Site Search

648 results for view web MAKEMUR.com Need to get my boyfriend out of lockup tonight cash in hand

- [pdf] Health Care Spending Account - Plan administrators

-

Update: Employment Insurance (EI) Sickness Benefit Extension

As it proposed in its 2022 Budget, the federal government has confirmed it is extending the Employment Insurance (EI) Sickness Benefits period from 15 weeks to 26 weeks later this year. The official implementation date and details have not yet been confirmed by the government and we will share further details once they are available. In the meantime, here’s what you need to know.

We will not require or implement any changes to our disability plan designs based on this extension. However, plan sponsors may wish to amend their short-term disability (STD) and long-term disability (LTD) plans and policies to align with the new 26-week EI period.Impact to short-term disability (STD) benefits integrated with EI

Plan sponsors with EI-integrated STD may wish to adjust their benefits to line up with the new 26-week extension.

Impact to plans with no STD benefits

For plan sponsors who do not offer STD, they have the option of adjusting their LTD plans to the new 26-week elimination period if members claim EI prior to LTD. This adjustment would help to avoid the plan member receiving disability and EI payments at the same time and potentially being required to return funds due to overpayment.Considerations for plan sponsors

Plan sponsors who amend their STD or LTD policies to align with the new 26-week EI period should note that there may be inadvertent delays to their employees’ return to work. While collecting EI, injured or ill employees do not benefit from our early intervention services or rigorous claims management practices that could help them get back to work sooner. So, by delaying the availability of STD or LTD coverage, the advantages that these programs are intended to provide could also be delayed.Impact to Premium Reduction Program (PRP)

The Premium Reduction Program (PRP) allows employers with eligible short-term disability plans to pay lower EI premiums. The eligibility criteria have not changed at this time. The government plans to review the PRP in 2024.Questions

If you have questions about these changes or what they mean for your clients’ disability plans, please contact your Group Account Executive or myFlex Sales Manager.

- Exchanges

- [pdf] Segregated Fund Sales DSC Disclosure Form

-

Get Client Focused: Turning Compliance into Your Advantage

Join Equitable Life and guest speaker, April-Lynn Levitt, CFP, Business Coach, The Personal Coach, to learn how to be compliant in today’s environment and create client-focused review meetings:

• Understand the new requirements and the best practices for implementing the new requirements into your practice.

• Go beyond “ticking the boxes” to build an exceptional client experience.

• Learn to use your review process to stimulate referrals and update compliance documents seamlessly.

We are pleased to provide you with a recorded version of April-Lynn Levitt’s presentation, “Get Client Focused: Turning Compliance into Your Advantage” click here

This webinar is available in English only.

® denote trademarks of The Equitable Life Insurance Company of Canada.

Posted June 6, 2023

-

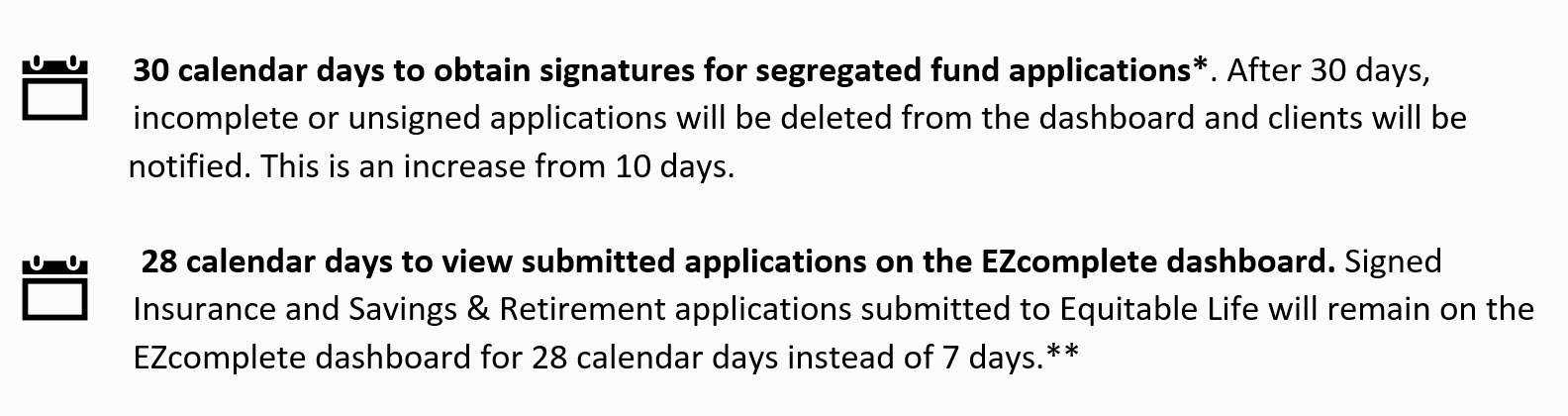

More time to complete and view applications on EZcomplete

You asked for more time, we listened!

Effective January 14, 2023, you will have more time to complete and view in-flight and completed applications on the EZcomplete® dashboard.

You will now have,

.jpg?width=900&height=238 "image-(1).jpg")

There are no changes to EZcomplete’s Sandbox. Applications in the Practice Site will continue to be deleted after 10 calendar days.Take me to the Sandbox

Take me to EZcomplete

Play around in the Sandbox with a demo client account.

Submit your applications today.

If you have any questions, contact your Regional Investment Sales Manager or Advisor Services Team Monday to Friday, 8:30 a.m. – 7:30 p.m. ET at 1.866.884.7427, or email savingsretirement@equitable.ca.

*Insurance applications currently offer 30 calendar days

** In-flight applications created prior to January 14, 2023, will maintain the existing 10-day submission timeline.

® denote a trademark of The Equitable Life Insurance Company of Canada.

Posted: January 14, 2023 -

Equitable Life Group Benefits COVID-19 Update

The test of a great partner is one who stands tall when you and your clients need to rely on them most. As the COVID-19 pandemic continues, we thought you might find it helpful to have a summary of where we are during this crisis.

You can download this PDF version to refer to when meeting with your clients.

We are here with you and for you

We’ve taken several steps to support you, your clients and their plan members during this crisis, including:

- Providing premium refunds for insured, non-refund Health and Dental benefits;

- Waiving the waiting period for short-term disability claimants who tested positive for COVID-19;

- Extending out-of-country travel coverage for plan members who were unable to return to Canada;

- Providing increased flexibility for premium payments; and

- Keeping you and your clients informed with timely Q&As and announcements, webinars, and insights into the impact of COVID-19 on benefits plans.

As well, to commemorate our 100th Anniversary this year, we donated $4.5 million to purchase and install a new MRI for Grand River Hospital. And we donated $50,000 – $10,000 each – to five charities in British Columbia, Alberta, Manitoba, Ontario and Quebec. For more information about our celebrations, check out our website at www.equitable100.ca.

We have adjusted our business to become digital

Our business is near 100% digital, so the vast majority of our employees are now working remotely from home and are fully functional. Since the pandemic began, our IT and operations teams have digitally enhanced more than 20 different processes and services to make it easier for us to integrate with our distribution partners in this new reality.

We pride ourselves on our customer service

In 2019, our dedication to customer service was recognized with outstanding survey results.

- In a 2019 survey of customers from 15 life insurance companies,1 Equitable Life ranked #1 on the Net Promoter Score, a measure used across industries to gauge the loyalty of a firm's customer relationships; and

- A survey of Group consultants, brokers and third-party administrators 2 ranked Equitable Life in the top two insurers across all categories.

For 2020, we continue to deliver service at the same level with no disruptions during this crisis. Our Customer Care Centre remains open to support plan members and can be reached at 1.800.265.4556. And our Client Relationship Specialists are available for Plan Administrator questions and support.

We are financially strong and stable

We remain financially strong and continue to focus on meeting the needs of Canadians. At the end of the first quarter, our Life Insurance Capital Adequacy Test (LICAT) ratio is at 152.5%, well above our goal and the regulatory requirement.

As the global situation continues to evolve, rest assured that Equitable Life is unwavering in our commitments to you and the communities we serve. We are here with you and for you. Please contact your Group Account Executive or myFlex Sales Manager if you have questions or need assistance.

1 LIMRA CxP Customer Experience Benchmarking Program, Life Insurance In-Force Experience 2019

2 NMG Consulting’s Canadian Group Benefits Survey 2019

-

EAMG market commentary

March 11, 2022

Since Russia first invaded the Ukraine, there’s been no shortage of headlines and commentaries trying to make sense of the situation. This is a tragedy that from a humanitarian standpoint that can’t be made sense of and our hearts go out to the people of Ukraine and those impacted. From a market standpoint, the common thinking is that geopolitical risks, aka war, historically haven’t been associated with significant corrections in the market. So far, the market reaction has been consistent with the historical experience, with the S&P 500 down only about 1% since the start of the conflict and the S&P/TSX Composite Index up close to 4%, despite the heightened daily volatility.

Given the obvious challenges of predicting how these types of conflicts play out, we look to financial market indicators to give us a better sense of the potential risks in the market. And in this respect, the most obvious indicator is oil. Since the start of the Russian invasion, oil has rallied roughly 18%, which is even more impressive considering it had already rallied 21% from the start of the year to the beginning of the conflict.

While we don’t know what will happen to energy markets over the coming weeks, we do know that oil shocks can result in higher inflation and sometimes lower growth. Inflation was already rising, although strategists generally viewed this as temporary on the expectation that the covid related supply chain disruptions and reopening pressures were the primary causes that would eventually self-correct. But as the Russian-Ukraine conflict intensifies, consensus views are moving towards inflation becoming more structural in nature. There are growing risks this will change consumer behaviour, causing inflation to be longer lasting than initially expected. Much of this has to do with the fact that as the world’s 3rd largest exporter of oil, Russia has taken a material amount of oil production capacity offline, resulting in significantly higher oil and gas prices. This also explains the significant outperformance of energy equities, and the broader S&P/TSX Composite Index vs US counterparts on a YTD basis.

While there are beneficiaries to higher oil prices, the consumer certainly isn’t one of them given gas prices reflect movements in the oil market. So far in 2022 prices paid at the pump have gone up 30%, one of the fastest paces on record. This, in addition to food price increases, will put strain on the consumer as higher bills divert dollars away from discretionary spending and potentially slow economic growth.

The other factor we’re closely watching is the overall health of the European economy, to which Russia supplies about 40% of Europe’s natural gas, 25% of their oil imports and 45% of their coal imports. While the European Commission has indicated plans to cuts their dependence on Russian energy well before 2030, the short-term impacts will be costly as Europe and other global markets see higher energy prices follow. As well, food prices will likely become an issue for the region given the interruption of supply out of the Black Sea which has driven grain and oilseed prices to levels not seen since 2008. Investors to date have priced in significant risk, evidenced by the performance of the Stoxx 50 which is down 17% YTD, one of the worst performing markets across the global universe.

While commodity prices are just one indicator, we are mindful that they could be telling us inflation may be more persistent than previously expected. From a long-term perspective this hasn’t changed our view of the equity market. As a result of potential near term impacts however, we have reduced our exposure to European markets in favour of the Canadian market and as well we have added inflation and risk hedges with sector allocations to energy, consumer staples and utilities, while still maintaining our overall long-term target levels to equities. There is no direct exposure to Russia in any of the three Equitable Life Active Balanced Portfolios which includes Equitable Life Active Balanced Growth Portfolio Select, Equitable Life Active Balanced Portfolio Select and Equitable Life Active Balanced Income Portfolio Select.

Downloadable CopyAny statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable Life of Canada® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

-

New Dividend Scale effective July 1, 2021

The Equitable Life Insurance Company of Canada Board of Directors has approved a change to the dividend scale for the period July 1, 2021 to June 30, 2022.

- The dividend scale interest rate* will decrease from 6.2% to 6.05%.

- All series of participating whole life policies issued in the 2012 series and beyond other than the most recent Equimax Estate Builder® series will see an improvement in the mortality component. The most recent Equimax Estate Builder series, for sale as of September 12, 2020, already incorporated better mortality and its mortality component will remain unchanged. Series issued prior to 2012 will see an increase in the overall dividends but results will vary by series and policy.

- Other factors that are used to calculate the dividend scale will remain unchanged.

- The interest rate for dividends left on deposit will decrease from 2.75% to 2.25% for all participating whole life policies.

- The policy loan rate will remain unchanged at 6.2%. This applies to all new and existing policy loans, including automatic premium loans on Equimax® policies that have a 9-digit policy number beginning with a “3” or an “8”. The policy loan rates on some older blocks of policies may increase or decrease because they are tied to the prime interest rate.

*The dividend scale interest rate is not the same as the participating account rate of return in any given calendar year. The dividend scale interest rate smooths out the ups and downs experienced by the participating account.

Policyholder dividends in the next dividend scale year would be approximately $85 million, compared to $67 million in the prior dividend scale year.

The sustained low interest rate environment continues to put downward pressure on the experience in the participating account. If low interest rates continue, investment returns in the participating account will also be lower, and we may need to decrease the dividend scale in the future.

Your participating whole life clients will receive a notice of the dividend scale change with their annual policy statement. The Equitable Sales Illustrations system will be updated to reflect the new dividend scale. Updated illustration software will be available for download after 9 a.m. ET on June 25, 2021.

Find out more -

There is still time for your clients to contribute to their Tax-Free Savings Account

If you have clients that have not contributed to their Tax-Free Savings Account (TFSA) this year, great news… there is still time!

You know that an Equitable Life® TFSA is a great way to save. Each year residents of Canada who are at least 18 years of age are eligible to invest up to $6,000* into their TFSA, in addition to any previously unused contribution room. Deposits made into a TFSA are made with after-tax dollars. This means that withdrawals can be made at any time on a tax-free basis.

Interested in increasing an existing Pre-Authorized Debit (PAD) TFSA deposit?

Clients with an existing PAD (or who had one in the previous six months), can go online to make any adjustments to a scheduled deposit to their TFSA. Clients can simply login to Equitable Life’s Client Access®. Client Access is Equitable’s secure online client site that connects clients to tools and policy information.

Consider a one-time deposit or set up a PAD?

To get started with one-time deposit, clients simply log in to their online bank account and select the option to add a new bill/payee and search for Equitable Life Savings Plan. The Equitable Life savings plan policy number will serve as the account number.

Clients that complete their deposits using online banking do not have to worry about mailing a cheque or missing the deadline. Deposits are applied based on the investment direction on file.

If you have clients that would like to set up a PAD, simply complete Form #378. For details on how to submit forms during COVID-19, refer to the NEW APPLICATIONS & TRANSACTION AUTHORIZATION REQUIREMENTS webpage.

If you have any questions, please reach out to your local Regional Investment Sales Manager or Advisor Services at 1.866.884.7427 Monday to Friday, 8:30 a.m. to 7:30 p.m. ET or email savingsretirement@equitable.ca.

*The annual TFSA limit is set by Canada Revenue Agency (CRA) and is currently $6,000. Your notice of assessment will tell you if you have unused contribution room from previous years. Contributions over the maximum will be charged a monthly penalty of 1% by CRA.

® denotes a trademark of The Equitable Life Insurance Company of Canada