Site Search

512 results for enter website fast MAKEMUR.com how much to bribe a customs officer to clear my cargo

-

All about the changes to the capital gains inclusion rate

Disclaimer: The following content is provided by and is the opinion of Invesco Canada Ltd. Equitable does not guarantee the adequacy, accuracy, timeliness, or completeness of the information. Equitable shall not be liable for any errors or omissions in the information provided by Invesco.

What has changed?

One noteworthy measure to come from Budget 2024 is the proposed change to the capital gains inclusion rate, which was previously held steady at 50% since 2001.

For individuals, capital gains more than $250,000 annually will be subject to an increased 66.67% inclusion rate as of June 25, 2024, while the capital gains up to $250,000 will continue to be subject to the existing 50% inclusion rate. As a transitional measure for 2024, only the capital gains realized by individuals on or after the effective date of June 25 that are above the $250,000 threshold will be subject to the increased inclusion rate.

For trusts and corporations, the inclusion rate on all capital gains will increase from 50% to 66.67% starting on June 25, 2024.

Who is affected?

Impact to individuals

Budget 2024 proposed to add transitional rules which would specifically identify capital gains and losses realized before the effective date (Period 1) and those realized on or after the effective date (Period 2). The effective date is June 25, 2024. Capital gains realized on or after that date will have an inclusion rate of 50% on the amount up to $250,000, and an inclusion rate of 66.67% on the amount above $250,000. All capital gains realized prior to the effective date will have an inclusion rate of 50%.

Take Ontario as an example, the proposed higher inclusion rate on capital gains would effectively increase the average federal-provincial marginal tax rate for Ontario residents on capital gains above $250,000 at the top marginal tax rate from 26.76% to 35.69%. A more detailed analysis on the impact of these changes to an individual’s tax rate is discussed below.

For net capital gains realized in Period 2, the annual $250,000 threshold would be fully available in 2024 (i.e., it would not be prorated) and it would apply only in respect of net capital gains realized in Period 2.

The $250,000 threshold would effectively apply to capital gains realized by an individual, either directly or indirectly via a partnership or trust, net of any: current-year capital losses, capital losses of other years applied to reduce current-year capital gains, and capital gains in respect of which the Lifetime Capital Gains Exemption, the proposed employee Ownership Trust Exemption or the proposed Canadian Entrepreneurs’ Incentive claimed.

Two common scenarios of reaching the $250,000 capital gain threshold are the deemed disposition of capital property at death, and the emigration from Canada (i.e., becoming a non-resident for income tax purposes). We have provided additional details on these topics below.

Deemed disposition upon death

When an individual passes away, they are deemed to have sold their capital property (e.g., units or shares of mutual funds, shares of corporations, and real property) at its fair market value (FMV) immediately before their death. If a capital gain arises because of this deemed disposition, that capital gain is reportable on the deceased’s final (terminal) tax return and the taxes owing as a result, if any, would be payable by the estate of the deceased. However, there are provisions that allow taxes to be deferred when the property is transferred to a spouse. For example, if a capital property is transferred to a surviving spouse or common-law partner, subsection 70(6) of the Income Tax Act (Canada) automatically deems the deceased to have disposed of that property and the spouse or common-law partner immediately acquires the same property at the deceased transferor’s adjusted cost base (ACB). This is commonly referred to as the “spousal rollover”. Another potential strategy to manage potential large capital gains taxes at death is life insurance, since the death benefit is typically paid out tax-free.

Without careful planning, the estate value could be substantially reduced by the changes to the capital gains inclusion rate. Furthermore, it would be prudent to ensure there are liquid assets or cash available in the estate to cover the associated tax liabilities.

Non-resident of Canada – Departure tax

Residency in Canada for income tax purposes is a question of fact, which primarily depends on the individual’s residential and social ties in Canada. When an individual becomes a non-resident of Canada, they are deemed to have disposed of and immediately reacquired certain types of property at FMV. The tax incurred because of this deemed disposition and reacquisition is also known as the departure tax. Some examples of properties subject to departure tax include securities inside a non-registered investment portfolio, shares of Canadian private corporations, and real estate situated outside of Canada. Note that there are some properties that are exempted from the departure tax, including: pensions and similar rights (including registered retirement savings plans (RRSPs), registered retirement income funds (RRIFs), and tax-free savings accounts (TFSAs)) and Canadian real property.

The departure tax rules coupled with the increased capital gain inclusion rate above the $250,000 threshold may incur additional tax payable for emigrants. However, there is an option to defer the payment of departure tax on income associated with the deemed disposition upon emigration. By making an election, the individual would pay the tax later, without interest, when the property is disposed of. This election can be done by completing CRA Form T1244, “Election Under Subsection 220(4.5) of the Income Tax Act, to Defer the Payment of Tax on Income Relating to the Deemed Disposition of Property," on or before April 30 of the year following their departure from Canada.

Impact to Entities

Corporations and trusts will also be impacted by the increased inclusion rate as of June 25, 2024. Unlike individuals, corporations and trusts will not have access to the old inclusion rate on the first $250,000 of capital gains: they will be subject to the new 66.67% inclusion rate from the very first dollar.

With the above in mind, there will be options available to shelter corporate and trust capital gains from the new inclusion rate.

For corporations:

The lifetime capital gains exemption (LCGE) can be used to eliminate capital gains taxes on the sale of qualified small business corporation shares (generally, these are shares of a Canadian-controlled private corporation that carries on an active business). The LCGE is also available on the sale of qualified farm or fishing property. The current lifetime limit for the LCGE is $1,016,836. Budget 2024 proposed to increase that limit to $1,250,000 starting on June 25, 2024, so certain business owners will be able to reduce or eliminate their exposure to the new inclusion rate if they are able to make use of the increased LCGE limit.

For trusts:

Budget 2024 suggests that capital gains allocated by a trust to its beneficiaries on or after June 25, 2024, will be included in the beneficiaries’ income at the old 50% rate up to the beneficiaries’ first $250,000 of capital gains for the year. While the specifics are not yet available, this opportunity will likely create further planning considerations surrounding the allocation of capital gains from a trust to its beneficiaries to reduce taxes. Capital gains can generally be allocated to a beneficiary for tax purposes when they are actually paid to the beneficiary, or when they are payable to a beneficiary (i.e., the beneficiary hasn’t received it, but has a right to demand payment of the capital gain). The option of making income paid (or payable) to its beneficiaries and allocating such income to be taxed in their hands will largely depend on the trust terms.

Historical reference: capital gains inclusion rate

Those of us around long enough, understand that this recent change was not the only time the capital gains inclusion rate has deviated from the 50% inclusion rate. Over the years, capital gains tax rate has ranged from nil to as high as 75% as indicated in the table below. In fact, the first instance of capital gain tax was introduced in 1972!

.jpg")

Excluding the 2024 tax year, we have given a rough estimate on the percentage of time spent at each of the various capital gains inclusion rates over the last 42 years. As we can see, for most of the time, the capital gains inclusion rate has remained at the 50 % inclusion rate. In fact, for the last 23 consecutive years, the inclusion rate has remained untouched with the last change being back in tax year 2000 with various changes introduced that year.

Tax impact by province/jurisdiction

With the increase in the capital gains inclusion rate, we want to demonstrate the potential tax impact of those changes across jurisdictions in Canada. The table below shows the 2024 marginal tax rate for the highest individual income earners in each jurisdiction at both the 50% and 66.67% capital gains inclusion rate, respectively. The average difference is an increase in taxes payable by 8.45%.

Next, we look at the additional taxes payable because of the inclusion increase, assuming varying capital gains income levels. Of course, this assumes that the capital gains do not otherwise benefit from a reduced inclusion rate or an outright exemption such as eligible in-kind donations of securities to registered charities, or shares that qualify for the lifetime capital gains exemption, to name a few.

Understanding the tax implications of investing is an essential part of financial planning and reinforces the importance of working with a knowledgeable financial advisor to understand the long-term impact of these changes as it applies to personal situations. No doubt, tax rates influence capital allocation decisions. Canadians who take more inherent risk with their capital have traditionally been afforded preferred taxation rates promoting innovation through capital investment, something the government can do with good tax policy to encourage business growth and spur economic expansion. This is evident in the breakdown of the tax rates depending on the characterization of the income as noted in the table below.

Clearly the tax rates reflect the added capital risk investors and business owners take. We can clearly see the preferred taxation rates afforded on small business income and at the general corporate tax rates on income over the small business limit, compared to the tax rate on interest income or that of employment income. That tax-preference also extends to investors of “riskier” allocations of capital in marketable securities such as stocks, bonds, mutual funds, and exchange traded funds, to name a few. The tax rates of less-risky investments (such as money market instruments) do not benefit from the capital gains tax-preferred inclusion rates. With the latest move, there is not much difference in earning eligible dividend income from Canadian resident corporations and from dispositions resulting in capital gains.

Some pundits have declared the move as a disincentive to capital and business investment and may encourage businesses to move into more tax-favoured jurisdictions outside Canada. The Federal government has promoted the change as impacting a very small overall percentage of investors, estimated at 0.13% of Canadian individuals and 12.6% of corporations. Further, the move has been argued by the Liberals as necessary to work towards “intergenerational fairness”.

How to prepare for the changes?

For now, advisors may want to start educating their clients about the basics of the changes, which starts with comparing the current inclusion rates with the new inclusion rates.

Individual investors with large unrealized capital gains will also likely ask if they should crystallize their capital gains before June 25th to save money on taxes in the long run. The assumption that selling now will result in overall savings will not be correct in all cases, however. There is an opportunity cost to paying taxes upfront, rather than deferring those taxes to a later year.

For example, let’s assume an Ontario client owns a $2.5 million non-registered equity portfolio with $2,000,000 in unrealized capital gains. They had no intention of selling those investments for another 5 yeas, but in light of the upcoming changes, they are considering selling immediately, paying the capital gains taxes now, then reinvesting the net amount after taxes back into those same investments for the 5-year investment period. They are currently in the top marginal tax bracket in Ontario (53.53%) and expect to continue to be in 5 years’ time. The assumed average rate of return on their investments is 6% annually over the next 5 years.

As can be seen in this example, at 6% annual compound growth rate, the option to realize much of the capital gains now resulted in a higher overall return in the amount of $61,992.66 over the 5-year period due to the lower inclusion rate. Alternatively stated, if the investor does not crystallize the gains today, the equivalent rate of return needed to have the exact net after tax amount at the end of the 5-year period (the “breakeven return”) would be a 6.60% compound annual return. While this certainly will not be true in all cases, this is the sort of analysis that will have to be conducted when assessing whether it makes sense to realize capital gains in 2024. The rate of return on investment and the investment horizon, among other things, are important determining factors.

Although we used securities investment in our example, a similar analysis can be done for other kinds of property held, such as a vacation property that is unlikely to benefit from the principal residence exemption. In addition, taxes often take a back seat to other planning considerations. These conversations should be had with the primary goals of the client in mind, which may supersede tax planning considerations.

For corporate investors, it will be important to emphasize the impact the capital gains inclusion increase will have on small business owners. As a refresher, a corporation is a separate legal entity from the shareholders who own it and is subject to tax on the income it generates. Income is first taxed within the corporation before it can be passed to the shareholders in the form of dividends out of its retained earnings. To avoid double tax on income that passes through a corporation to shareholders (and to prevent any unintended tax advantages), a dividend gross-up and tax credit model is applied at the individual level, along with a tax refund mechanism to the corporation on passive investment income. This is designed to integrate the tax system between the two entities: individual and corporation. Ideally, perfect integration is achieved when after-tax income is equal, whether it is earned individually or through a corporation. In reality, depending on the province and type of income earned, there could be a tax cost in earning passive investment income through a corporation, including earning passive investment capital gains income. Currently there is a tax cost of earning capital gains income through a corporation across all Canadian provinces/jurisdictions.

The latest change further increases the cost of earning passive investment income inside a corporation, though we do not yet know what changes will be made to the corporate tax refund mechanisms. As noted in the table below, the increase averages approximately 8.43% and closely equates the rate on eligible dividends. This rate reflects the initial tax rate on passive investment income earned within an active business.

For many small businesses, and perhaps to long-term individual investors, this increase in the tax rate will feel unfair as the accumulation of earning a pool of assets for retirement is often done within their small business corporation, and in many cases the sole source of retirement funds.

If an immediate crystallization of accumulated capital gains is not desired, what should investors consider in the longer run? Although many details of the new proposed rules are yet to be clarified, here are some general considerations.

For individuals, it may be helpful to plan the timing of future dispositions to stay below the annual $250,000 threshold. Also, it may seem obvious but maximizing investments within registered plans, including the new first home savings plan (FHSA) where eligible, can reduce exposure to future capital gains tax. Moreover, estate planning becomes even more important as the potential tax payable on the deemed disposition of capital property at death rises. On that front, strategies to reduce capital gains at death could be considered, such as inter-vivos gifting, charitable donation, spousal rollover, and acquiring life insurance to provide sufficient liquidity to the estate.

For business owners, some strategies to limit future capital gain exposure may include contributing to an individual pension plan (IPP), conducting an estate freeze to pass on future capital gains to succession owners, and ensuring the small business shares qualify for the LCGE. The suitable strategies are highly dependent on the business needs and personal situation of the business owner.

Acting too soon or not fast enough?

Finally, there is what many in the industry have been calling a “change of law” risk. That is, within the next year and a half, a federal election is scheduled, and this capital gains inclusion tax policy will surely be a primary election issue. As part of that election platform, parties may promise to repeal it outright or alter its scope and application. Consider also that any changes in the capital gains inclusion rate could be retroactive or simply not apply in all cases.

The information provided is general in nature and may not be relied upon nor considered to be the rendering of tax, legal, accounting or professional advice. Invesco Canada is not providing advice. Readers should consult with their own accountants, lawyers and/or other professionals for advice on their specific circumstances before taking any action. The information contained herein is from sources believed to be reliable, but accuracy cannot be guaranteed. Commissions, trailing commissions, management fees and expenses may all be associated with mutual fund investments. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. Please read the simplified prospectus before investing. Copies are available from your advisor or from Invesco Canada Ltd

Date posted: May 23, 2024 - [pdf] Equitable GIF Contract Provisions and Information Folder

-

Clients could win $5,000 in Equitable’s New Year’s Resolution, New Year’s Contribution Contest!

Equitable® wants to help clients achieve their financial goals in 2024.If they win, you win! The draw will be held March 20, 2024.

Clients could win $5,000 and you could win $1,000 in Equitable’s New Year’s Resolution, New Year’s Contribution Contest.

How it works:

The client makes a contribution between January 1 and February 29, 2024 to one or more of these accounts:

Equitable is dedicated to offering clients the products, the services, and the choices that best suit their needs. We provide multiple sales charge options, three distinct guarantee classes, and a diverse selection of investment funds.

Speak to your Regional Investment Sales Manager to learn more.

Posted: December 14, 2023

® denotes a registered trademark of The Equitable Life Insurance Company of Canada.

Equitable’s New Year’s Resolution, New Year’s Contribution Contest: No purchase necessary. Contest period January 1, 2024, to February 29, 2024. Enter by making a deposit to an Equitable FHSA, TFSA or RRSP during the contest period or by submitting a no-purchase entry. One prize for a total value of $5,000 CAD to be drawn on March 8, 2024, will be awarded. The servicing advisor for the policy to which the selected entrant made the deposit is also an eligible winner and will receive a $1,000 CAD prize. For example, if an Equitable client is a winner of the $5,000 prize, the client’s servicing advisor wins a $1,000 prize. Open to legal residents of Canada of the age of majority. Odds of winning depend on number of eligible Entries received during the Contest Period. For full contest rules, including no-purchase method of entry, see the full contest rules. -

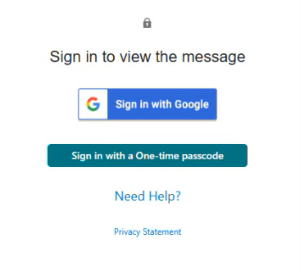

New secure encryption process for outstanding Equitable S&R business requirements

The Equitable® Savings and Retirement Operations team is improving how they send secure email messages to advisors. These emails are sent when there are outstanding requirements for an application or missing information for requests.

Previously, advisors had to manually password protect or unlock PDF documents. This caused delays and difficulties for recipients. The new encryption process will remove that confusion and make it easier for advisors to send and receive secure, encrypted messages.

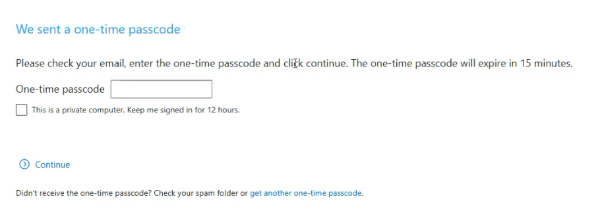

Advisors will now receive secure, encrypted emails from the QA annuity operations mailbox. These emails will use an encrypt option to protect personal client information, such as attachments or requests for personal documents. Recipients will get an email with a subject line saying they have a secure private message. They will need to sign in to view the message or choose to get a one-time passcode (OTP).

Please ensure to check the SPAM folder for the OTP option as it will expire in 15 minutes. Enter the OTP in the secure message

portal.

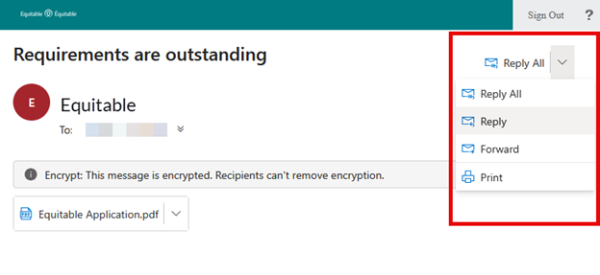

Emails are sent in both English and French, with automatic translation based on browser settings. Recipients must click the view button to access the message in the secure web portal where they can see the encrypted attachment.

Make sure to click Reply in the top right corner of the encrypted message to keep communications within the secure portal.

For more information or assistance, please contact your Director, Investment Sales.

Date posted: May 22, 2025 - Sales Illustrations

-

December 2023 eNews

Insights on EZBenefits from our Executive Vice-President, Group Insurance

When it comes to advising small business owners, it can be tough to find the right group benefits solution. Offering a competitive benefits plan is more important than ever to help small business owners attract and retain talent. They need an affordable solution that’s easy to implement, renew and maintain.

That’s why we launched EZBenefits for small business earlier this year. It’s a unique group benefits solution designed with you and your small business clients in mind.Marc Avaria, Executive Vice-President, Group Insurance, explains:

Find out more

Visit info.equitable.ca/EZBenefits for more details or to request a quote. If you have questions, contact your Equitable Group Account Executive.

Now that cold and flu season is here, many Canadians will start calling in sick or missing work to visit their doctor – if they can get an appointment. Now’s the time to remind your clients that Equitable offers Dialogue Virtual Healthcare. It can be added to any Equitable plan for an additional cost.

Supporting plan members through cold and flu season with Dialogue Virtual Healthcare*

Eligible plan members and dependants receive fast, on-demand access to virtual primary medical care—24/7, 365 days a year. Available for a variety of non-urgent health concerns, Dialogue Virtual Healthcare can make it easier to navigate cold and flu season by providing:- Access to the largest, most experienced bilingual medical team in Canada,

- In-app prescription renewals and refills,

- Personalized follow-ups after each consultation, and

- An all-in-one patient journey to address health issues. This reduces long waits and means less time away for doctor appointments.

Benefits of Virtual Healthcare for plan sponsors

When your clients provide Virtual Healthcare for their plan members, they can help:- Drive employee engagement;

- Reduce absenteeism related to in-person medical appointments;

- Manage chronic health issues;

- Attract and retain top talent; and

- Build a healthier workforce.

Learn how it works

Adding Dialogue Virtual Healthcare to your clients' plans

To learn more about adding Virtual Healthcare to your clients’ benefits plans, contact your Group Account Executive or myFlex® Account Executive. You can also share this resource from Dialogue on managing cold and flu season.

The Canada Employment Insurance Commission and Canada Revenue Agency have announced the 2024 changes to Maximum Insurable Earnings, and premiums for employment insurance. The following changes to Employment Insurance (EI) will take effect January 1, 2024:

Changes to Short-Term Disability benefits calculations*

How does this affect your clients?

To comply with client policy provisions, Equitable will revise Short-Term Disability (STD) benefits with the updated maximums based on the percentage of EI Maximum Weekly Insurance Earnings for policies that meet these conditions:- Policies that include a STD benefit that is tied to the EI Maximum Weekly Insurable Earnings, and

- Policies with a classification of employees that has less than a $668 maximum.

- The additional premium for any increase from their previous STD amounts and new STD amounts will be shown on your clients’ January 2024 Group Insurance Billings (as applicable).

If your clients wish to provide direction regarding revising their STD maximum, or have questions about the process, they can email Kari Gough, Manager, Group Issue and Special Projects.

*Indicates content that will be shared with your clients. - [pdf] How to access in-force illustrations

-

February 2020 Advisor eNews

In this issue:

Provincial biosimilar update

Legislative changes for Alberta’s Coverage for Seniors program

Coming soon: enhancements to Equitable EZClaim® Online

Provincial biosimilar update

Alberta Biosimilar Initiative

On December 12, 2019, the Alberta government introduced the launch of the Alberta Biosimilar Initiative. This program will require patients using several originator biologic drugs to switch to a biosimilar, and patients using a non-biologic complex drug (NBCD) to switch to its subsequent entry version before July 1, 2020 in order to maintain coverage.

Biologics are drugs that are engineered using living organisms like yeast and bacteria. The first version of a biologic developed is also known as the “originator” drug. Biosimilars are highly similar to the originator drug they are based on and have been shown to have no clinically meaningful differences in safety or efficacy.

Alberta Health will initially cover both the originator and biosimilar or subsequent entry version of a NBCD drug as patients start the switching process.

The following table outlines the affected originator drugs, their biosimilars or subsequent entry, and the conditions affected by the program.

Biosimilar Drug Originator Biosimilar/Subsequent Entry Indications Affected etanercept Enbrel Brenzys Ankylosing Spondylitis

Rheumatoid ArthritisErelzi Ankylosing Spondylitis

Psoriatic Arthritis

Rheumatoid Arthritisinfliximab Remicade Inflectra

RenflexisAnkylosing Spondylitis

Plaque Psoriasis

Psoriatic Arthritis

Rheumatoid Arthritis

Crohn’s Disease

Ulcerative Colitisinsulin glargine Lantus Basaglar Diabetes (Type 1 and 2) Filgrastim Neupogen Grastofil Neutropenia pegfilgrastim Neulasta Lapelga Neutropenia glatiramer* Copaxone Glatect Multiple Sclerosis *Glatiramer is a non-biologic complex drug where the originator is Copaxone and the subsequent entry is Glatect.

Equitable Life is actively investigating the benefit, risk and appropriate plan changes associated with this new policy on private drug plans and will keep you informed.

For more information about the Alberta Biosimilars Initiative, consult the Alberta government website.

British Columbia

In 2019, BC Pharmacare introduced a Biosimilars Policy that impacted coverage of three biologic drugs – Remicade, Enbrel and Lantus. As of November 25, 2019, these drugs were no longer eligible in BC for most conditions for which lower cost biosimilar versions are available. Patients in the province with these conditions were required to switch to biosimilar versions of these drugs in order to maintain their coverage.

The second phase of the BC Biosimilar Policy takes effect March 6, 2020 when Remicade will be delisted for Crohn’s Disease and Ulcerative Colitis. Patients in the province with these conditions will be required to switch to Inflectra or Renflexis in order to maintain their coverage.

Biosimilar Drug Originator Biosimilar Indications Affected infliximab Remicade Inflectra

RenflexisCrohn’s Disease

Ulcerative ColitisWe have communicated with the affected plan members, informing them of the need to switch medications. If plan members have any questions or concerns, our Customer Care team is here to help and support them through the transition.

If you have any questions about this policy, please contact your Group Account Executive or myFlex Sales Manager.

Ontario

In November 2019 Ontario Minister of Health Christine Elliot indicated that the government was planning to launch consultations to explore solutions in managing biologics.

Equitable Life will continue to monitor these developments and keep you informed of any impact on private drug plans.

Legislative changes for Alberta’s Coverage for Seniors program

The government of Alberta has announced that as of March 1, 2020, seniors’ family members (such as spouses and dependents) who are younger than 65 will no longer be covered by the provincial Coverage for Seniors program. Albertans 65 years of age and older will continue to be covered under the provincial plan.

Equitable Life plan members and their dependents will continue to be covered under the parameters of their group benefits plan.

For more information, please see the Alberta Seniors Health Benefits website.

Coming soon: enhancements to Equitable EZClaim® Online

Faster vision claims processing and payment

Equitable Life will soon provide real-time processing of vision claims submitted via EZClaim Online.

This means plan members will be able to find out the status of their vision claim almost instantaneously. And, for approved claims, they will receive payment even sooner – often in as little as 24 hours.

In order to allow for instantaneous processing and faster payment, plan members will be prompted to enter some additional information including the practitioner’s name, the date of the expense, the type of expense and amount of the expense when submitting their claims for these services.

Equitable Life plan members can submit all vision claims via EZClaim, including coordination of benefits and Health Care Spending Account claims.

This enhancement will be coming to our EZClaim Mobile app in the coming months.

New printable claims extract

As part of our ongoing efforts to improve customer experience for plan members, we will also offer a claims extract in a printable format within the plan member site. Plan members will be able to select a date range and claimant, then generate and download a detailed list of health and dental claims. This is a helpful way to keep track of claims, especially when reviewing them in preparation for income tax filing.

Once these enhancements are live you will be notified in an eNews, and an announcement will be posted on the plan member section of EquitableHealth.ca.

Elimination of Out-of-Country Travellers Program in Ontario

Effective January 1, 2020, the Ontario government eliminated OHIP coverage for emergency services for Ontarians travelling outside of Canada.

Previously, the Out-of-Country Travelers Program provided some reimbursement for services required to treat conditions that are acute, unexpected, arose outside Canada and require immediate treatment. The program covered between $200 and $400 per day for inpatient services and $50 per day for outpatient and doctor services.

For groups who have out-of-country coverage from Allianz, this change will not impact the cost to your plan members, or the process plan members follow in the event of an emergency while travelling.

Plan members should still call Allianz in the event of an out of country emergency. Allianz will deal with their claim as usual and will now pay for the portion of the claim previously paid by OHIP. Plan members will not have any additional out-of-pocket costs.

We will be sharing this information with plan members as a news item on our plan member website, equitablehealth.ca.

- [pdf] Path to Success - Objections: Anticipating the Objections Your Clients My Have

- Path to Success Module 3