Site Search

484 results for see portal PROBLEMGO.com hire someone to make false child abuse accusations

- [pdf] What's New July 6 2017

-

Tax impacts of the Canadian Dental Care Plan for your clients

Tax impacts of the Canadian Dental Care Plan for your clients*

Earlier this year, the government shared its progress on the Canadian Dental Care Plan (CDCP).

The CDCP will be available to Canadians with an annual family income of less than $90,000 who do not have dental benefits. Co-pays will be waived for eligible Canadians with a family income of less than $70,000.

Canadians who have access to private dental coverage are not eligible for the CDCP. This means that your clients must now report on T4s/T4As if dental coverage** was available on December 31 of the reporting tax year for:- Employees,

- Employees’ spouses and/or dependents,

- Former employees, and

- Spouses of deceased employees.

This new tax reporting requirement is mandatory starting with the 2023 tax year. Employee tax slips will include new boxes for employers to complete:- Box 45 (T4): Employer Offered Dental Benefits. This new box will be mandatory.

- Box 015 (T4A): Payer Offered Dental Benefits. This new box will be mandatory if plan sponsors report in Box 016, Pension or Superannuation. The box will otherwise be optional.

- Code 1: The plan member has no access to dental care insurance or coverage of dental services of any kind.

- Code 2: Only the plan member has access to any dental care insurance, or coverage of dental services of any kind.

- Code 3: The plan member, their spouse and their dependents have access to any dental care insurance, or coverage of dental services of any kind.

- Code 4: Only the plan member and their spouse have access to any dental care insurance, or coverage of dental services of any kind.

- Code 5: Only the plan member and their dependents have access to any dental care insurance, or coverage of dental services of any kind.

Reports for dependents

We have a report available for plan members who have enrolled their dependents in benefits coverage. Your clients can contact their local service team representative to receive a copy of the report. We are working to make it available on our Advisor and PA websites.

Questions

For guidance on your tax slips and reporting obligations, please encourage your clients to contact their accountant, payroll provider or tax advisor.

Supporting plan members affected by the Israeli-Palestinian conflict*

Traumatic events continue to unfold in the Middle East. Enduring ongoing news of conflict and suffering could challenge many Canadians. During this difficult time, Equitable encourages affected clients and plan members to access the mental health support they need.

Large-scale traumatic news events can cause people to experience intense reactions. This puts a lot of strain on their mental health. Having coping mechanisms to deal with the current crisis can be a huge help. Any Equitable Life plan member who needs mental health support can visit Homeweb.ca/equitable to access online resources or contact Homewood at 1.888.707.2115.

Support available to all Equitable plan members

Support available to plan members with the Homewood Health EFAP

For your clients that have purchased Homewood Health’s Employee and Family Assistance Program (EFAP), remind them that their plan members also have access to confidential counselling services. The EFAP provides plan members with 24/7 access to confidential counselling through a national network of mental health professionals. Whether it’s face-to-face, by phone, email, chat or video, plan members and their dependent family members will receive appropriate, timely support for the issue they’re dealing with.

Questions?

If you need more information, contact your Group Account Executive or myFlex account executive.

*Indicates content that will be shared with your clients. - [pdf] The Right Time To Buy And Sell

- [pdf] Policy summary premium error

- [pdf] Segregated Fund Sales DSC Disclosure Form

-

February 2020 Advisor eNews

In this issue:

Provincial biosimilar update

Legislative changes for Alberta’s Coverage for Seniors program

Coming soon: enhancements to Equitable EZClaim® Online

Provincial biosimilar update

Alberta Biosimilar Initiative

On December 12, 2019, the Alberta government introduced the launch of the Alberta Biosimilar Initiative. This program will require patients using several originator biologic drugs to switch to a biosimilar, and patients using a non-biologic complex drug (NBCD) to switch to its subsequent entry version before July 1, 2020 in order to maintain coverage.

Biologics are drugs that are engineered using living organisms like yeast and bacteria. The first version of a biologic developed is also known as the “originator” drug. Biosimilars are highly similar to the originator drug they are based on and have been shown to have no clinically meaningful differences in safety or efficacy.

Alberta Health will initially cover both the originator and biosimilar or subsequent entry version of a NBCD drug as patients start the switching process.

The following table outlines the affected originator drugs, their biosimilars or subsequent entry, and the conditions affected by the program.

Biosimilar Drug Originator Biosimilar/Subsequent Entry Indications Affected etanercept Enbrel Brenzys Ankylosing Spondylitis

Rheumatoid ArthritisErelzi Ankylosing Spondylitis

Psoriatic Arthritis

Rheumatoid Arthritisinfliximab Remicade Inflectra

RenflexisAnkylosing Spondylitis

Plaque Psoriasis

Psoriatic Arthritis

Rheumatoid Arthritis

Crohn’s Disease

Ulcerative Colitisinsulin glargine Lantus Basaglar Diabetes (Type 1 and 2) Filgrastim Neupogen Grastofil Neutropenia pegfilgrastim Neulasta Lapelga Neutropenia glatiramer* Copaxone Glatect Multiple Sclerosis *Glatiramer is a non-biologic complex drug where the originator is Copaxone and the subsequent entry is Glatect.

Equitable Life is actively investigating the benefit, risk and appropriate plan changes associated with this new policy on private drug plans and will keep you informed.

For more information about the Alberta Biosimilars Initiative, consult the Alberta government website.

British Columbia

In 2019, BC Pharmacare introduced a Biosimilars Policy that impacted coverage of three biologic drugs – Remicade, Enbrel and Lantus. As of November 25, 2019, these drugs were no longer eligible in BC for most conditions for which lower cost biosimilar versions are available. Patients in the province with these conditions were required to switch to biosimilar versions of these drugs in order to maintain their coverage.

The second phase of the BC Biosimilar Policy takes effect March 6, 2020 when Remicade will be delisted for Crohn’s Disease and Ulcerative Colitis. Patients in the province with these conditions will be required to switch to Inflectra or Renflexis in order to maintain their coverage.

Biosimilar Drug Originator Biosimilar Indications Affected infliximab Remicade Inflectra

RenflexisCrohn’s Disease

Ulcerative ColitisWe have communicated with the affected plan members, informing them of the need to switch medications. If plan members have any questions or concerns, our Customer Care team is here to help and support them through the transition.

If you have any questions about this policy, please contact your Group Account Executive or myFlex Sales Manager.

Ontario

In November 2019 Ontario Minister of Health Christine Elliot indicated that the government was planning to launch consultations to explore solutions in managing biologics.

Equitable Life will continue to monitor these developments and keep you informed of any impact on private drug plans.

Legislative changes for Alberta’s Coverage for Seniors program

The government of Alberta has announced that as of March 1, 2020, seniors’ family members (such as spouses and dependents) who are younger than 65 will no longer be covered by the provincial Coverage for Seniors program. Albertans 65 years of age and older will continue to be covered under the provincial plan.

Equitable Life plan members and their dependents will continue to be covered under the parameters of their group benefits plan.

For more information, please see the Alberta Seniors Health Benefits website.

Coming soon: enhancements to Equitable EZClaim® Online

Faster vision claims processing and payment

Equitable Life will soon provide real-time processing of vision claims submitted via EZClaim Online.

This means plan members will be able to find out the status of their vision claim almost instantaneously. And, for approved claims, they will receive payment even sooner – often in as little as 24 hours.

In order to allow for instantaneous processing and faster payment, plan members will be prompted to enter some additional information including the practitioner’s name, the date of the expense, the type of expense and amount of the expense when submitting their claims for these services.

Equitable Life plan members can submit all vision claims via EZClaim, including coordination of benefits and Health Care Spending Account claims.

This enhancement will be coming to our EZClaim Mobile app in the coming months.

New printable claims extract

As part of our ongoing efforts to improve customer experience for plan members, we will also offer a claims extract in a printable format within the plan member site. Plan members will be able to select a date range and claimant, then generate and download a detailed list of health and dental claims. This is a helpful way to keep track of claims, especially when reviewing them in preparation for income tax filing.

Once these enhancements are live you will be notified in an eNews, and an announcement will be posted on the plan member section of EquitableHealth.ca.

Elimination of Out-of-Country Travellers Program in Ontario

Effective January 1, 2020, the Ontario government eliminated OHIP coverage for emergency services for Ontarians travelling outside of Canada.

Previously, the Out-of-Country Travelers Program provided some reimbursement for services required to treat conditions that are acute, unexpected, arose outside Canada and require immediate treatment. The program covered between $200 and $400 per day for inpatient services and $50 per day for outpatient and doctor services.

For groups who have out-of-country coverage from Allianz, this change will not impact the cost to your plan members, or the process plan members follow in the event of an emergency while travelling.

Plan members should still call Allianz in the event of an out of country emergency. Allianz will deal with their claim as usual and will now pay for the portion of the claim previously paid by OHIP. Plan members will not have any additional out-of-pocket costs.

We will be sharing this information with plan members as a news item on our plan member website, equitablehealth.ca.

-

EAMG Market Commentary July 2024

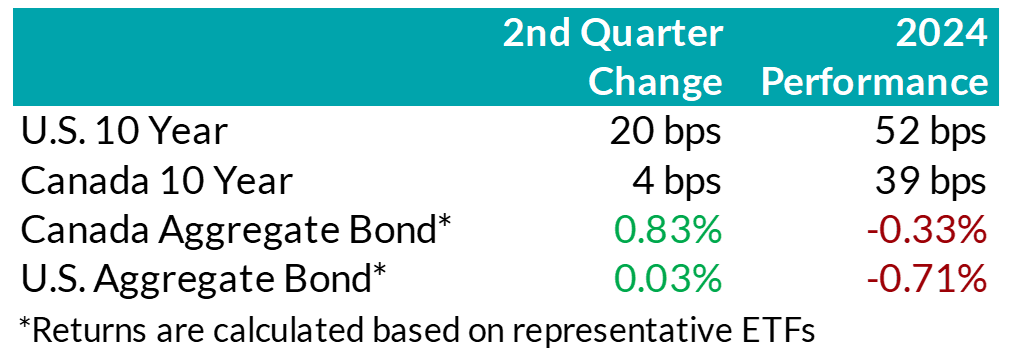

.png "Picture1-(3).png") Rates & Credit – In Q2 2024, U.S. inflation and economic growth data was mixed, leading to moderately higher interest rates in the U.S. Meanwhile, in Canada, long-end interest rates were little changed during the quarter, but short-term interest rates fell. That was due to the weaker economic outlook, as well as the Bank of Canada’s decision to reduce its overnight interest rate in June, with anticipation of further monetary policy easing to come. Canadian corporate bonds returned 1.1%, outperforming the 0.8% return of government bonds as well as the 0.9% return for the overall FTSE Canada Universe Bond index. Shorter-dated bonds outperformed longer-dated bonds. Within corporate bonds, lower-rated BBBs outperformed higher-rated A bonds, while industries that have shorter-dated debt (e.g. real estate and financials) outperformed those that tend to have longer-dated debt (e.g. communications and infrastructure).

Rates & Credit – In Q2 2024, U.S. inflation and economic growth data was mixed, leading to moderately higher interest rates in the U.S. Meanwhile, in Canada, long-end interest rates were little changed during the quarter, but short-term interest rates fell. That was due to the weaker economic outlook, as well as the Bank of Canada’s decision to reduce its overnight interest rate in June, with anticipation of further monetary policy easing to come. Canadian corporate bonds returned 1.1%, outperforming the 0.8% return of government bonds as well as the 0.9% return for the overall FTSE Canada Universe Bond index. Shorter-dated bonds outperformed longer-dated bonds. Within corporate bonds, lower-rated BBBs outperformed higher-rated A bonds, while industries that have shorter-dated debt (e.g. real estate and financials) outperformed those that tend to have longer-dated debt (e.g. communications and infrastructure).

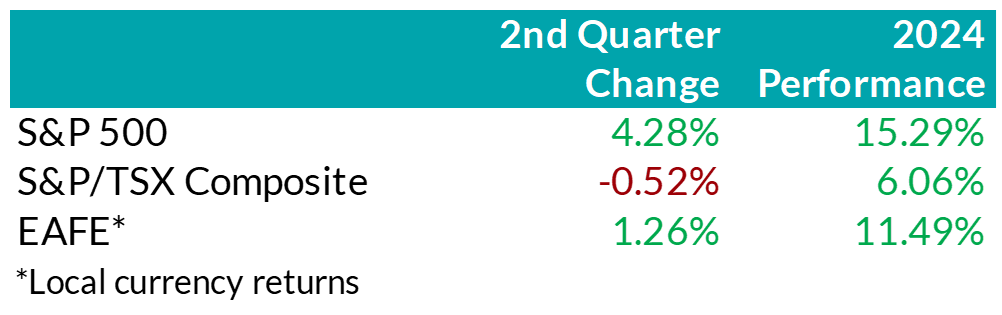

.png "Picture2-(2).png") Equity Overview – Against the backdrop of volatile inflation data and a lack of indication from the Federal Reserve that it was prepared to start cutting interest rates yet, U.S. equity markets decoupled from other regions. Crowding into AI-focused, mega-cap names accelerated in Q2. More specifically, investors defaulted toward the Magnificent 7 to navigate the current period, overlooking broadening earnings breadth and less expensive valuations from the remaining S&P 493. Outside the U.S., equity returns were generally mundane in dollar terms. That said, emerging markets proved to be a bright spot for investors seeking value, as the rebound in heavily discounted Chinese equities helped push frontier markets higher.

Equity Overview – Against the backdrop of volatile inflation data and a lack of indication from the Federal Reserve that it was prepared to start cutting interest rates yet, U.S. equity markets decoupled from other regions. Crowding into AI-focused, mega-cap names accelerated in Q2. More specifically, investors defaulted toward the Magnificent 7 to navigate the current period, overlooking broadening earnings breadth and less expensive valuations from the remaining S&P 493. Outside the U.S., equity returns were generally mundane in dollar terms. That said, emerging markets proved to be a bright spot for investors seeking value, as the rebound in heavily discounted Chinese equities helped push frontier markets higher.

U.S. Fundamentals – Corporate earnings continued to surpass expectations last quarter with stable operating margins helping businesses report better-than-expected bottom line results. Investors remain focused on the ability of companies to sustain debt levels ahead of renewing debt obligations, rewarding businesses with a strong ability to generate stable cash flows. Moreover, while prior quarters have witnessed earnings growth that was largely driven by highly profitable mega-cap technology stocks, U.S. markets are witnessing a broadening trend in earnings strength, with previously stunted segments of the market recovering. Our work shows that members of the Russell 1000 index, excluding the Magnificent 7, posted a median earnings growth of about 6% last quarter, with nearly 60% of companies increasing earnings versus the year prior. Furthermore, we observed an increase in the number of major companies that expect improving financial performance to approximately 27%, suggesting that the recovery in earnings breadth may persist.

U.S. Quant Factors – As mentioned, concentration in the equity market drove a surge in valuations as investors continued to chase specific mega-cap technology stocks. In fact, within the Russell 1000 growth factor – which screens for companies whose earnings are expected to grow at an above-average rate relative to the market – the Magnificent 7 totaled nearly 55% of the entire index by quarter-end. In addition, the Nasdaq 100 – which is generally viewed as a technology-biased index – saw the weight of the Magnificent 7 rise to almost 43% of the entire index by the end of the quarter. Furthermore, the equal-weighted S&P 500 underperformed the cap-weighted index by nearly 7% last quarter, bringing the year-to-date divergence to about 10%. With concentration accelerating, the cap-weighted index outperformance has soared past Covid-era levels, a period that saw investors rapidly crowd into profitable technology names due to panic and economic uncertainty. We remain cautious of a severely crowded market that trades near all-time highs as strong performance from 5-7 names distorts the overall stature of market conditions.

Canadian Fundamentals – Although Canadian companies exceeded bleak forecasts, earnings continue to contract on a year-over-year basis. Furthermore, earnings revisions have grinded lower with easing monetary conditions unable to offset concerns of a slowing economic environment. We note the sharp contrast versus the U.S. as the bifurcation of earnings performance widens. The CRB Raw Industrials Index, a measure of price changes of basic commodities, broke out of recent ranges as metals rallied higher despite a stronger U.S. dollar and elevated interest rates. The mining industry benefited from a sustained elevation in prices, helping the materials sector outperform over the quarter. Returns from the heavily-weighted Canadian banks were constrained last quarter with company-specific drivers – including regulatory challenges from TD, and underwhelming U.S. results from BMO – limiting performance. More broadly, the banks continue to build prudent credit provisions to mitigate uncertain economic forecasts and remain well capitalized.

Canadian Quant Factors – With investors remaining attentive to businesses’ ability to create value relative to financing costs, we see value in high quality, dividend-paying companies with strong earnings sustainability and a healthy degree of leverage. Based on our work, investors of the Canadian banks appear well compensated, with the current premium between value creation and current yield remaining compressed. In our opinion, the market has modest expectations regarding prospects for value generation from the banks and, therefore, we believe the industry stands to benefit if the premium reverts closer to historical norms. We also continue to see sources of quality dividend opportunities within certain areas of the energy sector. More specifically, we believe companies that have taken steps to improve their balance sheets through deleveraging efforts, and with improved operating leverage, offer attractive prospects given their stable and high-yielding composition.

Views From the Frontline

Rates – During the first half of the second quarter, interest rates in both Canada and the U.S. increased, continuing the upward momentum from Q1. Higher-than-expected inflation data in the U.S. along with mixed economic growth data caused investors to push out expectations for when the U.S. Federal Reserve would start lowering its interest rate. This trend shifted in the second half of Q2, as positive economic momentum slowed in the U.S. economy and inflation data began to soften. Interest rates in Canada declined more rapidly than in the U.S. due to more benign inflation, a weaker job market, and economic growth remaining below population growth. This economic weakening provided the confidence required for the Bank of Canada to cut rates by 25 basis points in June to 4.75%. The Bank also signaled that if inflation continues to ease and the Bank’s confidence grows that inflation would continue to trend toward its 2% inflation target, it is reasonable to expect further cuts. The second quarter marked a pivotal point for the global policy easing cycle. Sweden, Canada, and the European Central Bank all began lowering their policy rates, and Switzerland made a second rate cut, following one in Q1. The market continues to speculate on the timing of the U.S. Federal Reserve’s first rate cut. Interest rate cut expectations are largely unchanged in Canada since last quarter, with a total of three rate cuts expected throughout 2024. Expectations for the rate cuts by the U.S. Federal Reserve declined slightly, however, to two cuts in 2024.

Credit – The risk premium for corporate bonds (versus government bonds) was largely flat over the quarter, with spreads approaching the tight post-pandemic levels experienced in 2021. Corporate bond supply continues to be very robust, with $41bn in new issuance. Year-to-date, corporate issuance has set a new record, with an impressive $80bn in issuance. On balance, we do not think the current risk premium adequately compensates for downside risk, particularly in longer-dated corporate bonds, and have a bias towards shorter-dated credit where we view the risk / reward trade-off as being more favourable.

Equity – On the backdrop of a heavily concentrated U.S. market rally, we remain cautious of the distortion to market returns from high-flying technology stocks. As a result, we continue to favour a combination of the Dow Jones Industrial Average and the S&P 500 for our broad U.S. market exposure. The Dow provides a more diversified exposure to 30 prominent large-cap companies and less concentration in technology relative to the S&P. Broadening earnings strength presents an opportunity for previously out-of-favour names to “catch-up”. In our view, companies outside the Magnificent 7 that have demonstrated robust earnings growth, strong cash flow generation, along with decreased debt loads, are well-positioned to benefit from internal market rotations. As such, we gain exposure to these companies through the quality factor – companies with higher return-on-equity, strong operating performance, and healthy leverage levels – and the dividend growth factor – businesses with a lengthy and established history of increasing dividends.

In Canada, we remain attentive to how efficiently corporations are generating profits relative to financing costs. Looking forward, we continue to monitor the ability of businesses to generate profits given a decline in capital spending. More specifically, we are focused on businesses’ ability to grow and sustain dividends amid the lag between easing monetary conditions and consumption. Due to this, we observe value in higher yielding companies that are higher on the spectrum of quality. Geographically, we maintain our overweight U.S. exposure, underpinned by encouraging U.S. inflation data trends, broadening corporate earnings growth, and normalizing consumption. In addition, sluggish Chinese data and the lack of positive earnings revisions from EAFE tilt the risk-adjusted return profile in favour of the U.S. Lastly, as a Canadian investor, fluctuations in the Loonie’s relative value versus other major currencies continues to present tactical trading opportunities within our investment mandate.

Downloadable Copy

Mark Warywoda, CFA

VP, Public Portfolio ManagementIan Whiteside, CFA, MBA

AVP, Public Portfolio ManagementJohanna Shaw, CFA

Director, Portfolio ManagementJin Li

Director, Equity Portfolio Management

Tyler Farrow, CFA

Senior Analyst, Equity

Andrew Vermeer

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

-

EAMG - Macro Tear Sheet – Recent Market Volatility Summary

By separating the noise from the signals, we believe the rotation away from the mega-cap technology names is likely to continue. Recent market volatility, triggered by a multitude of factors that include the unwind of the carry trade, investor reactions to mixed mega-cap earnings, and U.S. economic data, may present more investment opportunities for long-term outperformance. Recall over the past year that the majority of U.S. stock market performance came from a limited number of mega-cap technology companies and, in our view, moving forward it will be prudent to analyze the source of returns as rapid market rotations may punish overly-concentrated portfolios.

Inflation Slows (July 11) – Headline U.S. inflation readings increased 3.0% year-over-year in June, decelerating from May (3.3%). With prices slowing ahead of forecasts but economic growth remaining strong, investors became more confident regarding the prospects of an economic soft landing.

Outcome: market strength broadened with traders rotating out of highly concentrated areas of the market (“Fabulous 5”) and into more economically sensitive stocks that had been left behind.

• Big Tech Earnings (July 23 – Aug 1) – High profile mega-cap technology companies – including many members of the Magnificent 7 – reported earnings growth that generally surpassed expectations as margins remained healthy. That said, investors were more focused on spending towards AI-initiatives, rewarding businesses with greater success translating their AI investments into higher sales.

Outcome: this trend is evident through the divergence of returns from IBM and Alphabet (Google’s parent company) after releasing their quarterly earnings. The limited number of companies that contributed to the returns of the S&P 500 failed to impress investors, extending the rotation into other areas of the market.

• Caution is Brewing – Following a strong rally of economically sensitive pockets of the market, notably a breakout of returns from U.S. small cap companies, the low volatility factor, which tends to outperform during times of stress, moved in sync with the small caps’ strength.

Outcome: with a lack of fundamental justification supporting small cap performance, markets showed signs of caution.

• Central Bank Decisions (July 31)– The Federal Reserve held interest rates unchanged during its July meeting, in line with market expectations, reiterating committee members’ need for greater confidence that inflation would continue to subside. That said, policymakers signaled a reduction in policy rates could be a possibility in the coming meetings. In contrast, the Bank of Japan (BoJ) increased its key interest rate while also announcing plans to scale back bond purchases – restrictive monetary policy maneuvers aimed at backstopping the depreciating Japanese currency.

Outcome: the bifurcation between the BoJ and most other major central banks sparked a sharp appreciation of the yen and a rapid unwind of the yen carry trade (see below for explanation).

• Growth Scare (August 2)– In early August, a downside surprise in U.S. nonfarm payrolls (114k actual versus 175k expected) and an increase in the unemployment rate to 4.3%, higher than the 4.1% that was expected and up from 3.5% a year ago triggered concerns of a cooling labor market.

Outcome: speculation swelled surrounding the pace of rate cuts with market participants expecting the Federal Reserve to cut rates as much as 125bps over the next 3 policy meetings, up from 50-75bps as of the end of July. Against this backdrop, the ongoing unwind of the yen carry trade accelerated.

Yen Carry Trade Explained

• Simply put, investors have been borrowing Japanese yen – a low yielding currency – to invest in higher-yielding foreign assets. The primary risks in a carry trade can include the uncertainty of foreign exchange rates (if unhedged), as well as changes to expectations of the underlying yields, among other risks. Over the last 2 decades, the BoJ has implemented an ultra-low interest rate monetary policy to combat deflation and stimulate growth. Furthermore, investors were emboldened by the Japanese yen’s ~53% depreciation versus the U.S. dollar over the last 10 years. With the BoJ hiking its key interest rate while also announcing plans to scale back bond purchases, the yen rallied abruptly. Consequently, highly leveraged investors have had to exit their long positions in riskier assets to repay their borrowed yen exposure.

Peak Carry Trade Unwind – Buying Opportunity

• Peak carry trade unwind, which implies heightened panic levels, has historically created an attractive buying environment. That said, we are focused on companies that have demonstrated robust earnings growth and healthy leverage. Given the unprecedented level of market concentration over the last year, we view the unwind of the carry trade as another catalyst for investors to rotate out of the “Fabulous 5”.

Our Findings:

We found that the peak unwind of the carry trade may be a buying opportunity. At present, the current level of the unwind is similar to many notable market bottoms, including the Great Financial Crisis (2008), the European debt crisis (2010), the oil crash (2014), the subsequent emerging market crisis (2015), the Covid-19 crash (2020), and the collapse of Silicon Valley Bank (2023). We assessed the degree of the unwind by looking at the one-month implied volatility between three currency pairs, U.S. Dollar/Yen, Australian Dollar/Yen, and Euro/Yen. Implied volatility is a measure of the expected future volatility of the underlying assets over a given time period. Amid strong earnings growth and steady margins from quality businesses within the U.S. market, the fundamental backdrop suggests that businesses outside the concentrated AI-darlings may drive the next leg of market returns.

Downloadable Copy

Mark Warywoda, CFA

VP, Public Portfolio ManagementIan Whiteside, CFA, MBA

AVP, Public Portfolio ManagementJohanna Shaw, CFA

Director, Portfolio ManagementJin Li

Director, Equity Portfolio Management

Tyler Farrow, CFA

Senior Analyst, Equity

Andrew Vermeer

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy. -

Market Commentary April 2026

Key Takeaways

• Markets started 2026 constructively, with positive returns in both stock and bond markets in the first two months of the year. However, the war on Iran by the U.S. and Israel drove significant changes to markets in March. The biggest driver was the spike in oil prices. Oil prices increased over 70% during the quarter to over US$100 per barrel as 20% of global oil production became trapped in the Middle East when Iran closed the Strait of Hormuz.

• Canadian equities returned 3.9% in the first quarter, outperforming U.S. equities which lost -4.3%. The Canadian market benefitted from its 40% exposure to strong performing Energy, Materials and Utilities sectors, which each gained over 10% in Q1. Conversely, the U.S. market has much less exposure to those strong performing sectors and therefore fell as geopolitical tensions weighed on performance of most other sectors.

• Canadian bonds posted modest gains as early-quarter strength was largely offset by March weakness. Rising commodity prices reignited inflation fears and prompted speculation for central bank interest rate hikes. Credit spreads widened as concerns regarding defaults and liquidity in the private credit market intensified.

• The Bank of Canada and the U.S. Federal Reserve held policy rates unchanged during the first quarter. Both central banks maintained a wait-and-see approach amid slowing labour markets, persistent inflation risks, and heightened global uncertainty.

Economic and Market UpdateEconomic Summary: The U.S. economy continued to grow at a steady pace in the first quarter. Inflation remained above the Federal Reserve’s target. The labour market showed signs of cooling as hiring slowed, but the unemployment rate remained stable. However, higher energy prices and risks to global supply chains added near term inflation pressures and weighed on the global outlook. The Federal Reserve held its policy interest rate unchanged during the quarter, maintaining the target range at 3.50% to 3.75%. Chair Powell highlighted ongoing uncertainty and reiterated that the Federal Reserve is well positioned to adjust policy as economic conditions evolve.

In Canada, economic growth remained subdued in the first quarter as excess supply persisted, and the labour market softened. Inflation stayed close to the 2.0% target, though rising global energy prices increased short term inflation risks. Trade uncertainty continued to weigh on confidence and business activity. The Bank of Canada held its policy interest rate steady at 2.25% throughout the quarter. The Governing Council noted it stands ready to respond if the economic outlook shifts materially. Bond Markets: The Canada Aggregate Bond Index returned 0.23% in the first quarter. A strong start to the year in January and February (+2.25%) was mostly offset by a weak March (-1.97%), as higher oil prices from the war in Iran led to higher interest rates on Canadian bonds (bond prices fall as interest rates go up). The increase in interest rates was most predominant in shorter term bonds, with higher oil prices driving inflation fears. These inflation fears reframed the market’s interest rate cut expectations for 2026: a 40% chance of an interest cut by the Bank of Canada has now shifted to a 70% chance of not just one, but two 25 basis point increases to the Bank of Canada overnight rate in 2026. In addition, the war in Iran has resulted in a higher risk premium for corporate bonds: credit spreads (i.e. the extra yield on corporate bonds versus government bonds to compensate for their extra risk) moved higher in March after reaching record low levels in January and February. These higher credit spreads resulted in corporate bonds modestly underperforming the overall index, albeit still with positive returns. Despite the modest risk off tone, investors remain buyers of corporate bonds as evidenced by investors’ enthusiasm to support the primary issuance market. Corporate bond supply continues to set new records, with an impressive $50 billion in new issuance in the quarter, a record start to the year and 23% higher than the same period in 2025.

Bond Markets: The Canada Aggregate Bond Index returned 0.23% in the first quarter. A strong start to the year in January and February (+2.25%) was mostly offset by a weak March (-1.97%), as higher oil prices from the war in Iran led to higher interest rates on Canadian bonds (bond prices fall as interest rates go up). The increase in interest rates was most predominant in shorter term bonds, with higher oil prices driving inflation fears. These inflation fears reframed the market’s interest rate cut expectations for 2026: a 40% chance of an interest cut by the Bank of Canada has now shifted to a 70% chance of not just one, but two 25 basis point increases to the Bank of Canada overnight rate in 2026. In addition, the war in Iran has resulted in a higher risk premium for corporate bonds: credit spreads (i.e. the extra yield on corporate bonds versus government bonds to compensate for their extra risk) moved higher in March after reaching record low levels in January and February. These higher credit spreads resulted in corporate bonds modestly underperforming the overall index, albeit still with positive returns. Despite the modest risk off tone, investors remain buyers of corporate bonds as evidenced by investors’ enthusiasm to support the primary issuance market. Corporate bond supply continues to set new records, with an impressive $50 billion in new issuance in the quarter, a record start to the year and 23% higher than the same period in 2025.

Stock Markets: The first quarter of 2026 marked a period of heightened investor caution with geopolitical tensions rising. Equity markets remained under pressure in March, as dip buyers remained cautious. Early market volatility was driven by several geopolitical developments, including Japan’s snap election, events in Venezuela, and U.S. interest in Greenland. Private credit markets also came under pressure as liquidity tightened and default risks increased, particularly in semi-liquid lending structures. The war on Iran raised concerns around demand destruction and inflation, pushing oil prices above US$100 per barrel for the first time since 2022. Gold continued to rise strongly early in the quarter. However, it later recorded its sharpest decline in years, driven by central bank selling. Despite this pullback, gold finished the quarter up 8% and continues to be viewed as a key safe-haven asset.

Stock Markets: The first quarter of 2026 marked a period of heightened investor caution with geopolitical tensions rising. Equity markets remained under pressure in March, as dip buyers remained cautious. Early market volatility was driven by several geopolitical developments, including Japan’s snap election, events in Venezuela, and U.S. interest in Greenland. Private credit markets also came under pressure as liquidity tightened and default risks increased, particularly in semi-liquid lending structures. The war on Iran raised concerns around demand destruction and inflation, pushing oil prices above US$100 per barrel for the first time since 2022. Gold continued to rise strongly early in the quarter. However, it later recorded its sharpest decline in years, driven by central bank selling. Despite this pullback, gold finished the quarter up 8% and continues to be viewed as a key safe-haven asset.

U.S. Equities: U.S. equities entered the first quarter with strong momentum, supported by robust earnings growth from technology companies. While earnings results confirmed this strength, investor sentiment weakened, particularly toward Software-as-a-Service (SaaS) companies. Rapid progress in AI agents developed by firms such as Anthropic and Google highlighted how quickly generative AI could automate core SaaS functions. As a result, software stocks sold off sharply in February, triggering a broader rotation away from largecap growth. Furthermore, tighter financial conditions and rising geopolitical tensions reduced risk tolerance and drove sharp sector rotation. The Energy sector led market performance, while Technology lagged and Financials underperformed due to stress in credit markets.

Canadian Equities: The Canadian stock market was supported by its high exposure to commodities. That structural tilt helped Canadian equities outperform U.S. equities as macro narratives shifted toward inflation concerns and supply risks. Performance during the quarter was marked by a sharp whipsaw between gold and oil, reflecting shifting investor sentiment. Investors sold gold aggressively and scrambled to source U.S. dollars as financial conditions tightened. Conversely, oil prices rose sharply on Middle East supply disruptions, lifting Energy stocks to become the strongest-performing sector of the quarter, up 29%.

Bottom line: The first quarter showed how quickly geopolitical shocks can reshape sectors’ performance. Canada outperformed U.S. growth markets due to its higher exposure to commodities, as energy prices rose and inflation concerns returned. The sharp move in gold and oil prices highlighted the market’s sensitivity to macro developments. The war against Iran forced investors to reprice both inflation expectations and Federal Reserve policy expectations. Looking ahead, geopolitical stability, energy prices, and central bank policy are likely to remain key drivers of market performance and sector leadership.

Downloadable Copy

Mark Warywoda, CFA

VP, Public InvestmentsIan Whiteside, CFA, MBA

AVP, Public InvestmentsJohanna Shaw, CFA

Director, Public InvestmentsJin Li

Director, Equity Investments

Wanyi Chen, CFA, FRM

Sr. Quantitative Analyst

Andrew Vermeer, CFA

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Edward Ng Cheng Hin

Analyst, Credit

Kate (Huyen) Vinh

Analyst, Equity

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

Except for statements of historical fact, all statements in this document are forward-looking statements. These forward-looking statements represent the portfolio manager’s current best judgment as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may be materially different from what is expressed. Furthermore, the portfolio manager’s views, opinions, or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable assumes no obligation to update any forward-looking information contained in this document. The reader is cautioned to consider these and other factors carefully and to not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.