Site Search

690 results for go page PROBLEMGO.COM Need to get my son out of juvenile hall tonight cash waiting HMP Long Lartin

- Individual insurance video library

- 2026 Elite Advisor Program

- Path to Success Module 1

- [pdf] Custom Quote - DIA/GIA

-

Levelizing taxes on fixed income investments

A smart strategy to promote with clients

Many clients choose fixed income investments because they are more stable and predictable than other investment types. However, there is a downside to this approach that many don’t think about – taxes, which increase as the investment grows. As an advisor, you can help clients reduce some of the money they pay in taxes by suggesting a different approach.

In most cases, fixed income investments are taxed yearly. To pay these taxes, clients usually take out some of the interest income earned, and leave the rest invested. This in turn increases the tax that must be paid on the interest earned the next year. As a result, a large amount of the investment income earned each year goes straight to taxes with a growing amount of tax that must be paid each year. You can show clients a solution that can help lower total taxes they pay on their fixed income investments.

The tax challenge

Using participating whole life (WL) insurance as part of a financial solution, you can help clients levelize their annual tax payment. And lower the cumulative tax they must pay on their fixed income investments.

The solution: levelize the tax

Each year the client takes out the full amount of the interest earned on the fixed income investment. They leave only the principal amount. Part of the interest income withdrawn is used to pay the taxes on the fixed income investment. The remaining amount is used to pay premiums for a participating WL policy. Because the client is leaving only the principal amount invested, the tax they pay each year is a levelized amount. This reduces the cumulative taxes they pay over the life of the fixed income investment.

How it works

With this solution, the value of the fixed income investment along with the potential value provided by the participating WL policy, can mean a higher estate value. And a lower cumulative tax bill than what can be achieved through only the fixed income investment.

The participating life insurance not only provides valuable life insurance coverage, but also offers tax-advantaged growth and the potential for dividends.

To help explain this concept to individual clients, feel free to share Levelize the tax on your fixed income investments with participating whole life (1799).

This concept also works with corporate owned participating whole life policies. Feel free to share Levelize the tax on fixed income investments with corporately-owned participating whole life (1874).

This solution isn’t just about lowering taxes. It’s about helping clients grow their money, plan for their future, and protect what matters most. As an advisor, guiding clients toward solutions that address both immediate and future needs can set you apart and help build trust.

Why it matters

Contact your wholesaler to learn more. - EquiNet-FAQ-FINAL_fr

-

Paper Pivotal Select applications (Form #1383 and #1384)

On April 27, 2020 Equitable Life® launched its NL-CB sales charge option to its Pivotal Select™ segregated fund lineup. The new option provides an additional choice to the existing Low Load (LL), No Load (NL) and Deferred Sales Charge (DSC) selections. To reflect the new sales charge option, Pivotal Select applications (Form #1383 and #1384) were updated.

The paper Pivotal Select applications (Form #1383 and #1384) with a version date prior to 2020/04/27 (located on the back page and in the bottom right-hand corner of the application) will no longer be accepted as of July 1, 2020. If you currently have applications with a date that is before 2020/04/27, please destroy them and order new applications from our Supply Team. To order new applications, click here.

Want to be sure you always have the most up-to-date application? Try our EZcomplete® online application platform. EZcomplete makes it easy to process your non-face-to-face applications and allows your clients to provide their signature remotely on their own device.

For more information about the NL-CB sales charge option, please click here. For more information about Equitable Life’s EZcomplete, click here. -

REMINDER that paper applications with a version date prior to 2021/04/02 are set to expire July 1, 2

To comply with the Government of Canada’s anti-money laundering legislation and FATCA/CRS changes, Equitable Life® has updated its Savings and Retirement and Life Insurance applications.

If you currently have applications with a version date before 2021/04/02, please destroy them and use our online pdf applications or order new applications from our Supply Team. Paper applications with a version date prior to 2021/04/02 (located on the back page and in the bottom right-hand corner of the application) will no longer be accepted after July 1, 2021 for:

● Savings and Retirement (Form #1383, #1384, #799, #355), and

● Life Insurance (Form #350)

To learn more about the Government of Canada’s anti-money laundering legislation and FATCA/CRS review the following links:

Want to be sure you always have the most up-to-date application? Try our EZcomplete® online platform for Individual Life, Critical Illness and Segregated fund applications.

For a complete list of all forms and applications affected by the anti-money laundering legislation, refer to the following links:

● Savings and Retirement Anti-money Laundering Legislation Requirements Summary.

● Life Insurance Anti-money laundering Legislation Requirements Summary.

● Government of Canada - Guidance on the Common Reporting Standard

● Financial Transactions and Reports Analysis Centre of Canada

If you have any other questions, contact your Regional Sales Manager or Equitable Life’s Advisor Services Team

® denotes a registered trademark of The Equitable Life Insurance Company of Canada.

-

EquiLiving offers more options to clients facing a covered Critical Illness condition

Consider these statistics…1 in 2 Canadians will develop cancer in their lifetimes1. They’re just numbers…until the day someone you know is diagnosed, someone who didn’t see it coming. Then it becomes very real - no longer incidence statistics, but costs. Today more people than ever are surviving and living with not only just the physical, but also the financial effects of their illness.

We’re there to help when illness strikes

NEW! EquiLiving® plans and riders have recently been enhanced including:

● 20 pay options with coverage to age 75 or coverage for life

● Support from Cloud DX to help monitor a client’s well-being from treatment to recovery.

● Added Acquired Brain Injury as a covered critical condition

● 30-day survival period removed for all non-cardiovascular covered conditions

● No age restriction to claim for Loss of Independent Existence (LOIE)

● EquiLiving Benefit now pays the higher of the EquiLiving Benefit or the Return of Premium Rider Benefit (not including Return of Premium on Death)

● And so much more …

Learn more

● CI product enhancement video

● Visit our launch event page with product change details and more

● Marketing Materials

Please contact your Regional Sales Manager for more information.

1 www.cancer.ca

-

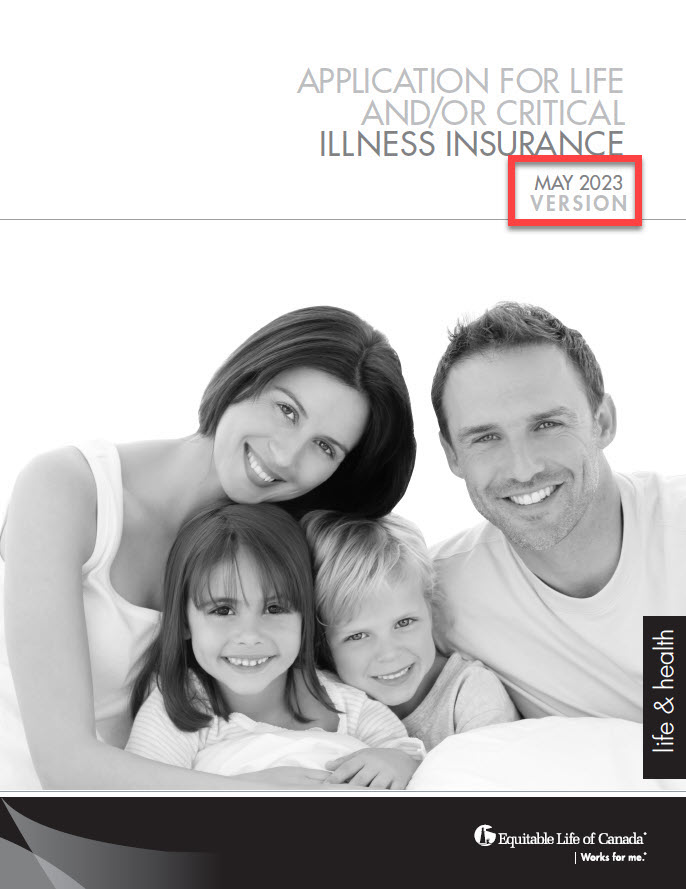

New 350 Life and CI Applications

On August 2nd, 2023, Equitable Life® will be updating the privacy and legal sections on some forms. This includes the form 350 Paper Application for Life and/or Critical Illness Insurance. This change will also be applied on our websites and our online application EZComplete®. These changes are part of Bill 64. The Bill is about the protection of personal and private information in Quebec. This will take effect on September 1st, 2023.

Due to this change, we ask all advisors to use the latest version dated May 2023 of the paper application after August 2nd. Applications in Quebec must use the lastest version from September 1, 2023 onwards.

For all regions outside Quebec, we will support a transition period from ‘old’ to ‘new’ applications until December 31st, 2023. After this date, we will no longer accept older versions of our Life and Critical Illness application.

To make sure you are using the latest version of the application, check the date on the title page. It should say May 2023. See the image below:

.jpg?width=200&height=259 "Form-350-Image-EN-(1).jpg")

To order paper copies, click here.

Email completed applications to supply@equitable.ca.

To learn more about Bill 64, please visit Assemblee nationale du Quebec - Bill 64. You may also contact your wholesaler.

® denote a registered trademark of The Equitable Life Insurance Company of Canada.