Site Search

656 results for open now MAKEMUR.com how to get inmate released early for money Federal Detention Center Oakdale

- Sales Illustrations

-

Regulator Reviews of Advisor Business Practices

The Financial Services Regulatory Authority of Ontario (FSRA) began targeted life agent examinations in 2021 as part of its Market Conduct: Life and Health Insurance Agent Supervision Framework. In March 2022, FSRA released its industry report which included a summary of the top regulatory violations or business practice gaps identified during those reviews, which included:

● Agent Disclosure – failure to ensure proper disclosure to clients regarding the insurers that the agent is authorized to represent, conflicts of interest or potential conflicts of interest and agent compensation;

● Continuing Education Credits – failure to complete CE credits as required or misrepresentation to the regulator regarding completion;

● Failure to complete the Life Insurance Replacement Declaration with clients when replacing an existing insurance policy;

● Missing or inadequate financial needs analysis and/or risk assessment (wealth) and insurance needs analysis;

● Missing or inadequate Reasons Why Letters for insurance recommendations;

● Missing evidence of policy illustrations;

● Missing or inadequate AML/ATF programs; and

● An overall lack of adequate notes to document client conversations and support recommendations made.

While these reviews are focused on agents licensed in Ontario, the review findings are helpful for all licensed advisors to ensure your business practices are aligned with regulatory and industry standards. Following these standards also helps you meet Equitable Life’s Advisor Code of Conduct. FSRA’s full report includes a copy of the Insurance Agent Market Conduct Questionnaire and can be viewed at https://www.fsrao.ca/newsroom/new-life-and-health-agent-supervisory-framework-enhances-consumer-protection.

-

Equitable Life Group Benefits COVID-19 Update

The test of a great partner is one who stands tall when you and your clients need to rely on them most. As the COVID-19 pandemic continues, we thought you might find it helpful to have a summary of where we are during this crisis.

You can download this PDF version to refer to when meeting with your clients.

We are here with you and for you

We’ve taken several steps to support you, your clients and their plan members during this crisis, including:

- Providing premium refunds for insured, non-refund Health and Dental benefits;

- Waiving the waiting period for short-term disability claimants who tested positive for COVID-19;

- Extending out-of-country travel coverage for plan members who were unable to return to Canada;

- Providing increased flexibility for premium payments; and

- Keeping you and your clients informed with timely Q&As and announcements, webinars, and insights into the impact of COVID-19 on benefits plans.

As well, to commemorate our 100th Anniversary this year, we donated $4.5 million to purchase and install a new MRI for Grand River Hospital. And we donated $50,000 – $10,000 each – to five charities in British Columbia, Alberta, Manitoba, Ontario and Quebec. For more information about our celebrations, check out our website at www.equitable100.ca.

We have adjusted our business to become digital

Our business is near 100% digital, so the vast majority of our employees are now working remotely from home and are fully functional. Since the pandemic began, our IT and operations teams have digitally enhanced more than 20 different processes and services to make it easier for us to integrate with our distribution partners in this new reality.

We pride ourselves on our customer service

In 2019, our dedication to customer service was recognized with outstanding survey results.

- In a 2019 survey of customers from 15 life insurance companies,1 Equitable Life ranked #1 on the Net Promoter Score, a measure used across industries to gauge the loyalty of a firm's customer relationships; and

- A survey of Group consultants, brokers and third-party administrators 2 ranked Equitable Life in the top two insurers across all categories.

For 2020, we continue to deliver service at the same level with no disruptions during this crisis. Our Customer Care Centre remains open to support plan members and can be reached at 1.800.265.4556. And our Client Relationship Specialists are available for Plan Administrator questions and support.

We are financially strong and stable

We remain financially strong and continue to focus on meeting the needs of Canadians. At the end of the first quarter, our Life Insurance Capital Adequacy Test (LICAT) ratio is at 152.5%, well above our goal and the regulatory requirement.

As the global situation continues to evolve, rest assured that Equitable Life is unwavering in our commitments to you and the communities we serve. We are here with you and for you. Please contact your Group Account Executive or myFlex Sales Manager if you have questions or need assistance.

1 LIMRA CxP Customer Experience Benchmarking Program, Life Insurance In-Force Experience 2019

2 NMG Consulting’s Canadian Group Benefits Survey 2019

- [pdf] Segregated Fund Semi-annual Report - June 30, 2025

-

May 2023 eNews

Update: Introducing changes to our Diabetes Management Program

Beginning June 1, 2023, we are introducing additional standard drug plan controls as part of our Diabetes Management Program.

The controls will apply to GLP-1 agonists approved by Health Canada for the treatment of diabetes, such as: Adlyxine, Mounjaro, Ozempic, Rybelsus, Trulicity, and Victoza.

This change will help manage the impact of these high-cost diabetes medications for your clients while continuing to provide plan members with access to effective treatments to manage their disease.

Why are we introducing this change?

GLP-1 agonists are the highest cost diabetes drugs on the market. Current Diabetes Canada Clinical Practice Guidelines recommend that most Type 2 diabetics begin treatment with lower-cost and equally effective first-line therapies, such as Metformin.

Some GLP-1 agonists are also used “off-label”. In other words, they are often prescribed for conditions for which they have not been approved by Health Canada, such as weight loss.

These additional controls will help ensure that these drugs are used appropriately – only for the treatment of diabetes and only after other first-line treatments have been tried.

If a client wishes to provide coverage for drugs specifically approved by Health Canada for weight loss, we have coverage options available.

How will this program work?

Plan members who receive a new prescription for a GLP-1 agonist will need to try a first-line diabetic treatment before they are eligible for coverage of the GLP-1 agonist. If the plan member has previously tried first-line therapies and found them ineffective, they will be eligible for a GLP-1 agonist.

Plan members who are already taking a GLP-1 agonist to treat diabetes will continue to be eligible for coverage. Some claimants may need to provide confirmation of their diabetes diagnosis from their physician or pharmacist in order to maintain coverage. We will provide claimants ample time to confirm their diagnosis.

Questions?

If you have any questions about these additional standard controls or how they will impact your clients, please contact your Group Account Executive or myFlex Sales Manager.

Coming soon: Survey for plan administrators with recent disability claims

We are regularly enhancing our communication processes to help your clients with disability plans manage their workplace absences more effectively. Later this month, we will distribute a short survey to plan administrators who have submitted a disability claim in the past six months. The survey will ask recipients about their satisfaction with the frequency and detail of our disability management communications.

The email will come from GBClientFeedback@equitable.ca, and the survey will remain open until the end of the day on May 19, 2023. All responses will be confidential. Survey respondents will receive the option to provide their contact information so that we can follow up on feedback they have provided.

We plan to use the feedback to help ensure that we’re meeting your clients’ expectations and delivering industry-leading service.

In a previous issue of eNews, we published a list of the average dental fee increases for general practitioners based on the latest Provincial and Territorial Dental Association fee guides.

Since then, the Canadian Life and Health Insurance Association (CLHIA) has updated the 2023 dental fees for some provinces. Provinces with dental fee updates since our previous eNews are bolded and italicized. Equitable Life uses these guides to help determine the reimbursement limits for dental procedures. For your reference, below is the list of the average dental fee increases for general practitioners that will be used by Equitable Life for 2023.

-

EAMG - Macro Tear Sheet – Recent Market Volatility Summary

By separating the noise from the signals, we believe the rotation away from the mega-cap technology names is likely to continue. Recent market volatility, triggered by a multitude of factors that include the unwind of the carry trade, investor reactions to mixed mega-cap earnings, and U.S. economic data, may present more investment opportunities for long-term outperformance. Recall over the past year that the majority of U.S. stock market performance came from a limited number of mega-cap technology companies and, in our view, moving forward it will be prudent to analyze the source of returns as rapid market rotations may punish overly-concentrated portfolios.

Inflation Slows (July 11) – Headline U.S. inflation readings increased 3.0% year-over-year in June, decelerating from May (3.3%). With prices slowing ahead of forecasts but economic growth remaining strong, investors became more confident regarding the prospects of an economic soft landing.

Outcome: market strength broadened with traders rotating out of highly concentrated areas of the market (“Fabulous 5”) and into more economically sensitive stocks that had been left behind.

• Big Tech Earnings (July 23 – Aug 1) – High profile mega-cap technology companies – including many members of the Magnificent 7 – reported earnings growth that generally surpassed expectations as margins remained healthy. That said, investors were more focused on spending towards AI-initiatives, rewarding businesses with greater success translating their AI investments into higher sales.

Outcome: this trend is evident through the divergence of returns from IBM and Alphabet (Google’s parent company) after releasing their quarterly earnings. The limited number of companies that contributed to the returns of the S&P 500 failed to impress investors, extending the rotation into other areas of the market.

• Caution is Brewing – Following a strong rally of economically sensitive pockets of the market, notably a breakout of returns from U.S. small cap companies, the low volatility factor, which tends to outperform during times of stress, moved in sync with the small caps’ strength.

Outcome: with a lack of fundamental justification supporting small cap performance, markets showed signs of caution.

• Central Bank Decisions (July 31)– The Federal Reserve held interest rates unchanged during its July meeting, in line with market expectations, reiterating committee members’ need for greater confidence that inflation would continue to subside. That said, policymakers signaled a reduction in policy rates could be a possibility in the coming meetings. In contrast, the Bank of Japan (BoJ) increased its key interest rate while also announcing plans to scale back bond purchases – restrictive monetary policy maneuvers aimed at backstopping the depreciating Japanese currency.

Outcome: the bifurcation between the BoJ and most other major central banks sparked a sharp appreciation of the yen and a rapid unwind of the yen carry trade (see below for explanation).

• Growth Scare (August 2)– In early August, a downside surprise in U.S. nonfarm payrolls (114k actual versus 175k expected) and an increase in the unemployment rate to 4.3%, higher than the 4.1% that was expected and up from 3.5% a year ago triggered concerns of a cooling labor market.

Outcome: speculation swelled surrounding the pace of rate cuts with market participants expecting the Federal Reserve to cut rates as much as 125bps over the next 3 policy meetings, up from 50-75bps as of the end of July. Against this backdrop, the ongoing unwind of the yen carry trade accelerated.

Yen Carry Trade Explained

• Simply put, investors have been borrowing Japanese yen – a low yielding currency – to invest in higher-yielding foreign assets. The primary risks in a carry trade can include the uncertainty of foreign exchange rates (if unhedged), as well as changes to expectations of the underlying yields, among other risks. Over the last 2 decades, the BoJ has implemented an ultra-low interest rate monetary policy to combat deflation and stimulate growth. Furthermore, investors were emboldened by the Japanese yen’s ~53% depreciation versus the U.S. dollar over the last 10 years. With the BoJ hiking its key interest rate while also announcing plans to scale back bond purchases, the yen rallied abruptly. Consequently, highly leveraged investors have had to exit their long positions in riskier assets to repay their borrowed yen exposure.

Peak Carry Trade Unwind – Buying Opportunity

• Peak carry trade unwind, which implies heightened panic levels, has historically created an attractive buying environment. That said, we are focused on companies that have demonstrated robust earnings growth and healthy leverage. Given the unprecedented level of market concentration over the last year, we view the unwind of the carry trade as another catalyst for investors to rotate out of the “Fabulous 5”.

Our Findings:

We found that the peak unwind of the carry trade may be a buying opportunity. At present, the current level of the unwind is similar to many notable market bottoms, including the Great Financial Crisis (2008), the European debt crisis (2010), the oil crash (2014), the subsequent emerging market crisis (2015), the Covid-19 crash (2020), and the collapse of Silicon Valley Bank (2023). We assessed the degree of the unwind by looking at the one-month implied volatility between three currency pairs, U.S. Dollar/Yen, Australian Dollar/Yen, and Euro/Yen. Implied volatility is a measure of the expected future volatility of the underlying assets over a given time period. Amid strong earnings growth and steady margins from quality businesses within the U.S. market, the fundamental backdrop suggests that businesses outside the concentrated AI-darlings may drive the next leg of market returns.

Downloadable Copy

Mark Warywoda, CFA

VP, Public Portfolio ManagementIan Whiteside, CFA, MBA

AVP, Public Portfolio ManagementJohanna Shaw, CFA

Director, Portfolio ManagementJin Li

Director, Equity Portfolio Management

Tyler Farrow, CFA

Senior Analyst, Equity

Andrew Vermeer

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy. - Path to Success Module 1

- [pdf] Poster - What did you wish for this year?

-

Market Commentary July 2025

Key Takeaways

• Markets were very volatile in April to start Q2 but calmed as the quarter progressed. Volatility was driven mostly by headlines about tariffs, but other fiscal policy developments also had an impact.

• Equity markets sold off sharply at the start of the quarter, continuing Q1’s weakness. Markets rebounded sharply once worst-case fears over tariffs eased. The markets continued to rally through the quarter as trade negotiations progressed. Stronger-thanexpected corporate earnings also boosted markets. Despite the shaky start to the quarter, most global equity markets set new all-time highs in Q2.

• Canadian bond markets delivered slightly negative returns in Q2. Weak performance was driven by rising interest rates, which outweighed the impact of tighter credit spreads. Higher interest rates hurt the performance of longer-term bonds most.

• Both the Bank of Canada and the U.S. Federal Reserve adopted a wait-and-see approach. They each held rates steady during Q2, awaiting greater clarity on the impacts of tariffs on both growth and inflation before considering further cuts.

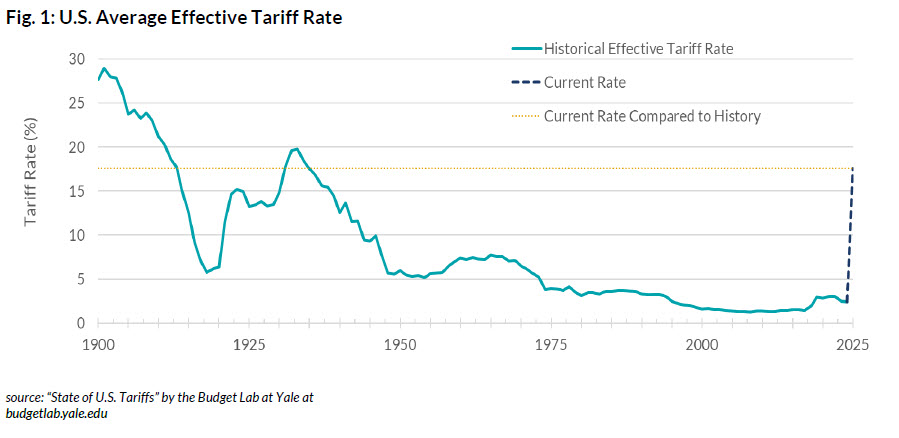

Economic and Market UpdateEconomic Summary: Most indicators of economic activity in the U.S. continued to expand at a decent pace. However, GDP data for the first quarter came in weaker than expected, as higher imports ahead of anticipated tariffs and weaker spending by consumers weighed on Q1 GDP. That said, GDP growth is expected to bounce back in Q2. Tariffs will likely continue to be an evolving story, with potential impacts on both economic growth and inflation. Those impacts will remain uncertain until trade agreements have been finalized.

In early April, President Trump announced larger-than-expected reciprocal tariffs, with the impact most notable on trade with China. However, progress followed with a 90-day pause in tariff implementation. The U.S. then reached trade agreements with the UK, China, and Vietnam. Negotiations with other major trade partners are ongoing. The conflict between Israel and Iran raised inflation concerns, due mostly to the possibility of higher oil prices. Those concerns eased following a ceasefire. Congress passed Trump’s tax cut and spending bill, raising concerns about its potential impact on the U.S. fiscal burden. Meanwhile, U.S. labour market conditions remain resilient, with the unemployment rate remaining low. Inflation has eased slightly but remains above the Federal Reserve’s target. Amid heightened uncertainty, the Federal Reserve held interest rates steady at 4.25%–4.50% at both of its meetings in Q2. Chair Jerome Powell stated that the Fed is “well positioned to wait for greater clarity before considering any adjustments to our policy stance.”

.jpg "Fig-One-(1).jpg")

In Canada, tariffs and trade-related uncertainty continue to weigh on the economy. A pullforward of exports and inventory accumulation ahead of tariffs helped keep first-quarter GDP firm, but growth is expected to slow in the second quarter. The labour market has weakened, particularly in trade-sensitive sectors. Inflation remains within the Bank of Canada’s 1–3% preferred range. However, core CPI remains above the Bank’s preferred 2% target. Canada’s fiscal deficit is expected to widen as Prime Minister Mark Carney aims to fast-track infrastructure development and increase defense spending. Amid ongoing trade uncertainty, the Bank of Canada held its policy rate at 2.75% during its April and June meetings. Governor Tiff Macklem signaled the Bank’s readiness to cut rates further if economic conditions deteriorate.

.jpg "Fig-Two-(1).jpg")

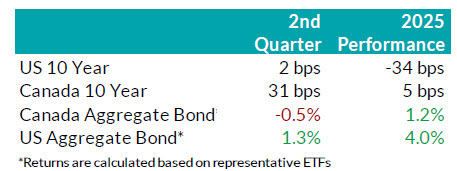

Bond Markets: During Q2, the FTSE Canada Universe Bond Index returned -0.6%. Yields for Canadian bonds rose across all maturities over the quarter. That reflected reduced expectations for rate cuts by the Bank of Canada and a higher risk premium on long-term debt. The impact of higher yields on government bonds was offset in part by tightening of credit spreads on provincial and corporate bonds. Overall corporate bonds saw a positive return for the quarter and outperformed government bonds, in part due to the strong recovery in credit spreads that started in late

April. While corporate issuance slowed considerably in April due to increased trade policy uncertainty, issuance in the Canadian bond markets during May and June were robust. There were 83 deals during Q2 that combined to raise $37 billion for issuers. June 2025 was the 3rd busiest month for issuance on record. We continue to expect higher credit spreads as the U.S. tariffs impact global growth. As such, we have maintained our conservative view with a bias towards shorter corporate bonds but remain ready to invest in longer corporate bonds as valuations become

attractive.

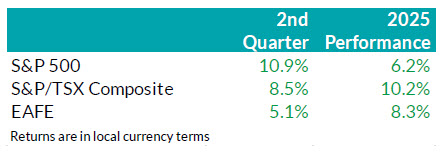

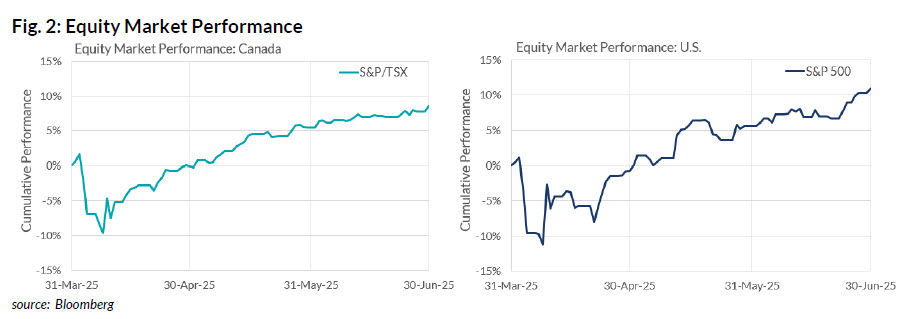

.jpg "Fig-Three-(1).jpg")

Stock Markets – Overview: Having done a round-trip following April tariff announcements, technology, consumer discretionary and industrial companies propelled the U.S. equity market to another record high. The S&P 500 ended the quarter up about 11%, outperforming Canadian and international markets. Canadian equities gained 8.5% in Q2, buoyed by front-loaded demand that benefited the Materials sector, while Financials recovered from a poor Q1. Meanwhile, as risk sentiment stabilized following the 90-day tariff pause and U.S. equities regained momentum, the appeal of the “Sell America” trade diminished. As a result, Europe, Australasia, and the Far East (EAFE) markets finished the quarter with a more modest gain of just over 5%, lagging the sharper

recovery seen in North America.

.jpg "Fig-Four-(1).jpg")

U.S. Equities: The U.S. equity market staged a V-shaped recovery on strong company earnings data in the second quarter. A stable job market and muted inflation reinforced the view of a resilient U.S. economy. At a company level, we observed positive corporate earnings surprises, steady profit margins and better-than-expected forward earnings guidance. Together they underpinned the equity market’s sharp reversal to the upside. Market breadth also improved over the quarter, with strength extending beyond Technology to include Industrials and Financials. That signalled that the market rally was supported by investors’ confidence in the U.S. economy. Furthermore, structural investment trends in artificial intelligence (AI) continued to accelerate, highlighted by rising enterprise capex in data centres. Beyond AI, Circle, a blockchain-based platform that supports stablecoin issuance, tokenized assets, and digital payment infrastructure, conducted a successful IPO. Its share price jumped 485% from its listing price as of quarter-end. On June 17, the U.S. Senate passed the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act, a regulatory framework for use of tokenized assets. While investors wait for the House’s decision, equity price actions suggest that the policy environment is increasingly supportive of blockchain innovation and digital efficiency.

Canadian Equities: Canadian equities posted solid gains in Q2, with Financials overtaking Materials to lead the market higher. Momentum from the Materials sector, which benefited from the pull-forward demand related to U.S. tariff uncertainty, faded toward quarter-end. Meanwhile, cooling inflation and muted domestic growth pushed investors towards highquality, high-dividend-paying companies. Notably, banks significantly outperformed the broader market, as investors favoured their stable corporate fundamentals. Energy surged briefly amid escalating geopolitical tensions, but those gains proved short-lived. In recap, investors in the Canadian market faced slowing resource demand and a stalling domestic economy, which fueled increased interest in high-quality, high-dividend-paying companies. That is a trend we expect to continue going forward.

Bottom line: Markets remain heavily influenced by sentiment, with U.S. policy developments and ongoing tariff negotiations continuing to cause periodic volatility. However, there is little

evidence of deterioration in the hard data to date. As such, we continue to anchor our positioning on underlying data rather than market narratives. Looking ahead, the combination of a structurally higher-for-longer interest rate environment and increasingly pro-growth policy backdrop presents selective opportunities. In the U.S., this favours highquality growth stocks, particularly within Technology, where strong balance sheets and long-term thematic tailwinds remain intact. In Canada, Financials, especially the relatively inexpensive banks, present a more compelling opportunity as earlier tailwinds from pullforward demand are beginning to wane. While we remain constructive, we are mindful of elevated equity valuations and continue to closely monitor macro conditions and policy developments for signs of inflection.

Downloadable Copy

Mark Warywoda, CFA

VP, Public InvestmentsIan Whiteside, CFA, MBA

AVP, Public InvestmentsJohanna Shaw, CFA

Director, Public InvestmentsJin Li

Director, Equity Investments

Wanyi Chen, CFA, FRM

Sr. Quantitative Analyst

Andrew Vermeer, CFA

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Edward Ng Cheng Hi

Analyst, Credit

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

-

Market Commentary July 2025

Key Takeaways

• Markets were very volatile in April to start Q2 but calmed as the quarter progressed. Volatility was driven mostly by headlines about tariffs, but other fiscal policy developments also had an impact.

• Equity markets sold off sharply at the start of the quarter, continuing Q1’s weakness. Markets rebounded sharply once worst-case fears over tariffs eased. The markets continued to rally through the quarter as trade negotiations progressed. Stronger-thanexpected corporate earnings also boosted markets. Despite the shaky start to the quarter, most global equity markets set new all-time highs in Q2.

• Canadian bond markets delivered slightly negative returns in Q2. Weak performance was driven by rising interest rates, which outweighed the impact of tighter credit spreads. Higher interest rates hurt the performance of longer-term bonds most.

• Both the Bank of Canada and the U.S. Federal Reserve adopted a wait-and-see approach. They each held rates steady during Q2, awaiting greater clarity on the impacts of tariffs on both growth and inflation before considering further cuts.

Economic and Market UpdateEconomic Summary: Most indicators of economic activity in the U.S. continued to expand at a decent pace. However, GDP data for the first quarter came in weaker than expected, as higher imports ahead of anticipated tariffs and weaker spending by consumers weighed on Q1 GDP. That said, GDP growth is expected to bounce back in Q2. Tariffs will likely continue to be an evolving story, with potential impacts on both economic growth and inflation. Those impacts will remain uncertain until trade agreements have been finalized.

In early April, President Trump announced larger-than-expected reciprocal tariffs, with the impact most notable on trade with China. However, progress followed with a 90-day pause in tariff implementation. The U.S. then reached trade agreements with the UK, China, and Vietnam. Negotiations with other major trade partners are ongoing. The conflict between Israel and Iran raised inflation concerns, due mostly to the possibility of higher oil prices. Those concerns eased following a ceasefire. Congress passed Trump’s tax cut and spending bill, raising concerns about its potential impact on the U.S. fiscal burden. Meanwhile, U.S. labour market conditions remain resilient, with the unemployment rate remaining low. Inflation has eased slightly but remains above the Federal Reserve’s target. Amid heightened uncertainty, the Federal Reserve held interest rates steady at 4.25%–4.50% at both of its meetings in Q2. Chair Jerome Powell stated that the Fed is “well positioned to wait for greater clarity before considering any adjustments to our policy stance.”

In Canada, tariffs and trade-related uncertainty continue to weigh on the economy. A pullforward of exports and inventory accumulation ahead of tariffs helped keep first-quarter GDP firm, but growth is expected to slow in the second quarter. The labour market has weakened, particularly in trade-sensitive sectors. Inflation remains within the Bank of Canada’s 1–3% preferred range. However, core CPI remains above the Bank’s preferred 2% target. Canada’s fiscal deficit is expected to widen as Prime Minister Mark Carney aims to fast-track infrastructure development and increase defense spending. Amid ongoing trade uncertainty, the Bank of Canada held its policy rate at 2.75% during its April and June meetings. Governor Tiff Macklem signaled the Bank’s readiness to cut rates further if economic conditions deteriorate.

Bond Markets: During Q2, the FTSE Canada Universe Bond Index returned -0.6%. Yields for Canadian bonds rose across all maturities over the quarter. That reflected reduced expectations for rate cuts by the Bank of Canada and a higher risk premium on long-term debt. The impact of higher yields on government bonds was offset in part by tightening of credit spreads on provincial and corporate bonds. Overall corporate bonds saw a positive return for the quarter and outperformed government bonds, in part due to the strong recovery in credit spreads that started in late

April. While corporate issuance slowed considerably in April due to increased trade policy uncertainty, issuance in the Canadian bond markets during May and June were robust. There were 83 deals during Q2 that combined to raise $37 billion for issuers. June 2025 was the 3rd busiest month for issuance on record. We continue to expect higher credit spreads as the U.S. tariffs impact global growth. As such, we have maintained our conservative view with a bias towards shorter corporate bonds but remain ready to invest in longer corporate bonds as valuations become

attractive.

Stock Markets – Overview: Having done a round-trip following April tariff announcements, technology, consumer discretionary and industrial companies propelled the U.S. equity market to another record high. The S&P 500 ended the quarter up about 11%, outperforming Canadian and international markets. Canadian equities gained 8.5% in Q2, buoyed by front-loaded demand that benefited the Materials sector, while Financials recovered from a poor Q1. Meanwhile, as risk sentiment stabilized following the 90-day tariff pause and U.S. equities regained momentum, the appeal of the “Sell America” trade diminished. As a result, Europe, Australasia, and the Far East (EAFE) markets finished the quarter with a more modest gain of just over 5%, lagging the sharper

recovery seen in North America.

U.S. Equities: The U.S. equity market staged a V-shaped recovery on strong company earnings data in the second quarter. A stable job market and muted inflation reinforced the view of a resilient U.S. economy. At a company level, we observed positive corporate earnings surprises, steady profit margins and better-than-expected forward earnings guidance. Together they underpinned the equity market’s sharp reversal to the upside. Market breadth also improved over the quarter, with strength extending beyond Technology to include Industrials and Financials. That signalled that the market rally was supported by investors’ confidence in the U.S. economy. Furthermore, structural investment trends in artificial intelligence (AI) continued to accelerate, highlighted by rising enterprise capex in data centres. Beyond AI, Circle, a blockchain-based platform that supports stablecoin issuance, tokenized assets, and digital payment infrastructure, conducted a successful IPO. Its share price jumped 485% from its listing price as of quarter-end. On June 17, the U.S. Senate passed the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act, a regulatory framework for use of tokenized assets. While investors wait for the House’s decision, equity price actions suggest that the policy environment is increasingly supportive of blockchain innovation and digital efficiency.

Canadian Equities: Canadian equities posted solid gains in Q2, with Financials overtaking Materials to lead the market higher. Momentum from the Materials sector, which benefited from the pull-forward demand related to U.S. tariff uncertainty, faded toward quarter-end. Meanwhile, cooling inflation and muted domestic growth pushed investors towards highquality, high-dividend-paying companies. Notably, banks significantly outperformed the broader market, as investors favoured their stable corporate fundamentals. Energy surged briefly amid escalating geopolitical tensions, but those gains proved short-lived. In recap, investors in the Canadian market faced slowing resource demand and a stalling domestic economy, which fueled increased interest in high-quality, high-dividend-paying companies. That is a trend we expect to continue going forward.

Bottom line: Markets remain heavily influenced by sentiment, with U.S. policy developments and ongoing tariff negotiations continuing to cause periodic volatility. However, there is little

evidence of deterioration in the hard data to date. As such, we continue to anchor our positioning on underlying data rather than market narratives. Looking ahead, the combination of a structurally higher-for-longer interest rate environment and increasingly pro-growth policy backdrop presents selective opportunities. In the U.S., this favours highquality growth stocks, particularly within Technology, where strong balance sheets and long-term thematic tailwinds remain intact. In Canada, Financials, especially the relatively inexpensive banks, present a more compelling opportunity as earlier tailwinds from pullforward demand are beginning to wane. While we remain constructive, we are mindful of elevated equity valuations and continue to closely monitor macro conditions and policy developments for signs of inflection.

Downloadable Copy

Mark Warywoda, CFA

VP, Public InvestmentsIan Whiteside, CFA, MBA

AVP, Public InvestmentsJohanna Shaw, CFA

Director, Public InvestmentsJin Li

Director, Equity Investments

Wanyi Chen, CFA, FRM

Sr. Quantitative Analyst

Andrew Vermeer, CFA

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Edward Ng Cheng Hi

Analyst, Credit

Francie Chen

Analyst, Rates

ADVISOR USE ONLY