Site Search

770 results for PROBLEMGO.com Paying to have an arrest record sealed dark web browse here anonymity guaranteed now

-

Market Commentary April 2025

Key Takeaways for Q1

- Economic policy became more uncertain with fluctuating tariff announcements from the U.S. and its trading partners.

- Global stocks markets experienced heightened volatility year-to-date, reflecting the negative repercussions of tariffs for highly integrated global economies.

- Within U.S. markets, investors rotated out of growth stocks into value and defensive areas of the market.

- Bond markets performed well during the quarter as interest rates moved lower.

- Most central banks continued to ease monetary policy by reducing their target interest rates. The U.S. Federal Reserve was a notable exception, electing to wait for greater clarity before lowering rates further.

Economic and Market UpdateEconomic Summary: In the U.S., the latest GDP data confirmed solid economic growth in 2024. However, as President Trump pushes forward his economic agenda, uncertainty surrounding fiscal policy and global trade have dampened market sentiment. Inflation pressures persisted, with the rate of inflation remaining above the central bank’s 2% objective. The labour market in the U.S. remained resilient, with unemployment rate staying low compared to historical norms. The Federal Reserve shifted to a more cautious approach, holding the policy rate steady through Q1 at the range 4.25% - 4.5%. The central bank raised its inflation forecast, lowered growth projections, and warned that “uncertainty around the economic outlook has increased.” U.S. bond yields were lower for most maturity dates during the first quarter, as the market priced in more growth concerns and anticipated more rate cuts from the Federal Reserve.

In Canada, recent GDP data showed stronger-than-expected growth. The inflation rate remained close to the 2% target but rose more than expected in February, and the labour market showed signs of improvement. U.S. tariffs continued to be a significant concern, and it is prompting businesses and consumers to become more cautious and slow their spending. The Bank of Canada warned that the economic impact of the tariffs could be “severe” and expected weaker growth in the coming quarters. For those reasons the Bank of Canada continued its easing cycle, cutting rates by 25 basis points at each of the January and March meetings, bringing the policy rate to 2.75%. Bond yields in Canada were also lower, with short-term interest rates decreasing faster than long-term interest rates as the Bank of Canada’s rate cuts outpaced market expectations.

Bond Markets: During Q1 2025, the FTSE Canada Universe Bond Index returned 2.0% as interest rates declined across all tenors. Although interest rates fell, this was partially offset by higher credit spreads (i.e. the extra yield on corporate bonds versus government bonds to compensate for their extra risk). Consequently, while corporate bonds still generated a positive return on the quarter, they underperformed government bonds. Widening credit spreads reflected the risk-off tone to the market, with on-off-on-off-on(?) tariffs contributing to the uncertainty. Lower-rated BBB bonds generally performed worse than higher-quality A-rated bonds. While credit spreads are higher than they were in December and January, they are still expensive compared to longer term averages. Corporate bond issuance remained robust up until the last week of March, as investor demand kept deals well supported. Overall, the market took in $40 billion in new issuance, the second highest on record, spread over 82 bonds. While corporate bonds are more attractive than in January 2025, we believe the more likely path is towards higher credit spreads as U.S. tariffs impact global growth. We have maintained our conservative view with a bias towards shorter-dated credit but remain ready to invest in longer dated corporate bonds as valuations become more attractive.

Stock Markets – Overview:

Uncertainty surrounding the scope and severity of new tariffs led investors to reassess global economic growth prospects and weighed on risk sentiment. As a result, the S&P 500 declined 4.3% over the quarter, underperforming Canadian and international markets. Within the U.S., investors rotated out of previously favoured growth stocks with loftier valuations – including members of the Magnificent 7 – into less volatile and value-cyclical companies. Meanwhile, Canadian equities returned 1.5% in Q1 despite ongoing trade negotiations and uncertain economic growth forecasts. Surging commodity prices helped the materials and energy sectors outperform, offsetting weakness in the technology and industrials sectors. Elsewhere, major developed markets from Europe and Asia (EAFE) were supported over the quarter by the introduction of a new German fiscal stimulus package and signs of improving Chinese economic growth. Following the quarter end, President Trump announced global tariffs on April 2nd, prompting some trading partners to hit back with retaliatory tariffs. The S&P 500 lost a record $5.2 trillion over two trading sessions and re-entered correction territory, with other global equity markets moving in tandem.

U.S. Equities: While the impact of tariffs has made investors more apprehensive, we have yet to witness a deterioration in financial performance. In fact, U.S. earnings continued to exceed forecasts last quarter, with approximately 70% of companies beating expectations. Furthermore, our bottom-up analysis shows that the skew of corporate earnings surprises continues to tilt positive. That said, we note that companies are providing more cautious guidance amid the increased economic uncertainty and that these earnings largely reflect conditions in 2024, not 2025. Notably, consumer stocks like Walmart have lowered growth forecasts for 2025, citing concerns surrounding consumer confidence and macroeconomic conditions. In addition to clouding the outlook, geopolitical shocks like sweeping tariffs may risk changing how companies choose to operate, including the structure of supply chains and sources of revenue. At this stage, it is still unclear how long these trade tensions will last, as that depends on how other countries choose to respond. If the tariffs are rolled back quickly, many companies may be able to absorb the temporary extra costs without serious damage to profits, and the broader economy could avoid lasting harm. But if the tariffs remain in place for a long time, the consequences could be much more serious; companies might have to change how they operate, restructure supply chains, and raise prices to deal with long-term pressure on profits.

Canadian Equities: Against the backdrop of worrisome trade developments, the Bank of Canada continued to ease monetary policy. While lower rates have helped Canadian companies report better-than-expected profit growth, consensus earnings expectations for 2025 have been revised 2% lower since the beginning of the year, reflecting the expectations for tariff headwinds. Falling bond yields made high quality, high dividend paying companies more attractive, helping this group outperform. Furthermore, the price of raw industrials – a basket of commodities – surged higher over the quarter and as a result, commodity-oriented companies benefitted. More specifically, the materials sector performed strongly with gold prices reaching new all-time highs throughout the quarter. However, if trade frictions continue to escalate and weaker growth projections materialize into a real economic slowdown, the Canadian market, given its cyclical nature and heavy reliance on commodity-driven businesses, remains particularly vulnerable to external headwinds. Moreover, given Canada’s weaker fundamental backdrop, we caution that the recent outperformance of Canadian equities relative to the U.S. may prove short-lived, particularly if trade tension persists.

Bottom line:

Heightened uncertainty surrounding global trade policies, coupled with deteriorating economic growth projections, continued to weigh on investor sentiment. Bond prices benefited from the flight to less-risky assets, with lower interest rates in anticipation of weaker economic conditions. In equity markets, the introduction of broad-based tariffs increased market volatility and drove major indices sharply lower year-to-date. Looking forward, we remain cautious of the recent outperformance of Canadian and international markets relative to the U.S. While tariffs began as a U.S. policy move, the ripple effects extend far beyond American borders, reflecting the systemic fragility that underpins global trade. If trade barriers persist, businesses may be forced to make structural shifts in their operations and review their current business models. Until markets achieve greater clarity on global trade policies, we continue to prioritize exposure to diversified large-cap stocks in the U.S., over defensive or growth-heavy positions. Within Canada, we continue to favour high quality, high dividend paying names with less sensitivity to downgrades in global growth.

Downloadable Copy

ADVISOR USE ONLYMark Warywoda, CFA

VP, Public Portfolio ManagementIan Whiteside, CFA, MBA

AVP, Public Portfolio ManagementJohanna Shaw, CFA

Director, Portfolio ManagementJin Li

Director, Equity Portfolio Management

Tyler Farrow, CFA

Senior Analyst, Equity

Andrew Vermeer

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Francie Chen

Analyst, Rates

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

-

NEW MARKETING MATERIAL! Equimax Participating Whole Life, Strong and Stable Dividends

Participating whole life policyholders can get some of the participating account earnings back as dividends.1

Dividend scales change over time. This new marketing piece shows how the actual values of policies look like against those that were estimated. It looks at two sample policies and compares them to the original sales illustrations. One example shows an Equimax Estate Builder® policy. The other example shows an Equimax® Wealth Accumulator® policy.

We are proud of our strong and stable dividend results. We have paid dividends to our participating policyholders every year since 1936. And we’re still going strong!

We want to make sure that we can continue to provide long-term income and growth to support the dividend scale and meet the product guarantees. We do this with constant focus on how we invest and manage risk to support the participating account.

As a mutual life insurance company, we are owned by our policyholders who count on us and our services. Their trust in our knowledge, experience, and financial strength helps us keep our commitments to them—now and in the future.

Dividend scales may change.2 But with a balanced approach, Equitable Life’s Equimax® Participating Whole Life continues to deliver excellent value. It gives guaranteed life insurance protection with the potential for earnings.

Want to learn more? Check out our new marketing piece: Equimax Participating Whole Life, Strong and Stable Dividends (2075).

For more information, reach out to your local wholesaler.

® and TM denote trademarks of The Equitable Life Insurance Company of Canada.

1 Dividends are not guaranteed and are paid at the sole discretion of the Board of Directors. Dividends may be subject to taxation. Dividends will vary based on the actual investment returns in the participating account as well as mortality, expenses, lapse, claims experience, taxes, and other experience of the participating block of policies.

2 If low interest rates continue, investment returns will be lower, and this may mean decreases in the dividend scale in the future. Dividend payments are not guaranteed, but they will never be negative. - COVID-19 Group Benefits FAQ

- [pdf] Daily/Guaranteed Interest Account Application - Registered/Non-Registered

-

Start a Conversation with EZstart – Now Available for Equimax Wealth Accumulator

Looking for an easy way to explain insurance? We have a digital tool to do just that!

Start a Conversation with EZstart™

EZstart helps to commence those initial client conversations. Think of it like a digital brochure: you start a conversation about life goals, enter a few details - and within a few clicks - get a quick quote on your phone or tablet instantly.

We have a NEW EZstart for Equimax Wealth Accumulator® available. Go to the EZstart for Equimax Wealth Accumulator now.

Don’t forget about our other EZstart tools that are available for you. Learn more.

® and TM denote trademarks of The Equitable Life Insurance Company of Canada. -

Savings & Retirement Policy and Procedure updates regarding Electronic Signatures

We have updated our policies and procedures regarding electronic signatures in the Savings and Retirement department. We are now able to accept electronically signed documents, from all major third-party signing vendors.

Including esign@equitable.ca as a non-signing reviewer is the preferred method as it ensures the security embedded documents are accurately and immediately available for Equitable. We will be automatically notified when signing is complete and will download eSigned forms immediately for processing. Including esign@equitable.ca as a non-signing reviewer is secure, quick, and efficient. Documents no longer need to be emailed to us – eSigned documents are sent directly to us once all signatures are completed, therefore you do not need to notify us once the documents are signed.

When esign@equitable.ca is not used to submit electronically signed documents, the following criteria are required:- The original signed form and audit trail with all the security features intact

- The email address used to sign must match what is in our files (as provided on the application, for electronic policy delivery or through previous communication). If an email address has changed, or we don’t have an email contact for the signer, we will follow up for confirmation.

A guide on how to use esign@equitable.ca can be found here.

Please note that Equitable does not accept digital signatures (images or fonts of a signature which are not stamped).

Date posted: June 13, 2024 -

Sharpen your skills with Equitable’s Path to Invest summer learning modules

Want to stay ahead, bring more value to clients, and earn Continuing Education (CE) credits?

Equitable® now offers new online summer modules to help you grow your financial knowledge. These self-paced Path to Invest modules are available on our ON24 platform. You can learn on your own schedule and earn CE credits with ease.

Whether you want to boost your investment skills or have better client conversations, these courses are here to support your growth.

The first module, Index Investing, explores the basics of index investing, how it compares to active management, and how using indexes can help diversify client portfolios.

The second module, Saving for a Home with Equitable, equips you with strategies and tools to guide clients through the homebuying journey, including insights on savings vehicles, intergenerational wealth transfers, and mortgage planning.

Each course is approved by the Alberta Insurance Council and the Insurance Council of Manitoba. You will earn 1 CE credit for each course after passing the quiz.

Start learning today! Visit our Learning Centre to begin.

If you have any questions, reach out to your Director, Investment Sales. When we work together, success is mutual.

Continuing Education Credits

To be eligible for CE credits, you must register individually, watch the webcast in full and complete a short quiz. These webcasts are available in English only. It is the advisor's responsibility to ensure Continuing Education credits being offered are accepted by the licensing body. Alberta Insurance Council (AIC) credits are valid in Yukon, British Columbia, Alberta, Saskatchewan, Ontario, New Brunswick, Prince Edward Island and Nova Scotia. Insurance Council of Manitoba (ICM) credits are valid in Manitoba only.

Date posted: July 17, 2025 - [pdf] Pivotal Solutions Fund Facts

-

Guaranteed Interest Account Application version update

Equitable® Guaranteed Interest Account applications with a version date prior to 2023/09/01 (located on the bottom right-hand corner of the application) will no longer be accepted after December 31, 2023. If you currently have applications with a date that is before 2023/09/01, please destroy them and download digital applications from EquiNet® or order paper applications from our Supply Team.

If you have any other questions, contact your Regional Investment Sales Manager or Equitable’s Advisor Services Team, Monday to Friday from 8:30 a.m. to 7:30 p.m. at 1.866.884.7427 or email savingsretirement@equitable.ca

Posted December 13, 2023® or ™ denotes a registered trademark of The Equitable Life Insurance Company of Canada.

-

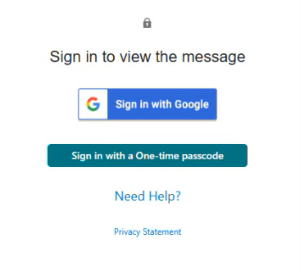

New secure encryption process for outstanding Equitable S&R business requirements

The Equitable® Savings and Retirement Operations team is improving how they send secure email messages to advisors. These emails are sent when there are outstanding requirements for an application or missing information for requests.

Previously, advisors had to manually password protect or unlock PDF documents. This caused delays and difficulties for recipients. The new encryption process will remove that confusion and make it easier for advisors to send and receive secure, encrypted messages.

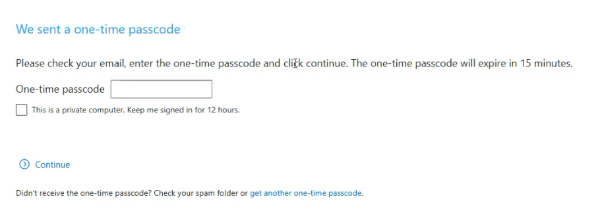

Advisors will now receive secure, encrypted emails from the QA annuity operations mailbox. These emails will use an encrypt option to protect personal client information, such as attachments or requests for personal documents. Recipients will get an email with a subject line saying they have a secure private message. They will need to sign in to view the message or choose to get a one-time passcode (OTP).

Please ensure to check the SPAM folder for the OTP option as it will expire in 15 minutes. Enter the OTP in the secure message

portal.

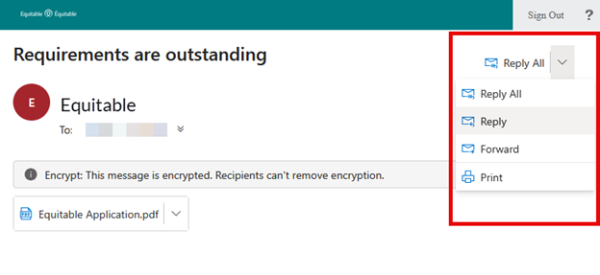

Emails are sent in both English and French, with automatic translation based on browser settings. Recipients must click the view button to access the message in the secure web portal where they can see the encrypted attachment.

Make sure to click Reply in the top right corner of the encrypted message to keep communications within the secure portal.

For more information or assistance, please contact your Director, Investment Sales.

Date posted: May 22, 2025