Site Search

663 results for PROBLEMGO.COM husband locked up need him out fast cash Macau

-

Coming March 23, 2020 – Equimax enhancements include 60 months of flexibility to make extra deposits

The following features will be available on Equimax Estate Builder® and Equimax Wealth Accumulator® plans!

.jpg?width=120&height=141 "Image-1-EDO-Prelaunch-Whatsnew-(1).jpg") 60 months of Excelerator Deposit Option (EDO) flexibility

60 months of Excelerator Deposit Option (EDO) flexibility- Up to 60 months to make initial EDO payment or resume stopped or reduced payments. No additional underwriting required.

- For approved EDO amounts exceeding $150,000 annually ($12,500 monthly), clients have up to 12 months from the date the EDO application was signed or the date of the last EDO payment to make an EDO payment before a contribution cap may apply.

- Available on all policies with an effective date of March 23, 2020 or later.

EDO available on case ratings of 300% or less- If a policy already in effect has a rating over 200% and up to and including 300%, the owner can apply to add EDO provided the policy was issued under the 2017 tax rules.

- Additional underwriting and submission of satisfactory evidence may be required.

Disability Benefit Disbursement at no extra cost

Disability Benefit Disbursement at no extra cost

- If a life insured becomes disabled from a severe mental or physical impairment as defined in the policy contract, the owner may apply for a tax-free,* lump sum payment of up to 100% of the policy’s cash value.

- Exclusions apply. See sample policy contract for full details, including the qualifications for the disbursement.

- Available on all policy issued under the 2017 tax rules.

* Tax laws are subject to change. The payment of the disability benefit disbursement may affect the adjusted cost basis (ACB) of the policy as it is considered payment of a capital benefit. Changes in ACB can affect the future taxation of the policy.Processing your Application

To make the transition as smooth as possible, please take a moment to review the following transition rules.

- About

-

Equitable Life Group Benefits Bulletin – September 2021

In this issue:

- Right drug, right dose*

- Responding to New Brunswick’s Biosimilar Initiative*

- Helping plan members access our convenient digital options*

- Reminder: Please access forms on EquitableHealth.ca*

- Over-age dependents losing coverage?*

Right drug, right dose

Equitable Life partners with Personalized Prescribing Inc. to help plan members avoid treatment trial and error

Patients suffering from mental health conditions often need to try several medications before they find one that works for them. This is frustrating and can result in negative side-effects, a longer recovery, lost productivity, or a delayed return to work.

To help plan members avoid this treatment trial and error, we have partnered with Personalized Prescribing Inc. to provide easier access to pharmacogenomic testing for plan members with mental health conditions.

Pharmacogenomics 101

Pharmacogenomics is the study of how an individual’s genes influence their response to medications. Pharmacogenomic testing can help determine how compatible a patient’s body may be to a particular drug, and helps their physician prescribe the most appropriate medication. The goal is to ensure the right drug is prescribed to deliver the most positive outcome with the fewest side effects.

Easier access to pharmacogenomic testing

Through our partnership with Personalized Prescribing Inc., any Equitable Life plan member diagnosed with a mental health condition can purchase a pharmacogenomic test for a discounted price of $399 plus HST – a 20% savings.

We are also introducing the option for plan sponsors to add coverage of pharmacogenomic tests provided by Personalized Prescribing Inc. for mental health conditions.

With this coverage, plan members are eligible for pharmacogenomic testing if:- They have been diagnosed with a mental health condition;

- They are currently taking or have stopped taking a medication for a mental health condition that does not work or has side effects; and

- The pharmacogenomic test is conducted by Personalized Prescribing Inc.

Getting a test is easy. The plan member starts by visiting www.personalizedprescribing.com/equitablelife to request a test kit.

Once they receive their test kit from Personalized Prescribing Inc., they simply provide a saliva sample and send it back (postage is pre-paid). Within 7-10 business days, they receive an Rx Report™ that they can share with their doctor. This report includes details to help their doctor prescribe the right drug and the right dose for them.

Benefits for plan members:- The plan member and their physician receive a full report that is easy to understand;

- The report identifies the most compatible medications for the plan member’s condition and the medications to avoid;

- The physician is able to prescribe the most appropriate medication with the fewest side effects; and

- The plan member avoids medication trial and error.

- Pharmacogenomic testing can be an effective prevention strategy to help employees stay healthy and potentially avoid a mental health-related work absence; and

- Employees suffering from mental health conditions may be more productive when they are on the right medication for them.

Responding to New Brunswick’s Biosimilar Initiative

We are changing coverage for some biologic drugs in New Brunswick in response to the province’s Biosimilar Initiative. These changes will help protect your clients from additional drug costs while still providing access to equally safe and effective biosimilars.

What is New Brunswick’s Biosimilar Initiative?

New Brunswick’s Biosimilar Initiative will end provincial coverage of several originator biologic drugs for some or all conditions beginning on December 1, 2021. Patients who are using these drugs for the affected conditions will be required to switch to biosimilar versions of the drugs to maintain coverage under the province’s government drug plan.

What is the impact on private drug plans?

The most significant risk to plan sponsors who maintain coverage of originator biologics is coordination of benefits (CoB) risk. If other insurance carriers follow suit with the province and delist the originator biologics, it could expose a plan that doesn’t delist them to significant coordination of benefits risk.

For example, consider a patient who is covered under two private plans – their employer plan and a spousal plan. If their employer plan was the first payer for the originator biologic but delists the drug, the spousal plan now becomes the first payor. If the spousal plan continues to cover the cost of the originator, it now pays most or all of the cost of the drug.

How is Equitable Life responding?

To protect your clients’ plans from paying additional and avoidable drug costs, we are changing coverage in New Brunswick for most biologic drugs included in the provincial initiative.

Beginning Feb. 1, 2022, plan members in New Brunswick will no longer be eligible for coverage of Humira, Lantus, Humalog and Copaxone if they have a condition for which Health Canada has approved a lower cost biosimilar version of the drug. These plan members will be required to switch to a biosimilar version of those drugs to maintain coverage under their Equitable Life plan.

How will Equitable Life communicate this change to plan members?

We will be communicating with affected claimants in early-December 2021 to allow them ample time to change their prescriptions and avoid any interruptions in their treatment or their coverage.

Can my client maintain coverage of these biologic drugs?

All groups, except myFlex clients, who wish to opt out of this change and maintain coverage of these originator biologics for New Brunswick plan members can submit a policy amendment. Amendments must be submitted no later than Nov. 30, 2021.

Advisors with myFlex Benefits clients who wish to maintain coverage of these originator biologics for New Brunswick plan members should speak to their myFlex Sales Manager to confirm their eligibility to opt out of this change.

Groups that opt out of this change are also opting out of any future changes to our New Brunswick biosimilar initiative. Their drug plans will continue to cover any additional originator biologics that we subsequently add to the program.

Will this change impact my clients’ rates?

The rate impact of this change and any cost savings associated with the change will be factored in at renewal.

If plan sponsors opt out of these changes and maintain coverage for the originator biologics, it may result in a rate increase. Any rate adjustment will be applied at renewal.

What is the difference between biologics and biosimilars?

Biologics are drugs that are engineered using living organisms like yeast and bacteria. The first version of a biologic developed is also known as the “originator” biologic. Biosimilars are also biologics. They are highly similar to the originator drug they are based on and have been shown to have no clinically meaningful differences in safety or efficacy.

Questions?

If you have any questions about this change, please contact your Group Account Executive or myFlex Sales Manager.

Helping plan members access our convenient digital options

Some of your clients’ plan members aren’t benefitting from our secure and convenient digital options to access and use their Group Benefits. They can sign up to submit claims electronically for faster claim payments, get claim payments deposited directly to their bank accounts, easily review their coverage details, quickly access their Group Benefits plan booklet, benefits card and more. We’ve made it easier than ever to sign up, with more resources all conveniently located at Equitable.ca/go/digital.

Your clients’ plan members can visit this link to view:- A brochure with all the high-level instructions they need to get started on EquitableHealth.ca and the EZClaim mobile app

- A full video guide on how to access and navigate EquitableHealth.ca

Reminder: Please access forms on EquitableHealth.ca*

We routinely update our Plan Administrator forms on EquitableHealth.ca based on their feedback and to stay compliant with legal and/or regulatory requirements. If your clients need a form, they should always pull the most recent version from EquitableHealth.ca instead of reusing forms they have saved on their computer. Using an old or outdated form may result in processing delays.

Your clients can access the Plan Administrator forms by following these steps:- Login to EquitableHealth.ca

- Select “Documents”

- Toggle between English and French forms

- Click on the document name to download a PDF copy

Over-age dependents losing coverage?*

Some of your clients’ plan members may have dependents who are reaching the maximum age for eligibility under their group benefits plan.

If they are attending school full-time or are disabled, they may be eligible for continued coverage. Plan members with over-age dependents can simply complete the Application for Coverage of Dependent Child Over Age 21 (Form #441) and submit it through our online document submission tool. They can access the tool by logging into their Group Benefits account at www.equitablehealth.ca and clicking My Resources.

If they are not attending school full-time or disabled, they will no longer be covered under the plan. However, they may be eligible for Coverage2go®. It allows individuals who are losing their group coverage to purchase personal month-to-month health and dental coverage that is affordable, reliable and works like their previous group benefits plan. They can choose the level of coverage and protection that suits their personal situation.

There are no medical questions – they simply need to apply within 60 days of losing their health coverage under their group benefits plan.*

Help your clients’ plan members and their dependents who are losing coverage by letting them know about Coverage2go. They can visit our website to learn more about Coverage2go and to get a quote.

*Quebec residents are not eligible for Coverage2go -

Equitable Life Group Benefits Bulletin – November 2020

In this issue:

- Telemedicine now included in Travel Assist*

- Take advantage of our convenient digital options*

- 2021 changes to Maximum Insurable Earnings, Maximum Weekly Insurable Earnings and Short Term Disability Benefit*

*Indicates content that will be shared with your clients

Telemedicine now included in Travel Assist*

Medical emergencies can be particularly stressful while travelling. Making your way to a medical facility can be a struggle. And once you get there, you could face long wait times, language barriers or even the risk of COVID-19 infection.

That’s why Allianz Global Assistance®, our Travel Assist provider, is adding two new virtual care options to provide plan members with timely and appropriate medical support.

As always, when a travel medical emergency strikes, plan members call Allianz for assistance. During the intake process plan members will be guided through a series of questions to triage their unique medical situation. Options for care now include two different virtual care services:

- TeleConsultation – Video and chat consultation with a locally licensed physician. This physician can diagnose simple medical conditions and provide a prescription. Available across Canada and in some high travel states in the United States.

- TeleAdvice – Video and chat consultation for situations which are not likely to require a prescription. The physician can diagnose simple medical conditions and provide medical guidance.

Plan members who use virtual care may benefit from:

- Reduced wait times;

- Care from the comfort of their current location;

- Reduced language barriers;

- No need to arrange transportation to a medical facility;

- Reduced impact on travel itinerary; and

- Reduced risk of exposure.

Both TeleConsultation and TeleAdvice will be available for all Equitable Life plan members beginning January 1st, 2021. There is no additional cost, no changes required to your client’s plans, and no change to the way plan members contact Allianz in the event of a travel medical emergency.

This PDF plan member update will also be included in the eNews to plan administrators.

If you have any questions about these new features, please contact your Equitable Life Group Account Executive or myFlex Sales Manager.

Allianz Global Assistance is a registered business name of AZGA Service Canada Inc. and AZGA Insurance Agency Canada Ltd.

Help your clients take advantage of our convenient digital options*

During this time of physical distancing, people are looking for ways to interact with their providers virtually. We recently enhanced our Online Plan Member Enrolment tool, allowing all groups to add new plan members without the need for paper forms.

Did you know, we have several other digital options available to make it easier for your clients to do business with us and for their plan members to access and use their benefits plan? Over 71% of plan administrators are managing their plan online and 78% of plan members are already using our digital tools.

For plan administrators:

- Plan Administrator Portal (EquitableHealth.ca) – plan administrators can easily manage their plan anytime and anywhere

- Digital Welcome Kits – personalized welcome kits are delivered to plan members via email

- Easy automated payments – plan administrators can avoid missed payments by setting up pre-authorized debit or electronic funds transfer

For plan members:

- Plan Member Portal (EquitableHealth.ca) – plan members get secure, 24/7 access to their claims history, coverage details and health and wellness resources

- Electronic Claim Payments and Notifications – plan members can get claim updates sooner in their email inbox and payments right into their bank account

- EZClaim Mobile App – submitting claims from a mobile device is fast, easy and secure

- Digital Benefits Cards – plan members no longer have to dig through their wallet – they can download their benefits card on their mobile device

Learn more about how we’re making it easier for your clients to do business with us

2021 changes to Maximum Insurable Earnings, Maximum Weekly Insurable Earnings and Short Term Disability Benefit*

The Canada Employment Insurance Commission and Canada Revenue Agency have announced the 2021 changes to Maximum Insurable Earnings, and premiums for employment insurance. These changes take effect January 1st, 2021.

Maximum Insurable Earnings (MIE)

The MIE will increase from $54,200 to $56,300.

Maximum Weekly Insurable Earnings (MWIE)

The MWIE will increase from $1,042 to $1,083.

EI Benefit (55% of the MWIE, rounded to the nearest dollar)

EI benefit will increase from $573 to $595

Information for Plan sponsors

If your client’s Group Policy with Equitable Life includes a Short Term Disability (STD) benefit which is tied to the EI MWIE, and at least one classification of employees has less than a $595 maximum:

- To comply with the provisions of their policy, their STD benefit will be revised with the maximums updated based on the percentage of EI MEIW shown in their policy.

- The additional premium for any increase from their previous STD amounts and new STD amounts will be show on their January 2021 Group Insurance Billing (as applicable).

If their STD maximum is currently higher than $595 or based on a flat amount (not based on a percentage or regular earnings):

- No change will be made to their plan unless otherwise directed.

If your clients wish to provide direction regarding revising their STD maximum, or have questions about the process, they can email Kari Gough, Manager, Group Quotes and Issue.

*Indicates content that will be shared with your clients

- Give the Gift of a Head Start

- [pdf] Shareholder Borrowing Checklist

-

Introducing Equitable EZBenefits: A better group benefits solution for your small business clients

If you serve small business owners, chances are they’re looking for a group benefits solution that’s affordable, sustainable and easy to manage. That’s why we introduced Equitable EZBenefits™. It’s a unique group benefits solution designed with you and your small business clients in mind.

Options to fit every need

Available to organizations with between 2 and 25 employees, EZBenefits offers a range of plan design options to match different needs and budgets. * Whether your client owns start-up or a growing company, we’ve got them covered. Plan options include a mix of Life, Health and Dental coverage. ** Clients can also add Long-Term Disability (LTD) coverage or a Health Care Spending Account (HCSA).

Embedded services to support health and wellness

To provide employees with added support for both their physical and mental wellbeing, all our plan design options include:- Anytime, online access to medical professionals through our Virtual Healthcare solution from Dialogue,

- Access to professional counselors – via the telephone, the web or in-person – through our Employee and Family Assistance Program from Homewood Health®, and

- Online resources to help manage health, financial and family challenges through Homeweb, Homewood Health’s online wellness portal.

EZBenefits also comes with built-in HR support through Equitable Life’s partnership with HRdownloads® This takes the heavy lifting out of common human resource tasks with HR support tools and services, including:- HR Technology: An award-winning cloud-based human resource information system to provide help from onboarding to offboarding and everything in between.

- HR Content: Access to a library of over 3,000 HR documents, templates, compliance resources and articles, with 25 free document downloads.

- HR Training: A free Workplace Diversity and Inclusion online training course.

- HR Support: One free Live HR Advice call with a seasoned HR expert.

We know that advising small business clients can be challenging. We’ve created a streamlined benefits process that provides rapid quotes, hassle-free plan implementation, simplified renewals and that is easy to administer. That way, you can spend more time advising your clients and building your business – and less time with administrative back and forth.

Pricing stability for long-term stability

When it comes to attracting and retaining talent, we know your small business clients are competing with larger organizations that have big budgets and lots of resources. That’s why we’ve designed EZBenefits to provide long-term pricing stability for health and dental benefits.

Find out more

Watch this video to learn how EZBenefits can help you and your clients. You can also visit info.equitable.ca/ezbenefits for more details or to request a quote. If you have questions, contact your Equitable Life Group Account Executive. If you don't have an Equitable Life Group Account Executive, email us at EZBenefits@equitable.ca.

* Not available in Quebec.

** Dental coverage is not included with the Bronze plan design option. -

Explore Equitable EZBenefits™

A better group benefits solution for your small business clients

Running a small business isn't easy, especially for companies with smaller budgets and fewer resources. It can be tough to find a competitively priced benefits plan with the features that clients want. That’s why we created Equitable EZBenefits™, a benefits solution designed with the needs of small businesses in mind.

Options to fit every need

Available to organizations with between 2 and 25 employees, EZBenefits offers a range of plan design options to match different needs and budgets. * Whether your client owns start-up or a growing company, we’ve got them covered. Plan options include a mix of Life, Health and Dental coverage. ** Clients can also add Long-Term Disability (LTD) coverage or a Health Care Spending Account (HCSA).

Embedded services to support health and wellness

To provide employees with added support for both their physical and mental wellbeing, all our plan design options include:

● Anytime, online access to medical professionals through our Virtual Healthcare solution from Dialogue,

● Access to professional counselors – via the telephone, the web or in-person – through our Employee and Family Assistance Program from Homewood Health®, and

● Online resources to help manage health, financial and family challenges through Homeweb, Homewood Health’s online wellness portal.

Extra HR support for EZBenefits clients

EZBenefits also comes with built-in HR support through Equitable’s partnership with Citation Canada® (formerly HRdownloads). It takes the heavy lifting out of common human resource tasks with HR support tools and services. Features include:

● an award-winning cloud-based human resource information system (HRIS) to provide help from onboarding to offboarding and everything in between,

● access to a library of over 3,000 HR documents, templates, compliance resources and articles, with 25 free document downloads,

● a free Workplace Diversity and Inclusion online training course, and

● one free Life HR advice call with a seasoned HR expert.

A streamlined process to optimize your time

We know that advising small business clients can be challenging. We’ve created a streamlined benefits process that provides rapid quotes, hassle-free plan implementation, simplified renewals and that is easy to administer. That way, you can spend more time advising your clients and building your business – and less time with administrative back and forth.

Pricing stability for long-term stability

When it comes to attracting and retaining talent, we know your small business clients are competing with larger organizations that have big budgets and lots of resources. That’s why we’ve designed EZBenefits to provide long-term pricing stability for health and dental benefits.

Find out more

To learn more about EZBenefits, watch our video to learn more or view our brochure. You can also visit info.equitable.ca/ezbenefits for more details or to request a quote. If you have questions, contact your Equitable Life Group Account Executive. If you don't have an Equitable Life Group Account Executive, email us at EZBenefits@equitable.ca.

* Not available in Quebec.

** Dental coverage is not included with the Bronze plan design option.

-

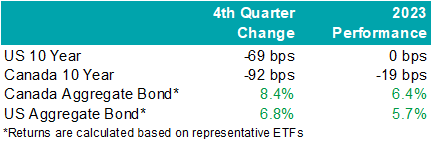

EAMG Market Commentary January 2024

Rates & Credit – Interest rates decreased sharply in Q4 as the market priced in aggressive interest rate cuts by central banks in 2024. The prospect of lower interest rates also drove a strong risk-on tone to the market, with the risk premium on corporate bonds grinding tighter as prospects for a “soft landing” improved. The rally in interest rates resulted in the best quarter for bonds over the past 15 years, with the FTSE Canada Universe Index returning 8.3%. Corporate bonds modestly underperformed the Universe Index with a return of 7.3%. The lower return for corporate bonds was primarily driven by the fact that the corporate bond index is less sensitive to interest rate movements (as compared to the government index), partially offset by the risk-on tone to the market. Within corporate bonds, lower-rated BBBs outperformed higher-rated A bonds. Industries with higher interest rate exposure such as infrastructure, energy, and communications outperformed those with less exposure (notably financials and securitization), consistent with the overall shift in the yield curve.

.png "image1-(1).png")

Santa Came to Town – Moving in sync with bonds, global equities jolted higher into the end of the year with cooling inflation data and dovish comments from central bankers. The U.S. market outperformed most regions last quarter with the S&P 500 returning 11.7% in USD terms, bringing the total return in 2023 to 26.3%. The TSX added 8.1% in Q4, boosting the total annual return to 11.8%. Meanwhile, major developed economies from Europe, Australasia, and the Far East (EAFE) gained 5.0% in local currency terms over the quarter, helping the region produce a 16.8% return from the year prior. Prospects of interest rate cuts by the Federal Reserve saw the Loonie rally into year-end and resultantly, investors of Canadian dollar securities witnessed enhanced returns. Strong domestic U.S. economic data helped value pockets of the market outperform. That said, this was not a synchronized trend as China’s economic disappointment weighed on the performance of EAFE.

U.S. Fundamentals – Our work shows that investors are shifting their focus away from operating margins and towards the ability to sustain debt levels ahead of renewing debt obligations. Corporate earnings beat modest expectations last quarter, contracting by less-than-expected on a year-over-year basis. Resilient operating margins continue to attract investors into equities. After three consecutive quarters of improving forward earnings guidance, we observed that the number of major companies expecting deteriorating financial performance grew to ~35%. We note that this is a sharp contrast relative to the optimistic run-up in equity valuations. In general, corporate pessimism has been underpinned by concerns for the health of the consumer, increasing wage pressures, and inflation.

U.S. Quant Factors – While mega-cap technology stocks gave back some ground in the second half, crowding into the magnificent 7 remains noticeable with the cap weighted S&P 500 outperforming the equal weighted index by 12.5% last year. That said, value areas of the market – which underperformed through the first three quarters of the year – were top performing companies last quarter as the prospects for an economic “soft-landing” improved with U.S. inflation continuing to ease without substantial deteriorations of employment or output data. Quality-growth businesses initially outperformed as the higher-for-longer narrative continued to drive investors toward large cash-rich companies with stable margins. That said, this basket of companies gave back relative returns into quarter-end as weakness in operating margins persisted, making fundamentals appear stretched. Low volatility stocks (i.e. stocks with lower sensitivity to broad market movement and lower price volatility) rallied to start the quarter before dovish comments from central bankers improved risk-sentiment and ultimately pushed this basket lower on a relative basis. Lastly, dividend growth companies, which include businesses with a lengthy and established history of increasing dividends, underperformed the broader index as market participants punished businesses that slowed capital growth projects during the rising interest rate environment. While operating margins have declined, the basket’s strong cash flow and low debt burden may be advantageous if the market’s anticipation of impending interest rate cuts proves to be incorrect or mistimed.

Canadian Fundamentals – Although Canadian companies exceeded bleak forecasts last quarter, earnings continue to contract on a year-over-year basis. Return on equity (ROE) – a gauge of how efficiently a corporation generates profits – continued to decline last quarter while corporate costs of capital remain elevated. In essence, Canadian companies are generating less value relative to their financing cost. Value creation underpins the sustainability of dividend payments, which are a unique and desirable attribute of the Canadian market. Meanwhile, the Bank of Canada held its overnight interest rate unchanged with market participants forecasting a higher probability of interest rate cuts in 2024. On the expectations of easing monetary conditions, dividend yields compressed while earnings forecasts improved with analysts predicting that index aggregate earnings will grow 6% to 8% in 2024. At a sector level, the energy industry’s financial performance normalized – in line with expectations – as weakening oil demand expectations overshadowed geopolitical conflict in the Middle East, ultimately pushing crude prices ~21% lower last quarter. The industrials and financials sectors beat expectations, helping offset softer-than-expected results from the consumer staples and technology sectors.

Canadian Quant Factors – The Canadian banks underperformed for most of the year as they reported increasing provisions for nonperforming loans, reflecting forecasts of worsening economic conditions. That said, expectations of interest rate cuts in 2024 helped tame recession fears and eased concerns of slowing loan growth, propelling banks higher in the fourth quarter as they appeared more stable and therefore favourable than prior estimates. The high-quality basket underperformed last quarter as improving risk sentiment in the market reduced the attractiveness of secure companies with lower earnings variability. Furthermore, high dividend payers with solid growth prospects outperformed in the fourth quarter as market participants rewarded companies that demonstrated a strong ability to support future dividends and punished high yielding businesses with less certain financial capabilities.

Views From the Frontline Rates – Interest rates declined sharply in Q4 as inflation continued to trend lower, fears of excess bond supply declined, and the Federal Open Market Committee signaled that the next change to their overnight policy interest rate would likely be lower. Labour market and consumer spending data remain resilient however businesses have indicated slowing across industries, more price-sensitive consumers, rising delinquencies, and concerns about the high cost of debt. Central banks remain committed to achieving their 2% inflation target and most acknowledge that interest rates have likely peaked.

Credit – The risk premium for corporate bonds (versus government bonds) tightened materially over the quarter, with a strong risk on tone to the market as investors priced in lower interest rates in 2024 and a “soft-landing” to economic concerns. Corporate bond supply was well received by the market. On the balance, we do not think the current risk premium adequately compensates for downside risk, and as such, we remain cautious on corporate bonds and have a bias towards higher-quality, shorter-dated credit where we view the risk / reward dynamic as being more favourable.

Equity – In the U.S., we allocated exposure to value names which outperformed over the quarter as the macroeconomic outlook improved on the backdrop of rate cut expectations. Looking forward, we expect that margins will continue to normalize as Covid-induced pent up demand fades. While we do not forecast margins to compress at an alarming rate, we believe sticky wage and input costs will continue to pressure businesses while consumers exhibit further exhaustion. As such, we are shifting our focus toward the balance between company reinvestment in capital projects and upcoming debt refinancing requirements. In line with this view, we favour businesses with stable cash flows and decreased debt loads as we believe they present an attractive contrarian opportunity if soft-landing projections prove to be overstated. Within Canada, we remain attentive to the inverse movements of ROE relative to financing costs over 2023. With the excess between ROE and financing costs compressing, businesses’ ability to create value appears more stretched than earlier in 2023. Therefore, we continue to favour high quality companies in Canada, which is typically defined by high ROE, stable earnings variability, and low financial leverage. Geographically, the U.S. economy appears to be in healthier condition with inflation easing while employment and output data remain stable and hence, our focus will be on capital expenditures. EAFE – which is generally more economically linked to China than North America – contains a large bucket of stable, high-quality businesses that may benefit from any upside economic surprises out of China. Lastly, through the lens of a Canadian investor, the Loonie’s relative value versus other major currencies presents another resource in our investment mandate to derive excess return.Downloadable Copy

Mark Warywoda, CFA

VP, Public Portfolio ManagementIan Whiteside, CFA, MBA

AVP, Public Portfolio ManagementJohanna Shaw, CFA

Director, Portfolio ManagementJin Li

Director, Equity Portfolio Management

Tyler Farrow, CFA

Senior Analyst, Equity

Andrew Vermeer

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

ADVISOR USE ONLY

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

-

The Equimax EVOLUTION Continues

Earlier this year, we announced a host of improvements to our Equimax® Participating Whole Life solution, designed to add value, flexibility, and affordability to an already excellent plan.

Today we’re pleased to announce the following additional updates took effect on August 12th, 2023:

1. Targeted improvements in rates, death benefits, and cash values for Equimax Estate Builder and Equimax Wealth Accumulator plans.

2. New joint last to die rates for the Wealth Accumulator plans to align with Estate Builder.

3. A new “rated age” calculation, and

4. New rates for determining the maximum enhancement amount with the Enhanced Protection dividend option.

Visit our splash page and watch our informative video to learn more and start selling the enhanced Equimax today.

.png "English-(1).png")

.png "French-(1).png")

.png "Chinese-(1).png")

Refer to our Transition Rules for all the details on processing your applications.

Our illustration tools are updated:

● New Web-based illustration software on secure EquiNet® (log in required)

● New Desktop illustration software

● New EZstart™ on EquiNet

Need more information?

For information on these changes, please contact your Equitable Life wholesaler.

® and TM denote trademarks of The Equitable Life Insurance Company of Canada.