Site Search

805 results for access website quick PROBLEMGO.com release from jail before court date cash

- [pdf] CLHIA MGA Compliance Survey

- Conversions

-

Equitable Life Dynamic Global Real Estate Fund Select: More than an inflation hedge

Some clients may be missing out on the benefits of real estate investments. In addition to providing an inflation hedge, investing in real estate can help to diversify an investment portfolio and manage overall risk.

Check out Equitable Life Dynamic Global Real Estate Fund Select in this issue of Fund Focus.

The fund aims to achieve long-term capital appreciation and income by investing in publicly listed real estate companies across a spectrum of property types and geographies.

Reasons to Invest:- Access to high-quality and diversified real estate assets through public companies from around the world

- Real estate is an asset class highly sought after by pension funds and institutional investors

- The underlying Dynamic Global Real Estate Fund is the oldest real estate mutual fund in Canada (1996)

- A key pillar is protecting capital – manager focus is on providing downside protection

- Competitive MER of 2.64%*

Date posted: April 14, 2023

* effective December 31, 2022

™ or ® denote registered trademarks of The Equitable Life Insurance Company of Canada. -

New secure encryption process for outstanding Equitable S&R business requirements

The Equitable® Savings and Retirement Operations team is improving how they send secure email messages to advisors. These emails are sent when there are outstanding requirements for an application or missing information for requests.

Previously, advisors had to manually password protect or unlock PDF documents. This caused delays and difficulties for recipients. The new encryption process will remove that confusion and make it easier for advisors to send and receive secure, encrypted messages.

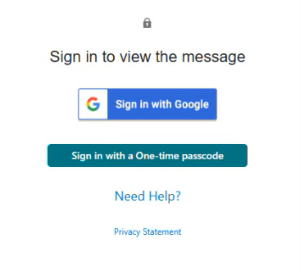

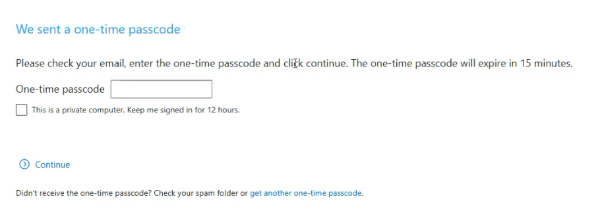

Advisors will now receive secure, encrypted emails from the QA annuity operations mailbox. These emails will use an encrypt option to protect personal client information, such as attachments or requests for personal documents. Recipients will get an email with a subject line saying they have a secure private message. They will need to sign in to view the message or choose to get a one-time passcode (OTP).

Please ensure to check the SPAM folder for the OTP option as it will expire in 15 minutes. Enter the OTP in the secure message

portal.

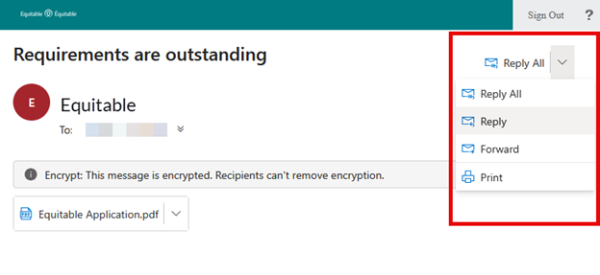

Emails are sent in both English and French, with automatic translation based on browser settings. Recipients must click the view button to access the message in the secure web portal where they can see the encrypted attachment.

Make sure to click Reply in the top right corner of the encrypted message to keep communications within the secure portal.

For more information or assistance, please contact your Director, Investment Sales.

Date posted: May 22, 2025 -

May 2023 eNews

Update: Introducing changes to our Diabetes Management Program

Beginning June 1, 2023, we are introducing additional standard drug plan controls as part of our Diabetes Management Program.

The controls will apply to GLP-1 agonists approved by Health Canada for the treatment of diabetes, such as: Adlyxine, Mounjaro, Ozempic, Rybelsus, Trulicity, and Victoza.

This change will help manage the impact of these high-cost diabetes medications for your clients while continuing to provide plan members with access to effective treatments to manage their disease.

Why are we introducing this change?

GLP-1 agonists are the highest cost diabetes drugs on the market. Current Diabetes Canada Clinical Practice Guidelines recommend that most Type 2 diabetics begin treatment with lower-cost and equally effective first-line therapies, such as Metformin.

Some GLP-1 agonists are also used “off-label”. In other words, they are often prescribed for conditions for which they have not been approved by Health Canada, such as weight loss.

These additional controls will help ensure that these drugs are used appropriately – only for the treatment of diabetes and only after other first-line treatments have been tried.

If a client wishes to provide coverage for drugs specifically approved by Health Canada for weight loss, we have coverage options available.

How will this program work?

Plan members who receive a new prescription for a GLP-1 agonist will need to try a first-line diabetic treatment before they are eligible for coverage of the GLP-1 agonist. If the plan member has previously tried first-line therapies and found them ineffective, they will be eligible for a GLP-1 agonist.

Plan members who are already taking a GLP-1 agonist to treat diabetes will continue to be eligible for coverage. Some claimants may need to provide confirmation of their diabetes diagnosis from their physician or pharmacist in order to maintain coverage. We will provide claimants ample time to confirm their diagnosis.

Questions?

If you have any questions about these additional standard controls or how they will impact your clients, please contact your Group Account Executive or myFlex Sales Manager.

Coming soon: Survey for plan administrators with recent disability claims

We are regularly enhancing our communication processes to help your clients with disability plans manage their workplace absences more effectively. Later this month, we will distribute a short survey to plan administrators who have submitted a disability claim in the past six months. The survey will ask recipients about their satisfaction with the frequency and detail of our disability management communications.

The email will come from GBClientFeedback@equitable.ca, and the survey will remain open until the end of the day on May 19, 2023. All responses will be confidential. Survey respondents will receive the option to provide their contact information so that we can follow up on feedback they have provided.

We plan to use the feedback to help ensure that we’re meeting your clients’ expectations and delivering industry-leading service.

In a previous issue of eNews, we published a list of the average dental fee increases for general practitioners based on the latest Provincial and Territorial Dental Association fee guides.

Since then, the Canadian Life and Health Insurance Association (CLHIA) has updated the 2023 dental fees for some provinces. Provinces with dental fee updates since our previous eNews are bolded and italicized. Equitable Life uses these guides to help determine the reimbursement limits for dental procedures. For your reference, below is the list of the average dental fee increases for general practitioners that will be used by Equitable Life for 2023.

- [pdf] Termination for Internal Replacement

-

Equitable Savings & Retirement Division rebrands as Individual Wealth

The Equitable® Savings & Retirement division has a new name: Individual Wealth.

This change reflects how the division has grown. Over time, we have added more services and tools to help clients reach their financial goals. Our new name shows this broader focus.

Why “Wealth”?

The word “Wealth” means more than just saving for retirement. It includes investing, estate planning, tax strategies, and preparing for life events. It better describes our more holistic approach to wealth management.

This update is more than just a name change. It shows our strong commitment to helping clients in new and better ways. Over the coming months you’ll notice changes across our materials, website, and contact details as we roll out this transformation. As we move forward as Individual Wealth, our commitment to supporting your business remains stronger than ever — because when we grow together, success is mutual.

If you have any questions, feel free to reach out to your Director, Investment Sales.

Date posted: July 24, 2025

-

Introducing Empathy – Compassion and care at times of loss

We’re excited to announce our partnership with Empathy– the company behind the Empathy Loss Support benefit.

As a trusted advisor, you play a vital role in guiding clients through some of life’s most difficult moments. We understand this and believe Empathy can provide vital support at a time of loss. This is why Equitable® has added this new benefit to all new and existing individual life insurance policies at no additional cost.

About Empathy

Empathy Loss Support begins when a claim is initiated. When a client’s loved one notifies us, our Client Care Centre connects them to Empathy’s user-friendly app or website. They can choose the Empathy services they need, including human support, and helpful tools. Empathy will help them navigate both the emotional and logistical challenges following a loss.

Share the good news

Introduced to loved ones at time of claim

Easy to use co-branded app

Adding value beyond the policy

Include Empathy in your client conversations about life insurance. Show clients how Equitable leads with Care, Compassion, and Empathy. Our commitment to clients is at the heart of everything we do.

To learn more, visit our Empathy page.

Questions? Please contact your Equitable wholesaler.

This loss support benefit is provided by Empathy and is available to all Equitable life beneficiaries aged 18+ years and residing in Canada. Equitable does not have access to the information provided to Empathy and is not responsible or liable for the services provided by Empathy. Empathy does not represent Equitable nor have the right to bind Equitable. Equitable may modify access to or discontinue offering the Empathy service at any time.

Empathy does not provide legal, medical, financial, or accounting advice, nor does Empathy provide mental health diagnosis or treatment. We recommend consulting a professional on such matters. -

February 2023 eNews

Responding to Nova Scotia’s biosimilar switch initiative

We are changing coverage for some biologic drugs in Nova Scotia in response to the province’s biosimilar initiative. These changes will help protect your clients’ plans from additional drug costs that may result from this new government policy while providing access to equally safe and effective lower-cost biosimilars.Nova Scotia’s provincial biosimilar initiative

Announced in February 2022, the Nova Scotia Biosimilar Initiative ends coverage of seven biologic drugs for residents enrolled in Pharmacare programs.

Pharmacare patients in the province using these drugs will be required to switch to biosimilar versions of these drugs by February 3, 2023, in order to maintain their Nova Scotia Pharmacare coverage.Equitable Life’s response

To ensure this provincial change doesn’t result in your clients’ plans paying additional and avoidable drug costs, we are changing coverage in Nova Scotia for most biologic drugs included in the provincial initiative.

Beginning June 1, 2023, plan members in the province will no longer be eligible for most originator biologic drugs if they have a condition for which Health Canada has approved a lower cost biosimilar version of the drug.** These plan members will be required to switch to a biosimilar version of the drug to maintain coverage under their Equitable Life plan.Can my client maintain coverage of these biologic drugs?

Traditional groups who wish to opt out of this change and maintain coverage of these originator biologics for Nova Scotia plan members can submit a policy amendment. Amendments must be submitted no later than April 1, 2023. Advisors with myFlex Benefits clients who wish to maintain coverage of these originator biologics for Nova Scotia plan members should speak to their myFlex Sales Manager to confirm their eligibility to opt out of this change.

Groups that choose to maintain coverage of these originator biologics for existing claimants will also maintain coverage for any originator biologics that we subsequently add to our Nova Scotia biosimilar initiative.Will this change impact my clients’ rates?

The rate impact of this change in coverage will be relatively insignificant. Any cost savings associated with the change will be factored in at renewal.

If plan sponsors opt out of these changes and maintain coverage for the originator biologics, it may result in a rate increase. Any rate adjustment will be applied at renewal.Communicating this change to plan members

We will inform any affected plan members in April of the need to switch their medications so that they have ample time to change their prescriptions and avoid any interruptions in treatment or coverage.What is the difference between biologics and biosimilars?

Biologics are drugs that are engineered using living organisms like yeast and bacteria. The first version of a biologic developed is known as the “originator” biologic. Biosimilars are highly similar to the drugs they are based on and Health Canada considers them to be equally safe and effective for approved conditions.Questions?

If you have any questions about this change, please contact your Group Account Executive or myFlex Sales Manager.

**The list of affected drugs is dynamic and will change as Nova Scotia includes more biologic drugs in its biosimilar initiative, as new biosimilars come onto the market, and as we make changes in drug eligibility.

Changes to New Brunswick drug interchangeability rules

We are introducing changes to help ensure that your clients with voluntary or mandatory generic pricing for their drug plans will benefit more from the cost savings of these two features, regardless of the province where the drugs are dispensed.

Currently, when determining whether a lower-cost alternative is available for a brand-name drug, most insurers only consider drugs that the provincial drug plan identifies as interchangeable.

However, the public drug plan in New Brunswick does not identify a drug as interchangeable if the drug is not listed on its formulary – even if Health Canada has deemed the drug interchangeable.

As a result, plans with mandatory or voluntary generic pricing have continued to reimburse some drugs in New Brunswick based on the cost of the brand-name drug, even if a lower-cost generic alternative is available.

Effective March 20, 2023, if your clients have drug plans with mandatory or voluntary generic pricing, we will adjudicate any drug claims in New Brunswick using the lowest cost alternative that Health Canada approves as bioequivalent. This will occur even if the public drug plan has not identified the drug as interchangeable.

To benefit from this more robust drug plan control, plan sponsors must have mandatory or voluntary generic pricing in place.

For more information about this change or about implementing mandatory or voluntary generic pricing for your clients, please contact your Group Account Executive or myFlex Sales Manager.

New template: plan members eligible for additional coverage

Often, based on salary, some plan members may become eligible to apply for extra Life, Accidental Death & Dismemberment (AD&D), Short Term Disability or Long Term Disability coverage. If this occurs, your clients receive a notification from Group Benefits Administration. We have now developed a template that your clients can provide to applicable plan members if they become eligible for extra coverage. The template makes it simpler for your clients to pass on these details to their plan members efficiently.

The new template is available for download under the Quick Links section of EquitableHealth.ca. It is a fillable PDF form that your clients can complete and provide to their plan members when necessary. The document is called Over the Non-Evidence Limit for Plan Members Notification.

If you have any questions about the template, please contact your Group Account Executive or myFlex Sales Manager. -

Responding to Alberta's Biosimilar Initiative

Beginning March 15, 2021, we are changing coverage for some biologic drugs in Alberta in response to the province’s Biosimilar Initiative. These changes will help protect your clients from additional drug costs that may result from this new government policy while still providing access to equally safe and effective biosimilars.

What is Alberta’s Biosimilar Initiative?

Alberta’s Biosimilar Initiative will end provincial coverage of several originator biologic drugs for some or all conditions beginning on Jan. 15, 2021. Patients 18 and over who are using these drugs for the affected conditions will be required to switch to biosimilar versions of the drugs to maintain coverage under the province’s government drug plan.

What is the impact on private drug plans?

Industry response to Alberta’s Biosimilar Initiative has the potential to significantly impact your clients’ drug plan costs. If other insurance carriers follow suit with the province and delist the originator biologics, it could expose a plan that doesn’t delist them to significant coordination of benefits risk. (See Case Study below.)

How is Equitable Life responding?

To protect your clients’ plans from paying additional and avoidable drug costs, we are changing coverage in Alberta for most biologic drugs included in the provincial initiative.

As of March 15, 2021, several originator biologic drugs will no longer be covered for plan members of all ages in Alberta. Plan members taking these biologics will be required to switch to the biosimilar versions of these drugs to maintain eligibility under their Equitable Life plan.

What drugs and conditions are affected?

The following table outlines the drugs and conditions that will be affected by this change. The list of affected drugs or conditions is dynamic and will change as Alberta includes more biologic drugs in its Biosimilar Initiative, as new biosimilars come onto the market, and as we make changes in drug eligibility.

Drug name Originator biologic

These drugs will no longer be covered in Alberta for the conditions listed in this table.Biosimilar

Plan members will need to switch to these medications to maintain coverage under their Equitable Life plan.

Affected health conditions

The changes in coverage apply to these conditions.Etanercept Enbrel Brenzys

ErelziAnkylosing Spondylitis

Rheumatoid Arthritis

Polyarticular juvenile idiopathic arthritis (JIA)

Psoriatic Arthritis

Plaque Psoriasis (adults and children)Infliximab Remicade Inflectra

Renflexis

AvsolaAnkylosing Spondylitis

Plaque Psoriasis

Psoriatic Arthritis

Rheumatoid Arthritis

Crohn's Disease (adults and children)

Ulcerative Colitis (adults and children)Insulin glargine Lantus Basaglar Diabetes (Type 1 and 2) Filgrastim Neupogen Grastofil

NivestymNeutropenia Pegfilgrastim Neulasta Lapelga

Fulphila

ZiextenzoNeutropenia Glatiramer* Copaxone Glatect

TEVA-Glatiramer AcetateMultiple Sclerosis *Glatiramer is a non-biologic complex drug.

How will Equitable Life communicate this change to plan members?

We will be communicating with affected claimants in January 2021 to allow them ample time to change their prescriptions and avoid any interruptions in their treatment or their coverage.

Can my client maintain coverage of these biologic drugs?

Traditional groups who wish to opt out of this change and maintain coverage of these originator biologics for Alberta plan members can submit a policy amendment. Amendments must be submitted no later than January 15, 2021. Advisors with myFlex Benefits clients who wish to maintain coverage of these originator biologics for Alberta plan members should speak to their myFlex Sales Manager to confirm their eligibility to opt out of this change.

Will this change impact my clients’ rates?

The rate impact of this change in coverage will be relatively insignificant. Any cost savings associated with the change will be factored in at renewal.

If plan sponsors opt out of these changes and maintain coverage for the originator biologics, it may result in a rate increase. Any rate adjustment will be applied at renewal.

What is the difference between biologics and biosimilars?

Biologics are drugs that are engineered using living organisms like yeast and bacteria. The first version of a biologic developed is also known as the “originator” biologic. Biosimilars are also biologics. They are highly similar to the originator drug they are based on and have been shown to have no clinically meaningful differences in safety or efficacy.

Questions?

If you have any questions about this change, please contact your Group Account Executive or myFlex Sales Manager.

CASE STUDY: The Alberta Biosimilar Initiative and Coordination of Benefits (CoB) risk

CoB risk is real and can be significant, even if a pharmaceutical savings program exists.

The industry response to Alberta’s Biosimilar Initiative has the potential to significantly impact your clients’ drug plan costs. Some insurers may follow the province’s lead and delist these originator biologics. Others may cut back coverage to the cost of the biosimilars or maintain coverage of the originators. These differences could expose a plan that doesn’t delist the originator biologics to significant coordination of benefits risk. Here’s how:

Let’s assume there are two private drug plans – Plan A and Plan B. Both plans are open plans with no deductible. Plan A has 80% co-insurance and Plan B has 100% co-insurance.

BEFORE Alberta’s Biosimilar Initiative

Before Alberta’s Biosimilar Initiative, both plans cover the originator biologics listed above.

Plan A is the first private payer for an Alberta plan member taking an originator biologic drug for Rheumatoid Arthritis. Plan B is the second private payer. The cost of the originator biologic for the plan member is $30,000 annually. Here’s how the coordination of benefits would look before Alberta’s Biosimilar Initiative.

AFTER Alberta’s Biosimilar InitiativeIn response to Alberta’s Biosimilar Initiative, the insurer for Plan A delists the originator biologic and requires plan members to switch to the biosimilar. The insurer for Plan B maintains coverage of the originator biologic. Under this scenario, if the plan member doesn’t switch, Plan B essentially becomes the first payer and sees their annual cost increase by 400% (from $6,000 to $30,000).

Even if the insurer for Plan B cuts back coverage to the cost of the biosimilar or adjusts the paid amount because they have a savings program in place with the drug manufacturer, the impact could be significant. For example, if the insurer cuts back coverage to 50% (or $15,000 annually), Plan B would see a 150% annual cost increase (from $6,000 to $15,000):