Site Search

899 results for access portal here MAKEMUR.com son locked up need him home today payment HMP Chelmsford

-

Let’s talk about Critical Illness insurance, the Equitable way.

Having critical illness insurance benefits in an important time of need is so valuable. Get the right critical illness insurance coverage for your clients.

In 2022, we made some significant updates to our EquiLiving® Critical Illness insurance plans to provide better choices and features for clients.

These significant updates included:

● The addition of Acquired Brain Injury as a covered condition

● The addition of 20 pay options allowing more choice when choosing the right plan for your clients

● The removal of the age restriction for juveniles to claim for Loss of Independent Existence

Plus, a Canadian first, the addition of Cloud DX. Cloud DX is a value-added service that provides remote patient monitoring to claimants in addition to the full critical illness benefit paid by Equitable Life®. Cloud DX delivers medical grade hardware directly to the client so that Cloud DX can remotely monitor their vitals to help ensure they are on and stay on the road to recovery.

View our new Critical Illness video on YouTube or Vimeo!

With these updates and more, EquiLiving Critical Illness Insurance is there for clients, not only at time of their claim but also during their recovery. To learn more about Critical Illness insurance, the Equitable way, contact your local wholesaler.

*Cloud DX is a non-contractual benefit and may be withdrawn or changed by Equitable Life® at any time. To be eligible for the Cloud DX offering, a claimant must be age 12 or older and have received payment on or after February 12, 2022 for a covered critical condition benefit under an individual critical illness insurance policy issued by Equitable Life. An early detection benefit payment does not qualify. Equitable Life pays for 6 months of Cloud DX subscription fees. If the claimant wishes to continue the Cloud DX service after 6 months, they will be responsible for the cost.

® and TM denote trademarks of The Equitable Life Insurance Company of Canada.

- Introducing Empathy – Compassion and care at time of loss

-

Short and long-term income solutions from Equitable Life

Do you have clients without a company pension plan, close to retiring and worried about outliving their savings? Have you talked to them about annuities? Maybe it’s time you did.

A payout annuity from Equitable Life® provides regular guaranteed income in retirement. Your clients can choose from

- Life Annuity – guaranteed income for life

- Joint Life Annuity – guaranteed income for two lives

- Term Certain – guaranteed income for a specific period of time (5 to 30 years)

- Term Certain to Age 90 – guaranteed income until age 90

There’s no need for your clients to worry about stock market fluctuations or changing interest rates, what better time to add an annuity to your client’s retirement savings strategy.

Payout annuities are an excellent solution for

- Converting your savings into retirement income

- Covering predictable fixed monthly expenses

- Providing lifetime income

For more information on payout annuities, please click here.

-

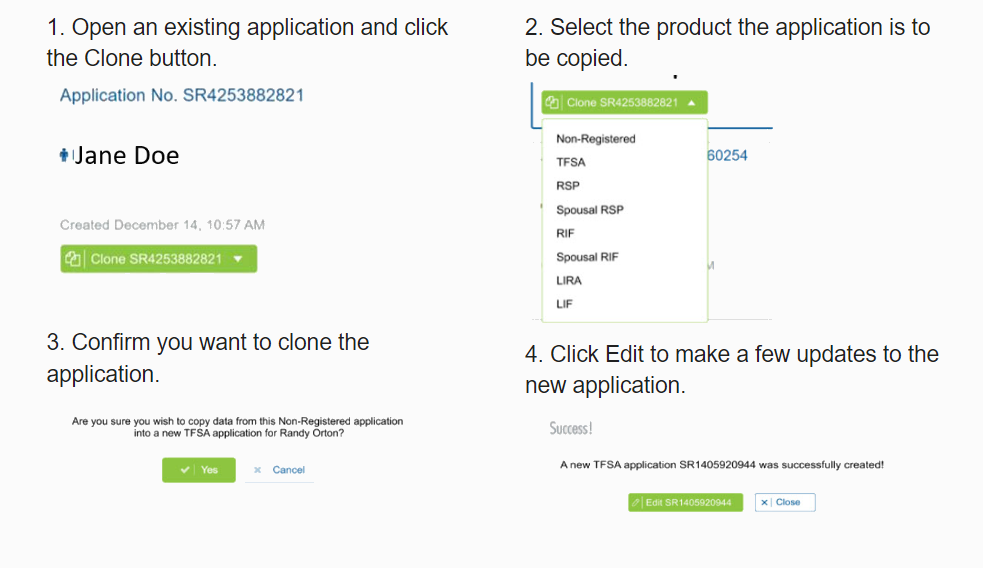

The new segregated fund EZcomplete cloning feature will save time and errors.

The new cloning feature for Savings & Retirement EZcomplete® applications means that advisors don’t need to enter the same client information when completing multiple applications for the same client.

Here's how easy it is to use.

.png "steps-(1).png")

Best of all, you can clone in progress and submitted applications.

This is just some of the information that will be automatically copied:-

Name

-

Date of birth

-

Gender

-

Occupation

-

Address

-

Phone numbers

-

Email address

-

Social Insurance Number

-

All beneficiary information

The new EZcomplete cloning feature will save advisors time and reduce errors..png?width=500&height=92 "sandbox-(3).png")

.png?width=500&height=92 "ezcomplete-(4).png")

.png?width=300&height=82 "sandboxtext-(2).png")

.png?width=300&height=39 "ezcompletetext-(1).png")

If you have any questions, contact your Regional Investment Sales Manager

® denotes a trademark of The Equitable Life Insurance Company of Canada.

Posted April 6, 2023 -

-

New rules in effect for all Quebec applications

The Quebec Regulatory Tribunal (AMF) made an important decision about selling insurance products to Quebec residents. As a result, Equitable® has changed its licensing rules for all future sales to clients in Quebec.

Effective on November 28, 2024, you must be licensed in Quebec to submit an application for a client who lives in Quebec. This requirement applies to all insurance and investment products.

Regardless of where the application is signed, if you meet with a client whose primary residence is in Quebec, you must be licensed in Quebec to submit on the client’s behalf.

If you are not licensed in Quebec, you will need to get licensed in Quebec for applications for Quebec clients to be processed.

What about licensing for clients outside of Quebec?

In all cases, we encourage you to be licensed in the province where a client lives to be able to do business or provide ongoing service.

Equitable is committed to providing solutions and service that is in the best interests of clients and advisors alike. We appreciate your continued support.

Questions?

Your Equitable Wholesaler is here to help.

You may also reach out to Advisor Services for more details. Email eastern-service@equitable.ca or call 1-800-668-4095.

® or TM denote trademarks of The Equitable Life Insurance Company of Canada. -

Group Benefits - Premium relief for Dental and Extended Health Care benefits

We know this is a difficult time for Canadian employers and that many of your clients are facing financial hardship as a result of the COVID-19 pandemic. We continue to look for ways to help employers manage while still supporting their employees.

With many health practitioners closing their offices due to the pandemic restrictions, plan member use of dental benefits and some health benefits has declined.

So, we are pleased to announce that we are offering premium relief for all Traditional and myFlex insured non-refund customers for Health and Dental benefits, as follows:

- A 50% reduction on Dental premiums; and

- A 20% reduction on vision and extended healthcare rates (excluding prescription drugs), which equates to an 8% reduction on Health premiums.

These reductions are retroactive to April 1, 2020 and will appear as a credit against the next available billing. We will assess the situation monthly and expect to continue with monthly refunds for as long as the current crisis period continues.

We expect that claims experience and premiums will return to normal once the current pandemic restrictions are lifted.

In the meantime, plan members will continue to have full access to their benefits coverage throughout the pandemic. In many cases, dental offices remain open for emergency services, and a variety of healthcare providers are available virtually.

Commissions

We know the pandemic has put financial strain on your business as well, so we will continue to pay full compensation. Although your overall commission will be unaffected by these premium reduction adjustments, you may see a temporary reduction in your commission payments if you are on a pay-as-earned basis while we put through mass changes. If so, we will then make an additional top-up payment to cover that shortfall as soon as we are able.

Communication

We will be communicating this premium relief program to your clients April 21st at 8:00am EST.

A PDF of the communication is also available here.Questions?

If you have any questions, please contact your Group Account Executive or myFlex Sales Manager. In the meantime, we have provided some Questions and Answers below.

Will the premium reduction on Health and Dental benefits have an impact on the renewals that were deferred?

No. Renewals will proceed as normal, with rate adjustments based only on months where full premium was paid. For most clients, we anticipate “normal” rate adjustments at renewal compared to rates paid prior to refunds taking effect.

Does this adjustment apply equally to clients who have had their renewal deferred?

Yes, these adjustments apply to all Traditional and myFlex insured, non-refund customers for Health and Dental benefits.

How does this affect clients who have terminated or amended a plan?

If a benefit is in-force during the month of April, the adjustment will be credited to the next available billing. For clients who have temporarily terminated all benefits, this will be applied against the first bill once benefits have been reinstated. No cash refunds will be paid.

Will you recover any of the adjustment at a future point in time?

No, we will not recover this adjustment.

Instead of this premium reduction adjustment, can a client cancel or adjust some of the benefits on their plan?

Yes, you and your clients always have the option of changing the coverage on a plan, such as reducing or removing a benefit to help control costs. Please speak to your Group Account Executive or myFlex Sales Manager about the options available.

Are TPAs and self-administered groups eligible for the premium reduction?

Yes. TPAs and self-administered groups are eligible for the premium reduction. However, timing for the credit will be dependent on the billing practices of the TPA or self-administered group. We will apply these credits as soon as we are able. -

April 2023 eNews

Vision care discounts from Bailey Nelson for Equitable Life plan members*

We are pleased to announce we are partnering with Bailey Nelson to provide Equitable Life plan members with discounts on prescription and non-prescription eyewear. Bailey Nelson is a leading provider of prescription glasses, contact lenses and sunglasses with locations across Canada, as well as an online store.

All Equitable Life plan members will have access to the following discounts from Bailey Nelson:

*Includes anti-reflection and anti-scratch treatment. Glasses offers are based on 2 pairs of single vision or 1 pair of premium progressive lenses. Lens add-ons, such as high-index lenses and prescription tinted lens tints may involve additional costs.

**Non-prescription glasses only. Cannot be combined with 2 for $200 discount.

Plan members can provide their Equitable Life discount code in-store or at online checkout. Your clients may wish to distribute this convenient flyer with an overview of the available discounts to their plan members.

Plan members can bring their prescription to a Bailey Nelson location or provide it online to order glasses and contact lenses. Bailey Nelson also provides eye exams in-store for $99.

If you have any questions, please contact your Group Account Executive or myFlex Sales Manager.

Equitable Life helps tackle benefits fraud through Joint Provider Fraud Investigation (JPFI) initiative*

Protecting your clients’ plans is important to us. That’s why Equitable Life is working with other Canadian life and health insurers to conduct joint investigations into health service providers that are suspected of fraudulent activities through the Canadian Life and Health Insurance Association’s (CLHIA’s) Joint Provider Fraud Investigation (JPFI) initiative. This collaborative initiative between major Canadian life and health insurers through the CLHIA is a major step toward reducing benefits fraud in the life and health benefits insurance industry.How the JPFI works

The JPFI builds on the 2022 launch of a CLHIA-supported industry program. The program uses advanced artificial intelligence to help identify fraudulent activity across an industry pool of anonymized claims data. Joint investigations will examine suspicious patterns across this data.

Through this project, Equitable Life can initiate a request to begin a joint fraud investigation when we:- See suspected provider fraud in our own data or the pooled data, or

- Receive a substantiated tip about potential provider fraud

How Equitable Life protects your clients’ benefits plans from fraud

Benefits fraud is a crime that affects insurers, employers and employees and puts the sustainability of workplace benefits at risk. CLHIA estimates that employers and insurers lose millions each year to benefits fraud and abuse.

Our Investigative Claims Unit (ICU) consists of security and fraud experts who use data analytics and artificial intelligence to proactively identify and investigate suspicious billing patterns or claims activity to open investigations. We de-list healthcare providers who are engaged in questionable or fraudulent practices, pursue the recovery of improperly obtained funds, and report practitioners to regulatory bodies and law enforcement where appropriate.

Learn more about benefits fraud, or contact your Group Account Executive or myFlex Sales Manager for more information.Second phase of TELUS eClaims transition*

In June 2022, we switched to TELUS Health eClaims as our digital billing provider to give our plan members a faster and more convenient option for submitting paramedical and vision claims. The switch has allowed our plan members to take advantage of TELUS’s extensive network of over 70,000 paramedical and vision providers.

We’ve now begun the second phase of our TELUS Health eClaims implementation. This phase will focus on improving the experience for paramedical and vision providers. We will begin issuing reconciliation statements for the claims they submit on behalf of their patients. These statements will make it easier for them to use the TELUS Health eClaims portal and provide incentive for even more providers to sign up.

Please encourage your clients to remind their plan members about this convenient option. We have created a helpful one-pager that plan members can bring with them next time they have an appointment with their healthcare provider.

If you have any questions about TELUS Health eClaims, please contact your Group Account Executive or myFlex Sales Manager.

Changes to STD application process for COVID-19 cases*

As the COVID-19 situation evolves, we continue to adjust our disability management practices to ensure ongoing support and a fair experience for all our plan members.

As of May 1, 2023, we will begin managing COVID-19-related short-term disability (STD) claims the same way that we manage disability claims for any other illness or condition. If a plan member is unable to work due to COVID-19 symptoms or a positive COVID-19 test, they must now use the standard STD application, including the Attending Physician Statement portion.

Once we receive the claim, we will adjudicate it according to our standard process.

If you have any questions, please contact your Group Account Executive or myFlex Sales Manager.

* Indicates content that will be shared with your clients.

- [pdf] Payout Annuity Interest Rate Guarantees (Advisor)

- [pdf] myFlex Options Guide

-

Flexibility for a client’s ever-changing life

Term life insurance offers full and partial conversion options to meet changing needs

Life is always changing—whether a client is buying their first home, welcoming a new baby, or sending the kids off to college. While most clients think of term life insurance as a solution to meet a temporary need, they don’t necessarily consider the power of term conversion options to meet their future needs.

Full and partial conversion options can help meet a client’s needs as their life journey and insurance needs change, without having to provide proof of continued good health.

Full conversion:

• With full conversion, clients can convert all of their term coverage from their policy or rider to permanent life insurance. This allows the client to lock in a level premium rate for life.

Partial conversion:

• With a partial conversion, clients can convert a portion of their term coverage from their policy or rider to a permanent plan. This allows them to help cover off both a short-term need and also provides lifetime protection.

Did you know?

Our partial conversion with a term rider carryover is now more flexible than ever. Read more about it here!

For more information, please consult the Equitable Term Life insurance admin guide.