Site Search

743 results for access here PROBLEMGO.com Need a bondsman who takes payment plans for release today

-

Anti-money laundering legislation changes

To comply with the Government of Canada’s anti-money laundering legislation and FATCA/CRS changes, Equitable Life® has made changes to the information that we collect on some of our applications and forms.

Changes and updates to our online forms and applications include the following:

● The 350 Application for Life Insurance - Advisors can order new paper applications from Equitable’s Supply Team by filling out the Supply Order form 1390 and emailing it to supply@equitable.ca. You will receive your copies as they become available.

◦ Paper applications submitted after May 15, 2021, with a version date before April 2, 2021 will be accepted with the caveat that additional information may be required from the advisor to comply with anti-money laundering legislation.

◦ As of July 1, 2021 any application with a version date prior to April 2, 2021 will no longer be accepted by Equitable Life.

● Equitable’s EZcomplete® online application reflects the new changes effective May 15, 2021. Any in-flight applications in EZcomplete will automatically be updated to comply with anti-money laundering legislation. You may be required to complete additional fields before submitting the application for signatures.

● Various other forms will now require additional information. A complete list of all forms and applications affected by the anti-money laundering legislation can be found here.

Learn more about the Government of Canada’s anti-money laundering legislation and Financial Transactions and Reports Analysis Centre of Canada -

This year’s RSP contribution deadline is March 1, 2023

The RSP deadline is fast approaching so whether you are using paper or EZtransact™ here are some important things to remember.

Issuing New Policy with EZcomplete®-

All online applications must be digitally signed and submitted and have a date stamp no later than March 1, 2023.

Issuing New Policy using Paper Application-

For contributions to qualify for the first 60 days, all paperwork must be completed and signed by March 1, 2023. Equitable Life must receive all paperwork by March 7, 2023.

Deposits to Existing Policy-

Advisors can setup a one-time or recurring deposit or edit an existing pre-authorized debit already in place using EZtransact. Online deposits must be made and have a date stamp by March 1, 2023, to qualify for a 2022 tax receipt.

-

New to EZtransact? Try our EZtransact Practice Site to see how EZ it is to use.

-

-

Clients can make online deposits to Equitable Life® through their financial institution’s online banking service. Online deposits must be made and have a date stamp by March 1, 2023, to qualify for a 2022 tax receipt.

-

Clients can also make a new deposit to an existing policy by cheque. The cheque must be dated and signed by March 1, 2023. Equitable Life must receive the cheque no later than March 7, 2023.

If online banking is being used to fund the policy – either topping up an existing policy or opening a new policy – the online banking transaction must be completed by March 1, 2023, to receive a 2022 tax receipt.

Please note that cheques and other paperwork cannot be backdated. They must be completed and signed by March 1, 2023, to qualify for a 2023 tax receipt.

Don’t forget about the Equitable Life RSP Grow Your Future Contest. We hope you have a great RSP season!

® denotes a trademark of The Equitable Life Insurance Company of Canada. -

-

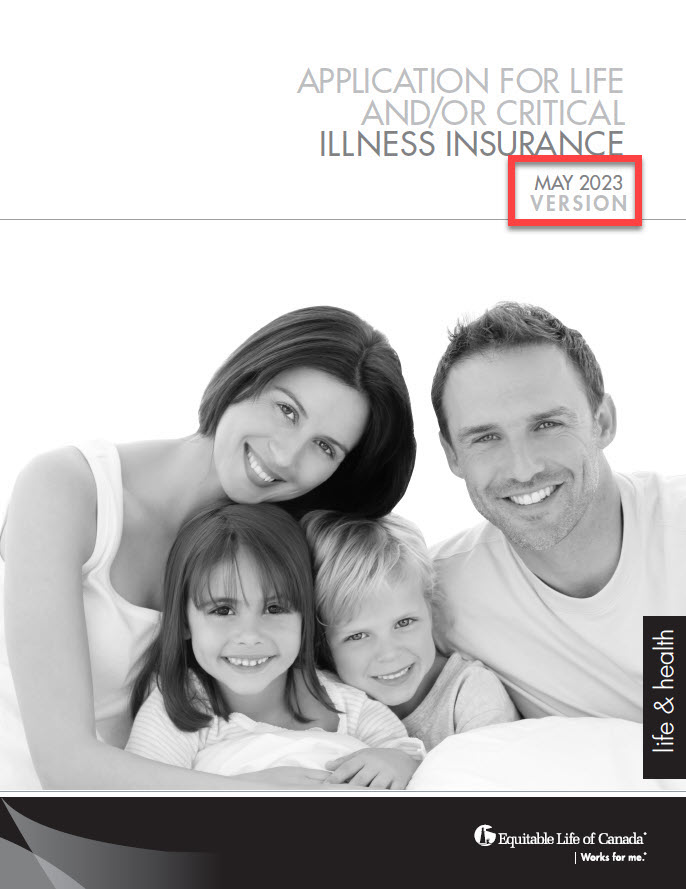

New 350 Life and CI Applications

On August 2nd, 2023, Equitable Life® will be updating the privacy and legal sections on some forms. This includes the form 350 Paper Application for Life and/or Critical Illness Insurance. This change will also be applied on our websites and our online application EZComplete®. These changes are part of Bill 64. The Bill is about the protection of personal and private information in Quebec. This will take effect on September 1st, 2023.

Due to this change, we ask all advisors to use the latest version dated May 2023 of the paper application after August 2nd. Applications in Quebec must use the lastest version from September 1, 2023 onwards.

For all regions outside Quebec, we will support a transition period from ‘old’ to ‘new’ applications until December 31st, 2023. After this date, we will no longer accept older versions of our Life and Critical Illness application.

To make sure you are using the latest version of the application, check the date on the title page. It should say May 2023. See the image below:

.jpg?width=200&height=259 "Form-350-Image-EN-(1).jpg")

To order paper copies, click here.

Email completed applications to supply@equitable.ca.

To learn more about Bill 64, please visit Assemblee nationale du Quebec - Bill 64. You may also contact your wholesaler.

® denote a registered trademark of The Equitable Life Insurance Company of Canada. -

Updates to Savings & Retirement applications and point of sale materials

Equitable Life has updated the following Savings & Retirement point of sale materials.

Form #

Form Name

Description

2086

Pivotal Select FHSA Application

New application to support the First Home Savings Account (FHSA) registration option

1403

Pivotal Select Contract & Information Folder

Updates have been made to support the new First Home Savings Account (FHSA) registration option

796

Guaranteed Interest Account TFSA Application

Updates have been made throughout the application to make it simpler and more straightforward. Additionally, a new “Privacy Consent” section has been added.

799

Guaranteed Interest Account Registered / Non-Registered

The new documents are available to download from EquiNet®. Paper documents are also available to order from Equitable’s Supply Team here.

To allow advisors time to transition to the new applications, we will continue to accept the following versions until further notice:-

Version 2020/06/30: Form #796 – Guaranteed Interest Account TFSA Application

-

Version 2022/03/02: Form #799 – Guaranteed Interest Account Registered/Non-Registered

If you have any questions, contact your Regional Investment Sales Manager or Advisors Services Team Monday to Friday, 8:30 a.m. – 7:30 p.m. ET at 1.866.884.7427, or email savingsretirement@equitable.ca.

® and ™ denotes a registered trademark of The Equitable Life Insurance Company of Canada.

Posted September 11, 2023 -

-

This year’s RSP contribution deadline is February 29, 2024

The RSP deadline is fast approaching and here are some important things to remember.

Issuing a New Policy with EZcomplete®

All online applications must be digitally signed and submitted and have a date stamp no later than February 29, 2024.

Issuing a New Policy using Paper Application

For contributions to qualify for the first 60 days, all paperwork must be completed and signed by February 29, 2024. Equitable® must receive all paperwork by March 8, 2024.

Deposits to an Existing Policy

Advisors can set up a one-time or recurring deposit or edit an existing pre-authorized debit already in place using EZtransact™. Online deposits must be made and have a date stamp by February 29, 2024, to qualify for a 2023 tax receipt.

Clients can make online deposits to Equitable through their financial institution’s online banking service. Online deposits must be made and have a date stamp by February 29, 2024, to qualify for a 2023 tax receipt.

Clients can also make a new deposit to an existing policy by cheque. The cheque must be dated and signed by February 29, 2024. Equitable must receive the cheque no later than March 8, 2024.

If online banking is being used to fund the policy – either topping up an existing policy or opening a new policy – the online banking transaction must be completed by February 29, 2024, to receive a 2023 tax receipt.

Please note that cheques and other paperwork cannot be backdated. They must be completed and signed by February 29, 2024, to qualify for a 2023 tax receipt.

If you haven’t already done so, consider EZcomplete and EZtransact our easy and fast online application and deposit tools to make life easier this RSP season.

For more information, please contact your Regional Investment Sales Manager.

® or ™ denotes a trademark of The Equitable Life Insurance Company of Canada.

Posted February 14, 2024 -

Growing your business in the large case market

At Equitable®, we’re growing at a rapid pace in the large case market. We’re excited to share a new video highlighting all the great reasons to choose Equitable for large case clients—featuring Rob Hollingsworth, Head of Distribution and Product Marketing, Individual Insurance.

Highlights at-a-glance

• We have capacity up to $130 million ultimate net amount at risk

• Up to $10 million internal retention

• Our mutual structure gives us a number of advantages, including the ability to provide personalized service

Equitable offers full support to help you work on large cases and successfully implement solutions, and we’re continually adding tremendous experience and talent to our organization. Our team of wholesalers, specialized underwriters, advanced case consultants, and tax and estate planning professionals are here to support you with your complex and larger files.

Our large case market webpage not only features our new video—it also showcases our team of large case experts and includes a growing list of marketing materials and resources to help you succeed.

Do you have a large case client opportunity, and want to expand in the large case market?

Visit our large case markets webpage to learn more.

® or TM denotes a trademark of The Equitable Life Insurance Company of Canada.

-

New! Evidence of Insurability Schedule

We are pleased to announce Equitable’s new Evidence of Insurability Schedule. The new schedule applies to all life and critical illness insurance applications signed on or after October 5, 2024.

Here are the benefits to you:

● New chart is easier to read with more clarity and transparency.

● ECG and TST are no longer routinely required for Life applicants.

● Blood and urine requirement is streamlined for Life applicants.

● Detailed underwriting requirements for higher coverage amounts and mature applicants.

Please refer to the new Evidence of Insurability schedule (Form #1343) for full details.

Equitable® has the right to ask for more evidence of insurability. We will do this if we feel it is needed to assess the risk.

Key changes – Age and amount requirements

Life applicants:

● Resting ECG: No longer a routine age and amount requirement. This may still be requested at our underwriter’s discretion.

● Treadmill ECG: No longer required at any age or amount.

● Standalone Urine: Standalone urine changed to blood and urine at $100,001 and $500,000 coverage amounts for clients over age 55.

● Mature Age Focus Interview (MAFI): New for clients aged 75+. As part of the paramedical, we will assess the applicant’s Activities of Daily Living, social activities, and word recall ability.

Life and Critical Illness applicants:

● For clients aged 70+, evidence is now valid (recent) if completed within the past 6 months. For all other applicants (ages 18-69), there is no change – evidence is valid if completed within the past 12 months.

Financial/Third-party verification

Reminder – this is required for life insurance amounts over $5M. Our underwriting team will be pleased to assist you with this step.

Questions? Please contact your Equitable wholesaler or reach out to our underwriting team.

® or TM denotes a trademark of the Equitable Life Insurance Company of Canada. -

Why tax refunds aren't always good

It’s important for advisors to help clients understand their finances. Many people think getting a tax refund is good, but that's not always true. Here are some reasons why.

1. Overpaying Taxes

A refund on a tax return means the client paid too much in taxes during the year. This is like giving the government an interest-free loan. Instead, clients could use that money each month for savings or investments.

2. Missed Investment Chances

When clients overpay taxes, they miss chances to invest that money. It could have been earning interest or growing in value instead of sitting with the government.

3. Poor Financial Planning

A big tax refund can show poor financial planning. It's better if clients break even, meaning they don't owe much and don't get a big return. This shows their tax withholdings are accurate.

4. False Sense of Security

A large tax refund can make clients feel falsely secure. They might spend it quickly instead of saving or investing it wisely.

5. Financial Hardship

Overpaying taxes can make it hard for clients to manage their money during the year. They might struggle with monthly expenses or saving for emergencies.

Advisors should teach clients about the downsides of tax refunds. By adjusting their withholdings, clients can manage their money better and take advantage of investment opportunities. Aim for a balanced tax situation to improve financial health.

Help clients make the most of their investment opportunities this tax season. For more information, contact your Director, Investment Sales.

Date posted: March 20, 2025 -

5 topics to discuss with large case clients

Are you working with high-net-worth business owner clients? It’s important to ask the right questions to get them interested in learning how corporate-owned life insurance might benefit their situation.

Here are a few suggestions from our large case team:

1. Capital Dividend Account: Are you taking full advantage of your company’s Capital Dividend Account for your family?

2. Cash flow and surplus: Do you have surplus cash or cash flow in your corporation? Why is it there? If it is for tax deferral, would you like to make some or all of that deferral permanent?

3. Legacy: What do you want to happen to your business when you’re no longer there? How much of what you have built do you want to preserve for your family? How much will be preserved?

4. Shareholder’s agreement: Do you have a shareholder’s agreement? How is it funded? Does it deal with triggering events like death, disability, and retirement?

5. Worse-case scenarios: If you were not able to show up at your business for 3 months, and no one expected it, what would happen? What would creditors, customers, suppliers, and employees do?

Visit our large case webpage and watch Ask our Experts to learn more about the importance of careful planning when it comes to corporate policy ownership.

-

Why fair treatment of clients matters

Building strong client relationships

Fair treatment of clients and excellent service goes beyond offering great products. It's about understanding and meeting clients’ needs at every single stage of life. At Equitable, we believe in putting clients first and building lasting, trusting relationships.

As an advisor, it’s important to build these strong client relationships for your business growth and success. This is achieved by focusing on each client’s interests and providing personalized financial care and support.

Here are some tips to build and maintain strong client relationships:

● Meet with clients at a minimum of every two years to maintain relationships and ensure clients have the right coverage for their needs. Updates to their insurance may be needed with life changes like marriage, children or purchasing a home.

● Regularly review products with investment components with clients. This may help ensure client investments stay on track to meet their needs and align with their financial goals.

● Reassess term policies and riders with clients throughout the term period, and at least six months before renewal. This can help clients understand any premium changes and consider options that may meet their ongoing needs.

Another important tip:

● Document each attempt to engage with clients. Regular meetings with advisors are needed to ensure the client has the right coverage for their current and future needs. Keeping a record of these attempts helps protect advisors when clients don’t respond or don’t want to meet.

Treating clients with fairness and ensuring their interests are protected will show that you are providing support to help ensure your clients' needs are covered. Building trust leads to happier clients, stronger relationships, and more business opportunities to help protect clients throughout their lifetime.