Site Search

657 results for enter source PROBLEMGO.com Buying early release from county jail

- Advisor Guide

-

Join us for an Equitable Master Class webcast featuring Rob Kochel from Invesco

Equitable® Master Class webcasts offer compelling topics and unique ideas from leading experts to help you manage and grow your business.

Losing a top client is never a pleasant experience because it makes it difficult to maintain current production levels and grow organically.

-

• 72.2% of financial professionals lose a top client each year1

-

• 61.3% of those financial professionals were “surprised”1

Join us for our Master Class webcast featuring Rob Kochel to discover how it’s surprisingly simple to manage clients. Contrary to most client retention models that are intensive and time consuming, the Golden Hour model aims to deliver maximum benefit at a truly implementable level.

Learn more

Shannon Labby

Vice-President, National Investment Sales

Equitable

Rob Kochel,

Director

Invesco Global ConsultingDate posted: March 27, 2024

Continuing Education Credits

To be eligible for CE credits, you must register individually, watch the webcast in full and complete a short quiz. This webcast is available in English only.

1Source: Study of 405 financial professionals, as conducted by R.A. Prince & Associates, Inc., under a proprietary contract of Invesco Global Consulting during the second half of 2015. Used with permission.

™ and ® denote trademarks of The Equitable Life Insurance Company of Canada.

-

-

Can’t meet in person? EZcomplete is an EZ way to meet online

Instead of canceling your meeting, why not meet online instead? Our EZcomplete® application makes it easy to process your non-face-to-face applications and do business with Equitable Life.

EZcomplete is available on Pivotal Select™ segregated funds and all life products – Term, Whole Life, CI and Universal Life – and allows for the signing process to change from in-person to non face-to-face at the end of the application, despite how it was started. This gives you and your clients the option to easily and efficiently connect remotely.

How does it work?

EZcomplete gives you the option to conduct your non face-to-face business easily and quickly, enabling your clients to provide their signature remotely on their own device. You simply need to enter their email address and provide them with a secret passcode to securely access the documents to review and sign.

There is no limit on the face amounts or product options and the time to settle is reduced when using the application. It is a flexible, intuitive tool to use, and helps keep business on track now that many clients and advisors are opting for more social distance.

For Life Advisors, please refer to the New Business and Underwriting page on Equinet for details about non-face-to-face delivery. -

Manage more details within Contract Delivery for New Business applications

We are excited to announce further enhancements to our eDelivery process to empower you, the advisor, the ability to manage client details more easily within Contract Delivery.

Effective January 15, 2022, advisors will need to create a Password within Contract Delivery when choosing “eDelivery” as the contract delivery method and provide the password to the client to use as their password:

The Password must be between 4 and 100 alpha/numeric characters, and cannot be the Policy number. For multiple signers the password (and email address) must be unique per each signer.

Advisors can now edit and/or update an email address within Contract Delivery, in the event of a bounce back or email change, to keep the eDelivery process moving and avoid delays in processing time. If a lock out occurs, advisors can trigger a resend of the signing email once they add a new valid email address in Contract Delivery. Simply click the pencil icon beside the Email field to enter the valid email address:

Another new feature- in the event a client has declined, the advisor will get an email from Equitable Life®. Click through to EquiNet® within the email to view the message within Contract Delivery that the client provided as the reason for decline under a new “Declined Details” section. This enables you to connect with the client to proceed with the sale by discussing the reasons for decline with them directly.

Also new for clients with this enhancement, policy owners of a policy created after January 15 will be able to see a PDF copy of their policy within client access. Note: this PDF copy is as the policy was originally issued.

Resources: -

New secure encryption process for outstanding Equitable S&R business requirements

The Equitable® Savings and Retirement Operations team is improving how they send secure email messages to advisors. These emails are sent when there are outstanding requirements for an application or missing information for requests.

Previously, advisors had to manually password protect or unlock PDF documents. This caused delays and difficulties for recipients. The new encryption process will remove that confusion and make it easier for advisors to send and receive secure, encrypted messages.

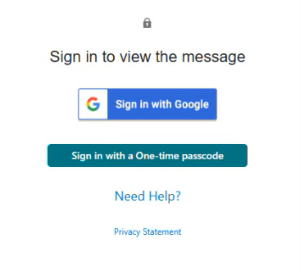

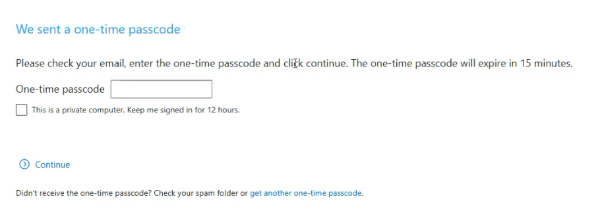

Advisors will now receive secure, encrypted emails from the QA annuity operations mailbox. These emails will use an encrypt option to protect personal client information, such as attachments or requests for personal documents. Recipients will get an email with a subject line saying they have a secure private message. They will need to sign in to view the message or choose to get a one-time passcode (OTP).

Please ensure to check the SPAM folder for the OTP option as it will expire in 15 minutes. Enter the OTP in the secure message

portal.

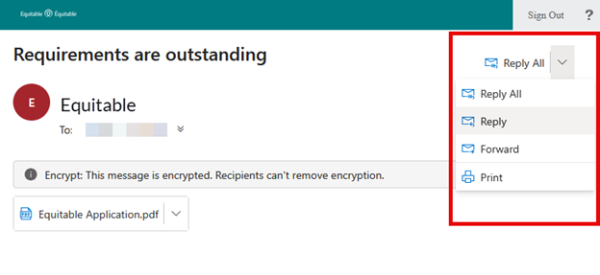

Emails are sent in both English and French, with automatic translation based on browser settings. Recipients must click the view button to access the message in the secure web portal where they can see the encrypted attachment.

Make sure to click Reply in the top right corner of the encrypted message to keep communications within the secure portal.

For more information or assistance, please contact your Director, Investment Sales.

Date posted: May 22, 2025 - Sales Illustrations

-

NEW MARKETING MATERIAL! Flexibility for supplemental income with Equimax

Equitable has created a new piece to help you understand our new Equimax® illustration feature, Paid-Up Additions (PUA) to Cash Dividends, now available!

Did you know Equimax clients can switch from the PUA dividend option to the cash dividend option by simply requesting a dividend option change?1,2

You can illustrate this for paid-up 10 pay and 20 pay Equimax plans! Show clients how they can build in added flexibility and use their policy to create a source of future supplemental income by simply changing the dividend option to cash.3

Illustration Considerations:

● Works with Equimax Estate Builder® or Equimax Wealth Accumulator®.

● Illustrate the Excelerator Deposit Option (EDO) to help build the policy values while the PUA dividend option is in effect. EDO payments can’t be made once the policy is switched to the cash dividend option.

● If a client needs temporary insurance coverage – like mortgage protection - illustrate term riders for how long they are needed to meet the specific goal.3

● If critical illness coverage is needed our competitively priced 20 pay critical illness riders are a great fit to provide paid-up critical illness coverage.3

Clients should apply for the coverage they need. This concept is about flexibility to create a future source of supplemental income.

Want to learn more? Check out our new marketing piece: Flexibility for supplemental income with Equimax (2077).

For more information, reach out to your local wholesaler.

® and TM denote trademarks of The Equitable Life Insurance Company of Canada.

1 Dividends are not guaranteed and are paid at the sole discretion of the Board of Directors. Dividends may be subject to taxation. Dividends will vary based on the actual investment returns in the participating account as well as mortality, expenses, lapse, claims experience, taxes, and other experience of the participating block of policies.

2 To request a change to the dividend option complete and submit form 558 (Request for Withdrawal of Dividends, Change in Option, or Premium Offset). A client can request a change to the cash dividend option from any other dividend option regardless of the premium type or whether premiums continue to be payable, subject to our current administration rules and guidelines. Some dividend option changes are subject to underwriting. Underwriting is not required to change from the PUA to cash dividend option, however, underwriting is required to change from the cash dividend option to the PUA dividend option.

3 This concept is intended to illustrate a one-time switch to cash dividends once premiums are no longer payable for the policy (including premiums for riders). Premiums are paid with after-tax dollars and dividends paid in cash are subject to taxation. If premiums are payable there will be tax savings for the client to use the before-tax cash dividend to reduce the premium instead of taking it entirely as a cash payment. This concept is intended for longer term planning, not to meet short term cash needs by switching back and forth between the PUA and cash options. Clients should consider a policy loan or a cash withdrawal to meet short-term cash needs; policy loans and cash withdrawals may be subject to taxation.

-

Update: Employment Insurance (EI) Sickness Benefit Extension

As it proposed in its 2022 Budget, the federal government has confirmed it is extending the Employment Insurance (EI) Sickness Benefits period from 15 weeks to 26 weeks later this year. The official implementation date and details have not yet been confirmed by the government and we will share further details once they are available. In the meantime, here’s what you need to know.

We will not require or implement any changes to our disability plan designs based on this extension. However, plan sponsors may wish to amend their short-term disability (STD) and long-term disability (LTD) plans and policies to align with the new 26-week EI period.Impact to short-term disability (STD) benefits integrated with EI

Plan sponsors with EI-integrated STD may wish to adjust their benefits to line up with the new 26-week extension.

Impact to plans with no STD benefits

For plan sponsors who do not offer STD, they have the option of adjusting their LTD plans to the new 26-week elimination period if members claim EI prior to LTD. This adjustment would help to avoid the plan member receiving disability and EI payments at the same time and potentially being required to return funds due to overpayment.Considerations for plan sponsors

Plan sponsors who amend their STD or LTD policies to align with the new 26-week EI period should note that there may be inadvertent delays to their employees’ return to work. While collecting EI, injured or ill employees do not benefit from our early intervention services or rigorous claims management practices that could help them get back to work sooner. So, by delaying the availability of STD or LTD coverage, the advantages that these programs are intended to provide could also be delayed.Impact to Premium Reduction Program (PRP)

The Premium Reduction Program (PRP) allows employers with eligible short-term disability plans to pay lower EI premiums. The eligibility criteria have not changed at this time. The government plans to review the PRP in 2024.Questions

If you have questions about these changes or what they mean for your clients’ disability plans, please contact your Group Account Executive or myFlex Sales Manager.

-

Responding to Ontario’s biosimilar switch initiative

We are changing coverage for some biologic drugs in Ontario in response to the province’s biosimilar initiative. These changes will help protect your clients’ plans from additional drug costs that may result from this government policy while providing access to equally safe and effective lower-cost biosimilars.

Ontario’s provincial biosimilar initiative

Announced in December 2022, Ontario’s biosimilar switch program ends coverage of eight biologic drugs for Ontario residents covered by the Ontario Drug Benefit (ODB). The transition to biosimilar versions of these drugs began on March 31, 2023. ODB recipients using these drugs will be required to switch to biosimilar versions of these drugs by December 29, 2023, to maintain their provincial coverageEquitable Life’s response

To ensure this provincial change doesn’t result in your clients paying additional and avoidable drug costs, we are changing coverage in Ontario for most biologic drugs included in the provincial initiative.

Beginning October 1, 2023, plan members in Ontario will no longer be eligible for most originator biologic drugs if they have a condition for which Health Canada has approved a lower cost biosimilar version of the drug.** These plan members will be required to switch to a biosimilar version of the drug to maintain coverage under their Equitable Life plan.Communicating this change to plan members

We will inform any affected plan members in early August of the need to switch their medications so that they have ample time to change their prescriptions and avoid any interruptions in treatment or coverage.Will this change impact my clients’ rates?

Any cost savings associated with the change will be factored in at renewal.What is the difference between biologics and biosimilars?

Biologics are drugs that are engineered using living organisms like yeast and bacteria. The first version of a biologic developed is known as the “originator” biologic. Biosimilars are highly similar to the drugs they are based on and Health Canada considers them to be equally safe and effective for approved conditionsQuestions?

** The list of affected drugs is dynamic and will change as Ontario includes more biologic drugs in its biosimilar initiative, as new biosimilars come onto the market, and as we make changes in drug eligibility.

If you have any questions about this change, please contact your Group Account Executive or myFlex Sales Manager. -

Announcing Equitable Life's National Biosimilar Program

Beginning March 1, 2024, we are expanding our biosimilar switch program nationally** to protect all our clients and to make our coverage consistent across Canada.

Our national biosimilar initiative will simplify drug plan coverage, replacing our provincial programs with one program across the country.

Why now?

Over the past few years, most provinces have introduced policies to delist some originator biologic drugs. They require most patients to switch to biosimilar versions of those drugs to be eligible for coverage under their public drug plans. Soon, it is expected that all provincial drug plans will cover only biosimilars.

In response, we have implemented biosimilar switch initiatives in BC, Alberta, Saskatchewan, Ontario, Quebec, New Brunswick and Nova Scotia to align with these provincial changes. Our initiatives are designed to protect our clients from additional drug costs that may result from these government policies while providing access to equally safe and effective lower cost biosimilars.

How will this affect clients’ drug plans?

Because we have already introduced biosimilar switch initiatives in most provinces, the impact of this change will be minimal. It will primarily affect plan members in provinces or territories where we haven’t already required the switch to biosimilars, and plan members who are taking biosimilars that were not originally included in the switch initiative for their province.

Regardless of where they live, plan members across Canada will no longer be eligible for most originator biologic drugs if they have a condition for which Health Canada has approved a lower cost biosimilar version of the drug. Plan members already taking the originator biologic will be required to switch to a biosimilar version of the drug to maintain coverage under their Equitable plan. We will support their transition with education, personalized communication, and resources.

Will this change affect clients' rates?

Any cost savings associated with the change will be factored in at renewal.

Biologics are drugs that are engineered using living organisms like yeast and bacteria. The first version of a biologic developed is known as the “originator” biologic. Biosimilars are highly similar to the drugs they are based on, and Health Canada considers them to be equally safe and effective for approved conditions.

What is the difference between biologics and biosimilars?

Advance notice

We will be communicating with affected claimants in early December to allow them ample time to change their prescription and avoid any interruptions in their treatment or their coverage.

If you have any questions about this change, please contact your Group Account Executive or myFlex Account Executive.

**Excludes plan members in Quebec who participate in a separate provincial program.