Site Search

492 results for enter source MAKEMUR.COM Buying dropped charges to get someone out of jail Chiayi

-

Enhancing the Transfer Process: Equitable's New Signature Guarantee Service

Equitable® is making transfers even easier with EZcomplete®.

This enhancement will help advisors and clients by reducing the number of rejections from other institutions that need a signature guarantee. Reducing transfer rejections means less time and effort for advisors, and faster transfers from other institutions.

Signature Guarantees

Equitable will now offer signature guarantees on most transfers requested through EZcomplete.

When is a signature guarantee not available?

• For entity owned accounts

• If a Power of Attorney is signing on behalf of an owner

• If the transferring account has an irrevocable beneficiary

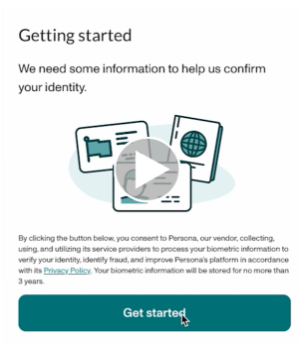

Watch the quick Identity Check with Persona video or read through instructions below.

To offer a signature guarantee, Equitable first needs to check the identity of all owners using Persona, a third-party service provider.

The advisor starts by selecting a signature guarantee in EZcomplete. An email link is sent to all proposed owners.

Clients can click the link within the email to Persona's verification process.

They will be prompted to take a picture of their photo ID and a selfie, turning their head slightly left and right by following the prompts.

Their identity can then be confirmed in seconds.

Sending Transfer Forms:

• If all owners' identities are verified, Equitable will send the transfer form with a signature guarantee stamp and the e-signature audit log to the transferring institution.

• If ID verification fails, clients will be prompted to try up to three times. If still unsuccessful, the transfer form and e-signature audit log is sent to the transferring institution without the signature guarantee stamp.

Handling Issues:

• Advisors’ obligations to verify ID is not affected by this process; ID verification is still required.

• If the client times out or loses the email to access Persona, the advisor can resend the link.

• If the client’s name or email changes after ID verification, the advisor will need to redo the ID verification with the updated information to get a signature guarantee.

This update strives to make processes smoother and more efficient for everyone. Just another reason to do business with Equitable. When we work together, success is mutual.

For more information or assistance, please contact your Director, Investment Sales.

Date published: May 7, 2025 -

Elevate your business with industry best practices and needs-based selling

Keeping your business aligned with industry best practices is vital for your success. It not only supports the fair treatment of clients – it also helps you meet certain market conduct requirements and Equitable’s expectations for needs-based selling.

The Financial Services Regulatory Authority of Ontario (FSRA) has a program that checks how well advisors follow the Insurance Act and its conduct rules. FSRA looks at how well advisors follow industry best practices and fair treatment of clients guidance (see CLHIA’s guidance document, “The Approach”). Their focus is on key areas such as giving sound advice, managing conflicts of interest, and putting clients’ needs first. FSRA selects advisors’ client files and looks for documentation that indicates needs-based selling.

In December 2024, FSRA released its latest Market Conduct Supervision Report. It highlights the need for advisors to follow certain rules and industry best practices. The report found five key areas where improvement is needed:

1. Missing notes from client meetings and calls

2. Inadequate advisor disclosure

3. Missing sales illustrations for different product options

4. Missing insurance needs analysis

5. Missing policy delivery receipts

By following industry best practices and keeping thorough records, you show your commitment to providing clients with the solutions they need. For example, taking notes during client meetings helps you track all discussions that support your recommendations. Having an insurance needs analysis shows you are providing clients with suitable advice to buy the solutions that best meet their needs.

Resources: Equitable® has resources that can help improve your business practices and help you treat clients fairly. We encourage you to check these out:

1. PPT: “Ensuring a Compliant, Needs-based Insurance Sale”. The steps to follow in needs-based selling and the records to keep.

Get CE credits! We offer the above as a self-study course that qualifies for 1 Continuing Education (CE) credit. Access it here: https://equitable-life-education.teachable.com/. (Use your contracted email to log in).

2. Client File Reference: The records to keep when selling investments, life insurance, or critical illness insurance, including key documents insurers and regulators look for during compliance audits.

3. Investor Profile Questionnaires: These will help you document your sales recommendations for:

● Universal Life (UL) sales: 1190.pdf, and

● Pivotal Select (Segregated Fund) sales: 1165.pdf

Questions? Contact your Equitable wholesaler. They are ready to support your success! -

Equitable Life Group Benefits Bulletin – September 2021

In this issue:

- Right drug, right dose*

- Responding to New Brunswick’s Biosimilar Initiative*

- Helping plan members access our convenient digital options*

- Reminder: Please access forms on EquitableHealth.ca*

- Over-age dependents losing coverage?*

Right drug, right dose

Equitable Life partners with Personalized Prescribing Inc. to help plan members avoid treatment trial and error

Patients suffering from mental health conditions often need to try several medications before they find one that works for them. This is frustrating and can result in negative side-effects, a longer recovery, lost productivity, or a delayed return to work.

To help plan members avoid this treatment trial and error, we have partnered with Personalized Prescribing Inc. to provide easier access to pharmacogenomic testing for plan members with mental health conditions.

Pharmacogenomics 101

Pharmacogenomics is the study of how an individual’s genes influence their response to medications. Pharmacogenomic testing can help determine how compatible a patient’s body may be to a particular drug, and helps their physician prescribe the most appropriate medication. The goal is to ensure the right drug is prescribed to deliver the most positive outcome with the fewest side effects.

Easier access to pharmacogenomic testing

Through our partnership with Personalized Prescribing Inc., any Equitable Life plan member diagnosed with a mental health condition can purchase a pharmacogenomic test for a discounted price of $399 plus HST – a 20% savings.

We are also introducing the option for plan sponsors to add coverage of pharmacogenomic tests provided by Personalized Prescribing Inc. for mental health conditions.

With this coverage, plan members are eligible for pharmacogenomic testing if:- They have been diagnosed with a mental health condition;

- They are currently taking or have stopped taking a medication for a mental health condition that does not work or has side effects; and

- The pharmacogenomic test is conducted by Personalized Prescribing Inc.

Getting a test is easy. The plan member starts by visiting www.personalizedprescribing.com/equitablelife to request a test kit.

Once they receive their test kit from Personalized Prescribing Inc., they simply provide a saliva sample and send it back (postage is pre-paid). Within 7-10 business days, they receive an Rx Report™ that they can share with their doctor. This report includes details to help their doctor prescribe the right drug and the right dose for them.

Benefits for plan members:- The plan member and their physician receive a full report that is easy to understand;

- The report identifies the most compatible medications for the plan member’s condition and the medications to avoid;

- The physician is able to prescribe the most appropriate medication with the fewest side effects; and

- The plan member avoids medication trial and error.

- Pharmacogenomic testing can be an effective prevention strategy to help employees stay healthy and potentially avoid a mental health-related work absence; and

- Employees suffering from mental health conditions may be more productive when they are on the right medication for them.

Responding to New Brunswick’s Biosimilar Initiative

We are changing coverage for some biologic drugs in New Brunswick in response to the province’s Biosimilar Initiative. These changes will help protect your clients from additional drug costs while still providing access to equally safe and effective biosimilars.

What is New Brunswick’s Biosimilar Initiative?

New Brunswick’s Biosimilar Initiative will end provincial coverage of several originator biologic drugs for some or all conditions beginning on December 1, 2021. Patients who are using these drugs for the affected conditions will be required to switch to biosimilar versions of the drugs to maintain coverage under the province’s government drug plan.

What is the impact on private drug plans?

The most significant risk to plan sponsors who maintain coverage of originator biologics is coordination of benefits (CoB) risk. If other insurance carriers follow suit with the province and delist the originator biologics, it could expose a plan that doesn’t delist them to significant coordination of benefits risk.

For example, consider a patient who is covered under two private plans – their employer plan and a spousal plan. If their employer plan was the first payer for the originator biologic but delists the drug, the spousal plan now becomes the first payor. If the spousal plan continues to cover the cost of the originator, it now pays most or all of the cost of the drug.

How is Equitable Life responding?

To protect your clients’ plans from paying additional and avoidable drug costs, we are changing coverage in New Brunswick for most biologic drugs included in the provincial initiative.

Beginning Feb. 1, 2022, plan members in New Brunswick will no longer be eligible for coverage of Humira, Lantus, Humalog and Copaxone if they have a condition for which Health Canada has approved a lower cost biosimilar version of the drug. These plan members will be required to switch to a biosimilar version of those drugs to maintain coverage under their Equitable Life plan.

How will Equitable Life communicate this change to plan members?

We will be communicating with affected claimants in early-December 2021 to allow them ample time to change their prescriptions and avoid any interruptions in their treatment or their coverage.

Can my client maintain coverage of these biologic drugs?

All groups, except myFlex clients, who wish to opt out of this change and maintain coverage of these originator biologics for New Brunswick plan members can submit a policy amendment. Amendments must be submitted no later than Nov. 30, 2021.

Advisors with myFlex Benefits clients who wish to maintain coverage of these originator biologics for New Brunswick plan members should speak to their myFlex Sales Manager to confirm their eligibility to opt out of this change.

Groups that opt out of this change are also opting out of any future changes to our New Brunswick biosimilar initiative. Their drug plans will continue to cover any additional originator biologics that we subsequently add to the program.

Will this change impact my clients’ rates?

The rate impact of this change and any cost savings associated with the change will be factored in at renewal.

If plan sponsors opt out of these changes and maintain coverage for the originator biologics, it may result in a rate increase. Any rate adjustment will be applied at renewal.

What is the difference between biologics and biosimilars?

Biologics are drugs that are engineered using living organisms like yeast and bacteria. The first version of a biologic developed is also known as the “originator” biologic. Biosimilars are also biologics. They are highly similar to the originator drug they are based on and have been shown to have no clinically meaningful differences in safety or efficacy.

Questions?

If you have any questions about this change, please contact your Group Account Executive or myFlex Sales Manager.

Helping plan members access our convenient digital options

Some of your clients’ plan members aren’t benefitting from our secure and convenient digital options to access and use their Group Benefits. They can sign up to submit claims electronically for faster claim payments, get claim payments deposited directly to their bank accounts, easily review their coverage details, quickly access their Group Benefits plan booklet, benefits card and more. We’ve made it easier than ever to sign up, with more resources all conveniently located at Equitable.ca/go/digital.

Your clients’ plan members can visit this link to view:- A brochure with all the high-level instructions they need to get started on EquitableHealth.ca and the EZClaim mobile app

- A full video guide on how to access and navigate EquitableHealth.ca

Reminder: Please access forms on EquitableHealth.ca*

We routinely update our Plan Administrator forms on EquitableHealth.ca based on their feedback and to stay compliant with legal and/or regulatory requirements. If your clients need a form, they should always pull the most recent version from EquitableHealth.ca instead of reusing forms they have saved on their computer. Using an old or outdated form may result in processing delays.

Your clients can access the Plan Administrator forms by following these steps:- Login to EquitableHealth.ca

- Select “Documents”

- Toggle between English and French forms

- Click on the document name to download a PDF copy

Over-age dependents losing coverage?*

Some of your clients’ plan members may have dependents who are reaching the maximum age for eligibility under their group benefits plan.

If they are attending school full-time or are disabled, they may be eligible for continued coverage. Plan members with over-age dependents can simply complete the Application for Coverage of Dependent Child Over Age 21 (Form #441) and submit it through our online document submission tool. They can access the tool by logging into their Group Benefits account at www.equitablehealth.ca and clicking My Resources.

If they are not attending school full-time or disabled, they will no longer be covered under the plan. However, they may be eligible for Coverage2go®. It allows individuals who are losing their group coverage to purchase personal month-to-month health and dental coverage that is affordable, reliable and works like their previous group benefits plan. They can choose the level of coverage and protection that suits their personal situation.

There are no medical questions – they simply need to apply within 60 days of losing their health coverage under their group benefits plan.*

Help your clients’ plan members and their dependents who are losing coverage by letting them know about Coverage2go. They can visit our website to learn more about Coverage2go and to get a quote.

*Quebec residents are not eligible for Coverage2go - [pdf] Benefits of segregated funds in a TFSA

- [pdf] Equitable Guaranteed Investment Funds – Investment Class

- [pdf] Application for Agency Contract to Sell Insurance Products - MGA, AGA and National

- Invesco

-

Equimax® Participating Whole Life – A whole life solution for everyone

Recently, we made some exciting changes for Equimax Estate Builder® and Equimax Wealth Accumulator®.

These enhancements, launched in February, make Equimax the preferred solution for clients and their families. In particular, buying a whole life solution for children gives them a head start for tomorrow. Life insurance on a child gives them:

- Permanent insurance at children’s rates

- A stable tax-advantaged investment option

- A boost in financial planning

Watch our new Equimax for Children video to learn more. View on Vimeo or YouTube.

Plus, visit our Equimax product page on EquiNet®, then click on the Marketing Materials tab for the latest Equimax marketing materials.

Need more information? Please contact your local wholesaler.

® denotes trademarks of The Equitable Life Insurance Company of Canada.

- [pdf] Path to Success Client Email Template

- [pdf] Alternative Identification Requirements