Site Search

323 results for fc coins cheap ps4 Besuche die Website Buyfc26coins.com. Top Service, gerne wieder..gzeO

- [pdf] Segregated Fund Annual Report - December 31, 2025

-

Equitable Life Group Benefits Bulletin – May 2021

In this issue:

- Graduating dependents losing coverage?*

- New Brunswick expands the use of biosimilars*

- Proposed changes to federal recovery and EI benefits*

- Removal of plan administrator access to update plan member banking*

- BioScript recognized as one of Canada’s Best Managed Companies*

Graduating dependents losing coverage?

Let plan members know about Coverage2go

As we reach the end of spring, some of your clients’ plan members may have dependents who are graduating from university or college and will no longer be eligible for coverage under the benefits plan.

Fortunately, we offer Coverage2go®. It allows individuals who are losing their group coverage to purchase personal month-to-month health and dental coverage that is affordable, reliable and works like their previous group benefits plan. They can choose the level of coverage and protection that suits their personal situation.

There are no medical questions – they simply need to apply within 60 days of losing their health coverage under their group benefits plan.*

Help your plan members and their dependents who are losing coverage by letting them know about Coverage2go. They can visit our website to learn more about Coverage2go and to get a quote.

*Quebec residents are not eligible for Coverage2goNew Brunswick expands the use of biosimilars

The New Brunswick government recently announced that it will be implementing a biosimilar transition program.

Patients using originator biologic drugs for diseases such as inflammatory arthritis, inflammatory bowel disease, diabetes and psoriasis, will have until November 30, 2021 to switch to the biosimilar version of their medications in order to maintain coverage under the province’s public drug plans. This process will be completed in consultation with the patients’ physicians.

Biosimilars are highly similar to the drugs they are based on and Health Canada considers them to be equally safe and effective for approved conditions.

Equitable Life® actively monitors and investigates all biosimilar policy changes and the ongoing evolution of biosimilar drugs entering Canada. We will keep you informed of any impact on private drug plans and how we are responding.Proposed changes to federal recovery and EI benefits

In its recent 2021 budget, the federal government proposed a variety of changes to its benefit programs.

The proposed changes include providing up to 12 additional weeks of the Canada Recovery Benefit to a maximum of 50 weeks. The first 12 weeks of this benefit would be paid at $500 per week and the remaining eight weeks at $300 per week.

Multiple changes have also been proposed to make Employment Insurance (EI) more accessible to Canadians. The changes include: maintaining uniform access to EI benefits across all regions, supporting multiple job holders and those who switch jobs by ensuring that all insurable hours and employment count towards their eligibility, and simplifying many rules around EI to ensure Canadians can receive benefits sooner. It has also been proposed that the regular EI benefits be extended to no later than November 20, 2021, if needed.

We are analyzing the impact these changes may have to disability benefits. We will provide more details later in the year.Removal of plan administrator access to update plan member banking

In early June, plan administrators will no longer be able to update banking information for their plan members on EquitableHealth.ca after their initial enrolment. This change has been made to allow plan members to have full control over where they want their claim payments deposited.

Plan members can update their banking information online through their plan member web portal or through the EZClaim mobile app. They will continue to be notified via email if and when they make any changes.BioScript Solutions recognized as one of Canada’s Best Managed Companies

Congratulations to our partner, BioScript Solutions, for being recognized as one of Canada’s Best Managed Companies of 2021 by Deloitte.

We have partnered with BioScript since 2016 for our Specialty Drug Preferred Pharmacy Network (PPN). This partnership offers cost savings while providing comprehensive, best-in-class patient care.

BioScript is one of Canada’s leading specialty pharmacies and recently celebrated its 20th anniversary.

-

Special 5% rate for clients until Pivotal Select FHSA is available

Great news for clients saving for their first home! For a limited time, clients who intend on setting up a First Home Savings Account (FHSA) with Equitable Life® can deposit money to a Guaranteed Interest Account (GIA) now and enjoy a special rate of 5.00%.1

The special rate applies only if the client transfers the funds to an FHSA by December 28, 2023; otherwise, the standard Daily Interest Account (DIA) rate will be applied to those funds.

Here’s how to take advantage of this special rate:

For New Clients:- Complete an application for a non-registered GIA. On the application select “Daily Interest Account” as the investment instructions and write the amount to be deposited (minimum $500, maximum $8,000).

- In the Special Instructions section of the application, write “FHSA”.

- The GIA application form (799) can be found here

For Existing Clients - must have a GIA (Compound Interest Only) policy:- Submit a letter of direction or complete the Investment Direction form requesting to deposit funds to the DIA for the FHSA promotion (minimum $500, maximum $8,000)

- Complete sections 1, 3, 4, 12 and 13 of the Investment Direction form, and in the Special Instructions area, write “FHSA”.

- The Investment Direction form (693ANN) can be found here

The GDA will be a non-registered account and any interest earned will be taxable.

Once the Equitable Life FHSA is available:- Submit a Pivotal Select™ FHSA application, and request to transfer the funds from the GDA to the Pivotal Select policy.2 No Market Value Adjustment fees will be charged.

- In the Special Instructions section, indicate the source of funds to be “FHSA promotion funds” and provide instructions on where to direct any excess funds in the GIA if applicable.

- The funds will be transferred to the FHSA.3

- Any excess funds over $8,000 will be returned to the client as a direct deposit, a cheque, or the client can keep the GIA open.

This is a great opportunity for clients to start saving for their first home today while earning an excellent rate. The advisor receives a reduced upfront commission4 for the pre-FHSA deposit to the GDA, in addition to the commission that will be earned by moving the funds to the Pivotal Select FHSA.

This special savings rate promotion is available until the launch date of Equitable Life’s FHSA unless the promotion is ended on an earlier date at Equitable Life’s discretion. The maximum amount on which a client can receive the special savings rate is $8,000.

Clients who do not transfer funds to the FHSA on or before December 28, 2023 will not receive the promotional rate. We will transfer the funds from the special GDA to the DIA account effective as of the date of deposit. As a result, the interest received by the client from the date of deposit to December 28, 2023 will be the DIA rate rather than the promotional rate.

Questions? Please see our FAQ

For more information, please contact your Regional Investment Sales Manager. Additional details about the FHSA can be found on the Government of Canada’s website.

® denotes a trademark of The Equitable Life Insurance Company of Canada.

1 The pre-FHSA special saving rate of 5.00% per year compounds daily and takes effect from the date Equitable Life receives the deposit and will end on the date the FHSA Pivotal Select segregated fund product is launched later this year (December 28, 2023 at the latest). In the unlikely event Equitable Life’s Pivotal Select FHSA is unavailable in 2023, the funds subject to the promotion will earn the 5.00% rate for 1 year from the date of deposit through maturity in 2024.

2 The FHSA promotion will only be available as a Pivotal Select Segregated Fund policy. Clients can open a FHSA only if they meet the eligibility criteria when they sign the application.

3The funds in the Guaranteed Interest Account will be transferred to the FHSA in the form of a contribution of up to $8,000 on or after the date the client signs the FHSA application form. Clients must open a FHSA to receive the special bonus interest.

4 Commission of 0.20% paid upfront for money received and deposited to the policy by September 29, 2023. 0.05% paid upfront for money received and deposited after September 29, 2023, and the earlier of the promotion termination or December 28, 2023. Commissions are paid through an adjustment to our current 40bps commission on our one-year GDA by way of a chargeback reducing the commission to the rate stated in this note.

Posted June 1, 2023 - [pdf] Why do business with Equitable

-

Enhancing the Transfer Process: Equitable's New Signature Guarantee Service

Equitable® is making transfers even easier with EZcomplete®.

This enhancement will help advisors and clients by reducing the number of rejections from other institutions that need a signature guarantee. Reducing transfer rejections means less time and effort for advisors, and faster transfers from other institutions.

Signature Guarantees

Equitable will now offer signature guarantees on most transfers requested through EZcomplete.

When is a signature guarantee not available?

• For entity owned accounts

• If a Power of Attorney is signing on behalf of an owner

• If the transferring account has an irrevocable beneficiary

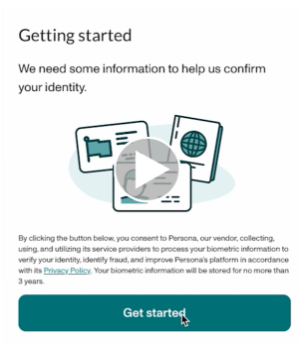

Watch the quick Identity Check with Persona video or read through instructions below.

To offer a signature guarantee, Equitable first needs to check the identity of all owners using Persona, a third-party service provider.

The advisor starts by selecting a signature guarantee in EZcomplete. An email link is sent to all proposed owners.

Clients can click the link within the email to Persona's verification process.

They will be prompted to take a picture of their photo ID and a selfie, turning their head slightly left and right by following the prompts.

Their identity can then be confirmed in seconds.

Sending Transfer Forms:

• If all owners' identities are verified, Equitable will send the transfer form with a signature guarantee stamp and the e-signature audit log to the transferring institution.

• If ID verification fails, clients will be prompted to try up to three times. If still unsuccessful, the transfer form and e-signature audit log is sent to the transferring institution without the signature guarantee stamp.

Handling Issues:

• Advisors’ obligations to verify ID is not affected by this process; ID verification is still required.

• If the client times out or loses the email to access Persona, the advisor can resend the link.

• If the client’s name or email changes after ID verification, the advisor will need to redo the ID verification with the updated information to get a signature guarantee.

This update strives to make processes smoother and more efficient for everyone. Just another reason to do business with Equitable. When we work together, success is mutual.

For more information or assistance, please contact your Director, Investment Sales.

Date published: May 7, 2025 -

October 2019 Advisor eNews

Coverage of Remicade, Enbrel and Lantus in BC

As we announced in August, BC PharmaCare recently introduced a new Biosimilars Initiative that ends coverage of three biologic drugs, including Remicade, Enbrel, and Lantus. These drugs will no longer be eligible in British Columbia for most conditions for which lower-cost biosimilar versions are available. Patients in the province with these conditions will be required to switch to biosimilar versions of these drugs by Nov. 25, 2019 in order to maintain their coverage under BC PharmaCare. Patients taking Remicade for Crohn's Disease or Ulcerative Colitis will not be required to switch to a biosimilar until March 6, 2020.

Biologics are drugs that are engineered using living organisms, such as yeast and bacteria. Biosimilars are highly similar to the originator drugs they are based on and most have been shown to have no clinically meaningful differences in safety or efficacy.

To ensure this provincial change doesn’t result in your clients’ plans paying additional drug costs, we have aligned our drug eligibility for these three biologic drugs with that of BC PharmaCare.

As previously announced, effective Nov. 25, 2019, Remicade and Enbrel will no longer be eligible for BC plan members with conditions for which lower-cost biosimilar versions of the drugs are available. These plan members will be required to switch to the biosimilar versions of these drugs in order to maintain eligibility on the Equitable Life drug plan. We have communicated with Plan Administrators about this change, and we have informed affected claimants of the need to switch medications.

As well, effective Feb. 3, 2020, the drug ingredient cost for Lantus will no longer be eligible for BC plan members; only the dispensing fee may be eligible under their Equitable Life plan. Plan members taking Lantus will be required to switch to Basaglar, the lower-cost biosimilar version of the drug, in order to maintain coverage under their Equitable Life plan. We will be communicating with Lantus claimants in the coming weeks to allow them ample time to change their prescription and avoid any interruptions in their treatment or their coverage.

If you have any questions about this change, please contact your Group Account Executive or myFlex Sales Manager.De-listed service providers

As part of our ongoing initiative to have Group Benefits plans only reimburse eligible claims, we conduct reviews of the billing and administrative practices of service providers, including clinics, facilities and medical suppliers.As a result of these reviews we may de-list certain providers. We will no longer accept, or process claims for services and/or supplies obtained from those providers. The plan member can still choose to obtain services or supplies from these providers, but Equitable Life will not provide reimbursement for the claims.

Review Equitable Life’s de-listed service providers

The delisted service provider list is also posted on EquitableHealth.ca for plan members to review to determine if their claim(s) are eligible for reimbursement under their Group Benefits plan.

For more information about protecting group benefits plans from abuse, check out our articles.

-

New Online Policy Loan Form

Advisors will now have access to a new digital policy loan form on EquiNet™.

On eligible policies, you can launch a customized policy loan form through the Values tab in Policy Inquiry. (login required)

This form is quick and intuitive. You tell us the loan amount, how your client wants to receive the funds, then confirm your client’s contact info and submit! Once your client signs, it is sent for review and processing within our current service standards.

This is the first form to be digitalized and we plan to continue this work with more forms later this year.

® and ™ denotes trademarks of The Equitable Life Insurance Company of Canada. -

Delivery Update of Pivotal Select segregated fund client statements

We understand the importance of timely delivery of our Pivotal Select™ segregated fund client statements. We have resolved the issue with delivery of these statements. I can confirm that our Pivotal Select segregated fund client statements will be delivered on February 17, 2025.

We regret the impact this delay may have had on you and clients. Rest assured, we are committed to delivering the highest standard of service and will continue to work hard to earn your business and that of clients. If you have questions or need further assistance, reach out to our Client Care Team at 1.866.884.7427.

Best Regards,

.png "signature-(1).png")

Cam Crosbie,Executive Vice-President, Savings and Retirement Division

Equitable

Posted: February 12 2025 - [pdf] Facts & Figures

- [pdf] CLHIA MGA Compliance Survey