Site Search

743 results for access here PROBLEMGO.com Need a bondsman who takes payment plans for release today

-

Market Commentary October 2025

Key Takeaways

• Market sentiment improved significantly in Q3 as economic uncertainties eased.

• Both U.S. and Canadian stock markets posted strong gains. The rally was supported by sector-specific earnings strength and structural growth drivers in AI and digital infrastructure. Equity valuations remain elevated, which could become a potential headwind for future performance.

• Canadian bond markets delivered positive returns in Q3. Returns were largely from underlying interest income, supported by modestly lower interest rates and continued strong performance from tighter credit spreads.

• Both the Bank of Canada and the U.S. Federal Reserve restarted easing in Q3. Each central bank cut rates by 25 basis points in September, responding to rising risks to labour markets.

Economic and Market UpdateEconomic Summary: In the U.S., economic activity has remained relatively steady through 2025. However, while business investment remained robust, the pace of hiring slowed. Inflation has increased in recent months, but overall price pressures appear contained. Trade uncertainty eased in the third quarter as the U.S. reached agreements on tariffs with several key trading partners. Countries such as Japan, South Korea, and Indonesia, as well as the European Union, negotiated compromise deals. These deals typically involved U.S. tariffs in the range of 15% to 20% in exchange for market access or investment commitments. However, other nations faced higher tariffs of 30-50% following failed negotiations. Mexico and China are currently in a 90-day pause on tariff hikes, which will expire on October 29 and November 10, respectively. At its September meeting, the U.S. Federal Reserve (the “Fed”) lowered its policy rate by 25 basis points to a range of 4.00%– 4.25%. The Fed also signaled that additional interest rate cuts will likely be required to support the economy. Chair Jerome Powell highlighted increasing risks to the labour market and decreasing risks to inflation. He emphasized that the Fed remains data dependent and that interest rate decisions will be made “meeting-by-meeting”. The October 1 shutdown of the U.S. government added further uncertainty to the economic outlook. Key data releases are expected to be delayed, and the White House has warned of mass layoffs of federal workers.

The Canadian economy experienced a modest rebound in July following weak growth in the second quarter. However, U.S. tariffs and ongoing trade policy uncertainty continue to present risks to the economy. The labour market continues to weaken while inflationary pressures have eased in recent months. On July 31, the U.S. increased tariffs on Canadian imports from 25% to 35% for those products not exempted under USMCA. In addition, the U.S. has expanded its list of sector-specific tariffs. This is expected to place further strain on Canadian exporters. In response to these developments, the Bank of Canada cut its policy rate by 25 basis points to 2.50% during its September meeting. Governor Tiff Macklem indicated that the Bank is prepared to take further action if the balance of risks shifts to weaker growth.

Bond Markets: During Q3, the FTSE Canada Universe Bond Index returned 1.5%. Yields on Canadian bonds with maturities of 10 years or less declined. That reflected increased expectations for interest rate cuts by the Bank of Canada. Yields on bonds with maturities of greater than 10 years increased moderately, as investors continued to demand a higher risk premium for long-term debt.

Overall, corporate bonds saw a positive return for the quarter and outperformed government bonds. This outperformance was due to the higher interest rate on corporate bonds relative to government bonds, with an assist from modestly tighter credit spreads. Corporate issuance was robust during the quarter with strong investor demand, as investors were willing to look past U.S. tariffs and their potential impact to global growth. There were 99 corporate bond issuances during Q3 that combined to raise $45 billion for issuers, a new record. Indeed, the new issuance market is tracking ahead of last year, the previous high-water mark for issuance.

Notwithstanding the continued strong performance from corporate bonds, we have maintained a bias towards shorter corporate bonds where the risk and reward are better balanced. We remain ready to invest in longer corporate bonds as valuations become attractive.

Stock Markets: Equity markets posted strong gains in Q3. The S&P 500 returned 8.1% for the quarter, led by Information Technology and Communication Services. Investors focused on the expansion of AI infrastructure and a more favourable regulatory environment for blockchain technology. These themes supported risk appetite despite valuations remaining high relative to historical averages. The Canadian market returned 12.5% in Q3, outperforming the U.S. by more than 4%. This was driven mainly by strong returns in the Materials sector. Meanwhile, the Europe, Australasia, and Far East Index (EAFE) returned 5.4%, as international investors re-evaluated the “Sell America” trade trend.

U.S. Equities: In Q3, U.S. equities rose on strong momentum in AI infrastructure investment and growing interest in blockchain innovation. Mega-cap tech stocks led the rally. Major announcements such as NVIDIA’s $100 billion investment in OpenAI and Oracle’s $300 billion multi-year cloud deal highlighted the rapid growth of hyperscale data centers and the deepening commitment to AI development. A more supportive regulatory environment for blockchain technology also boosted investor interest in digital assets. This was reflected in robust IPO activity from crypto-focused companies such as Figure Technology and Gemini. Both stocks saw sharp gains following their public market debuts. That said, the S&P 500 continues to trade at nearly 23 times its forward earnings, roughly 20% above its 10-year average.

Canadian Equities: Canadian equities rose on better-than-expected economic data and sector-driven earnings, outperforming the U.S. by more than 4% in Q3. The Materials sector drove the rally, contributing nearly half of the gain for the TSX in Q3, as the price of gold surged past US$3850/oz (+45% YTD). The Technology sector also posted solid results, highlighted by Shopify’s continued strong performance. Shopify’s AI-driven product expansion and scalable digital commerce growth pushed the stock to trade around 85 times its forward earnings over the next twelve months. Positive sentiment extended to the Financials sector, where better-than-expected provisions for credit losses helped support a revaluation of bank stocks.

Overall, Q3 marked a risk-on environment across North American equities, underpinned by sector-specific earnings strength and structural growth drivers. In the U.S., enthusiasm around AI and digital infrastructure continued to dominate. In Canada, the rally was driven by surging gold prices and better-than-expected bank earnings. These catalysts helped sustain broad-based market strength across both markets.

Bottom line: Overall market sentiment improved in the third quarter following the volatility earlier in the year caused by tariffs. Investors benefited from resilient performance in North American equities and positive performance in fixed income. In the U.S., the Federal Reserve resumed its rate-cutting cycle, while strong consumer demand and continued capex-spending acted as key drivers for the market strength. In Canada, gold prices continued to surge amid persistent safe-haven demand driven by geopolitical risks. Looking ahead, we will continue to closely monitor valuation levels and underlying economic data for signals of inflection as the cycle progresses.

Downloadable Copy

Mark Warywoda, CFA

VP, Public InvestmentsIan Whiteside, CFA, MBA

AVP, Public InvestmentsJohanna Shaw, CFA

Director, Public InvestmentsJin Li

Director, Equity Investments

Wanyi Chen, CFA, FRM

Sr. Quantitative Analyst

Andrew Vermeer, CFA

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Edward Ng Cheng Hin

Analyst, Credit

Kate (Huyen) Vinh

Analyst, Equity

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy. - [pdf] S&R Supply Order Form

-

Market Commentary January 2025

Key Takeaways

Full year 2024:

-

Despite reductions of policy-setting interest rates by central banks, yields on longer-term bonds finished the year higher than they started the year.

-

Positive risk appetite helped corporate bonds perform well, led by lower-quality issuers.

-

Global equity markets posted robust returns, with U.S. equities outperforming other developed markets, driven by heavy concentration into the ‘Magnificent 7’ stocks.

Fourth Quarter:

-

Central banks continued to ease monetary policy in Q4, with the Bank of Canada cutting its policy interest rate more aggressively than did the U.S. Federal Reserve.

-

The Republican victory across both the executive and legislative branches in the U.S. ignited expectations of economic growth, pushing bond yields and stock prices higher.

-

Risk sentiment helped corporate bonds continue to outperform government bonds.

-

Markets remained volatile: while North American stock markets continued to outperform most international indices, Canadian stocks managed to outperform U.S. stocks in Q4, as sources of returns in the U.S. narrowed into year-end.

Economic and Market Update

Economic Summary: In the U.S., economic activity continued to expand at a solid pace in Q4. The rate of inflation continued to slow but remained above the central bank’s 2% objective. The labour market in the U.S. remained resilient, as the unemployment rate has remained low compared to historical norms. A decisive victory for Donald Trump and the Republican Party further boosted expectations for continued growth. The return of the President-elect’s old tactics of threatening tariffs to influence trade, security, and drug control re-introduced some economic uncertainty, particularly regarding the potential return of inflationary pressures. Those concerns prompted the Federal Reserve to slow the pace of its policy easing, as it lowered rates by just 0.25% at each of its two meetings in Q4, following the 0.50% cut in September. Throughout 2024, the Fed reduced rates by a total of 100 basis points, from 5.50% to 4.50%. Nonetheless, bond yields were significantly higher for most maturity terms during the fourth quarter as the market priced in not just a stronger economy than had been the expectation during Q3, implying less interest rate cuts by the Fed, but also growing concerns about the government deficit.

In Canada, growth remained positive during 2024 and improved a bit to close the year, but continued to fall short of the Bank of Canada’s expectations. Similarly, inflation came in lower than expected and below the Bank’s 2% target. The labour market continued to soften for much of the year, with employment growth falling short of labour force growth. The weakness in the labour market and economy, along with tamed inflation, prompted the Central Bank to cut rates at the pace of 50 basis points at each of its two meetings in Q4. For the full year, the Bank of Canada ended up lowering its policy rate by a total of 175 basis points, from 5% to 3.25%. The market has been expecting the Bank of Canada to need to continue cutting rates due to slower economic growth in Canada, but the fear of a possible trade war with the U.S. has made the economic outlook somewhat murkier.

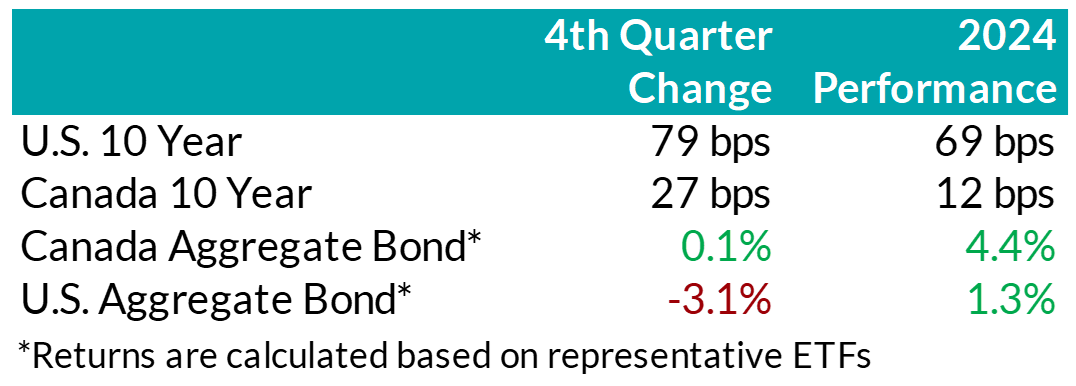

.png "Chart1-(1).png")

Bond Markets: During the quarter, yields on mid- to long-term bonds in Canada rose in sympathy with rising bond yields in the U.S. However, bond yields in Canada rose to a lesser extent, and yields on shorter-term bonds were actually little changed over the quarter. The FTSE Canada Universe Bond Index was basically flat during Q4 and posted a return of 4.2% for the full year. Although interest rates rose, credit spreads (i.e. the extra yield on corporate bonds versus government bonds to compensate for their extra risk) continued to grind lower, helping corporate bonds post positive overall returns in the quarter. Tightening credit spreads reflected the generally positive risk-on tone to the market, despite some volatility. Lower-rated BBB bonds generally performed better than higher-quality A-rated bonds. Credit spreads have now generally fallen back to levels similar to those experienced in 2021, when markets did quite well after the pandemic. The on-going appetite of investors for the extra yield offered by corporate bonds over government bonds is indicated not just by falling credit spreads, but also by investors’ enthusiasm to support the primary issuance market. Corporate bond supply continued to be very robust in the quarter, with $30 billion in new issuance, resulting in a record-breaking year with $141 billion of new issuance in 2024. Nonetheless, on balance, we do not think the current risk premium adequately compensates for downside risk, particularly in longer-dated corporate bonds, and have a bias towards shorter-dated credit where we view the risk / reward trade-off as being more favourable.

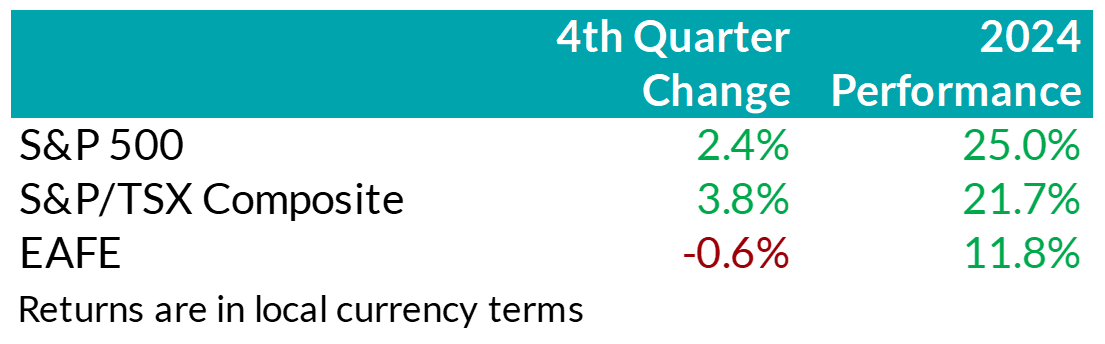

.png "Chart2-(1).png") Stock Markets – Overview: Trump’s presidential victory and the Republican party’s ‘red sweep’ in the Senate and House of Representatives sparked optimism surrounding economic growth and a new era of U.S. exceptionalism. As a result, North American equity markets extended their rally in Q4, capping off a year of robust returns. The S&P 500 returned 2.4%, bringing its year-to-date return to 25%. Within the U.S., the broadening of returns paused during the quarter as the chase for growth intensified, with mega-cap growth names like Tesla driving performance. Canadian equities surprisingly outperformed the U.S. market over the quarter, returning 3.8% in Q4, despite threats of widespread tariff negotiations looming on the horizon that could negatively impact Canadian corporate fundamentals. At a sector level, strength in the technology, financials, and energy sectors more than offset weakness in telecommunication companies as well as in the materials sector. Elsewhere, major developed markets from Europe and Asia (EAFE) underperformed last quarter as deteriorating Chinese growth prospects and weak economic growth in the Eurozone weighed on equities. Notably, foreign investors of U.S. denominated securities benefitted from a rebounding U.S. dollar with the dollar index adding over 7.6% in Q4.

Stock Markets – Overview: Trump’s presidential victory and the Republican party’s ‘red sweep’ in the Senate and House of Representatives sparked optimism surrounding economic growth and a new era of U.S. exceptionalism. As a result, North American equity markets extended their rally in Q4, capping off a year of robust returns. The S&P 500 returned 2.4%, bringing its year-to-date return to 25%. Within the U.S., the broadening of returns paused during the quarter as the chase for growth intensified, with mega-cap growth names like Tesla driving performance. Canadian equities surprisingly outperformed the U.S. market over the quarter, returning 3.8% in Q4, despite threats of widespread tariff negotiations looming on the horizon that could negatively impact Canadian corporate fundamentals. At a sector level, strength in the technology, financials, and energy sectors more than offset weakness in telecommunication companies as well as in the materials sector. Elsewhere, major developed markets from Europe and Asia (EAFE) underperformed last quarter as deteriorating Chinese growth prospects and weak economic growth in the Eurozone weighed on equities. Notably, foreign investors of U.S. denominated securities benefitted from a rebounding U.S. dollar with the dollar index adding over 7.6% in Q4.

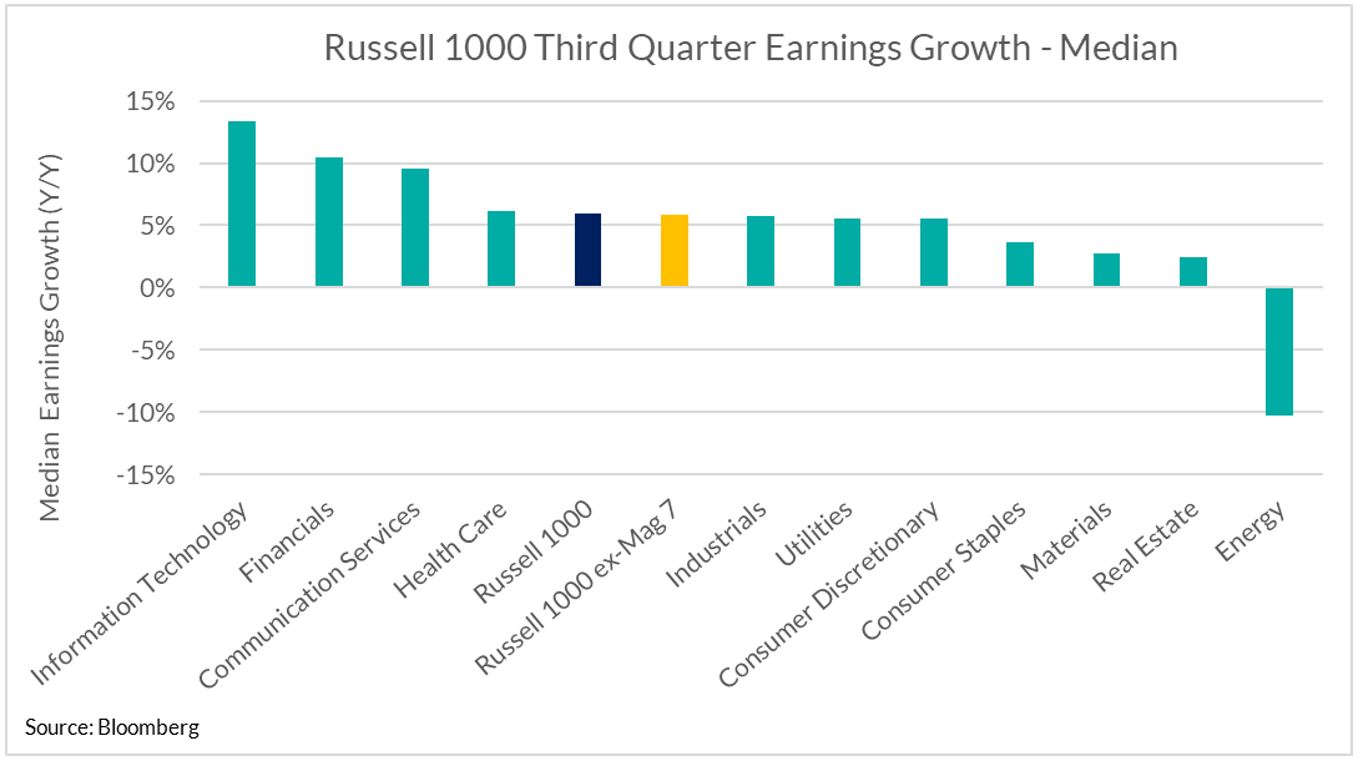

.png "Chart3-(1).png") U.S. Equities: U.S. equities remain supported by resilient margins and strong corporate earnings growth with over 70% of businesses surpassing bottom-line expectations last quarter. We remain attentive to the broadening of earnings performance and note that this trend has continued, albeit at a normalized pace versus prior quarters. More specifically, our work shows that members of the Russell 1000, excluding the Magnificent 7, posted median earnings growth of 6% last quarter, down from nearly 9% in Q3 but comparable to Q2 (6%). Looking forward to 2025, analysts continue to forecast U.S. exceptionalism, with forecasts of ~12% earnings growth.

U.S. Equities: U.S. equities remain supported by resilient margins and strong corporate earnings growth with over 70% of businesses surpassing bottom-line expectations last quarter. We remain attentive to the broadening of earnings performance and note that this trend has continued, albeit at a normalized pace versus prior quarters. More specifically, our work shows that members of the Russell 1000, excluding the Magnificent 7, posted median earnings growth of 6% last quarter, down from nearly 9% in Q3 but comparable to Q2 (6%). Looking forward to 2025, analysts continue to forecast U.S. exceptionalism, with forecasts of ~12% earnings growth.

Following Trump’s presidential victory, stocks with greater sensitivity to the U.S. economy, such as small cap businesses, benefitted from expectations of domestically focused growth initiatives. However, stubborn inflation and expectations of fewer interest rate cuts by the Federal Reserve saw the trend of broadening sources of returns pause into the end of the year. Instead, market concentration reaccelerated with investors rushing back towards mega-cap growth stocks. In fact, Tesla – which is approximately 2% of the S&P 500 Index by market cap – contributed approximately one-third of the total index return in Q4, while the Mag 7 as a group contributed over 100% of total returns. In other words, U.S. large cap companies excluding the Magnificent 7 declined in aggregate last quarter.

Canadian Equities: Against the backdrop of cooling inflation and below-trend growth, the Bank of Canada continued to loosen monetary policy. As a result, Canadian companies

showed signs of improving efficiency with return on equity – a gauge of corporate profitability – improving versus prior quarters. Under these conditions, investors remained focused on higher quality, high-dividend paying companies – particularly within the financial sector. Relative to prior quarters, this group witnessed greater contribution out of non-bank financials (such as asset managers and insurance companies), as the premium investors were willing to pay for Canadian banks remained elevated. Across other sectors, the energy sector had a positive quarter as the price of oil stabilized, but falling prices for raw industrials pushed the materials sector lower.

Bottom line: U.S. political developments and subsequent growth expectations dominated market sentiment last quarter. As a result, investors dialed back rate cut expectations and bond yields moved higher. In equity markets, the potential for an era of higher-for-longer rates prompted a resumption of investors crowding into growth stocks. Going forward, we remain cautious of elevated valuations and continue to prioritize diversified sources of returns with a long-term outlook. Nonetheless, despite rich valuations, our base case remains that investors’ enthusiasm for equities will persist in the near-term and stocks should continue to outperform bonds.

Downloadable Copy

ADVISOR USE ONLYMark Warywoda, CFA

VP, Public Portfolio ManagementIan Whiteside, CFA, MBA

AVP, Public Portfolio ManagementJohanna Shaw, CFA

Director, Portfolio ManagementJin Li

Director, Equity Portfolio Management

Tyler Farrow, CFA

Senior Analyst, Equity

Andrew Vermeer

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Francie Chen

Analyst, Rates

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

-

- [pdf] A Unique Approach to Managing Disability

- [pdf] Segregated Fund Annual Report - December 31, 2025

- [pdf] myFlex - How it works, what to consider

- [pdf] B2B Investment Loan Application Process

- [pdf] Guide to MGA contracting

- [pdf] B2B Loan Application Tips

- [pdf] FundSERV - Schedule "B" Commission Schedule