivotal Select Application - Registered/Non-Registered

-

Market Commentary January 2026

.png "EAMG-(1).png")

Key Takeaways

Full year 2025:

• Government policy was very impactful for markets in 2025. U.S. trade policy unsettled markets in the first half of the year, as the U.S. implemented significant tariffs and engaged in tough negotiations with major trading partners. However, by mid-year, fiscal policy provided positive support for markets, particularly with the passing in the U.S. of the One Big Beautiful Bill Act in July.

• Artificial Intelligence (“AI”) continued to attract investment, particularly in the United States. This investment provided strong support for equity market performance.

• Global equity markets delivered strong performance, most notably Canadian equities, which returned an impressive 31.7%.

• Positive risk appetite supported solid corporate bond performance, which outpaced government bonds.

Fourth Quarter:

• U.S. equities advanced at a slower pace in the fourth quarter after a strong surge in the prior two quarters. Canadian equities outperformed U.S. equities, fueled by a powerful rally in the Materials, Consumer Discretionary, and Financials sectors.

• Canadian bond markets posted slightly negative returns during the quarter as higher interest rates weighed on performance. Strong corporate bond performance partially offset weakness in government bonds.

• Both the Bank of Canada and the U.S. Federal Reserve lowered policy interest rates during the quarter, with Canada dropping its benchmark rate by 25 basis points and the U.S. dropping its policy rate by 50 basis points. Both central banks signalled a cautious approach for further easing.

Economic and Market UpdateEconomic Summary: The U.S. economy continued to expand at a moderate pace, supported by strong consumer spending and AI investment. However, job growth slowed and the unemployment rate has edged higher. Inflation remains higher than the 2% target, despite easing trends. While some U.S. trading partners have made trade agreements, uncertainty remains regarding reciprocal tariffs, with a case before the U.S. Supreme Court as to their legality. The Federal Reserve lowered its policy interest rate twice during the quarter, first in October and again in December, to reach a target rate of 3.50% to 3.75%. Chair Powell cited downside risks to employment as a key factor behind the rate cut decisions and emphasized that officials are “well positioned” to wait and assess how the economy evolves.

In Canada, U.S. tariffs on steel, aluminum, autos, and lumber have weighed heavily on these sectors. While most goods continue to enter the U.S. tariff-free due to the Canada-United States-Mexico Agreement (“CUSMA”), broader uncertainty around U.S. trade policy is dampening business investment. Third quarter GDP growth exceeded market expectations, but growth tracked weaker in the fourth quarter amid the trade disputes. The labour market showed signs of improvement in the fourth quarter after earlier weakness. Headline inflation has hovered near the 2% target, while core inflation remained persistent. The Bank of Canada lowered its policy interest rate by 25 basis points to 2.25% in October and made no changes in December. Going into 2026, trade uncertainty remains with the CUSMA up for renegotiation. The Bank of Canada reiterated its readiness to respond if new shocks or accumulating evidence materially alter the outlook.

Bond Markets: During the quarter, the FTSE Canada Universe Bond Index returned -0.3% as interest rates on Canadian bonds rose (bond prices fall as interest rates go up). The increase reflected reduced expectations for interest rate cuts by the Bank of Canada and a higher risk premium demanded by investors for long-term debt. Although interest rates increased, credit spreads (i.e. the extra yield on corporate bonds versus government bonds to compensate for their extra risk) continued to move lower. These lower credit spreads resulted in positive overall returns for corporate bonds in the quarter, despite the overall bond market recording a loss. Tightening credit spreads reflected the continued risk-on tone to the market. Despite some volatility, lower-rated BBB bonds generally performed better than higher-quality A-rated bonds. Credit spreads have now rallied back to the tightest spreads since the 2008 financial crisis, nearing the tightest spreads in history. Despite expensive levels, investors remain buyers of corporate bonds, evidenced not just by falling credit spreads, but also by investors’ enthusiasm to support the primary issuance market. Corporate bond supply continues to set new records, with an impressive $37.5 billion in new issuance in the fourth quarter helping 2025 to exceed the prior year’s issuance. All told, 2025 saw an impressive $160 billion in new issuance via 358 new bonds, versus 2024’s prior record of $139 billion from 301 new bonds.

Bond Markets: During the quarter, the FTSE Canada Universe Bond Index returned -0.3% as interest rates on Canadian bonds rose (bond prices fall as interest rates go up). The increase reflected reduced expectations for interest rate cuts by the Bank of Canada and a higher risk premium demanded by investors for long-term debt. Although interest rates increased, credit spreads (i.e. the extra yield on corporate bonds versus government bonds to compensate for their extra risk) continued to move lower. These lower credit spreads resulted in positive overall returns for corporate bonds in the quarter, despite the overall bond market recording a loss. Tightening credit spreads reflected the continued risk-on tone to the market. Despite some volatility, lower-rated BBB bonds generally performed better than higher-quality A-rated bonds. Credit spreads have now rallied back to the tightest spreads since the 2008 financial crisis, nearing the tightest spreads in history. Despite expensive levels, investors remain buyers of corporate bonds, evidenced not just by falling credit spreads, but also by investors’ enthusiasm to support the primary issuance market. Corporate bond supply continues to set new records, with an impressive $37.5 billion in new issuance in the fourth quarter helping 2025 to exceed the prior year’s issuance. All told, 2025 saw an impressive $160 billion in new issuance via 358 new bonds, versus 2024’s prior record of $139 billion from 301 new bonds.

Stock Markets: The fourth quarter marked a pivotal shift in the global equity market rally of 2025. After three quarters of a highly concentrated, tech-led rally in the U.S., cyclical and valueoriented sectors outperformed in Q4. The S&P 500 advanced at a slower 2.7% in the fourth quarter, reflecting a market that is recalibrating after an extended period of concentrated gains. Canadian equities outperformed U.S. equities as the S&P/TSX Composite returned 6.3% in the quarter, finishing the year with an impressive 31.7% return. That was its strongest annual gain since 2009. The strong returns in Canadian equities were fueled by a powerful rally in the Materials sector, supported by soaring gold and base metal prices, and reinforced by the resilience of the Consumer Discretionary and Financials sectors. Internationally, developed markets in Europe and Asia gained 6.2% for the quarter, bringing their annual return to 21.2%. This move signals a healthy rebalancing as global investors rotated into attractivelyvalued international equities to hedge against elevated U.S. valuations. Capital is now flowing toward regions and sectors offering stronger earnings visibility and defensive characteristics rather than purely speculative growth.

Stock Markets: The fourth quarter marked a pivotal shift in the global equity market rally of 2025. After three quarters of a highly concentrated, tech-led rally in the U.S., cyclical and valueoriented sectors outperformed in Q4. The S&P 500 advanced at a slower 2.7% in the fourth quarter, reflecting a market that is recalibrating after an extended period of concentrated gains. Canadian equities outperformed U.S. equities as the S&P/TSX Composite returned 6.3% in the quarter, finishing the year with an impressive 31.7% return. That was its strongest annual gain since 2009. The strong returns in Canadian equities were fueled by a powerful rally in the Materials sector, supported by soaring gold and base metal prices, and reinforced by the resilience of the Consumer Discretionary and Financials sectors. Internationally, developed markets in Europe and Asia gained 6.2% for the quarter, bringing their annual return to 21.2%. This move signals a healthy rebalancing as global investors rotated into attractivelyvalued international equities to hedge against elevated U.S. valuations. Capital is now flowing toward regions and sectors offering stronger earnings visibility and defensive characteristics rather than purely speculative growth.

U.S. Equities: U.S. equities entered the fourth quarter at elevated valuations. Despite fundamentally strong earnings growth, stock prices struggled to move higher because investor expectations were for even stronger growth. Technology remained the primary driver of earnings, but the sector faced intense pressure to prove its value. Specifically, investors questioned the pace at which companies could convert AI investments into actual revenue. Investors also worried that growth remained concentrated among too few companies rather than more broadly across the economy. Sector-wise, Communication Services emerged as the top performer for the full year due to significant margin expansion. This was driven by a wave of media-related merger activity and the successful use of AI to make digital advertising more efficient. Industrials also advanced as new tax incentives for domestic manufacturing boosted factory orders. Nevertheless, the market remains concentrated with the top ten stocks representing nearly 40% of the S&P 500 Index. This level of concentration makes the market vulnerable to sudden price swings. As inflation moderated and the Federal Reserve cut rates in December, investors shifted toward more defensive sectors and international equities. This rotation signals a preference for companies with stable cash flows over speculative growth.

Canadian Equities: The Canadian market was a global standout during the quarter, supported by lower borrowing costs, a stable Financials sector, and rally in the prices of metals (including gold, but also base metals like nickel and copper). The Materials sector led the way as a weaker U.S. dollar and geopolitical tensions pushed gold to a record of US$4,550 per ounce in late December. For major mining companies, these prices generated record cash flow allowing them to raise dividends and buy back shares. The Bank of Canada interest rate cut supported both the Consumer Discretionary and Financials sectors, reducing borrowing costs, and helping banks maintain stable net interest margins. The Big Six Canadian Banks delivered strong earnings results in Q4. These were driven by a surge in capital markets activity and better-than-expected provisions for credit losses, as the economy remained resilient. Trading at 17 times forward earnings, the Canadian market appears attractively valued, prompting investors to shift away from U.S. volatility toward more tangible assets and reliable dividends.

Bottom line: The final quarter of 2025 saw a notable shift in investor positioning. As recession fears receded, attention turned to navigating a period of moderate economic expansion. In Canada, capital flowed into profitable, cash flow-generating companies in the Financials and Material sectors. Momentum in U.S. equities slowed as investors reduced risk amid caution around AI developments. Although major indices remain highly valued, opportunities persist in sectors and regions with stable cash flows and pricing power.

Downloadable Copy

Mark Warywoda, CFA

VP, Public InvestmentsIan Whiteside, CFA, MBA

AVP, Public InvestmentsJohanna Shaw, CFA

Director, Public InvestmentsJin Li

Director, Equity Investments

Wanyi Chen, CFA, FRM

Sr. Quantitative Analyst

Andrew Vermeer, CFA

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Edward Ng Cheng Hin

Analyst, Credit

Kate (Huyen) Vinh

Analyst, Equity

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy. -

EAMG Market Commentary January 2024

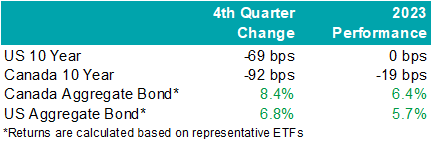

Rates & Credit – Interest rates decreased sharply in Q4 as the market priced in aggressive interest rate cuts by central banks in 2024. The prospect of lower interest rates also drove a strong risk-on tone to the market, with the risk premium on corporate bonds grinding tighter as prospects for a “soft landing” improved. The rally in interest rates resulted in the best quarter for bonds over the past 15 years, with the FTSE Canada Universe Index returning 8.3%. Corporate bonds modestly underperformed the Universe Index with a return of 7.3%. The lower return for corporate bonds was primarily driven by the fact that the corporate bond index is less sensitive to interest rate movements (as compared to the government index), partially offset by the risk-on tone to the market. Within corporate bonds, lower-rated BBBs outperformed higher-rated A bonds. Industries with higher interest rate exposure such as infrastructure, energy, and communications outperformed those with less exposure (notably financials and securitization), consistent with the overall shift in the yield curve.

.png "image1-(1).png")

Santa Came to Town – Moving in sync with bonds, global equities jolted higher into the end of the year with cooling inflation data and dovish comments from central bankers. The U.S. market outperformed most regions last quarter with the S&P 500 returning 11.7% in USD terms, bringing the total return in 2023 to 26.3%. The TSX added 8.1% in Q4, boosting the total annual return to 11.8%. Meanwhile, major developed economies from Europe, Australasia, and the Far East (EAFE) gained 5.0% in local currency terms over the quarter, helping the region produce a 16.8% return from the year prior. Prospects of interest rate cuts by the Federal Reserve saw the Loonie rally into year-end and resultantly, investors of Canadian dollar securities witnessed enhanced returns. Strong domestic U.S. economic data helped value pockets of the market outperform. That said, this was not a synchronized trend as China’s economic disappointment weighed on the performance of EAFE.

U.S. Fundamentals – Our work shows that investors are shifting their focus away from operating margins and towards the ability to sustain debt levels ahead of renewing debt obligations. Corporate earnings beat modest expectations last quarter, contracting by less-than-expected on a year-over-year basis. Resilient operating margins continue to attract investors into equities. After three consecutive quarters of improving forward earnings guidance, we observed that the number of major companies expecting deteriorating financial performance grew to ~35%. We note that this is a sharp contrast relative to the optimistic run-up in equity valuations. In general, corporate pessimism has been underpinned by concerns for the health of the consumer, increasing wage pressures, and inflation.

U.S. Quant Factors – While mega-cap technology stocks gave back some ground in the second half, crowding into the magnificent 7 remains noticeable with the cap weighted S&P 500 outperforming the equal weighted index by 12.5% last year. That said, value areas of the market – which underperformed through the first three quarters of the year – were top performing companies last quarter as the prospects for an economic “soft-landing” improved with U.S. inflation continuing to ease without substantial deteriorations of employment or output data. Quality-growth businesses initially outperformed as the higher-for-longer narrative continued to drive investors toward large cash-rich companies with stable margins. That said, this basket of companies gave back relative returns into quarter-end as weakness in operating margins persisted, making fundamentals appear stretched. Low volatility stocks (i.e. stocks with lower sensitivity to broad market movement and lower price volatility) rallied to start the quarter before dovish comments from central bankers improved risk-sentiment and ultimately pushed this basket lower on a relative basis. Lastly, dividend growth companies, which include businesses with a lengthy and established history of increasing dividends, underperformed the broader index as market participants punished businesses that slowed capital growth projects during the rising interest rate environment. While operating margins have declined, the basket’s strong cash flow and low debt burden may be advantageous if the market’s anticipation of impending interest rate cuts proves to be incorrect or mistimed.

Canadian Fundamentals – Although Canadian companies exceeded bleak forecasts last quarter, earnings continue to contract on a year-over-year basis. Return on equity (ROE) – a gauge of how efficiently a corporation generates profits – continued to decline last quarter while corporate costs of capital remain elevated. In essence, Canadian companies are generating less value relative to their financing cost. Value creation underpins the sustainability of dividend payments, which are a unique and desirable attribute of the Canadian market. Meanwhile, the Bank of Canada held its overnight interest rate unchanged with market participants forecasting a higher probability of interest rate cuts in 2024. On the expectations of easing monetary conditions, dividend yields compressed while earnings forecasts improved with analysts predicting that index aggregate earnings will grow 6% to 8% in 2024. At a sector level, the energy industry’s financial performance normalized – in line with expectations – as weakening oil demand expectations overshadowed geopolitical conflict in the Middle East, ultimately pushing crude prices ~21% lower last quarter. The industrials and financials sectors beat expectations, helping offset softer-than-expected results from the consumer staples and technology sectors.

Canadian Quant Factors – The Canadian banks underperformed for most of the year as they reported increasing provisions for nonperforming loans, reflecting forecasts of worsening economic conditions. That said, expectations of interest rate cuts in 2024 helped tame recession fears and eased concerns of slowing loan growth, propelling banks higher in the fourth quarter as they appeared more stable and therefore favourable than prior estimates. The high-quality basket underperformed last quarter as improving risk sentiment in the market reduced the attractiveness of secure companies with lower earnings variability. Furthermore, high dividend payers with solid growth prospects outperformed in the fourth quarter as market participants rewarded companies that demonstrated a strong ability to support future dividends and punished high yielding businesses with less certain financial capabilities.

Views From the Frontline Rates – Interest rates declined sharply in Q4 as inflation continued to trend lower, fears of excess bond supply declined, and the Federal Open Market Committee signaled that the next change to their overnight policy interest rate would likely be lower. Labour market and consumer spending data remain resilient however businesses have indicated slowing across industries, more price-sensitive consumers, rising delinquencies, and concerns about the high cost of debt. Central banks remain committed to achieving their 2% inflation target and most acknowledge that interest rates have likely peaked.

Credit – The risk premium for corporate bonds (versus government bonds) tightened materially over the quarter, with a strong risk on tone to the market as investors priced in lower interest rates in 2024 and a “soft-landing” to economic concerns. Corporate bond supply was well received by the market. On the balance, we do not think the current risk premium adequately compensates for downside risk, and as such, we remain cautious on corporate bonds and have a bias towards higher-quality, shorter-dated credit where we view the risk / reward dynamic as being more favourable.

Equity – In the U.S., we allocated exposure to value names which outperformed over the quarter as the macroeconomic outlook improved on the backdrop of rate cut expectations. Looking forward, we expect that margins will continue to normalize as Covid-induced pent up demand fades. While we do not forecast margins to compress at an alarming rate, we believe sticky wage and input costs will continue to pressure businesses while consumers exhibit further exhaustion. As such, we are shifting our focus toward the balance between company reinvestment in capital projects and upcoming debt refinancing requirements. In line with this view, we favour businesses with stable cash flows and decreased debt loads as we believe they present an attractive contrarian opportunity if soft-landing projections prove to be overstated. Within Canada, we remain attentive to the inverse movements of ROE relative to financing costs over 2023. With the excess between ROE and financing costs compressing, businesses’ ability to create value appears more stretched than earlier in 2023. Therefore, we continue to favour high quality companies in Canada, which is typically defined by high ROE, stable earnings variability, and low financial leverage. Geographically, the U.S. economy appears to be in healthier condition with inflation easing while employment and output data remain stable and hence, our focus will be on capital expenditures. EAFE – which is generally more economically linked to China than North America – contains a large bucket of stable, high-quality businesses that may benefit from any upside economic surprises out of China. Lastly, through the lens of a Canadian investor, the Loonie’s relative value versus other major currencies presents another resource in our investment mandate to derive excess return.Downloadable Copy

Mark Warywoda, CFA

VP, Public Portfolio ManagementIan Whiteside, CFA, MBA

AVP, Public Portfolio ManagementJohanna Shaw, CFA

Director, Portfolio ManagementJin Li

Director, Equity Portfolio Management

Tyler Farrow, CFA

Senior Analyst, Equity

Andrew Vermeer

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

ADVISOR USE ONLY

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

-

Equitable Life Group Benefits Bulletin – November 2021

In this issue:

- Deadline to opt out of New Brunswick biosimilar program*

- Web Reports Quick Reference Guide now available for plan administrators*

- Reminder: Review manual allocations for HCSAs and/or TSAs*

- Help your clients take advantage of our convenient digital options*

Reminder: Deadline to opt out of New Brunswick biosimilar program*

Earlier this year, we announced via eNews that on Feb. 1, 2022, we are ending coverage for some originator biologic drugs in New Brunswick in response to the province’s Biosimilar Initiative.* These changes will help protect your clients’ plans from additional drug costs while still providing access to equally safe and effective biosimilars.

Do my clients need to take any action?

No action is required if employers want to have the originator biologics excluded from their plan. Plan members taking these targeted originator biologics will be contacted directly to allow them ample time to transition to the biosimilar. Any cost savings associated with the change will be factored in at renewal.

All groups, except myFlex clients, who wish to opt out of this change and maintain coverage of these originator biologics for existing claimants in New Brunswick can submit a policy amendment. Amendments must be submitted no later than Nov. 30, 2021.

Advisors with myFlex Benefits clients who wish to maintain coverage of these originator biologics for New Brunswick plan members should speak to their myFlex Sales Manager to confirm their eligibility to opt out of this change.

Groups that opt out of this change are also opting out of any future changes to our New Brunswick biosimilar initiative. This means that their drug plans will continue to cover any additional originator biologics for which we subsequently end coverage as part of the biosimilar program.

Questions?

If you have a question that isn’t answered here, please contact your Equitable Life Group Account Executive or myFlex Sales Manager.

* The list of affected drugs or conditions is dynamic and may change.Web Reports Quick Reference Guide now available for plan administrators

A Web Reports Quick Reference Guide is now available for plan administrators on EquitableHealth.ca. This new guide offers a listing of our newest reports available on the plan administrator web. It also provides instructions for plan administrators outlining how to pull the report using the plan administrator portal.

The guide is available under the Quick Links section on both the advisor and plan administrator portals on EquitableHealth.ca.Reminder: Review manual allocations for HCSAs and/or TSAs*

If your client’s Health Care Spending Account (HCSA) and/or Taxable Spending Account (TSA) has manual allocations, they need to allocate these amounts to plan members each year. Please review all your plan members’ profiles on EquitableHealth.ca to ensure they have received their allocation(s) for the current benefit year.

If your clients have Plan Administrator update access on EquitableHealth.ca, they can update these amounts online by doing the following:- Select “View certificate”

- Select “Health Care Spending Account” or “Taxable Spending Account”

- Select “Update Allocation” in Task Center

- Enter amount in “Revised Allocation Amount”

- Override Reason – “Plan Administrator Request”

- Select “Save”

- Select “Reports”

- Select “New”

- Select “Next”

- Select “HCSA” or “TSA Totals by Plan Member”

- Select “Next”

- Enter end date of “12/31/2020”

- Select “Next”

- Select “Finish”

- View “Report”

Help your clients take advantage of our convenient digital options*

We have several digital options available to make it easier for your clients to do business with us and for their plan members to access and use their benefits plan. Over 71% of plan administrators are managing their plan online and 78% of plan members are already using our digital tools.

For plan administrators:- Online Plan Member Enrolment tool – allows all groups to add new plan members without the need for paper forms

- Plan Administrator Portal (EquitableHealth.ca) – plan administrators can easily manage their plan anytime and anywhere

- Digital Welcome Kits – personalized welcome kits are delivered to plan members via email

- Easy automated payments – plan administrators can avoid missed payments by setting up pre-authorized debit or electronic funds transfer

- Plan Member Portal (EquitableHealth.ca) – plan members get secure, 24/7 access to their claims history, coverage details and health and wellness resources

- Electronic Claim Payments and Notifications – plan members can get claim updates sooner in their email inbox and payments right into their bank account

- EZClaim Mobile App – submitting claims from a mobile device is fast, easy and secure

- Digital Benefits Cards – plan members no longer have to dig through their wallet – they can download their benefits card on their mobile device

We’ve created a brochure and a video guide to help plan members access and use their digital resources. For further assistance, plan members can visit www.equitable.ca/go/digital. They can also contact our Web Services team at 1.800.265.4556 ext. 283 or groupbenefitsadmin@equitable.ca. -

Market Commentary January 2025

Key Takeaways

Full year 2024:

-

Despite reductions of policy-setting interest rates by central banks, yields on longer-term bonds finished the year higher than they started the year.

-

Positive risk appetite helped corporate bonds perform well, led by lower-quality issuers.

-

Global equity markets posted robust returns, with U.S. equities outperforming other developed markets, driven by heavy concentration into the ‘Magnificent 7’ stocks.

Fourth Quarter:

-

Central banks continued to ease monetary policy in Q4, with the Bank of Canada cutting its policy interest rate more aggressively than did the U.S. Federal Reserve.

-

The Republican victory across both the executive and legislative branches in the U.S. ignited expectations of economic growth, pushing bond yields and stock prices higher.

-

Risk sentiment helped corporate bonds continue to outperform government bonds.

-

Markets remained volatile: while North American stock markets continued to outperform most international indices, Canadian stocks managed to outperform U.S. stocks in Q4, as sources of returns in the U.S. narrowed into year-end.

Economic and Market Update

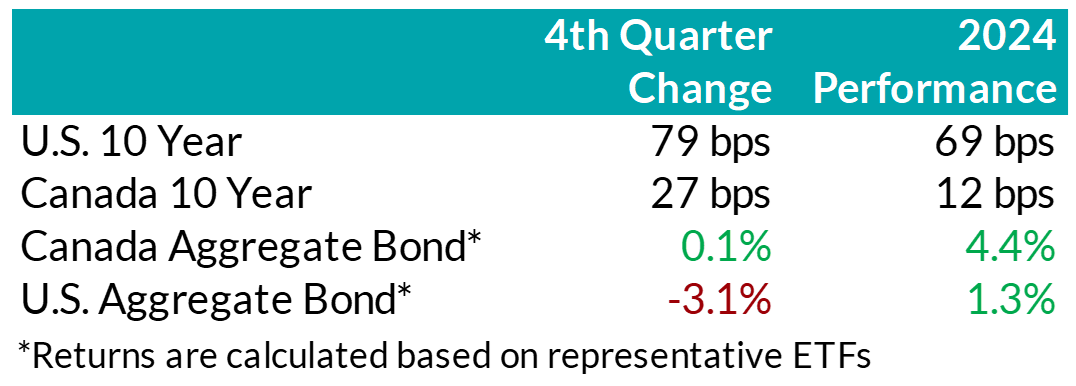

Economic Summary: In the U.S., economic activity continued to expand at a solid pace in Q4. The rate of inflation continued to slow but remained above the central bank’s 2% objective. The labour market in the U.S. remained resilient, as the unemployment rate has remained low compared to historical norms. A decisive victory for Donald Trump and the Republican Party further boosted expectations for continued growth. The return of the President-elect’s old tactics of threatening tariffs to influence trade, security, and drug control re-introduced some economic uncertainty, particularly regarding the potential return of inflationary pressures. Those concerns prompted the Federal Reserve to slow the pace of its policy easing, as it lowered rates by just 0.25% at each of its two meetings in Q4, following the 0.50% cut in September. Throughout 2024, the Fed reduced rates by a total of 100 basis points, from 5.50% to 4.50%. Nonetheless, bond yields were significantly higher for most maturity terms during the fourth quarter as the market priced in not just a stronger economy than had been the expectation during Q3, implying less interest rate cuts by the Fed, but also growing concerns about the government deficit.

In Canada, growth remained positive during 2024 and improved a bit to close the year, but continued to fall short of the Bank of Canada’s expectations. Similarly, inflation came in lower than expected and below the Bank’s 2% target. The labour market continued to soften for much of the year, with employment growth falling short of labour force growth. The weakness in the labour market and economy, along with tamed inflation, prompted the Central Bank to cut rates at the pace of 50 basis points at each of its two meetings in Q4. For the full year, the Bank of Canada ended up lowering its policy rate by a total of 175 basis points, from 5% to 3.25%. The market has been expecting the Bank of Canada to need to continue cutting rates due to slower economic growth in Canada, but the fear of a possible trade war with the U.S. has made the economic outlook somewhat murkier.

.png "Chart1-(1).png")

Bond Markets: During the quarter, yields on mid- to long-term bonds in Canada rose in sympathy with rising bond yields in the U.S. However, bond yields in Canada rose to a lesser extent, and yields on shorter-term bonds were actually little changed over the quarter. The FTSE Canada Universe Bond Index was basically flat during Q4 and posted a return of 4.2% for the full year. Although interest rates rose, credit spreads (i.e. the extra yield on corporate bonds versus government bonds to compensate for their extra risk) continued to grind lower, helping corporate bonds post positive overall returns in the quarter. Tightening credit spreads reflected the generally positive risk-on tone to the market, despite some volatility. Lower-rated BBB bonds generally performed better than higher-quality A-rated bonds. Credit spreads have now generally fallen back to levels similar to those experienced in 2021, when markets did quite well after the pandemic. The on-going appetite of investors for the extra yield offered by corporate bonds over government bonds is indicated not just by falling credit spreads, but also by investors’ enthusiasm to support the primary issuance market. Corporate bond supply continued to be very robust in the quarter, with $30 billion in new issuance, resulting in a record-breaking year with $141 billion of new issuance in 2024. Nonetheless, on balance, we do not think the current risk premium adequately compensates for downside risk, particularly in longer-dated corporate bonds, and have a bias towards shorter-dated credit where we view the risk / reward trade-off as being more favourable.

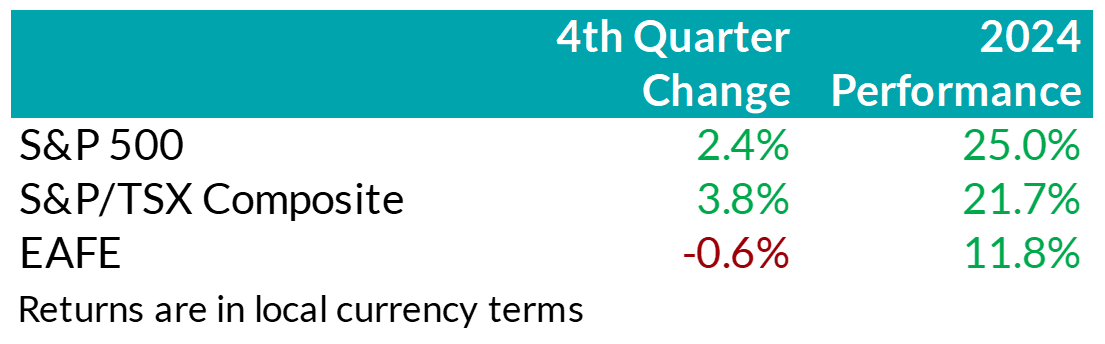

.png "Chart2-(1).png") Stock Markets – Overview: Trump’s presidential victory and the Republican party’s ‘red sweep’ in the Senate and House of Representatives sparked optimism surrounding economic growth and a new era of U.S. exceptionalism. As a result, North American equity markets extended their rally in Q4, capping off a year of robust returns. The S&P 500 returned 2.4%, bringing its year-to-date return to 25%. Within the U.S., the broadening of returns paused during the quarter as the chase for growth intensified, with mega-cap growth names like Tesla driving performance. Canadian equities surprisingly outperformed the U.S. market over the quarter, returning 3.8% in Q4, despite threats of widespread tariff negotiations looming on the horizon that could negatively impact Canadian corporate fundamentals. At a sector level, strength in the technology, financials, and energy sectors more than offset weakness in telecommunication companies as well as in the materials sector. Elsewhere, major developed markets from Europe and Asia (EAFE) underperformed last quarter as deteriorating Chinese growth prospects and weak economic growth in the Eurozone weighed on equities. Notably, foreign investors of U.S. denominated securities benefitted from a rebounding U.S. dollar with the dollar index adding over 7.6% in Q4.

Stock Markets – Overview: Trump’s presidential victory and the Republican party’s ‘red sweep’ in the Senate and House of Representatives sparked optimism surrounding economic growth and a new era of U.S. exceptionalism. As a result, North American equity markets extended their rally in Q4, capping off a year of robust returns. The S&P 500 returned 2.4%, bringing its year-to-date return to 25%. Within the U.S., the broadening of returns paused during the quarter as the chase for growth intensified, with mega-cap growth names like Tesla driving performance. Canadian equities surprisingly outperformed the U.S. market over the quarter, returning 3.8% in Q4, despite threats of widespread tariff negotiations looming on the horizon that could negatively impact Canadian corporate fundamentals. At a sector level, strength in the technology, financials, and energy sectors more than offset weakness in telecommunication companies as well as in the materials sector. Elsewhere, major developed markets from Europe and Asia (EAFE) underperformed last quarter as deteriorating Chinese growth prospects and weak economic growth in the Eurozone weighed on equities. Notably, foreign investors of U.S. denominated securities benefitted from a rebounding U.S. dollar with the dollar index adding over 7.6% in Q4.

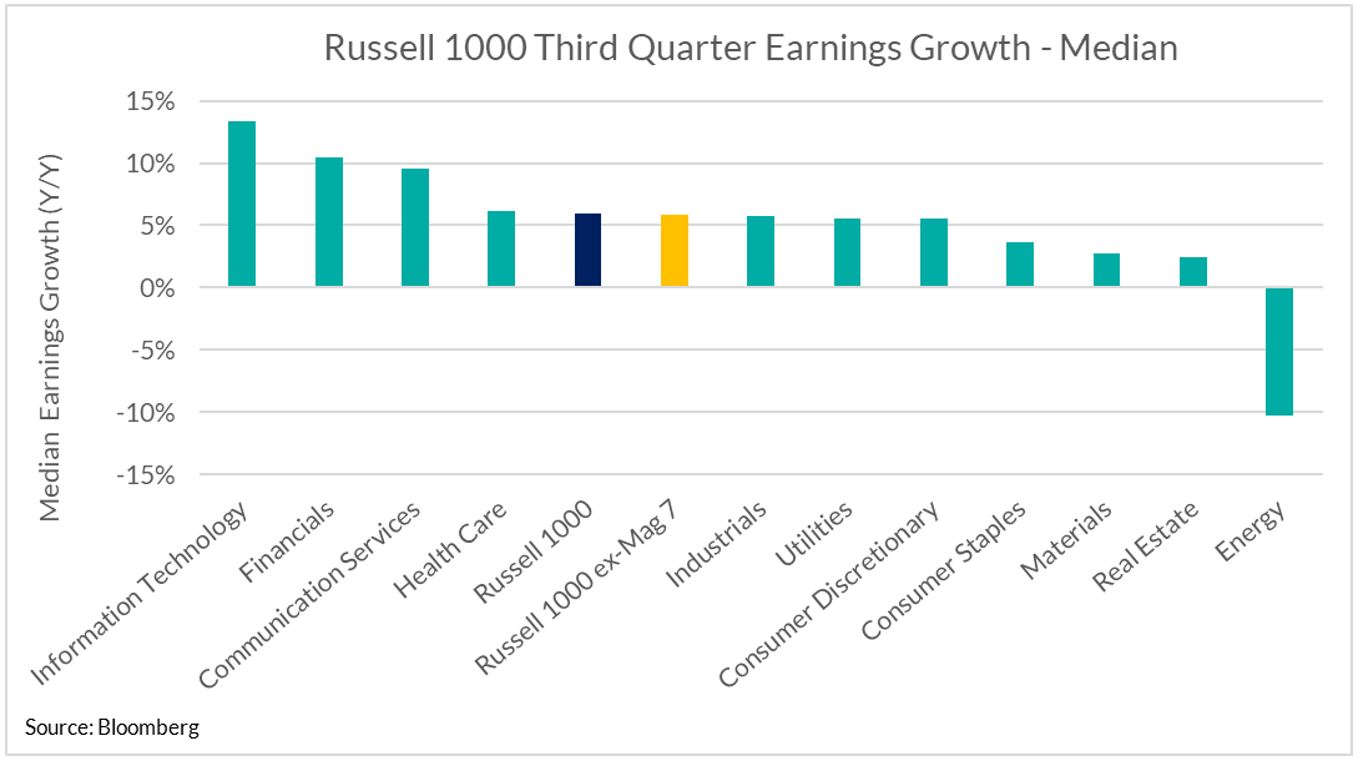

.png "Chart3-(1).png") U.S. Equities: U.S. equities remain supported by resilient margins and strong corporate earnings growth with over 70% of businesses surpassing bottom-line expectations last quarter. We remain attentive to the broadening of earnings performance and note that this trend has continued, albeit at a normalized pace versus prior quarters. More specifically, our work shows that members of the Russell 1000, excluding the Magnificent 7, posted median earnings growth of 6% last quarter, down from nearly 9% in Q3 but comparable to Q2 (6%). Looking forward to 2025, analysts continue to forecast U.S. exceptionalism, with forecasts of ~12% earnings growth.

U.S. Equities: U.S. equities remain supported by resilient margins and strong corporate earnings growth with over 70% of businesses surpassing bottom-line expectations last quarter. We remain attentive to the broadening of earnings performance and note that this trend has continued, albeit at a normalized pace versus prior quarters. More specifically, our work shows that members of the Russell 1000, excluding the Magnificent 7, posted median earnings growth of 6% last quarter, down from nearly 9% in Q3 but comparable to Q2 (6%). Looking forward to 2025, analysts continue to forecast U.S. exceptionalism, with forecasts of ~12% earnings growth.

Following Trump’s presidential victory, stocks with greater sensitivity to the U.S. economy, such as small cap businesses, benefitted from expectations of domestically focused growth initiatives. However, stubborn inflation and expectations of fewer interest rate cuts by the Federal Reserve saw the trend of broadening sources of returns pause into the end of the year. Instead, market concentration reaccelerated with investors rushing back towards mega-cap growth stocks. In fact, Tesla – which is approximately 2% of the S&P 500 Index by market cap – contributed approximately one-third of the total index return in Q4, while the Mag 7 as a group contributed over 100% of total returns. In other words, U.S. large cap companies excluding the Magnificent 7 declined in aggregate last quarter.

Canadian Equities: Against the backdrop of cooling inflation and below-trend growth, the Bank of Canada continued to loosen monetary policy. As a result, Canadian companies

showed signs of improving efficiency with return on equity – a gauge of corporate profitability – improving versus prior quarters. Under these conditions, investors remained focused on higher quality, high-dividend paying companies – particularly within the financial sector. Relative to prior quarters, this group witnessed greater contribution out of non-bank financials (such as asset managers and insurance companies), as the premium investors were willing to pay for Canadian banks remained elevated. Across other sectors, the energy sector had a positive quarter as the price of oil stabilized, but falling prices for raw industrials pushed the materials sector lower.

Bottom line: U.S. political developments and subsequent growth expectations dominated market sentiment last quarter. As a result, investors dialed back rate cut expectations and bond yields moved higher. In equity markets, the potential for an era of higher-for-longer rates prompted a resumption of investors crowding into growth stocks. Going forward, we remain cautious of elevated valuations and continue to prioritize diversified sources of returns with a long-term outlook. Nonetheless, despite rich valuations, our base case remains that investors’ enthusiasm for equities will persist in the near-term and stocks should continue to outperform bonds.

Downloadable Copy

ADVISOR USE ONLYMark Warywoda, CFA

VP, Public Portfolio ManagementIan Whiteside, CFA, MBA

AVP, Public Portfolio ManagementJohanna Shaw, CFA

Director, Portfolio ManagementJin Li

Director, Equity Portfolio Management

Tyler Farrow, CFA

Senior Analyst, Equity

Andrew Vermeer

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Francie Chen

Analyst, Rates

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

-

- [pdf] Investment Direction Form - DIA/GIA

- Policy Change eDelivery

- [pdf] Pivotal Select Fund Facts