Site Search

85 results for dividend scale

-

The Equimax EVOLUTION Continues

Earlier this year, we announced a host of improvements to our Equimax® Participating Whole Life solution, designed to add value, flexibility, and affordability to an already excellent plan.

Today we’re pleased to announce the following additional updates took effect on August 12th, 2023:

1. Targeted improvements in rates, death benefits, and cash values for Equimax Estate Builder and Equimax Wealth Accumulator plans.

2. New joint last to die rates for the Wealth Accumulator plans to align with Estate Builder.

3. A new “rated age” calculation, and

4. New rates for determining the maximum enhancement amount with the Enhanced Protection dividend option.

Visit our splash page and watch our informative video to learn more and start selling the enhanced Equimax today.

.png "English-(1).png")

.png "French-(1).png")

.png "Chinese-(1).png")

Refer to our Transition Rules for all the details on processing your applications.

Our illustration tools are updated:

● New Web-based illustration software on secure EquiNet® (log in required)

● New Desktop illustration software

● New EZstart™ on EquiNet

Need more information?

For information on these changes, please contact your Equitable Life wholesaler.

® and TM denote trademarks of The Equitable Life Insurance Company of Canada. -

Product updates - See our latest!

Good news! The updates to Equitable’s individual insurance solutions, scheduled for October 5th, 2024, as announced last week, are now in effect!

What’s new in this product update?

1. A new premium rate band for Equimax® policies with $5 Million and more of basic life insurance coverage.2. A new illustration for switches from Paid-up Additions (PUA) to the Cash dividend option when premium offset is selected.3. A new way to calculate commission on Equimax life insurance, Term life insurance, and EquiLiving® critical illness insurance plans when clients choose monthly payments.4. A new life Evidence of Insurability Schedule (Form #1343)

…and there’s more!

Visit our new splash page for a complete summary of the product changes, our latest video, and links to our sales tools and important resources:

*Video available in English with French and Chinese sub-titles

Please refer to our Transition Rules for all the details on processing your applications.

Need more information? Please contact your Equitable wholesaler.

® or TM denote trademarks of The Equitable Life Insurance Company of Canada. - Product at a glance

- Franklin Templeton

- [pdf] Large case insurance solutions

-

EAMG - Macro Tear Sheet – Recent Market Volatility Summary

By separating the noise from the signals, we believe the rotation away from the mega-cap technology names is likely to continue. Recent market volatility, triggered by a multitude of factors that include the unwind of the carry trade, investor reactions to mixed mega-cap earnings, and U.S. economic data, may present more investment opportunities for long-term outperformance. Recall over the past year that the majority of U.S. stock market performance came from a limited number of mega-cap technology companies and, in our view, moving forward it will be prudent to analyze the source of returns as rapid market rotations may punish overly-concentrated portfolios.

Inflation Slows (July 11) – Headline U.S. inflation readings increased 3.0% year-over-year in June, decelerating from May (3.3%). With prices slowing ahead of forecasts but economic growth remaining strong, investors became more confident regarding the prospects of an economic soft landing.

Outcome: market strength broadened with traders rotating out of highly concentrated areas of the market (“Fabulous 5”) and into more economically sensitive stocks that had been left behind.

• Big Tech Earnings (July 23 – Aug 1) – High profile mega-cap technology companies – including many members of the Magnificent 7 – reported earnings growth that generally surpassed expectations as margins remained healthy. That said, investors were more focused on spending towards AI-initiatives, rewarding businesses with greater success translating their AI investments into higher sales.

Outcome: this trend is evident through the divergence of returns from IBM and Alphabet (Google’s parent company) after releasing their quarterly earnings. The limited number of companies that contributed to the returns of the S&P 500 failed to impress investors, extending the rotation into other areas of the market.

• Caution is Brewing – Following a strong rally of economically sensitive pockets of the market, notably a breakout of returns from U.S. small cap companies, the low volatility factor, which tends to outperform during times of stress, moved in sync with the small caps’ strength.

Outcome: with a lack of fundamental justification supporting small cap performance, markets showed signs of caution.

• Central Bank Decisions (July 31)– The Federal Reserve held interest rates unchanged during its July meeting, in line with market expectations, reiterating committee members’ need for greater confidence that inflation would continue to subside. That said, policymakers signaled a reduction in policy rates could be a possibility in the coming meetings. In contrast, the Bank of Japan (BoJ) increased its key interest rate while also announcing plans to scale back bond purchases – restrictive monetary policy maneuvers aimed at backstopping the depreciating Japanese currency.

Outcome: the bifurcation between the BoJ and most other major central banks sparked a sharp appreciation of the yen and a rapid unwind of the yen carry trade (see below for explanation).

• Growth Scare (August 2)– In early August, a downside surprise in U.S. nonfarm payrolls (114k actual versus 175k expected) and an increase in the unemployment rate to 4.3%, higher than the 4.1% that was expected and up from 3.5% a year ago triggered concerns of a cooling labor market.

Outcome: speculation swelled surrounding the pace of rate cuts with market participants expecting the Federal Reserve to cut rates as much as 125bps over the next 3 policy meetings, up from 50-75bps as of the end of July. Against this backdrop, the ongoing unwind of the yen carry trade accelerated.

Yen Carry Trade Explained

• Simply put, investors have been borrowing Japanese yen – a low yielding currency – to invest in higher-yielding foreign assets. The primary risks in a carry trade can include the uncertainty of foreign exchange rates (if unhedged), as well as changes to expectations of the underlying yields, among other risks. Over the last 2 decades, the BoJ has implemented an ultra-low interest rate monetary policy to combat deflation and stimulate growth. Furthermore, investors were emboldened by the Japanese yen’s ~53% depreciation versus the U.S. dollar over the last 10 years. With the BoJ hiking its key interest rate while also announcing plans to scale back bond purchases, the yen rallied abruptly. Consequently, highly leveraged investors have had to exit their long positions in riskier assets to repay their borrowed yen exposure.

Peak Carry Trade Unwind – Buying Opportunity

• Peak carry trade unwind, which implies heightened panic levels, has historically created an attractive buying environment. That said, we are focused on companies that have demonstrated robust earnings growth and healthy leverage. Given the unprecedented level of market concentration over the last year, we view the unwind of the carry trade as another catalyst for investors to rotate out of the “Fabulous 5”.

Our Findings:

We found that the peak unwind of the carry trade may be a buying opportunity. At present, the current level of the unwind is similar to many notable market bottoms, including the Great Financial Crisis (2008), the European debt crisis (2010), the oil crash (2014), the subsequent emerging market crisis (2015), the Covid-19 crash (2020), and the collapse of Silicon Valley Bank (2023). We assessed the degree of the unwind by looking at the one-month implied volatility between three currency pairs, U.S. Dollar/Yen, Australian Dollar/Yen, and Euro/Yen. Implied volatility is a measure of the expected future volatility of the underlying assets over a given time period. Amid strong earnings growth and steady margins from quality businesses within the U.S. market, the fundamental backdrop suggests that businesses outside the concentrated AI-darlings may drive the next leg of market returns.

Downloadable Copy

Mark Warywoda, CFA

VP, Public Portfolio ManagementIan Whiteside, CFA, MBA

AVP, Public Portfolio ManagementJohanna Shaw, CFA

Director, Portfolio ManagementJin Li

Director, Equity Portfolio Management

Tyler Farrow, CFA

Senior Analyst, Equity

Andrew Vermeer

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy. - Give the Gift of a Head Start

- Fidelity Investments Canada

-

EAMG Market Commentary April 2024

April 2024

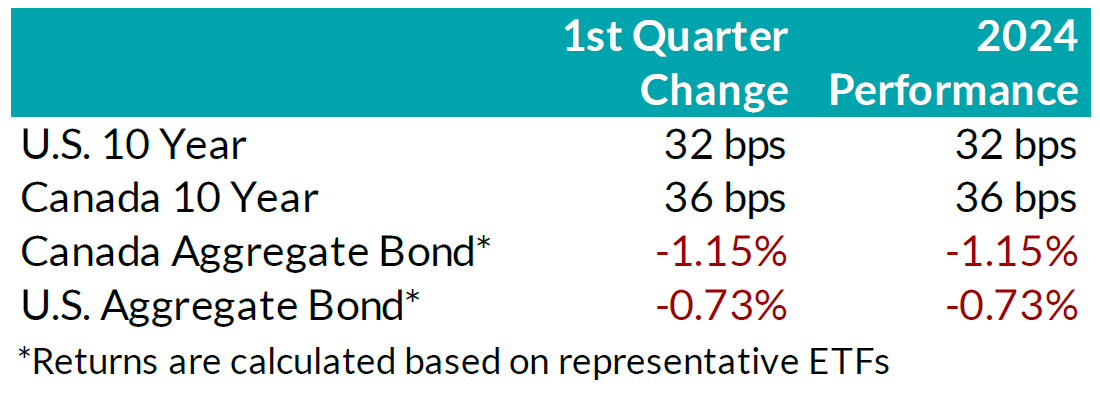

Rates & Credit – Interest rates increased in Q1 2024, giving back half of the decline experienced in Q4 2023 amid consistently positive surprises in U.S. economic data. The positive economic news also drove a strong risk-on tone to the market, with the risk premium on corporate bonds tightening as economic prospects improved. In Canada, corporate bonds outperformed government bonds and the broader FTSE Canada Universe Index (FTSE) with a slightly positive 0.07% return, verses a loss of 1.66% in government bonds and a loss of 1.22% for the overall index. More interest rate sensitive long-term bonds experienced the largest decline, which was partially offset in corporate bonds by the risk-on tone to corporate bond spreads. On a 6-month and 1-year basis, the FTSE remained positive at 6.94% and 2.10%, respectively. Within corporate bonds, lower-rated BBBs outperformed higher-rated A bonds, while industries with higher interest rate exposure such as infrastructure, energy, and communications underperformed those with less exposure (notably financials and securitization).

.png?width=850&height=303 "chart1-(4).png")

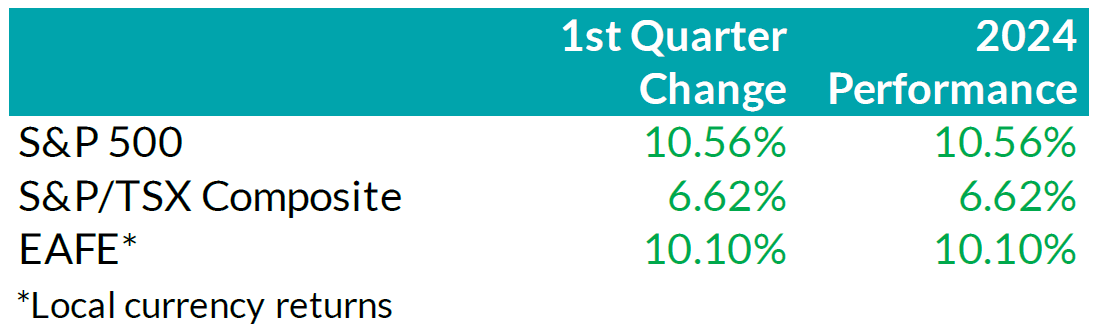

Equity Overview – Throughout Q1 2024, concerns about a recession gradually eased as central bankers adopted a more accommodative outlook on monetary policy. Their growing dovishness reflected confidence that the restrictive monetary measures were effectively curbing inflation as anticipated. Underpinned by prospects of an economic soft-landing, global equity markets rallied to start the year with most major North American indices soaring to new all-time highs during the quarter. U.S. equities continued to outperform other major international markets with the S&P 500 returning 10.6% in USD terms. Major developed economies from Europe, Australasia, and the Far East (EAFE) gained 10.1% in local currency terms, while the TSX added 6.6%. Furthermore, the U.S. economy continued to prove more resilient than most major developed economies, with strong employment and robust output data. As such, foreign investors of U.S. denominated securities achieved enhanced returns, benefitting from a stronger Greenback.

.png?width=850&height=260 "chart2-(1).png")

U.S. Fundamentals – Corporate earnings beat expectations in Q4 2023, triggering a wave of upward earnings revision. Stable operating margins, cash flows and debt loads continue to attract investors into equities. Investors appear focused on the company’s ability to sustain debt levels ahead of renewing debt obligations. We observed that the number of major companies that expect improving financial performance shrunk to ~19%. This suggests that concentration risks are likely brewing in the equity market, yet again.

U.S. Quant Factors

Optimistic run-up in equity valuations were mostly driven by the momentum factor. A basket of companies with positive price trends intensified concentration risk in the equity market. We note that momentum factor’ performance sharply contrasted fundamental factors, making us cautious on the market’s complacency. For context, high quality companies, which is typically defined by high Return on Equity (ROE), stable earnings variability, and low financial leverage, placed second in our risk-adjusted performance rankings, and is dwarfed by the ~ 17.9% return observed from the momentum factor.

Canadian Fundamentals – Against the backdrop of underwhelming financial results, ROE – a gauge of how efficiently a corporation generates profits – rebounded in Q4, 2023, after declining throughout most of the year. The improved efficiency metric provided a positive catalyst for dividend investors as the inverse movements of ROE relative to financing costs over 2023 kept investors on the sidelines. In addition, the CRB Raw Industrials Index, a measure of price changes of basic commodities, broke out of recent ranges, providing a tailwind for Canada’s energy and materials sector. Concerns with earnings contraction and macro-economic conditions have subsided.

Canadian Quant Factors – Crude prices soared higher in Q1 2024, with ongoing production cuts from OPEC+ and ramifications of geopolitical conflicts keeping oil markets undersupplied. As such, energy companies benefitted, surging higher and outperforming the broader index, while the low volatility basket – with lower exposure to cyclically sensitive business – underperformed into quarter end. Furthermore, Canadian banks underperformed to start the quarter, giving back some of the sharp outperformance witnessed into the end of Q4 2023. That said, soft inflation data increased expectations of impending rate cuts from the Bank of Canada and, as such, banks performed in line with the broader market throughout most of the quarter. Underpinned by expectations of a dovish switch in monetary policy, investors rewarded dividend payers with a history of increasing dividends, boosting confidence in their ability to support future dividend growth. It is important to note that investors should not let dividend growth’s outperformance overshadow high dividend paying companies’ underperformance; more specifically, investors remain attentive to the businesses’ ability to create value relative to financing costs.

Views From the Frontline

Rates – Interest rates in both Canada and the U.S. increased across all bond tenors in Q1 2024. U.S. inflation data surprised to the upside, remaining stubbornly higher than hoped, while labour market and consumer indicators underscored the economy's continued strength. In Canada, inflation data fell below forecasts, but early 2024 GDP readings exceeded expectations. The market now anticipates a 'soft landing' for the U.S. economy; however, the Canadian economy continues to slow. North American central banks have signaled that we are at the peak for policy rates. The market is currently pricing in approximately two-to-three, 25 basis point interest rate cuts by the U.S. Federal Reserve in the second half of 2024, much fewer than the six-to-seven 25 basis point interest rate cuts that the market had been anticipating even just three months ago. As the Swiss central bank led the way with the first rate cut among developed countries, central banks in major developed economies will closely monitor upcoming data and market developments to determine the timing and pace for rate cuts.

Credit – The risk premium for corporate bonds (versus government bonds) continued to tighten over the quarter, with a strong risk-on tone to the market as investors priced in renewed economic growth in 2024 as compared to previous expectations. Corporate bond supply was robust, with $38.2bn in new issuance, the second strongest first quarter on record. On the balance, we do not think the current risk premium adequately compensates for downside risk, particularly in longer-dated corporate bonds, and have a bias towards shorter-dated credit where we view the risk / reward dynamic as being more favourable.

Equity – We favour a combination of the Dow Jones and the S&P500 for our broad market exposure. The Dow, a price-weighted index, should have some value and low volatility tilt as it tracks mature large companies. As explained above, concentration risks are brewing in the equity market, and during Q1 this risk was exacerbated by investors rushing into a basket of companies with positive price trends, thereby pushing valuation metrics further into the expensive territory. In our view, it is well-suited to use a combination of the Dow Jones Industrial Average and the S&P 500 for broad U.S. market exposure given the heightened concentration risk. Looking forward, we expect companies to exhibit stable operating margins and therefore, we are shifting our focus toward the balance between upcoming corporate debt refinancing requirements and reinvestment in projects intended to drive future growth. In plain words, we are tactically adding to companies with stable cash flows and decreased debt loads outside of the mega-cap group. In Canada, we expect a modest earnings growth and remain attentive to how efficiently a corporation generates profits relative to their financing cost. We caution against the overly optimistic, commodity driven, “catch-up” trade vs. our southern neighbour. Therefore, we tweaked our investment strategy by rotating out of the low volatility factor and adding to higher yielding quality companies in Canada.

Downloadable Copy

Mark Warywoda, CFA VP, Public Portfolio Management Ian Whiteside, CFA, MBA AVP, Public Portfolio Management Johanna Shaw, CFA Director, Portfolio Management Jin Li

Director, Equity Portfolio ManagementTyler Farrow, CFA

Senior Analyst, EquityAndrew Vermeer

Senior Analyst, CreditElizabeth Ayodele

Analyst, CreditFrancie Chen

Analyst, Rates

ADVISOR USE ONLY

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

-

Market Comments - October 2024

Key Takeaways for Q3· Central banks eased monetary policy by reducing their target interest rates.

· Bond markets performed very well during the quarter as interest rates fell.

· Risk markets experienced some volatility, but stock markets had robust returns.

· Canadian stocks outperformed U.S. stocks in Q3, while the sources of returns in the U.S. market were more balanced and diversified than in the first half of the year.

Views From the Frontline

Bond Markets: During the third quarter, interest rates in both Canada and the U.S. moved significantly lower as markets anticipated that the Bank of Canada would continue – and the Federal Reserve would start – cutting rates. Additionally, the expectation became that the central banks would end up lowering rates more aggressively than previously assumed. That’s because inflation data has softened sufficiently to give the central banks the scope to ease policy, and other economic data, especially from the labour market, indicated the need for them to ease policy in order to prevent economic activity from cooling too much. For instance, in Canada, inflation slowed to the Bank of Canada’s 2% target, while the labour market showed warning signs with the unemployment rate rising to 6.6%. The Bank of Canada cut its target interest rate by 0.25% at each of its July and September meetings. Governor Macklem indicated that if growth does not materialize as expected, “it could be appropriate to move faster on interest rates”. In the U.S., the Federal Reserve kicked off its easing cycle by cutting its target rate by 0.50% in September. The growing signs of a cooling labour market amidst slowing inflation motivated the larger-than-typical move. That said, consumer spending in the U.S. continued to be strong, and GDP is still tracking a healthy growth rate.

While interest rates fell, bonds returns were also boosted by solid behaviour of corporate bonds. Credit spreads (i.e. the risk premium for corporate bonds versus government bonds) continued to grind lower over the quarter. Tightening credit spreads reflected the generally positive risk-on tone to the market, despite some volatility. Lower-rated BBB bonds performed better than higher-quality A-rated bonds. Credit spreads have now generally fallen back to levels that are largely consistent with the tight post-pandemic levels experienced in 2021. The on-going appetite of investors for the extra yield offered by corporate bonds over government bonds is indicated not just by falling credit spreads, but also by investors’ enthusiasm to support the primary issuance market. Corporate bond supply continues to be very robust, with $29B (billion) in new issuance during the quarter, resulting in an impressive $119B issued year-to-date, a new record. Nonetheless, on balance, we do not think the current risk premium adequately compensates for downside risk, particularly in longer-dated corporate bonds, and have a bias towards shorter-dated credit where we view the risk / reward trade-off as being more favourable.

Stock Markets: In the U.S., we continue to caution against heavily concentrated sources of market returns and emphasize a diversified portfolio. Last quarter, diversification proved essential as a multitude of factors heightened market volatility. These factors – which included the unwind of the yen carry trade, investor reactions to mixed mega-cap earnings, and concerns of a slowing labour market – drove investors away from mega-cap technology names and into defensive areas of the market. Following the Federal Reserve’s decision to reduce interest rates by 0.5%, sources of investment returns continued to broaden as investors rotated into economically-sensitive baskets. Underpinned by decelerating inflation and easing monetary policy, we believe the rotation away from the mega-cap tech names is likely to persist and we continue to emphasize portfolio diversification. In Canada, high-quality, high-yielding businesses – composed of the financial sector and non-financial dividend payers – outperformed over the quarter as investors rewarded companies that demonstrated a strong ability to sustain dividends, as well as greater efficiency generating profits. While we continue to favour these businesses, we have taken profit on our financial sector dividend exposure after a sharp reversion in the premium between value creation and current yield. In addition, Chinese officials introduced a wave of stimulus to revitalize growth, bringing life back to the metals and luxury goods sectors. Accordingly, Canadian and European equities have benefitted recently.

Market Update

Rates & Credit: In Q3, interest rates in both Canada and the U.S. decreased significantly, with front-end interest rates declining faster than long-end interest rates amid cooling inflation and a weakening labour market. As a result, the FTSE Canada Universe Index posted a positive return of 4.7%. Coincidentally, Canadian corporate bonds and government bonds each also generated returns of 4.7%, totally in-line with the Universe index. On the other hand, despite short-term interest rates falling much more than long-term interest rates, the higher price sensitivity of long-dated bonds had them outperform shorter-dated bonds, with the Long-Term bond index up 5.8% while the Short-Term bond index gained 3.4%. Similarly, within corporate bonds, industries that have longer-dated debt (e.g. energy and infrastructure) outperformed those that tend to have shorter-dated debt (e.g. real estate and financials).

Rates & Credit: In Q3, interest rates in both Canada and the U.S. decreased significantly, with front-end interest rates declining faster than long-end interest rates amid cooling inflation and a weakening labour market. As a result, the FTSE Canada Universe Index posted a positive return of 4.7%. Coincidentally, Canadian corporate bonds and government bonds each also generated returns of 4.7%, totally in-line with the Universe index. On the other hand, despite short-term interest rates falling much more than long-term interest rates, the higher price sensitivity of long-dated bonds had them outperform shorter-dated bonds, with the Long-Term bond index up 5.8% while the Short-Term bond index gained 3.4%. Similarly, within corporate bonds, industries that have longer-dated debt (e.g. energy and infrastructure) outperformed those that tend to have shorter-dated debt (e.g. real estate and financials).

Equity Overview: Underpinned by decelerating inflation data and easing monetary policy – including the outsize 50-basis cut from the Federal Reserve – prospects for an economic soft landing increased over the quarter. That favourable outlook spurred global equity markets to all-time highs, with previously lagging areas of the market narrowing the performance gap compared to the U.S. mega-cap technology names that had led returns in the first half of the year. Canadian equities outperformed their U.S. counterpart last quarter, rising 10.5% as strength in the banking and materials sectors pushed the index higher. Major developed markets from Europe, Australasia, and the Far East (EAFE) were more subdued, gaining 0.9% (in local currency terms) last quarter. That said, grand expectations for further interest rate cuts in the U.S. pushed the greenback to its lowest level in over a year, boosting EAFE returns to over 7% in U.S. dollar terms. Within the U.S., sources of market returns broadened as well, with investors rotating out of concentrated AI companies and into more economically sensitive businesses.

Equity Overview: Underpinned by decelerating inflation data and easing monetary policy – including the outsize 50-basis cut from the Federal Reserve – prospects for an economic soft landing increased over the quarter. That favourable outlook spurred global equity markets to all-time highs, with previously lagging areas of the market narrowing the performance gap compared to the U.S. mega-cap technology names that had led returns in the first half of the year. Canadian equities outperformed their U.S. counterpart last quarter, rising 10.5% as strength in the banking and materials sectors pushed the index higher. Major developed markets from Europe, Australasia, and the Far East (EAFE) were more subdued, gaining 0.9% (in local currency terms) last quarter. That said, grand expectations for further interest rate cuts in the U.S. pushed the greenback to its lowest level in over a year, boosting EAFE returns to over 7% in U.S. dollar terms. Within the U.S., sources of market returns broadened as well, with investors rotating out of concentrated AI companies and into more economically sensitive businesses.

U.S. Fundamentals: Outside of the Magnificent 7, investors are interpreting downside earnings surprises as a normalization of financial performance rather than a deterioration. For example, McDonald’s share price rallied over 17% into quarter-end following its earnings release despite announcing declining sales and contracting earnings per share. Within the AI-ecosystem, investors are beginning to look for opportunities beyond chip manufacturers, such as nuclear energy providers. At an index level, our work shows that members of the Russell 1000 index, excluding the Mag-7, posted a median earnings growth of nearly 9% year-over-year, expanding from the ~6% witnessed in Q2. Furthermore, the number of companies from this group reporting positive earnings growth grew to approximately 67%, up from 60% in the prior quarter. In our view, the ongoing broadening of earnings strength outside of the Mag-7 can provide tailwinds to current market rotations into previously left-behind companies. Within the mega-cap tech space, investors have become more discriminant than in prior quarters, rewarding businesses with greater success monetizing their AI-investments. This trend was evident through the divergence of returns from IBM and Alphabet (Google’s parent company) following their quarterly earnings.

U.S. Quant Factors: Decelerating U.S. inflation data prompted a rotation out of highly concentrated areas of the market (growth) and into more economically-sensitive companies (value). Then, concerns of a slowing U.S. labour market and the unwind of the yen carry trade increased market volatility, leading investors to shelter their positions by reallocating to low volatility. As the quarter progressed, expectations of easing monetary policy and stabilizing employment data helped calm return to the market and the rotation from mega-cap tech sector resumed, albeit at a lesser pace. Notably, this “catch-up” trade also benefitted dividend-paying companies, particularly those with a lengthy and established history of increasing dividends, as investors favoured those more mature operations.

Canadian Fundamentals: Investors returned to the Canadian market after Canadian companies showed signs of recovery last quarter with earnings expanding by more than expected. With inflation showing clearer signs of deceleration and the outlook regarding the path of monetary policy increasingly implying lower interest rates going forward, investors are allocating toward high-quality, dividend-paying companies. From a sector level, surging gold prices provided a tailwind for Canadian miners, helping the materials sector outperform over the quarter. More recently, the materials sector has benefitted from elevated base metal prices following the arrival of Chinese stimulus. In contrast, oil prices declined over 16% last quarter as fears of an oversupplied market swelled following speculation that OPEC+ would look to dial back production cuts. As a result, investors looked past lingering geopolitical risks and the energy sector underperformed.

Canadian Quant Factors: Amid an improving Canadian macroeconomic backdrop and clearer outlook on the trajectory of monetary policy, dividend-yielding businesses became sought after. More specifically, investors continued to emphasize dividend sustainability last quarter, rewarding dividend-paying businesses that demonstrated strong financial performance and the ability to support future payouts. For example, the major Canadian banks sharply outperformed in Q3 after reporting earnings growth that mostly exceeded expectations. In essence, investors have become more constructive on this high-yielding group as their ability to create value relative to financing costs improves.

Downloadable Copy

ADVISOR USE ONLYMark Warywoda, CFA

VP, Public Portfolio ManagementIan Whiteside, CFA, MBA

AVP, Public Portfolio ManagementJohanna Shaw, CFA

Director, Portfolio ManagementJin Li

Director, Equity Portfolio Management

Tyler Farrow, CFA

Senior Analyst, Equity

Andrew Vermeer

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Francie Chen

Analyst, Rates

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.