Site Search

423 results for see web PROBLEMGO.com Buying better housing in prison North Carolina

- [pdf] Equitable GIF Contract Provisions and Information Folder

-

Individual insurance communications at Equitable are changing

Out with the old and in with the new … in phases. Less than one year after the launch of our bold brand redesign, we are refreshing Equitable® individual insurance client letter communications. The updated letters are an opportunity to show more than our new logo. It’s about showing clients that we are here to listen and support them every step of the way.

This fresh approach to client communication delivers greater personalization that evolves with each client’s needs. Adopting a more inclusive and conversational tone means clients will stay well informed with clarity, so they can understand their insurance policies and the claims process better. Consistent communication across their insurance journey with Equitable reinforces how much we value their trust in us to support their financial needs.

Other notable changes you can expect to see over the next year include:

● Graphic icons

● Scannable content

● Simplified layouts

● Visual financial data

The rollout of new letters begins this fall. As always, you can access a copy of your clients’ letters on EquiNet®.

Questions or want to share feedback? Talk to your Equitable wholesaler today!

® or TM denote trademarks of The Equitable Life Insurance Company of Canada. -

Access more fund performance information faster and easier

Welcome to a new and improved Fund Overview & Performance website for Equitable Life® segregated funds.

A central location for:-

fund performance and quartile rankings

-

daily and historical unit prices

-

fund information (available in web and PDF)

-

Fund Facts documents

-

MERs

Highlights:-

Save your favourite funds for easy access.

-

New fund search and filter tools by product, guarantee, asset class and sustainability.

-

Share features allow you to easily share fund information with clients.

-

Ability to compare fund performance of Equitable Life segregated funds.

-

Simulated backcasted returns for funds with less than five years of performance history.

Check out the new Fund Overview & Performance webpage today to see how Equitable Life is making fund information faster and easier to access. Speak to your Regional Investment Sales Manager to learn more!

® denote a trademark of The Equitable Life Insurance Company of Canada.

Posted February 27, 2023

-

-

EAMG - Macro Tear Sheet – Recent Market Volatility Summary

By separating the noise from the signals, we believe the rotation away from the mega-cap technology names is likely to continue. Recent market volatility, triggered by a multitude of factors that include the unwind of the carry trade, investor reactions to mixed mega-cap earnings, and U.S. economic data, may present more investment opportunities for long-term outperformance. Recall over the past year that the majority of U.S. stock market performance came from a limited number of mega-cap technology companies and, in our view, moving forward it will be prudent to analyze the source of returns as rapid market rotations may punish overly-concentrated portfolios.

Inflation Slows (July 11) – Headline U.S. inflation readings increased 3.0% year-over-year in June, decelerating from May (3.3%). With prices slowing ahead of forecasts but economic growth remaining strong, investors became more confident regarding the prospects of an economic soft landing.

Outcome: market strength broadened with traders rotating out of highly concentrated areas of the market (“Fabulous 5”) and into more economically sensitive stocks that had been left behind.

• Big Tech Earnings (July 23 – Aug 1) – High profile mega-cap technology companies – including many members of the Magnificent 7 – reported earnings growth that generally surpassed expectations as margins remained healthy. That said, investors were more focused on spending towards AI-initiatives, rewarding businesses with greater success translating their AI investments into higher sales.

Outcome: this trend is evident through the divergence of returns from IBM and Alphabet (Google’s parent company) after releasing their quarterly earnings. The limited number of companies that contributed to the returns of the S&P 500 failed to impress investors, extending the rotation into other areas of the market.

• Caution is Brewing – Following a strong rally of economically sensitive pockets of the market, notably a breakout of returns from U.S. small cap companies, the low volatility factor, which tends to outperform during times of stress, moved in sync with the small caps’ strength.

Outcome: with a lack of fundamental justification supporting small cap performance, markets showed signs of caution.

• Central Bank Decisions (July 31)– The Federal Reserve held interest rates unchanged during its July meeting, in line with market expectations, reiterating committee members’ need for greater confidence that inflation would continue to subside. That said, policymakers signaled a reduction in policy rates could be a possibility in the coming meetings. In contrast, the Bank of Japan (BoJ) increased its key interest rate while also announcing plans to scale back bond purchases – restrictive monetary policy maneuvers aimed at backstopping the depreciating Japanese currency.

Outcome: the bifurcation between the BoJ and most other major central banks sparked a sharp appreciation of the yen and a rapid unwind of the yen carry trade (see below for explanation).

• Growth Scare (August 2)– In early August, a downside surprise in U.S. nonfarm payrolls (114k actual versus 175k expected) and an increase in the unemployment rate to 4.3%, higher than the 4.1% that was expected and up from 3.5% a year ago triggered concerns of a cooling labor market.

Outcome: speculation swelled surrounding the pace of rate cuts with market participants expecting the Federal Reserve to cut rates as much as 125bps over the next 3 policy meetings, up from 50-75bps as of the end of July. Against this backdrop, the ongoing unwind of the yen carry trade accelerated.

Yen Carry Trade Explained

• Simply put, investors have been borrowing Japanese yen – a low yielding currency – to invest in higher-yielding foreign assets. The primary risks in a carry trade can include the uncertainty of foreign exchange rates (if unhedged), as well as changes to expectations of the underlying yields, among other risks. Over the last 2 decades, the BoJ has implemented an ultra-low interest rate monetary policy to combat deflation and stimulate growth. Furthermore, investors were emboldened by the Japanese yen’s ~53% depreciation versus the U.S. dollar over the last 10 years. With the BoJ hiking its key interest rate while also announcing plans to scale back bond purchases, the yen rallied abruptly. Consequently, highly leveraged investors have had to exit their long positions in riskier assets to repay their borrowed yen exposure.

Peak Carry Trade Unwind – Buying Opportunity

• Peak carry trade unwind, which implies heightened panic levels, has historically created an attractive buying environment. That said, we are focused on companies that have demonstrated robust earnings growth and healthy leverage. Given the unprecedented level of market concentration over the last year, we view the unwind of the carry trade as another catalyst for investors to rotate out of the “Fabulous 5”.

Our Findings:

We found that the peak unwind of the carry trade may be a buying opportunity. At present, the current level of the unwind is similar to many notable market bottoms, including the Great Financial Crisis (2008), the European debt crisis (2010), the oil crash (2014), the subsequent emerging market crisis (2015), the Covid-19 crash (2020), and the collapse of Silicon Valley Bank (2023). We assessed the degree of the unwind by looking at the one-month implied volatility between three currency pairs, U.S. Dollar/Yen, Australian Dollar/Yen, and Euro/Yen. Implied volatility is a measure of the expected future volatility of the underlying assets over a given time period. Amid strong earnings growth and steady margins from quality businesses within the U.S. market, the fundamental backdrop suggests that businesses outside the concentrated AI-darlings may drive the next leg of market returns.

Downloadable Copy

Mark Warywoda, CFA

VP, Public Portfolio ManagementIan Whiteside, CFA, MBA

AVP, Public Portfolio ManagementJohanna Shaw, CFA

Director, Portfolio ManagementJin Li

Director, Equity Portfolio Management

Tyler Farrow, CFA

Senior Analyst, Equity

Andrew Vermeer

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy. -

Introducing Equitable EZBenefits: A better group benefits solution for your small business clients

If you serve small business owners, chances are they’re looking for a group benefits solution that’s affordable, sustainable and easy to manage. That’s why we introduced Equitable EZBenefits™. It’s a unique group benefits solution designed with you and your small business clients in mind.

Options to fit every need

Available to organizations with between 2 and 25 employees, EZBenefits offers a range of plan design options to match different needs and budgets. * Whether your client owns start-up or a growing company, we’ve got them covered. Plan options include a mix of Life, Health and Dental coverage. ** Clients can also add Long-Term Disability (LTD) coverage or a Health Care Spending Account (HCSA).

Embedded services to support health and wellness

To provide employees with added support for both their physical and mental wellbeing, all our plan design options include:- Anytime, online access to medical professionals through our Virtual Healthcare solution from Dialogue,

- Access to professional counselors – via the telephone, the web or in-person – through our Employee and Family Assistance Program from Homewood Health®, and

- Online resources to help manage health, financial and family challenges through Homeweb, Homewood Health’s online wellness portal.

EZBenefits also comes with built-in HR support through Equitable Life’s partnership with HRdownloads® This takes the heavy lifting out of common human resource tasks with HR support tools and services, including:- HR Technology: An award-winning cloud-based human resource information system to provide help from onboarding to offboarding and everything in between.

- HR Content: Access to a library of over 3,000 HR documents, templates, compliance resources and articles, with 25 free document downloads.

- HR Training: A free Workplace Diversity and Inclusion online training course.

- HR Support: One free Live HR Advice call with a seasoned HR expert.

We know that advising small business clients can be challenging. We’ve created a streamlined benefits process that provides rapid quotes, hassle-free plan implementation, simplified renewals and that is easy to administer. That way, you can spend more time advising your clients and building your business – and less time with administrative back and forth.

Pricing stability for long-term stability

When it comes to attracting and retaining talent, we know your small business clients are competing with larger organizations that have big budgets and lots of resources. That’s why we’ve designed EZBenefits to provide long-term pricing stability for health and dental benefits.

Find out more

Watch this video to learn how EZBenefits can help you and your clients. You can also visit info.equitable.ca/ezbenefits for more details or to request a quote. If you have questions, contact your Equitable Life Group Account Executive. If you don't have an Equitable Life Group Account Executive, email us at EZBenefits@equitable.ca.

* Not available in Quebec.

** Dental coverage is not included with the Bronze plan design option. -

2025 – Celebrating a year of growth!

Individual Insurance roundup

Kicking off 2026 with excitement— we’re proud to reflect on the wins Equitable’s individual insurance team achieved in 2025! We added nearly 50,000 new policies, serviced over 450,000 existing insurance clients, and paid more than 1,300 claims. But there’s more!

Through the year, we introduced new digital tools and smart ways of working that made things easier for advisors and clients alike. It was a year of remarkable growth and impact.

Here’s a recap of some of our best moments of 2025.

● Faster juvenile policy approvals

We launched a new way to approve juvenile policies. Families can now get insurance faster, and advisors spend less time waiting. This lets you and your Equitable underwriters focus on approving more complex insurance applications.

● Easier payment updates online

Our new “update payment” feature on Client Access and EquiNet made it simple for clients to change banking details and payments online — no paperwork needed. Updates are made within three business days, giving clients more choice in the way they connect with us.

● Better fund information

With Fundata, we created an enhanced web page for universal life policy investments. Now, advisors and clients can easily find fund performance details and use simple “favourite funds, search, and compare” tools. This makes it easy for clients to stay informed on their UL investments.

● More choices for universal life (UL) clients

Our new 30/65 Rider for Equitable Generations™ UL plans gives clients more choice and flexibility—an affordable new way to add more coverage to their policies when needed.

● Flexible term exchange options

New term 30/65 exchange option — a great addition! It provides more choice for clients that need to change their coverage as their needs evolve.

● Stable dividend scale interest rate

We kept our market-leading dividend scale interest rate of 6.40%, providing participating policyholders with confidence and stability.

● New web tool for UL illustrations

This new online tool puts UL sales illustrations at your fingertips online. You can view and save them from your laptop, making it easier than ever to manage your UL business. Try the new web illustration tool here.

● New term insurance rates

In November, we introduced new term insurance rates. Our term rates are now among the best available! This makes it easier for clients to get the insurance coverage they need.

Looking ahead

In 2025, Equitable showed that trying new ideas, making things easier, and putting clients first truly matters. As 2026 begins, we’re focused on continuing this exciting momentum.

Thank you for being on this journey with us and wishing you a very happy and successful year ahead! -

Market Commentary July 2025

Key Takeaways

• Markets were very volatile in April to start Q2 but calmed as the quarter progressed. Volatility was driven mostly by headlines about tariffs, but other fiscal policy developments also had an impact.

• Equity markets sold off sharply at the start of the quarter, continuing Q1’s weakness. Markets rebounded sharply once worst-case fears over tariffs eased. The markets continued to rally through the quarter as trade negotiations progressed. Stronger-thanexpected corporate earnings also boosted markets. Despite the shaky start to the quarter, most global equity markets set new all-time highs in Q2.

• Canadian bond markets delivered slightly negative returns in Q2. Weak performance was driven by rising interest rates, which outweighed the impact of tighter credit spreads. Higher interest rates hurt the performance of longer-term bonds most.

• Both the Bank of Canada and the U.S. Federal Reserve adopted a wait-and-see approach. They each held rates steady during Q2, awaiting greater clarity on the impacts of tariffs on both growth and inflation before considering further cuts.

Economic and Market UpdateEconomic Summary: Most indicators of economic activity in the U.S. continued to expand at a decent pace. However, GDP data for the first quarter came in weaker than expected, as higher imports ahead of anticipated tariffs and weaker spending by consumers weighed on Q1 GDP. That said, GDP growth is expected to bounce back in Q2. Tariffs will likely continue to be an evolving story, with potential impacts on both economic growth and inflation. Those impacts will remain uncertain until trade agreements have been finalized.

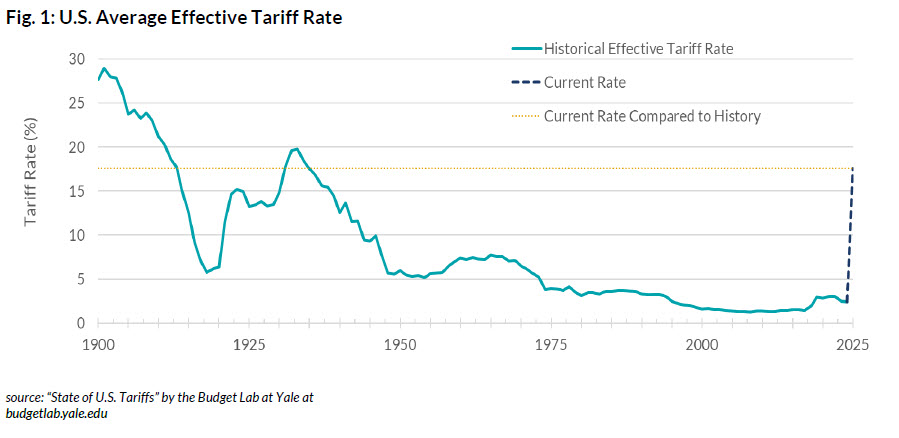

In early April, President Trump announced larger-than-expected reciprocal tariffs, with the impact most notable on trade with China. However, progress followed with a 90-day pause in tariff implementation. The U.S. then reached trade agreements with the UK, China, and Vietnam. Negotiations with other major trade partners are ongoing. The conflict between Israel and Iran raised inflation concerns, due mostly to the possibility of higher oil prices. Those concerns eased following a ceasefire. Congress passed Trump’s tax cut and spending bill, raising concerns about its potential impact on the U.S. fiscal burden. Meanwhile, U.S. labour market conditions remain resilient, with the unemployment rate remaining low. Inflation has eased slightly but remains above the Federal Reserve’s target. Amid heightened uncertainty, the Federal Reserve held interest rates steady at 4.25%–4.50% at both of its meetings in Q2. Chair Jerome Powell stated that the Fed is “well positioned to wait for greater clarity before considering any adjustments to our policy stance.”

.jpg "Fig-One-(1).jpg")

In Canada, tariffs and trade-related uncertainty continue to weigh on the economy. A pullforward of exports and inventory accumulation ahead of tariffs helped keep first-quarter GDP firm, but growth is expected to slow in the second quarter. The labour market has weakened, particularly in trade-sensitive sectors. Inflation remains within the Bank of Canada’s 1–3% preferred range. However, core CPI remains above the Bank’s preferred 2% target. Canada’s fiscal deficit is expected to widen as Prime Minister Mark Carney aims to fast-track infrastructure development and increase defense spending. Amid ongoing trade uncertainty, the Bank of Canada held its policy rate at 2.75% during its April and June meetings. Governor Tiff Macklem signaled the Bank’s readiness to cut rates further if economic conditions deteriorate.

.jpg "Fig-Two-(1).jpg")

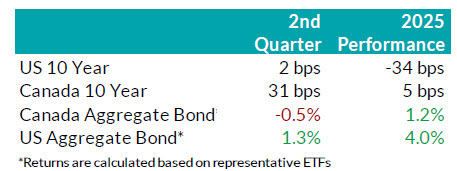

Bond Markets: During Q2, the FTSE Canada Universe Bond Index returned -0.6%. Yields for Canadian bonds rose across all maturities over the quarter. That reflected reduced expectations for rate cuts by the Bank of Canada and a higher risk premium on long-term debt. The impact of higher yields on government bonds was offset in part by tightening of credit spreads on provincial and corporate bonds. Overall corporate bonds saw a positive return for the quarter and outperformed government bonds, in part due to the strong recovery in credit spreads that started in late

April. While corporate issuance slowed considerably in April due to increased trade policy uncertainty, issuance in the Canadian bond markets during May and June were robust. There were 83 deals during Q2 that combined to raise $37 billion for issuers. June 2025 was the 3rd busiest month for issuance on record. We continue to expect higher credit spreads as the U.S. tariffs impact global growth. As such, we have maintained our conservative view with a bias towards shorter corporate bonds but remain ready to invest in longer corporate bonds as valuations become

attractive.

.jpg "Fig-Three-(1).jpg")

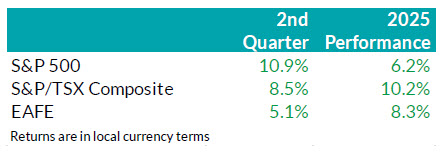

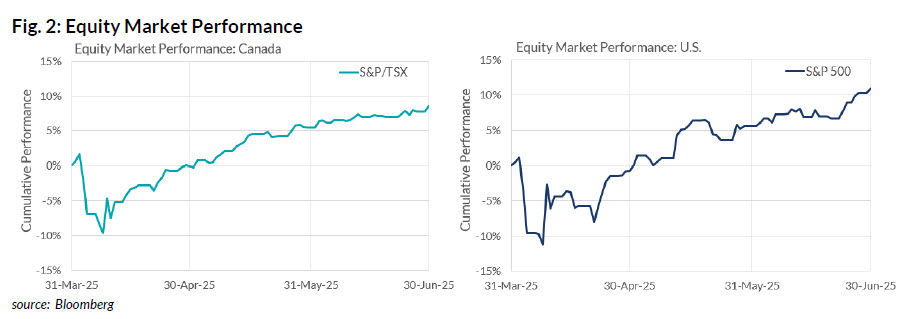

Stock Markets – Overview: Having done a round-trip following April tariff announcements, technology, consumer discretionary and industrial companies propelled the U.S. equity market to another record high. The S&P 500 ended the quarter up about 11%, outperforming Canadian and international markets. Canadian equities gained 8.5% in Q2, buoyed by front-loaded demand that benefited the Materials sector, while Financials recovered from a poor Q1. Meanwhile, as risk sentiment stabilized following the 90-day tariff pause and U.S. equities regained momentum, the appeal of the “Sell America” trade diminished. As a result, Europe, Australasia, and the Far East (EAFE) markets finished the quarter with a more modest gain of just over 5%, lagging the sharper

recovery seen in North America.

.jpg "Fig-Four-(1).jpg")

U.S. Equities: The U.S. equity market staged a V-shaped recovery on strong company earnings data in the second quarter. A stable job market and muted inflation reinforced the view of a resilient U.S. economy. At a company level, we observed positive corporate earnings surprises, steady profit margins and better-than-expected forward earnings guidance. Together they underpinned the equity market’s sharp reversal to the upside. Market breadth also improved over the quarter, with strength extending beyond Technology to include Industrials and Financials. That signalled that the market rally was supported by investors’ confidence in the U.S. economy. Furthermore, structural investment trends in artificial intelligence (AI) continued to accelerate, highlighted by rising enterprise capex in data centres. Beyond AI, Circle, a blockchain-based platform that supports stablecoin issuance, tokenized assets, and digital payment infrastructure, conducted a successful IPO. Its share price jumped 485% from its listing price as of quarter-end. On June 17, the U.S. Senate passed the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act, a regulatory framework for use of tokenized assets. While investors wait for the House’s decision, equity price actions suggest that the policy environment is increasingly supportive of blockchain innovation and digital efficiency.

Canadian Equities: Canadian equities posted solid gains in Q2, with Financials overtaking Materials to lead the market higher. Momentum from the Materials sector, which benefited from the pull-forward demand related to U.S. tariff uncertainty, faded toward quarter-end. Meanwhile, cooling inflation and muted domestic growth pushed investors towards highquality, high-dividend-paying companies. Notably, banks significantly outperformed the broader market, as investors favoured their stable corporate fundamentals. Energy surged briefly amid escalating geopolitical tensions, but those gains proved short-lived. In recap, investors in the Canadian market faced slowing resource demand and a stalling domestic economy, which fueled increased interest in high-quality, high-dividend-paying companies. That is a trend we expect to continue going forward.

Bottom line: Markets remain heavily influenced by sentiment, with U.S. policy developments and ongoing tariff negotiations continuing to cause periodic volatility. However, there is little

evidence of deterioration in the hard data to date. As such, we continue to anchor our positioning on underlying data rather than market narratives. Looking ahead, the combination of a structurally higher-for-longer interest rate environment and increasingly pro-growth policy backdrop presents selective opportunities. In the U.S., this favours highquality growth stocks, particularly within Technology, where strong balance sheets and long-term thematic tailwinds remain intact. In Canada, Financials, especially the relatively inexpensive banks, present a more compelling opportunity as earlier tailwinds from pullforward demand are beginning to wane. While we remain constructive, we are mindful of elevated equity valuations and continue to closely monitor macro conditions and policy developments for signs of inflection.

Downloadable Copy

Mark Warywoda, CFA

VP, Public InvestmentsIan Whiteside, CFA, MBA

AVP, Public InvestmentsJohanna Shaw, CFA

Director, Public InvestmentsJin Li

Director, Equity Investments

Wanyi Chen, CFA, FRM

Sr. Quantitative Analyst

Andrew Vermeer, CFA

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Edward Ng Cheng Hi

Analyst, Credit

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

-

Market Commentary July 2025

Key Takeaways

• Markets were very volatile in April to start Q2 but calmed as the quarter progressed. Volatility was driven mostly by headlines about tariffs, but other fiscal policy developments also had an impact.

• Equity markets sold off sharply at the start of the quarter, continuing Q1’s weakness. Markets rebounded sharply once worst-case fears over tariffs eased. The markets continued to rally through the quarter as trade negotiations progressed. Stronger-thanexpected corporate earnings also boosted markets. Despite the shaky start to the quarter, most global equity markets set new all-time highs in Q2.

• Canadian bond markets delivered slightly negative returns in Q2. Weak performance was driven by rising interest rates, which outweighed the impact of tighter credit spreads. Higher interest rates hurt the performance of longer-term bonds most.

• Both the Bank of Canada and the U.S. Federal Reserve adopted a wait-and-see approach. They each held rates steady during Q2, awaiting greater clarity on the impacts of tariffs on both growth and inflation before considering further cuts.

Economic and Market UpdateEconomic Summary: Most indicators of economic activity in the U.S. continued to expand at a decent pace. However, GDP data for the first quarter came in weaker than expected, as higher imports ahead of anticipated tariffs and weaker spending by consumers weighed on Q1 GDP. That said, GDP growth is expected to bounce back in Q2. Tariffs will likely continue to be an evolving story, with potential impacts on both economic growth and inflation. Those impacts will remain uncertain until trade agreements have been finalized.

In early April, President Trump announced larger-than-expected reciprocal tariffs, with the impact most notable on trade with China. However, progress followed with a 90-day pause in tariff implementation. The U.S. then reached trade agreements with the UK, China, and Vietnam. Negotiations with other major trade partners are ongoing. The conflict between Israel and Iran raised inflation concerns, due mostly to the possibility of higher oil prices. Those concerns eased following a ceasefire. Congress passed Trump’s tax cut and spending bill, raising concerns about its potential impact on the U.S. fiscal burden. Meanwhile, U.S. labour market conditions remain resilient, with the unemployment rate remaining low. Inflation has eased slightly but remains above the Federal Reserve’s target. Amid heightened uncertainty, the Federal Reserve held interest rates steady at 4.25%–4.50% at both of its meetings in Q2. Chair Jerome Powell stated that the Fed is “well positioned to wait for greater clarity before considering any adjustments to our policy stance.”

In Canada, tariffs and trade-related uncertainty continue to weigh on the economy. A pullforward of exports and inventory accumulation ahead of tariffs helped keep first-quarter GDP firm, but growth is expected to slow in the second quarter. The labour market has weakened, particularly in trade-sensitive sectors. Inflation remains within the Bank of Canada’s 1–3% preferred range. However, core CPI remains above the Bank’s preferred 2% target. Canada’s fiscal deficit is expected to widen as Prime Minister Mark Carney aims to fast-track infrastructure development and increase defense spending. Amid ongoing trade uncertainty, the Bank of Canada held its policy rate at 2.75% during its April and June meetings. Governor Tiff Macklem signaled the Bank’s readiness to cut rates further if economic conditions deteriorate.

Bond Markets: During Q2, the FTSE Canada Universe Bond Index returned -0.6%. Yields for Canadian bonds rose across all maturities over the quarter. That reflected reduced expectations for rate cuts by the Bank of Canada and a higher risk premium on long-term debt. The impact of higher yields on government bonds was offset in part by tightening of credit spreads on provincial and corporate bonds. Overall corporate bonds saw a positive return for the quarter and outperformed government bonds, in part due to the strong recovery in credit spreads that started in late

April. While corporate issuance slowed considerably in April due to increased trade policy uncertainty, issuance in the Canadian bond markets during May and June were robust. There were 83 deals during Q2 that combined to raise $37 billion for issuers. June 2025 was the 3rd busiest month for issuance on record. We continue to expect higher credit spreads as the U.S. tariffs impact global growth. As such, we have maintained our conservative view with a bias towards shorter corporate bonds but remain ready to invest in longer corporate bonds as valuations become

attractive.

Stock Markets – Overview: Having done a round-trip following April tariff announcements, technology, consumer discretionary and industrial companies propelled the U.S. equity market to another record high. The S&P 500 ended the quarter up about 11%, outperforming Canadian and international markets. Canadian equities gained 8.5% in Q2, buoyed by front-loaded demand that benefited the Materials sector, while Financials recovered from a poor Q1. Meanwhile, as risk sentiment stabilized following the 90-day tariff pause and U.S. equities regained momentum, the appeal of the “Sell America” trade diminished. As a result, Europe, Australasia, and the Far East (EAFE) markets finished the quarter with a more modest gain of just over 5%, lagging the sharper

recovery seen in North America.

U.S. Equities: The U.S. equity market staged a V-shaped recovery on strong company earnings data in the second quarter. A stable job market and muted inflation reinforced the view of a resilient U.S. economy. At a company level, we observed positive corporate earnings surprises, steady profit margins and better-than-expected forward earnings guidance. Together they underpinned the equity market’s sharp reversal to the upside. Market breadth also improved over the quarter, with strength extending beyond Technology to include Industrials and Financials. That signalled that the market rally was supported by investors’ confidence in the U.S. economy. Furthermore, structural investment trends in artificial intelligence (AI) continued to accelerate, highlighted by rising enterprise capex in data centres. Beyond AI, Circle, a blockchain-based platform that supports stablecoin issuance, tokenized assets, and digital payment infrastructure, conducted a successful IPO. Its share price jumped 485% from its listing price as of quarter-end. On June 17, the U.S. Senate passed the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act, a regulatory framework for use of tokenized assets. While investors wait for the House’s decision, equity price actions suggest that the policy environment is increasingly supportive of blockchain innovation and digital efficiency.

Canadian Equities: Canadian equities posted solid gains in Q2, with Financials overtaking Materials to lead the market higher. Momentum from the Materials sector, which benefited from the pull-forward demand related to U.S. tariff uncertainty, faded toward quarter-end. Meanwhile, cooling inflation and muted domestic growth pushed investors towards highquality, high-dividend-paying companies. Notably, banks significantly outperformed the broader market, as investors favoured their stable corporate fundamentals. Energy surged briefly amid escalating geopolitical tensions, but those gains proved short-lived. In recap, investors in the Canadian market faced slowing resource demand and a stalling domestic economy, which fueled increased interest in high-quality, high-dividend-paying companies. That is a trend we expect to continue going forward.

Bottom line: Markets remain heavily influenced by sentiment, with U.S. policy developments and ongoing tariff negotiations continuing to cause periodic volatility. However, there is little

evidence of deterioration in the hard data to date. As such, we continue to anchor our positioning on underlying data rather than market narratives. Looking ahead, the combination of a structurally higher-for-longer interest rate environment and increasingly pro-growth policy backdrop presents selective opportunities. In the U.S., this favours highquality growth stocks, particularly within Technology, where strong balance sheets and long-term thematic tailwinds remain intact. In Canada, Financials, especially the relatively inexpensive banks, present a more compelling opportunity as earlier tailwinds from pullforward demand are beginning to wane. While we remain constructive, we are mindful of elevated equity valuations and continue to closely monitor macro conditions and policy developments for signs of inflection.

Downloadable Copy

Mark Warywoda, CFA

VP, Public InvestmentsIan Whiteside, CFA, MBA

AVP, Public InvestmentsJohanna Shaw, CFA

Director, Public InvestmentsJin Li

Director, Equity Investments

Wanyi Chen, CFA, FRM

Sr. Quantitative Analyst

Andrew Vermeer, CFA

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Edward Ng Cheng Hi

Analyst, Credit

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

- [pdf] Daily/Guaranteed Interest Account Application - FHSA

-

New Dividend Scale effective July 1, 2021

The Equitable Life Insurance Company of Canada Board of Directors has approved a change to the dividend scale for the period July 1, 2021 to June 30, 2022.

- The dividend scale interest rate* will decrease from 6.2% to 6.05%.

- All series of participating whole life policies issued in the 2012 series and beyond other than the most recent Equimax Estate Builder® series will see an improvement in the mortality component. The most recent Equimax Estate Builder series, for sale as of September 12, 2020, already incorporated better mortality and its mortality component will remain unchanged. Series issued prior to 2012 will see an increase in the overall dividends but results will vary by series and policy.

- Other factors that are used to calculate the dividend scale will remain unchanged.

- The interest rate for dividends left on deposit will decrease from 2.75% to 2.25% for all participating whole life policies.

- The policy loan rate will remain unchanged at 6.2%. This applies to all new and existing policy loans, including automatic premium loans on Equimax® policies that have a 9-digit policy number beginning with a “3” or an “8”. The policy loan rates on some older blocks of policies may increase or decrease because they are tied to the prime interest rate.

*The dividend scale interest rate is not the same as the participating account rate of return in any given calendar year. The dividend scale interest rate smooths out the ups and downs experienced by the participating account.

Policyholder dividends in the next dividend scale year would be approximately $85 million, compared to $67 million in the prior dividend scale year.

The sustained low interest rate environment continues to put downward pressure on the experience in the participating account. If low interest rates continue, investment returns in the participating account will also be lower, and we may need to decrease the dividend scale in the future.

Your participating whole life clients will receive a notice of the dividend scale change with their annual policy statement. The Equitable Sales Illustrations system will be updated to reflect the new dividend scale. Updated illustration software will be available for download after 9 a.m. ET on June 25, 2021.

Find out more