Retirement Savings Plan (RSP, LIRA, RIF, LIF)

WHAT'S NEW

The Home Buyer’s Plan is offering temporary repayment relief for qualifying withdrawals from their RRSP.

Learn MoreRetirement Savings Plan

Government income programs make up part of a retirement plan, but they do not provide the level of income that most Canadians look for during retirement. A Retirement Savings Plan (RSP) is one of the best ways to help ensure your financial security. You may also know it as a Registered Retirement Savings Plan (RRSP). Only when it is set up with Canada Revenue Agency (CRA) is it called a RRSP. Around for over 60 years, the tax structure allows you to defer paying income tax on your deposits and earnings. It is only when you withdraw the money that tax is applied. Since many Canadians have a higher tax rate during their working years than retirement years, this often results in overall tax-savings.Notable features

- • Annual limit contribution – 18% of earned income (subject to the annual contribution limit)

- • Unused contribution room – Carried forward from year to year

- • Home Buyers' Plan

- • Lifelong Learning Plan

- • Income splitting

- • Retirement Income Fund

You can locate your maximum contribution limit by looking on your most recent Notice of Assessment. This Notice is issued from CRA. This maximum amount is based on 18% of your previous year’s earned income, up to the maximum RSP contribution limit. It also includes any unused contribution room from previous years. If you are a member of a pension plan, your pension adjustment will reduce the amount you can contribute to your RRSP. Unused contribution room can be carried forward and used in future years.

Contributing to an RSP

RSP contributions can be made during the tax year or within the first 60 days of the following tax year. Contributions can also be made monthly. When you contribute monthly, you benefit from something called dollar cost averaging. Dollar cost averaging is an investment strategy. Deposits of a fixed-dollar amount are made at regularly scheduled intervals. This means that you make regular purchases and your costs are averaged over the year. This benefits you in two ways. One is that this helps reduce the impact of a bumpy market. And two, your contributions are compounding over the year, making your money work that much harder for you. Making retirement savings a financial priority can help you achieve your desired retirement income.Products that offer an RSP

- • Guaranteed Interest Account

- • Pivotal Select segregated funds

.png)

| Target audience | Message | Download |

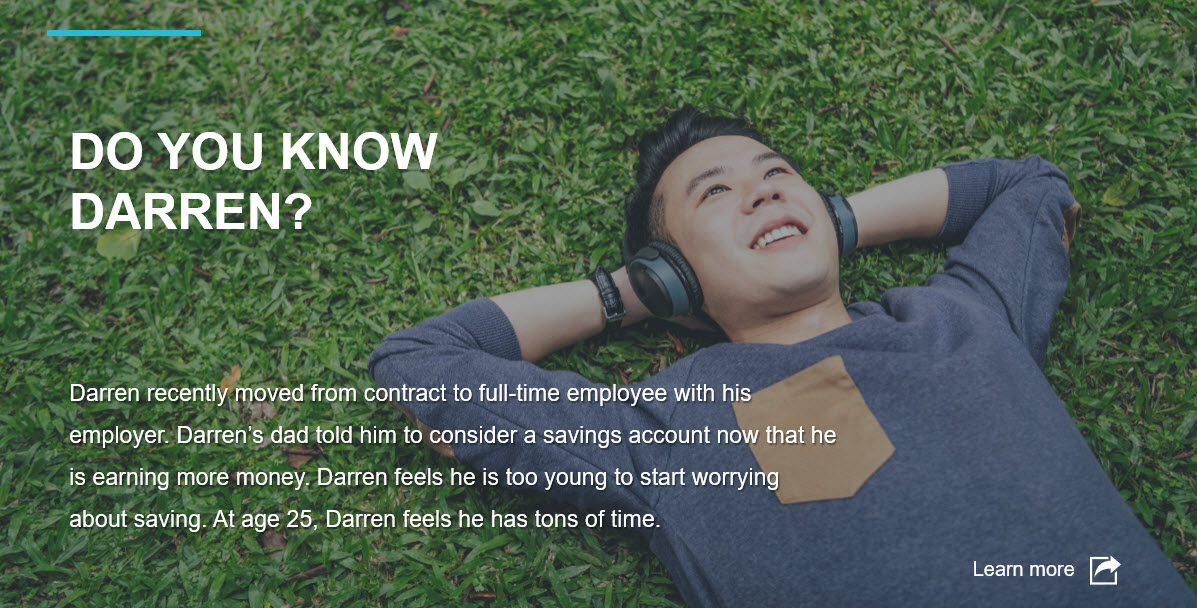

18 to 34 |

Are you on the right track financially? Someone once said, pay yourself first. A great idea but you know, and I know, that often we are the last to get paid. Bills, student loans, rent are often the priority, but did you know there is a way to pay yourself first? |

|

|

35 to 50

|

Are you financially on track for retirement? Most of us realize that it is in our best interest to save for retirement. We put aside money when we can, but often we are unsure if we will have enough saved in order to achieve a financially secure retirement. |

|

51 to 70

|

There is still time to figure it all out No doubt your plans for retirement have changed several times over the years. I suspect your retirement plans have taken a backseat more years than you care to count. Well good news, there’s still time. |

|

| Form Number | Cover | Marketing Material Name | Available Languages | Product |

|---|---|---|---|---|

| 0799 |

Daily/Guaranteed Interest Account Application - Registered/Non-Registered

File

Submit this request digitally via EZcomplete for faster processing. |

FR | ||

| 1384 |

Pivotal Select Application - Registered/Non-Registered

File

Submit this request digitally via EZcomplete for faster processing. |

FR | ||

| 1673 |

RRSP to RRIF Conversion Form

File

Submit this request digitally via EZtransact for faster processing. |

FR |

| Form Number | Cover | Marketing Material Name | Available Languages | Product |

|---|---|---|---|---|

| 2125 |

|

Another reason to invest with Equitable

File

In case you need another reason, Equitable is a member of Assuris. Assuris is an independent, not for profit, industry-funded organization that protects contractholders, should their insurance company fail. |

FR | |

| 1965B |

|

Personalized Ads - Facts & Figures

File

Equitable is pleased to offer you professionally designed personalized ads to advertise. |

FR | |

| 1357 |

|

Managing a Retirement Savings Plan tax refund

File

If you have ever received a tax refund you will know the dilemma that comes when that money hits your bank account. The initial reaction is to spend it on something for you; and why not! You have worked hard all year and deserve a reward! |

FR | |

| 1355 |

|

A Retirement Savings Plan is just as relevant now as it was over 60 years ago

File

Yes, that old thing. With the popularity of the Tax-Free Savings Account, the Retirement Savings Plan (RSP) does not seem to evoke the same wow factor it once did. An RSP from Equitable Life can support your goal of home ownership, further education, and retirement. |

FR | |

| 1965 |

|

Facts & Figures

File

TFSA Contribution Limits, RRSP Contribution Limits, TOP Marginal Tax Rates, Retirement Income Fund Minimum, Canada Pension Plan Benefits. |

FR | |

| 1583 |

|

Make your money work for you

File

We all know a Retirement Savings Plan (RSP) is a great way to save for retirement. When we make an RSP contribution we receive an immediate tax refund. |

FR | |

| 1613 |

|

Online banking makes saving simple.

File

Did you know clients can make additional deposits to their Equitable savings plan through their financial institution’s online banking service? |

FR | |

| 1460 |

|

Personalized Ads - What does your retirement bucket list include?

File

Equitable is pleased to offer you professionally designed personalized ads to advertise the benefits of an Equitable RSP. |

FR | |

| 1551 |

|

Pivotal Select Guarantee Fees

File

One of the most attractive features of segregated funds is the guarantees that are embedded into the product. (Available in PDF only) |

FR | |

| 1354 |

|

Borrowing money to save money

File

Have you ever considered borrowing money to contribute to your Retirement Savings Plan (RSP)? No? Well consider this. Unlike credit card debt, RSP loans are considered “good debt”. Investment loans and mortgages fall into the “good debt” category because they help to increase your net worth. |

FR | |

| 1910 |

|

Personalized Brochure - What did you wish for this year?

File

Equitable is pleased to offer you professionally designed personalized ads to advertise the benefits of an Equitable RSP. |

FR | |

| 1352 |

|

Retirement Realities

File

The perception of retirement has changed. You remember watching those commercials about the retired couple playing golf, yachting, or strolling down a sandy white beach. |

FR | |

| 1899 |

|

Taking money out of your RSP?

File

A Retirement Savings Plan (RSP) is an excellent way to save for retirement. Of course, it never fails that there is always that moment in life when you need extra cash. For those moments that require a large amount of money, think twice before pulling it out of your retirement savings. |

FR | |

| 1909 |

|

When it is time to convert your RSP to a RIF

File

The thought of retirement can be a blessing or can cause concern. The difference in attitude comes down to planning. If you have planned for retirement, congratulations. If you have not, you have got some work to do. |

FR |

| Article | |||

| You can start planning and saving for your retirement at any age Many of us know we should start early so our money has a longer time to grow. With the costs of buying a home, raising kids (and paying for their education), it may be hard to get going, let alone know where to begin. Here are four steps that will help you get started. |

.png?width=30&height=31 "facebook-(2).png") |

.png?width=30&height=30 "Twitter-(1).png") |

.png?width=30&height=29 "LinkedIN-(1).png") |

| If you’re like most people, the dollars you have for savings are not unlimited That means you have some decisions to make, including whether it makes more sense to pay down your mortgage quickly or invest in an Retirement Savings Plan (RSP). It’s true that reducing your mortgage quickly makes a lot of sense, but you’ll also need a significant nest egg if you want to retire in comfort. |

|

|

|

| How to choose between an RSP and a TFSA For years Canadians have utilized Retirement Savings Plans (RSPs) as the primary investment vehicle for retirement savings. With the introduction of Tax-Free Savings Account (TFSA), there has been great debate over where to invest: RSP or TFSA? Although the two account types share some common traits, there are some key differences. |

|

|

|

.jpg?width=150&height=76 "Do-you-know-Darren-(1).jpg")

.jpg?width=150&height=75 "Do-you-know-Alyssa-(2).jpg")

Notable Features

- Flexible income options (subject to government minimums and maximums)

- Competitive interest rates

- Choice of investment options

Products that offer a RIF and LIF

- Guaranteed Interest Account

- Pivotal Select

| Form Number | Cover | Marketing Material Name | Available Languages | Product |

|---|---|---|---|---|

| 1690 |

|

Converting Your Savings into Retirement Income

File

As you approach retirement you will need to develop an income strategy that provides you with dependable income throughout your retirement. |

FR | |

| 1845 |

|

Retirement Income Fund Understanding minimum withdrawal percentages

File

The federal government has set minimum withdrawal percentages for a Retirement Income Fund (RIF). The minimum withdrawal is based on age at the beginning of the year and the value of your fund on December 31 of the previous year. (Available in PDF only) |

FR | |

| 1909 |

|

When it is time to convert your RSP to a RIF

File

The thought of retirement can be a blessing or can cause concern. The difference in attitude comes down to planning. If you have planned for retirement, congratulations. If you have not, you have got some work to do. |

FR | |

| 1673 |

RRSP to RRIF Conversion Form

File

Submit this request digitally via EZtransact for faster processing. |

FR |