Site Search

386 results for ZQU.XSXSK.COM order charlie white cocaine Wellington best market

- Sales Strategies

- Advisor Guide

-

EAMG market commentary

March 11, 2022

Since Russia first invaded the Ukraine, there’s been no shortage of headlines and commentaries trying to make sense of the situation. This is a tragedy that from a humanitarian standpoint that can’t be made sense of and our hearts go out to the people of Ukraine and those impacted. From a market standpoint, the common thinking is that geopolitical risks, aka war, historically haven’t been associated with significant corrections in the market. So far, the market reaction has been consistent with the historical experience, with the S&P 500 down only about 1% since the start of the conflict and the S&P/TSX Composite Index up close to 4%, despite the heightened daily volatility.

Given the obvious challenges of predicting how these types of conflicts play out, we look to financial market indicators to give us a better sense of the potential risks in the market. And in this respect, the most obvious indicator is oil. Since the start of the Russian invasion, oil has rallied roughly 18%, which is even more impressive considering it had already rallied 21% from the start of the year to the beginning of the conflict.

While we don’t know what will happen to energy markets over the coming weeks, we do know that oil shocks can result in higher inflation and sometimes lower growth. Inflation was already rising, although strategists generally viewed this as temporary on the expectation that the covid related supply chain disruptions and reopening pressures were the primary causes that would eventually self-correct. But as the Russian-Ukraine conflict intensifies, consensus views are moving towards inflation becoming more structural in nature. There are growing risks this will change consumer behaviour, causing inflation to be longer lasting than initially expected. Much of this has to do with the fact that as the world’s 3rd largest exporter of oil, Russia has taken a material amount of oil production capacity offline, resulting in significantly higher oil and gas prices. This also explains the significant outperformance of energy equities, and the broader S&P/TSX Composite Index vs US counterparts on a YTD basis.

While there are beneficiaries to higher oil prices, the consumer certainly isn’t one of them given gas prices reflect movements in the oil market. So far in 2022 prices paid at the pump have gone up 30%, one of the fastest paces on record. This, in addition to food price increases, will put strain on the consumer as higher bills divert dollars away from discretionary spending and potentially slow economic growth.

The other factor we’re closely watching is the overall health of the European economy, to which Russia supplies about 40% of Europe’s natural gas, 25% of their oil imports and 45% of their coal imports. While the European Commission has indicated plans to cuts their dependence on Russian energy well before 2030, the short-term impacts will be costly as Europe and other global markets see higher energy prices follow. As well, food prices will likely become an issue for the region given the interruption of supply out of the Black Sea which has driven grain and oilseed prices to levels not seen since 2008. Investors to date have priced in significant risk, evidenced by the performance of the Stoxx 50 which is down 17% YTD, one of the worst performing markets across the global universe.

While commodity prices are just one indicator, we are mindful that they could be telling us inflation may be more persistent than previously expected. From a long-term perspective this hasn’t changed our view of the equity market. As a result of potential near term impacts however, we have reduced our exposure to European markets in favour of the Canadian market and as well we have added inflation and risk hedges with sector allocations to energy, consumer staples and utilities, while still maintaining our overall long-term target levels to equities. There is no direct exposure to Russia in any of the three Equitable Life Active Balanced Portfolios which includes Equitable Life Active Balanced Growth Portfolio Select, Equitable Life Active Balanced Portfolio Select and Equitable Life Active Balanced Income Portfolio Select.

Downloadable CopyAny statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable Life of Canada® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

-

Wrapping up 2025 with our new term rates!

Among the most competitive in the market

Equitable® is wrapping up 2025 with our new term rates effective November 22, 2025. Many Canadians view life insurance as unaffordable, with 34% saying cost is the top reason they go without coverage.1 Our new term rates are designed to help address these concerns. They offer flexible and affordable options to help clients get the protection they need.

1 Investment Executive at Survey finds affordability, lack of trust, barriers to buying life insurance | Investment Executive

What’s New:

Updated premium rates for Term coverage, included on:• Term 10, Term 20 and Term 30/65 plans• Including Term Riders on Critical Illness (CI), Whole Life (WL), Equitable Generations® Universal Life (UL) and Equation Generation® IV Universal Life

View our Transition Rules for all the details on processing your applications.

New term rate highlights*:

*Effective November 22, 2025. Our term rates ranked among the best on LifeGuide when compared against top carriers in key markets.

Check out our new term rates for yourself. Run quotes monthly (versus annually) for our best term rates.

Contact your Equitable wholesaler today to learn more!

-

EAMG - Macro Tear Sheet – Recent Market Volatility Summary

By separating the noise from the signals, we believe the rotation away from the mega-cap technology names is likely to continue. Recent market volatility, triggered by a multitude of factors that include the unwind of the carry trade, investor reactions to mixed mega-cap earnings, and U.S. economic data, may present more investment opportunities for long-term outperformance. Recall over the past year that the majority of U.S. stock market performance came from a limited number of mega-cap technology companies and, in our view, moving forward it will be prudent to analyze the source of returns as rapid market rotations may punish overly-concentrated portfolios.

Inflation Slows (July 11) – Headline U.S. inflation readings increased 3.0% year-over-year in June, decelerating from May (3.3%). With prices slowing ahead of forecasts but economic growth remaining strong, investors became more confident regarding the prospects of an economic soft landing.

Outcome: market strength broadened with traders rotating out of highly concentrated areas of the market (“Fabulous 5”) and into more economically sensitive stocks that had been left behind.

• Big Tech Earnings (July 23 – Aug 1) – High profile mega-cap technology companies – including many members of the Magnificent 7 – reported earnings growth that generally surpassed expectations as margins remained healthy. That said, investors were more focused on spending towards AI-initiatives, rewarding businesses with greater success translating their AI investments into higher sales.

Outcome: this trend is evident through the divergence of returns from IBM and Alphabet (Google’s parent company) after releasing their quarterly earnings. The limited number of companies that contributed to the returns of the S&P 500 failed to impress investors, extending the rotation into other areas of the market.

• Caution is Brewing – Following a strong rally of economically sensitive pockets of the market, notably a breakout of returns from U.S. small cap companies, the low volatility factor, which tends to outperform during times of stress, moved in sync with the small caps’ strength.

Outcome: with a lack of fundamental justification supporting small cap performance, markets showed signs of caution.

• Central Bank Decisions (July 31)– The Federal Reserve held interest rates unchanged during its July meeting, in line with market expectations, reiterating committee members’ need for greater confidence that inflation would continue to subside. That said, policymakers signaled a reduction in policy rates could be a possibility in the coming meetings. In contrast, the Bank of Japan (BoJ) increased its key interest rate while also announcing plans to scale back bond purchases – restrictive monetary policy maneuvers aimed at backstopping the depreciating Japanese currency.

Outcome: the bifurcation between the BoJ and most other major central banks sparked a sharp appreciation of the yen and a rapid unwind of the yen carry trade (see below for explanation).

• Growth Scare (August 2)– In early August, a downside surprise in U.S. nonfarm payrolls (114k actual versus 175k expected) and an increase in the unemployment rate to 4.3%, higher than the 4.1% that was expected and up from 3.5% a year ago triggered concerns of a cooling labor market.

Outcome: speculation swelled surrounding the pace of rate cuts with market participants expecting the Federal Reserve to cut rates as much as 125bps over the next 3 policy meetings, up from 50-75bps as of the end of July. Against this backdrop, the ongoing unwind of the yen carry trade accelerated.

Yen Carry Trade Explained

• Simply put, investors have been borrowing Japanese yen – a low yielding currency – to invest in higher-yielding foreign assets. The primary risks in a carry trade can include the uncertainty of foreign exchange rates (if unhedged), as well as changes to expectations of the underlying yields, among other risks. Over the last 2 decades, the BoJ has implemented an ultra-low interest rate monetary policy to combat deflation and stimulate growth. Furthermore, investors were emboldened by the Japanese yen’s ~53% depreciation versus the U.S. dollar over the last 10 years. With the BoJ hiking its key interest rate while also announcing plans to scale back bond purchases, the yen rallied abruptly. Consequently, highly leveraged investors have had to exit their long positions in riskier assets to repay their borrowed yen exposure.

Peak Carry Trade Unwind – Buying Opportunity

• Peak carry trade unwind, which implies heightened panic levels, has historically created an attractive buying environment. That said, we are focused on companies that have demonstrated robust earnings growth and healthy leverage. Given the unprecedented level of market concentration over the last year, we view the unwind of the carry trade as another catalyst for investors to rotate out of the “Fabulous 5”.

Our Findings:

We found that the peak unwind of the carry trade may be a buying opportunity. At present, the current level of the unwind is similar to many notable market bottoms, including the Great Financial Crisis (2008), the European debt crisis (2010), the oil crash (2014), the subsequent emerging market crisis (2015), the Covid-19 crash (2020), and the collapse of Silicon Valley Bank (2023). We assessed the degree of the unwind by looking at the one-month implied volatility between three currency pairs, U.S. Dollar/Yen, Australian Dollar/Yen, and Euro/Yen. Implied volatility is a measure of the expected future volatility of the underlying assets over a given time period. Amid strong earnings growth and steady margins from quality businesses within the U.S. market, the fundamental backdrop suggests that businesses outside the concentrated AI-darlings may drive the next leg of market returns.

Downloadable Copy

Mark Warywoda, CFA

VP, Public Portfolio ManagementIan Whiteside, CFA, MBA

AVP, Public Portfolio ManagementJohanna Shaw, CFA

Director, Portfolio ManagementJin Li

Director, Equity Portfolio Management

Tyler Farrow, CFA

Senior Analyst, Equity

Andrew Vermeer

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy. -

EAMG Market Commentary January 2024

Rates & Credit – Interest rates decreased sharply in Q4 as the market priced in aggressive interest rate cuts by central banks in 2024. The prospect of lower interest rates also drove a strong risk-on tone to the market, with the risk premium on corporate bonds grinding tighter as prospects for a “soft landing” improved. The rally in interest rates resulted in the best quarter for bonds over the past 15 years, with the FTSE Canada Universe Index returning 8.3%. Corporate bonds modestly underperformed the Universe Index with a return of 7.3%. The lower return for corporate bonds was primarily driven by the fact that the corporate bond index is less sensitive to interest rate movements (as compared to the government index), partially offset by the risk-on tone to the market. Within corporate bonds, lower-rated BBBs outperformed higher-rated A bonds. Industries with higher interest rate exposure such as infrastructure, energy, and communications outperformed those with less exposure (notably financials and securitization), consistent with the overall shift in the yield curve.

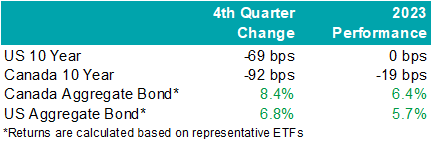

.png "image1-(1).png")

Santa Came to Town – Moving in sync with bonds, global equities jolted higher into the end of the year with cooling inflation data and dovish comments from central bankers. The U.S. market outperformed most regions last quarter with the S&P 500 returning 11.7% in USD terms, bringing the total return in 2023 to 26.3%. The TSX added 8.1% in Q4, boosting the total annual return to 11.8%. Meanwhile, major developed economies from Europe, Australasia, and the Far East (EAFE) gained 5.0% in local currency terms over the quarter, helping the region produce a 16.8% return from the year prior. Prospects of interest rate cuts by the Federal Reserve saw the Loonie rally into year-end and resultantly, investors of Canadian dollar securities witnessed enhanced returns. Strong domestic U.S. economic data helped value pockets of the market outperform. That said, this was not a synchronized trend as China’s economic disappointment weighed on the performance of EAFE.

U.S. Fundamentals – Our work shows that investors are shifting their focus away from operating margins and towards the ability to sustain debt levels ahead of renewing debt obligations. Corporate earnings beat modest expectations last quarter, contracting by less-than-expected on a year-over-year basis. Resilient operating margins continue to attract investors into equities. After three consecutive quarters of improving forward earnings guidance, we observed that the number of major companies expecting deteriorating financial performance grew to ~35%. We note that this is a sharp contrast relative to the optimistic run-up in equity valuations. In general, corporate pessimism has been underpinned by concerns for the health of the consumer, increasing wage pressures, and inflation.

U.S. Quant Factors – While mega-cap technology stocks gave back some ground in the second half, crowding into the magnificent 7 remains noticeable with the cap weighted S&P 500 outperforming the equal weighted index by 12.5% last year. That said, value areas of the market – which underperformed through the first three quarters of the year – were top performing companies last quarter as the prospects for an economic “soft-landing” improved with U.S. inflation continuing to ease without substantial deteriorations of employment or output data. Quality-growth businesses initially outperformed as the higher-for-longer narrative continued to drive investors toward large cash-rich companies with stable margins. That said, this basket of companies gave back relative returns into quarter-end as weakness in operating margins persisted, making fundamentals appear stretched. Low volatility stocks (i.e. stocks with lower sensitivity to broad market movement and lower price volatility) rallied to start the quarter before dovish comments from central bankers improved risk-sentiment and ultimately pushed this basket lower on a relative basis. Lastly, dividend growth companies, which include businesses with a lengthy and established history of increasing dividends, underperformed the broader index as market participants punished businesses that slowed capital growth projects during the rising interest rate environment. While operating margins have declined, the basket’s strong cash flow and low debt burden may be advantageous if the market’s anticipation of impending interest rate cuts proves to be incorrect or mistimed.

Canadian Fundamentals – Although Canadian companies exceeded bleak forecasts last quarter, earnings continue to contract on a year-over-year basis. Return on equity (ROE) – a gauge of how efficiently a corporation generates profits – continued to decline last quarter while corporate costs of capital remain elevated. In essence, Canadian companies are generating less value relative to their financing cost. Value creation underpins the sustainability of dividend payments, which are a unique and desirable attribute of the Canadian market. Meanwhile, the Bank of Canada held its overnight interest rate unchanged with market participants forecasting a higher probability of interest rate cuts in 2024. On the expectations of easing monetary conditions, dividend yields compressed while earnings forecasts improved with analysts predicting that index aggregate earnings will grow 6% to 8% in 2024. At a sector level, the energy industry’s financial performance normalized – in line with expectations – as weakening oil demand expectations overshadowed geopolitical conflict in the Middle East, ultimately pushing crude prices ~21% lower last quarter. The industrials and financials sectors beat expectations, helping offset softer-than-expected results from the consumer staples and technology sectors.

Canadian Quant Factors – The Canadian banks underperformed for most of the year as they reported increasing provisions for nonperforming loans, reflecting forecasts of worsening economic conditions. That said, expectations of interest rate cuts in 2024 helped tame recession fears and eased concerns of slowing loan growth, propelling banks higher in the fourth quarter as they appeared more stable and therefore favourable than prior estimates. The high-quality basket underperformed last quarter as improving risk sentiment in the market reduced the attractiveness of secure companies with lower earnings variability. Furthermore, high dividend payers with solid growth prospects outperformed in the fourth quarter as market participants rewarded companies that demonstrated a strong ability to support future dividends and punished high yielding businesses with less certain financial capabilities.

Views From the Frontline Rates – Interest rates declined sharply in Q4 as inflation continued to trend lower, fears of excess bond supply declined, and the Federal Open Market Committee signaled that the next change to their overnight policy interest rate would likely be lower. Labour market and consumer spending data remain resilient however businesses have indicated slowing across industries, more price-sensitive consumers, rising delinquencies, and concerns about the high cost of debt. Central banks remain committed to achieving their 2% inflation target and most acknowledge that interest rates have likely peaked.

Credit – The risk premium for corporate bonds (versus government bonds) tightened materially over the quarter, with a strong risk on tone to the market as investors priced in lower interest rates in 2024 and a “soft-landing” to economic concerns. Corporate bond supply was well received by the market. On the balance, we do not think the current risk premium adequately compensates for downside risk, and as such, we remain cautious on corporate bonds and have a bias towards higher-quality, shorter-dated credit where we view the risk / reward dynamic as being more favourable.

Equity – In the U.S., we allocated exposure to value names which outperformed over the quarter as the macroeconomic outlook improved on the backdrop of rate cut expectations. Looking forward, we expect that margins will continue to normalize as Covid-induced pent up demand fades. While we do not forecast margins to compress at an alarming rate, we believe sticky wage and input costs will continue to pressure businesses while consumers exhibit further exhaustion. As such, we are shifting our focus toward the balance between company reinvestment in capital projects and upcoming debt refinancing requirements. In line with this view, we favour businesses with stable cash flows and decreased debt loads as we believe they present an attractive contrarian opportunity if soft-landing projections prove to be overstated. Within Canada, we remain attentive to the inverse movements of ROE relative to financing costs over 2023. With the excess between ROE and financing costs compressing, businesses’ ability to create value appears more stretched than earlier in 2023. Therefore, we continue to favour high quality companies in Canada, which is typically defined by high ROE, stable earnings variability, and low financial leverage. Geographically, the U.S. economy appears to be in healthier condition with inflation easing while employment and output data remain stable and hence, our focus will be on capital expenditures. EAFE – which is generally more economically linked to China than North America – contains a large bucket of stable, high-quality businesses that may benefit from any upside economic surprises out of China. Lastly, through the lens of a Canadian investor, the Loonie’s relative value versus other major currencies presents another resource in our investment mandate to derive excess return.Downloadable Copy

Mark Warywoda, CFA

VP, Public Portfolio ManagementIan Whiteside, CFA, MBA

AVP, Public Portfolio ManagementJohanna Shaw, CFA

Director, Portfolio ManagementJin Li

Director, Equity Portfolio Management

Tyler Farrow, CFA

Senior Analyst, Equity

Andrew Vermeer

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

ADVISOR USE ONLY

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

-

Take emotions out of investing

Taking the emotion out of investing can be easier said then done. Most of us at one time or another have decided upon something strictly because of how we felt at the time, not because it was logical or made good financial sense. I am sure most of us have a good story to tell.

When it comes to financial planning, you always want to encourage your clients to be a rational investor and accept that market fluctuation is part of the investment journey. Over the last few months, even the hardiest rational investor has been challenged to accept the market fluctuations. History shows us that this too, shall pass and markets will rise once more. The biggest question asked is always, when?

While no one has a crystal ball with that answer, the best we can do is help our clients understand that when building portfolios, risk is always at the forefront of any good investment strategy. The level of risk is just one of the building blocks to constructing a financial portfolio that will see the client through good times and bad.

Need more help? Equitable Life has created an emotional investing brochure to help your clients manage through these extraordinary times. To download a copy, click here. We have also included a template letter that you can personalize and use to reach out to your clients. To download an editable copy, click here.

-

Equitable offers a fresh approach to guaranteed investing

Please take a few minutes to watch the video.

Equitable’s Daily Interest Account and Guaranteed Interest Accounts offer a fresh client-focused approach within a digital business solution.

Clients will appreciate:-

• Market leading1 interest rates with even higher rates available for larger deposits

-

• A full suite of available account types including the First Home Savings Account, and

-

• Options to invest up to age 952.

Advisors will value:-

Enhanced rate guarantees to secure the best rates available for clients,

-

An easy digital application process using Equitable’s EZcomplete® and,

-

A simplified product design to save you time.

Equitable® is committed to offering valuable guaranteed investment solutions in a competitive market. Our fresh approach to guaranteed investing makes Equitable’s Daily Interest Account or Guaranteed Interest Account an easy choice.Learn more about Equitable’s Daily and Guaranteed Interest Accounts

1 Equitable has made every effort to ensure accuracy of competitive information as of July 22, 2024. Accuracy is not guaranteed.

2 Some available term lengths may be limited starting at age 90.® or ™ denotes a trademark of The Equitable Life Insurance Company of Canada.

Posted July 22 -

-

Market Commentary April 2026

Key Takeaways

• Markets started 2026 constructively, with positive returns in both stock and bond markets in the first two months of the year. However, the war on Iran by the U.S. and Israel drove significant changes to markets in March. The biggest driver was the spike in oil prices. Oil prices increased over 70% during the quarter to over US$100 per barrel as 20% of global oil production became trapped in the Middle East when Iran closed the Strait of Hormuz.

• Canadian equities returned 3.9% in the first quarter, outperforming U.S. equities which lost -4.3%. The Canadian market benefitted from its 40% exposure to strong performing Energy, Materials and Utilities sectors, which each gained over 10% in Q1. Conversely, the U.S. market has much less exposure to those strong performing sectors and therefore fell as geopolitical tensions weighed on performance of most other sectors.

• Canadian bonds posted modest gains as early-quarter strength was largely offset by March weakness. Rising commodity prices reignited inflation fears and prompted speculation for central bank interest rate hikes. Credit spreads widened as concerns regarding defaults and liquidity in the private credit market intensified.

• The Bank of Canada and the U.S. Federal Reserve held policy rates unchanged during the first quarter. Both central banks maintained a wait-and-see approach amid slowing labour markets, persistent inflation risks, and heightened global uncertainty.

Economic and Market UpdateEconomic Summary: The U.S. economy continued to grow at a steady pace in the first quarter. Inflation remained above the Federal Reserve’s target. The labour market showed signs of cooling as hiring slowed, but the unemployment rate remained stable. However, higher energy prices and risks to global supply chains added near term inflation pressures and weighed on the global outlook. The Federal Reserve held its policy interest rate unchanged during the quarter, maintaining the target range at 3.50% to 3.75%. Chair Powell highlighted ongoing uncertainty and reiterated that the Federal Reserve is well positioned to adjust policy as economic conditions evolve.

In Canada, economic growth remained subdued in the first quarter as excess supply persisted, and the labour market softened. Inflation stayed close to the 2.0% target, though rising global energy prices increased short term inflation risks. Trade uncertainty continued to weigh on confidence and business activity. The Bank of Canada held its policy interest rate steady at 2.25% throughout the quarter. The Governing Council noted it stands ready to respond if the economic outlook shifts materially. Bond Markets: The Canada Aggregate Bond Index returned 0.23% in the first quarter. A strong start to the year in January and February (+2.25%) was mostly offset by a weak March (-1.97%), as higher oil prices from the war in Iran led to higher interest rates on Canadian bonds (bond prices fall as interest rates go up). The increase in interest rates was most predominant in shorter term bonds, with higher oil prices driving inflation fears. These inflation fears reframed the market’s interest rate cut expectations for 2026: a 40% chance of an interest cut by the Bank of Canada has now shifted to a 70% chance of not just one, but two 25 basis point increases to the Bank of Canada overnight rate in 2026. In addition, the war in Iran has resulted in a higher risk premium for corporate bonds: credit spreads (i.e. the extra yield on corporate bonds versus government bonds to compensate for their extra risk) moved higher in March after reaching record low levels in January and February. These higher credit spreads resulted in corporate bonds modestly underperforming the overall index, albeit still with positive returns. Despite the modest risk off tone, investors remain buyers of corporate bonds as evidenced by investors’ enthusiasm to support the primary issuance market. Corporate bond supply continues to set new records, with an impressive $50 billion in new issuance in the quarter, a record start to the year and 23% higher than the same period in 2025.

Bond Markets: The Canada Aggregate Bond Index returned 0.23% in the first quarter. A strong start to the year in January and February (+2.25%) was mostly offset by a weak March (-1.97%), as higher oil prices from the war in Iran led to higher interest rates on Canadian bonds (bond prices fall as interest rates go up). The increase in interest rates was most predominant in shorter term bonds, with higher oil prices driving inflation fears. These inflation fears reframed the market’s interest rate cut expectations for 2026: a 40% chance of an interest cut by the Bank of Canada has now shifted to a 70% chance of not just one, but two 25 basis point increases to the Bank of Canada overnight rate in 2026. In addition, the war in Iran has resulted in a higher risk premium for corporate bonds: credit spreads (i.e. the extra yield on corporate bonds versus government bonds to compensate for their extra risk) moved higher in March after reaching record low levels in January and February. These higher credit spreads resulted in corporate bonds modestly underperforming the overall index, albeit still with positive returns. Despite the modest risk off tone, investors remain buyers of corporate bonds as evidenced by investors’ enthusiasm to support the primary issuance market. Corporate bond supply continues to set new records, with an impressive $50 billion in new issuance in the quarter, a record start to the year and 23% higher than the same period in 2025.

Stock Markets: The first quarter of 2026 marked a period of heightened investor caution with geopolitical tensions rising. Equity markets remained under pressure in March, as dip buyers remained cautious. Early market volatility was driven by several geopolitical developments, including Japan’s snap election, events in Venezuela, and U.S. interest in Greenland. Private credit markets also came under pressure as liquidity tightened and default risks increased, particularly in semi-liquid lending structures. The war on Iran raised concerns around demand destruction and inflation, pushing oil prices above US$100 per barrel for the first time since 2022. Gold continued to rise strongly early in the quarter. However, it later recorded its sharpest decline in years, driven by central bank selling. Despite this pullback, gold finished the quarter up 8% and continues to be viewed as a key safe-haven asset.

Stock Markets: The first quarter of 2026 marked a period of heightened investor caution with geopolitical tensions rising. Equity markets remained under pressure in March, as dip buyers remained cautious. Early market volatility was driven by several geopolitical developments, including Japan’s snap election, events in Venezuela, and U.S. interest in Greenland. Private credit markets also came under pressure as liquidity tightened and default risks increased, particularly in semi-liquid lending structures. The war on Iran raised concerns around demand destruction and inflation, pushing oil prices above US$100 per barrel for the first time since 2022. Gold continued to rise strongly early in the quarter. However, it later recorded its sharpest decline in years, driven by central bank selling. Despite this pullback, gold finished the quarter up 8% and continues to be viewed as a key safe-haven asset.

U.S. Equities: U.S. equities entered the first quarter with strong momentum, supported by robust earnings growth from technology companies. While earnings results confirmed this strength, investor sentiment weakened, particularly toward Software-as-a-Service (SaaS) companies. Rapid progress in AI agents developed by firms such as Anthropic and Google highlighted how quickly generative AI could automate core SaaS functions. As a result, software stocks sold off sharply in February, triggering a broader rotation away from largecap growth. Furthermore, tighter financial conditions and rising geopolitical tensions reduced risk tolerance and drove sharp sector rotation. The Energy sector led market performance, while Technology lagged and Financials underperformed due to stress in credit markets.

Canadian Equities: The Canadian stock market was supported by its high exposure to commodities. That structural tilt helped Canadian equities outperform U.S. equities as macro narratives shifted toward inflation concerns and supply risks. Performance during the quarter was marked by a sharp whipsaw between gold and oil, reflecting shifting investor sentiment. Investors sold gold aggressively and scrambled to source U.S. dollars as financial conditions tightened. Conversely, oil prices rose sharply on Middle East supply disruptions, lifting Energy stocks to become the strongest-performing sector of the quarter, up 29%.

Bottom line: The first quarter showed how quickly geopolitical shocks can reshape sectors’ performance. Canada outperformed U.S. growth markets due to its higher exposure to commodities, as energy prices rose and inflation concerns returned. The sharp move in gold and oil prices highlighted the market’s sensitivity to macro developments. The war against Iran forced investors to reprice both inflation expectations and Federal Reserve policy expectations. Looking ahead, geopolitical stability, energy prices, and central bank policy are likely to remain key drivers of market performance and sector leadership.

Downloadable Copy

Mark Warywoda, CFA

VP, Public InvestmentsIan Whiteside, CFA, MBA

AVP, Public InvestmentsJohanna Shaw, CFA

Director, Public InvestmentsJin Li

Director, Equity Investments

Wanyi Chen, CFA, FRM

Sr. Quantitative Analyst

Andrew Vermeer, CFA

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Edward Ng Cheng Hin

Analyst, Credit

Kate (Huyen) Vinh

Analyst, Equity

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

Except for statements of historical fact, all statements in this document are forward-looking statements. These forward-looking statements represent the portfolio manager’s current best judgment as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may be materially different from what is expressed. Furthermore, the portfolio manager’s views, opinions, or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable assumes no obligation to update any forward-looking information contained in this document. The reader is cautioned to consider these and other factors carefully and to not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy. - Navigating the current market