Site Search

616 results for access link MAKEMUR.COM Looking to pay a court officer to let me make an extra call

- Par Whole Life Summary

-

2023 is here and we are here for you!

Equitable Life® would like to wish everyone a Happy New Year and we are looking forward to doing more business together in 2023!

Just a reminder, we made some changes in 2022 to make doing business with Equitable Life easier. Some of the most recent enhancements include:

Opt in for text messages on new applications

● Upon submission of an application, you can opt-in to receive text message updates for your new business applications. That’s a text message when the application is received, when a decision is made, when it’s ready for delivery and when the commissions have been triggered.

Cloning pages on EZcomplete®

● You now have the ability to clone an application on EZcomplete. A whole family or a spouse can have a lot of duplicate information and the ability to clone an application can save tremendous amounts of time and make for a much more pleasant client experience.

Jump around on EZcomplete

● Jump from one part of the application to another and back again. You no longer have to complete the application one section after another in order. This will allow a lot more flexibility when submitting a policy application.

To learn more about these great enhancements contact your local wholesaler.

Continue watching for news from Equitable Life for more great launches and enhancements in 2023!

® and TM denote trademarks of The Equitable Life Insurance Company of Canada.

-

EAMG Market Commentary April 2024

April 2024

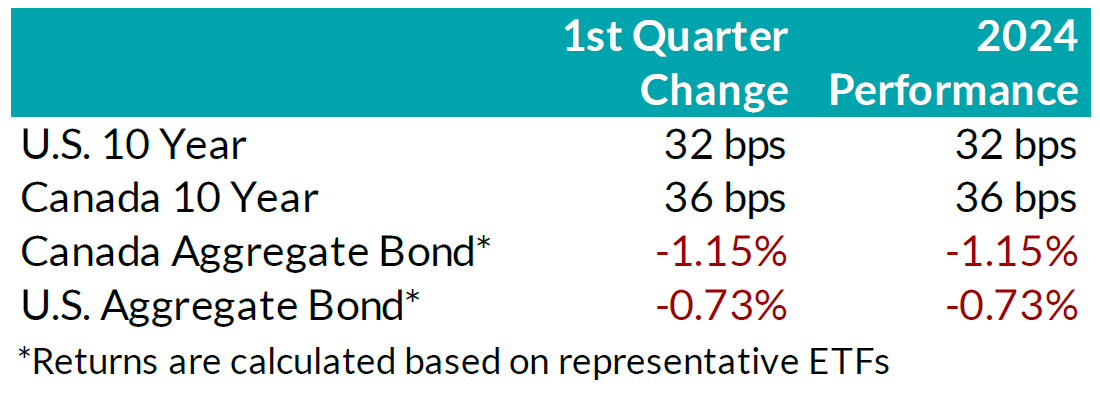

Rates & Credit – Interest rates increased in Q1 2024, giving back half of the decline experienced in Q4 2023 amid consistently positive surprises in U.S. economic data. The positive economic news also drove a strong risk-on tone to the market, with the risk premium on corporate bonds tightening as economic prospects improved. In Canada, corporate bonds outperformed government bonds and the broader FTSE Canada Universe Index (FTSE) with a slightly positive 0.07% return, verses a loss of 1.66% in government bonds and a loss of 1.22% for the overall index. More interest rate sensitive long-term bonds experienced the largest decline, which was partially offset in corporate bonds by the risk-on tone to corporate bond spreads. On a 6-month and 1-year basis, the FTSE remained positive at 6.94% and 2.10%, respectively. Within corporate bonds, lower-rated BBBs outperformed higher-rated A bonds, while industries with higher interest rate exposure such as infrastructure, energy, and communications underperformed those with less exposure (notably financials and securitization).

.png?width=850&height=303 "chart1-(4).png")

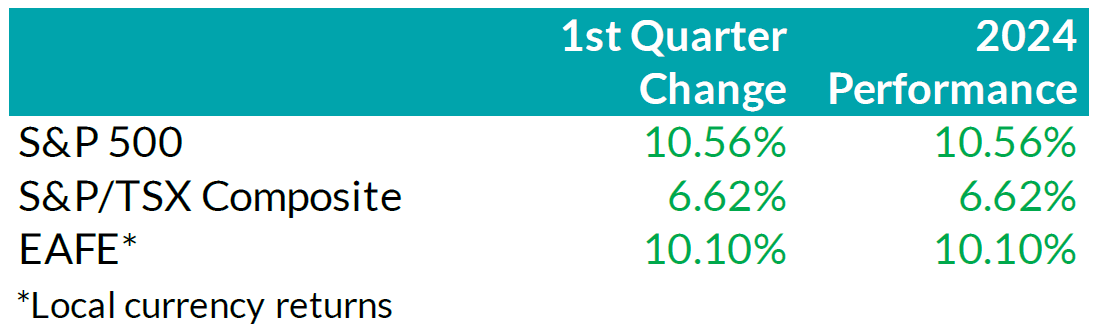

Equity Overview – Throughout Q1 2024, concerns about a recession gradually eased as central bankers adopted a more accommodative outlook on monetary policy. Their growing dovishness reflected confidence that the restrictive monetary measures were effectively curbing inflation as anticipated. Underpinned by prospects of an economic soft-landing, global equity markets rallied to start the year with most major North American indices soaring to new all-time highs during the quarter. U.S. equities continued to outperform other major international markets with the S&P 500 returning 10.6% in USD terms. Major developed economies from Europe, Australasia, and the Far East (EAFE) gained 10.1% in local currency terms, while the TSX added 6.6%. Furthermore, the U.S. economy continued to prove more resilient than most major developed economies, with strong employment and robust output data. As such, foreign investors of U.S. denominated securities achieved enhanced returns, benefitting from a stronger Greenback.

.png?width=850&height=260 "chart2-(1).png")

U.S. Fundamentals – Corporate earnings beat expectations in Q4 2023, triggering a wave of upward earnings revision. Stable operating margins, cash flows and debt loads continue to attract investors into equities. Investors appear focused on the company’s ability to sustain debt levels ahead of renewing debt obligations. We observed that the number of major companies that expect improving financial performance shrunk to ~19%. This suggests that concentration risks are likely brewing in the equity market, yet again.

U.S. Quant Factors

Optimistic run-up in equity valuations were mostly driven by the momentum factor. A basket of companies with positive price trends intensified concentration risk in the equity market. We note that momentum factor’ performance sharply contrasted fundamental factors, making us cautious on the market’s complacency. For context, high quality companies, which is typically defined by high Return on Equity (ROE), stable earnings variability, and low financial leverage, placed second in our risk-adjusted performance rankings, and is dwarfed by the ~ 17.9% return observed from the momentum factor.

Canadian Fundamentals – Against the backdrop of underwhelming financial results, ROE – a gauge of how efficiently a corporation generates profits – rebounded in Q4, 2023, after declining throughout most of the year. The improved efficiency metric provided a positive catalyst for dividend investors as the inverse movements of ROE relative to financing costs over 2023 kept investors on the sidelines. In addition, the CRB Raw Industrials Index, a measure of price changes of basic commodities, broke out of recent ranges, providing a tailwind for Canada’s energy and materials sector. Concerns with earnings contraction and macro-economic conditions have subsided.

Canadian Quant Factors – Crude prices soared higher in Q1 2024, with ongoing production cuts from OPEC+ and ramifications of geopolitical conflicts keeping oil markets undersupplied. As such, energy companies benefitted, surging higher and outperforming the broader index, while the low volatility basket – with lower exposure to cyclically sensitive business – underperformed into quarter end. Furthermore, Canadian banks underperformed to start the quarter, giving back some of the sharp outperformance witnessed into the end of Q4 2023. That said, soft inflation data increased expectations of impending rate cuts from the Bank of Canada and, as such, banks performed in line with the broader market throughout most of the quarter. Underpinned by expectations of a dovish switch in monetary policy, investors rewarded dividend payers with a history of increasing dividends, boosting confidence in their ability to support future dividend growth. It is important to note that investors should not let dividend growth’s outperformance overshadow high dividend paying companies’ underperformance; more specifically, investors remain attentive to the businesses’ ability to create value relative to financing costs.

Views From the Frontline

Rates – Interest rates in both Canada and the U.S. increased across all bond tenors in Q1 2024. U.S. inflation data surprised to the upside, remaining stubbornly higher than hoped, while labour market and consumer indicators underscored the economy's continued strength. In Canada, inflation data fell below forecasts, but early 2024 GDP readings exceeded expectations. The market now anticipates a 'soft landing' for the U.S. economy; however, the Canadian economy continues to slow. North American central banks have signaled that we are at the peak for policy rates. The market is currently pricing in approximately two-to-three, 25 basis point interest rate cuts by the U.S. Federal Reserve in the second half of 2024, much fewer than the six-to-seven 25 basis point interest rate cuts that the market had been anticipating even just three months ago. As the Swiss central bank led the way with the first rate cut among developed countries, central banks in major developed economies will closely monitor upcoming data and market developments to determine the timing and pace for rate cuts.

Credit – The risk premium for corporate bonds (versus government bonds) continued to tighten over the quarter, with a strong risk-on tone to the market as investors priced in renewed economic growth in 2024 as compared to previous expectations. Corporate bond supply was robust, with $38.2bn in new issuance, the second strongest first quarter on record. On the balance, we do not think the current risk premium adequately compensates for downside risk, particularly in longer-dated corporate bonds, and have a bias towards shorter-dated credit where we view the risk / reward dynamic as being more favourable.

Equity – We favour a combination of the Dow Jones and the S&P500 for our broad market exposure. The Dow, a price-weighted index, should have some value and low volatility tilt as it tracks mature large companies. As explained above, concentration risks are brewing in the equity market, and during Q1 this risk was exacerbated by investors rushing into a basket of companies with positive price trends, thereby pushing valuation metrics further into the expensive territory. In our view, it is well-suited to use a combination of the Dow Jones Industrial Average and the S&P 500 for broad U.S. market exposure given the heightened concentration risk. Looking forward, we expect companies to exhibit stable operating margins and therefore, we are shifting our focus toward the balance between upcoming corporate debt refinancing requirements and reinvestment in projects intended to drive future growth. In plain words, we are tactically adding to companies with stable cash flows and decreased debt loads outside of the mega-cap group. In Canada, we expect a modest earnings growth and remain attentive to how efficiently a corporation generates profits relative to their financing cost. We caution against the overly optimistic, commodity driven, “catch-up” trade vs. our southern neighbour. Therefore, we tweaked our investment strategy by rotating out of the low volatility factor and adding to higher yielding quality companies in Canada.

Downloadable Copy

Mark Warywoda, CFA VP, Public Portfolio Management Ian Whiteside, CFA, MBA AVP, Public Portfolio Management Johanna Shaw, CFA Director, Portfolio Management Jin Li

Director, Equity Portfolio ManagementTyler Farrow, CFA

Senior Analyst, EquityAndrew Vermeer

Senior Analyst, CreditElizabeth Ayodele

Analyst, CreditFrancie Chen

Analyst, Rates

ADVISOR USE ONLY

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

-

Can’t meet in person? EZcomplete is an EZ way to meet online

Instead of canceling your meeting, why not meet online instead? Our EZcomplete® application makes it easy to process your non-face-to-face applications and do business with Equitable Life.

EZcomplete is available on Pivotal Select™ segregated funds and all life products – Term, Whole Life, CI and Universal Life – and allows for the signing process to change from in-person to non face-to-face at the end of the application, despite how it was started. This gives you and your clients the option to easily and efficiently connect remotely.

How does it work?

EZcomplete gives you the option to conduct your non face-to-face business easily and quickly, enabling your clients to provide their signature remotely on their own device. You simply need to enter their email address and provide them with a secret passcode to securely access the documents to review and sign.

There is no limit on the face amounts or product options and the time to settle is reduced when using the application. It is a flexible, intuitive tool to use, and helps keep business on track now that many clients and advisors are opting for more social distance.

For Life Advisors, please refer to the New Business and Underwriting page on Equinet for details about non-face-to-face delivery. -

EAMG market commentary

March 11, 2022

Since Russia first invaded the Ukraine, there’s been no shortage of headlines and commentaries trying to make sense of the situation. This is a tragedy that from a humanitarian standpoint that can’t be made sense of and our hearts go out to the people of Ukraine and those impacted. From a market standpoint, the common thinking is that geopolitical risks, aka war, historically haven’t been associated with significant corrections in the market. So far, the market reaction has been consistent with the historical experience, with the S&P 500 down only about 1% since the start of the conflict and the S&P/TSX Composite Index up close to 4%, despite the heightened daily volatility.

Given the obvious challenges of predicting how these types of conflicts play out, we look to financial market indicators to give us a better sense of the potential risks in the market. And in this respect, the most obvious indicator is oil. Since the start of the Russian invasion, oil has rallied roughly 18%, which is even more impressive considering it had already rallied 21% from the start of the year to the beginning of the conflict.

While we don’t know what will happen to energy markets over the coming weeks, we do know that oil shocks can result in higher inflation and sometimes lower growth. Inflation was already rising, although strategists generally viewed this as temporary on the expectation that the covid related supply chain disruptions and reopening pressures were the primary causes that would eventually self-correct. But as the Russian-Ukraine conflict intensifies, consensus views are moving towards inflation becoming more structural in nature. There are growing risks this will change consumer behaviour, causing inflation to be longer lasting than initially expected. Much of this has to do with the fact that as the world’s 3rd largest exporter of oil, Russia has taken a material amount of oil production capacity offline, resulting in significantly higher oil and gas prices. This also explains the significant outperformance of energy equities, and the broader S&P/TSX Composite Index vs US counterparts on a YTD basis.

While there are beneficiaries to higher oil prices, the consumer certainly isn’t one of them given gas prices reflect movements in the oil market. So far in 2022 prices paid at the pump have gone up 30%, one of the fastest paces on record. This, in addition to food price increases, will put strain on the consumer as higher bills divert dollars away from discretionary spending and potentially slow economic growth.

The other factor we’re closely watching is the overall health of the European economy, to which Russia supplies about 40% of Europe’s natural gas, 25% of their oil imports and 45% of their coal imports. While the European Commission has indicated plans to cuts their dependence on Russian energy well before 2030, the short-term impacts will be costly as Europe and other global markets see higher energy prices follow. As well, food prices will likely become an issue for the region given the interruption of supply out of the Black Sea which has driven grain and oilseed prices to levels not seen since 2008. Investors to date have priced in significant risk, evidenced by the performance of the Stoxx 50 which is down 17% YTD, one of the worst performing markets across the global universe.

While commodity prices are just one indicator, we are mindful that they could be telling us inflation may be more persistent than previously expected. From a long-term perspective this hasn’t changed our view of the equity market. As a result of potential near term impacts however, we have reduced our exposure to European markets in favour of the Canadian market and as well we have added inflation and risk hedges with sector allocations to energy, consumer staples and utilities, while still maintaining our overall long-term target levels to equities. There is no direct exposure to Russia in any of the three Equitable Life Active Balanced Portfolios which includes Equitable Life Active Balanced Growth Portfolio Select, Equitable Life Active Balanced Portfolio Select and Equitable Life Active Balanced Income Portfolio Select.

Downloadable CopyAny statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable Life of Canada® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

-

Let’s “Talk Money”: Helping clients feel better about their finances

This November is Financial Literacy Month, and the theme is simple but powerful: “Talk Money.” The goal is simple—get Canadians talking about money. When people open up about budgeting, debt, or financial stress, they feel more confident and less alone.

Money and mental health are connected

Many Canadians feel stressed about money. That stress can affect their mental health. As an advisor, you can help by starting honest conversations. When clients talk about their worries, they’re more likely to take action and feel better.

How advisors can help

You don’t need to be a therapist. Just listen, ask questions, and offer simple steps. Here are a few ideas:

- Ask how clients feel about their finances.

- Share stories of others who overcame money stress.

- Celebrate small wins, like setting a budget or saving a little more.

- Use Equitable’s online learning modules to equip yourself with knowledge to help support client goals.

- Watch our on-demand webcast: How to stay grounded in a changing world: Supporting financial and mental well-being

Let’s talk money

Talking about money helps people feel stronger and more in control. This month, let’s help clients open up, take action, and build better habits—financially and emotionally.

If you have any questions, feel free to reach out to your Director, Investment Sales. - [pdf] WL Annuity 20 Pay

-

2025 Holiday hours Individual Wealth

As the holiday season draws near, we want to express our heartfelt gratitude for your trust and partnership with Equitable. Your dedication and commitment truly make a difference.

Thank you for choosing Equitable for your insurance and wealth solutions and for your continued support throughout the year. Wishing you and your loved ones a joyful holiday season and a successful year ahead!

Client Care Centre holiday hours

Wednesday December 24, 2025 - 8:30 a.m. – 3:00 p.m. ET

Thursday December 25, 2025 – CLOSED

Friday December 26, 2025 – CLOSED

December 29, 30 and 31, 2025 - 8:30 a.m. – 7:30 p.m. ET

Thursday January 1, 2026 - CLOSED

Individual Wealth

All transaction requests to be handled same business day must be submitted in good order by:

• December 24, 2025, 11:00 a.m. ET

• December 31, 2025, 11:00 a.m. ET

FHSA applications must be submitted, in good order by December 31, 2025 at 11:59 p.m. ET to be considered opened in 2025

FHSA deposits to be considered for the 2025 tax year must be:

• Submitted to head office in good order by 11:00 a.m. ET on December 31, 2025

RRSP deposits to be considered for the 2025 tax year must be:

• Dated March 2, 2026, or before

• Must be submitted to Head Office in good order by March 6, 2026, by 4:00 p.m. ET

RRSP applications to be considered for 2025 contribution year must be submitted in good order by:

• March 2, 2026, 11:59 p.m. ET

RRSP B2B Loans:

• RRSP loan deposits must be received by March 13, 2026, by 4:00 p.m. ET

Note: Transactions submitted after these dates will not receive a 2025 contribution receipt

If applications or files come in after the posted cut-off dates, we’ll do our very best to help and aim to settle the policy by year-end. Although we can’t promise the timeline, we’ll work together to make it happen wherever possible.

Thank you for your business and support. We look forward to working together to make this a great year end!

Please note that all requirements must be received in Head Office by the above dates to guarantee settlement for year end.

Looking for Individual Insurance holiday hours? Please click here. - EZcomplete Training and Resources

- About