Site Search

486 results for MAKEMUR.COM How to bribe a guard to get extra privileges in prison Franklin County Jail

-

Questions about eDelivery? New eDelivery page

Find information on the eDelivery process quickly with our new eDelivery of a Contract landing page.

We’ve made it easier to get the information you need to electronically deliver the insurance contract promptly.

eDelivery makes it quick and easy, and our new landing page ensures you’re able to find the information you need regarding the New Business eDelivery process, or the Policy Change and Conversions eDelivery process. You can find various resources in the Links section on the right-hand side of each page to help you along the way.

-

Start a Conversation with EZstart – Now Available for Equimax Wealth Accumulator

Looking for an easy way to explain insurance? We have a digital tool to do just that!

Start a Conversation with EZstart™

EZstart helps to commence those initial client conversations. Think of it like a digital brochure: you start a conversation about life goals, enter a few details - and within a few clicks - get a quick quote on your phone or tablet instantly.

We have a NEW EZstart for Equimax Wealth Accumulator® available. Go to the EZstart for Equimax Wealth Accumulator now.

Don’t forget about our other EZstart tools that are available for you. Learn more.

® and TM denote trademarks of The Equitable Life Insurance Company of Canada. - [pdf] Corporate Preferred Estate Transfer using universal life

- [pdf] Corporate Preferred Estate Transfer using Equimax

- Equitable’s EZstart tool

-

Coming soon — enhanced Equitable Generations™ universal life (UL)

See what’s ahead

Equitable Generations UL insurance solution is about to get even better! In the next few weeks, Level cost of insurance (COI)* option will be added to our offering. The new Level COI option will add more value, choices, and opportunities for clients.

The enhanced Equitable Generations is designed to meet client’s UL needs. To simplify our UL products, Equation Generation® IV UL insurance solution will soon no longer be available for new sales.

Stay tuned for more details and the effective date.

Check out the Transition Rules for new and in-progress universal life applications.

* For Level COI, only Account Value Protector is offered as a death benefit option.

- [pdf] Health Care Spending Account - Plan members

-

New online course available

Boost your knowledge and earn CE Credits

Looking to deepen your understanding of Universal Life insurance and get a new CE Credit?

Equitable is excited to offer a new addition to our online learning center: The mechanics of Universal Life. Whether you are new to the concept or looking to refresh your expertise, this course will help provide the knowledge you need to start conversations with clients.

Our CE credit courses allow you to learn at your own pace and earn CE credits quickly and easily.

Available Courses:

• The mechanics of Universal Life *NEW*

• Introduction to Whole Life Insurance

• Participating Whole Life for the Children’s Market – A head start for tomorrow

• Path to Success - Expert Advice on Navigating CI Sales

• Ensuring a Compliant, Needs-based Insurance Sale

• Where UL Fits in your product portfolio

• Building your business with Critical Illness insurance

• Harness the Power of Whole Life Cash Value

A few important notes before you get started:

• The programs are hosted on Teachable: https://equitable-life-education.teachable.com

• Username: Please use your email address that you are contracted with

• Password: Equitable

• Please use Google Chrome to access the courses

You can earn CE credits right away when you complete these courses.

Start earning CE Credits!

Check out the individual insurance online learning centre on EquiNet to stay up to date on new courses.

All courses are accredited by Alberta Insurance Council, Insurance Council of Manitoba, The Institute for Advanced Financial Education, and Chambre de la sécurité financière*.

Questions?

Contact your local wholesaler.

Are you having trouble logging in?

Email equitableiimarketing@equitable.ca for assistance. -

Market Commentary January 2025

Key Takeaways

Full year 2024:

-

Despite reductions of policy-setting interest rates by central banks, yields on longer-term bonds finished the year higher than they started the year.

-

Positive risk appetite helped corporate bonds perform well, led by lower-quality issuers.

-

Global equity markets posted robust returns, with U.S. equities outperforming other developed markets, driven by heavy concentration into the ‘Magnificent 7’ stocks.

Fourth Quarter:

-

Central banks continued to ease monetary policy in Q4, with the Bank of Canada cutting its policy interest rate more aggressively than did the U.S. Federal Reserve.

-

The Republican victory across both the executive and legislative branches in the U.S. ignited expectations of economic growth, pushing bond yields and stock prices higher.

-

Risk sentiment helped corporate bonds continue to outperform government bonds.

-

Markets remained volatile: while North American stock markets continued to outperform most international indices, Canadian stocks managed to outperform U.S. stocks in Q4, as sources of returns in the U.S. narrowed into year-end.

Economic and Market Update

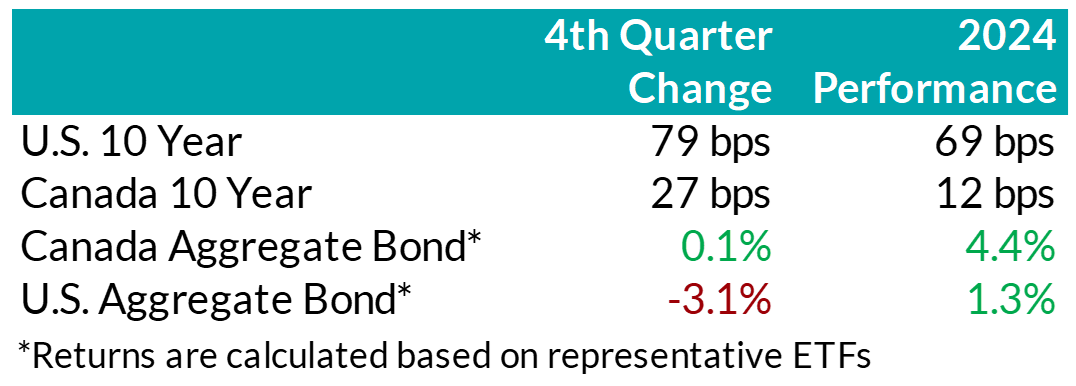

Economic Summary: In the U.S., economic activity continued to expand at a solid pace in Q4. The rate of inflation continued to slow but remained above the central bank’s 2% objective. The labour market in the U.S. remained resilient, as the unemployment rate has remained low compared to historical norms. A decisive victory for Donald Trump and the Republican Party further boosted expectations for continued growth. The return of the President-elect’s old tactics of threatening tariffs to influence trade, security, and drug control re-introduced some economic uncertainty, particularly regarding the potential return of inflationary pressures. Those concerns prompted the Federal Reserve to slow the pace of its policy easing, as it lowered rates by just 0.25% at each of its two meetings in Q4, following the 0.50% cut in September. Throughout 2024, the Fed reduced rates by a total of 100 basis points, from 5.50% to 4.50%. Nonetheless, bond yields were significantly higher for most maturity terms during the fourth quarter as the market priced in not just a stronger economy than had been the expectation during Q3, implying less interest rate cuts by the Fed, but also growing concerns about the government deficit.

In Canada, growth remained positive during 2024 and improved a bit to close the year, but continued to fall short of the Bank of Canada’s expectations. Similarly, inflation came in lower than expected and below the Bank’s 2% target. The labour market continued to soften for much of the year, with employment growth falling short of labour force growth. The weakness in the labour market and economy, along with tamed inflation, prompted the Central Bank to cut rates at the pace of 50 basis points at each of its two meetings in Q4. For the full year, the Bank of Canada ended up lowering its policy rate by a total of 175 basis points, from 5% to 3.25%. The market has been expecting the Bank of Canada to need to continue cutting rates due to slower economic growth in Canada, but the fear of a possible trade war with the U.S. has made the economic outlook somewhat murkier.

.png "Chart1-(1).png")

Bond Markets: During the quarter, yields on mid- to long-term bonds in Canada rose in sympathy with rising bond yields in the U.S. However, bond yields in Canada rose to a lesser extent, and yields on shorter-term bonds were actually little changed over the quarter. The FTSE Canada Universe Bond Index was basically flat during Q4 and posted a return of 4.2% for the full year. Although interest rates rose, credit spreads (i.e. the extra yield on corporate bonds versus government bonds to compensate for their extra risk) continued to grind lower, helping corporate bonds post positive overall returns in the quarter. Tightening credit spreads reflected the generally positive risk-on tone to the market, despite some volatility. Lower-rated BBB bonds generally performed better than higher-quality A-rated bonds. Credit spreads have now generally fallen back to levels similar to those experienced in 2021, when markets did quite well after the pandemic. The on-going appetite of investors for the extra yield offered by corporate bonds over government bonds is indicated not just by falling credit spreads, but also by investors’ enthusiasm to support the primary issuance market. Corporate bond supply continued to be very robust in the quarter, with $30 billion in new issuance, resulting in a record-breaking year with $141 billion of new issuance in 2024. Nonetheless, on balance, we do not think the current risk premium adequately compensates for downside risk, particularly in longer-dated corporate bonds, and have a bias towards shorter-dated credit where we view the risk / reward trade-off as being more favourable.

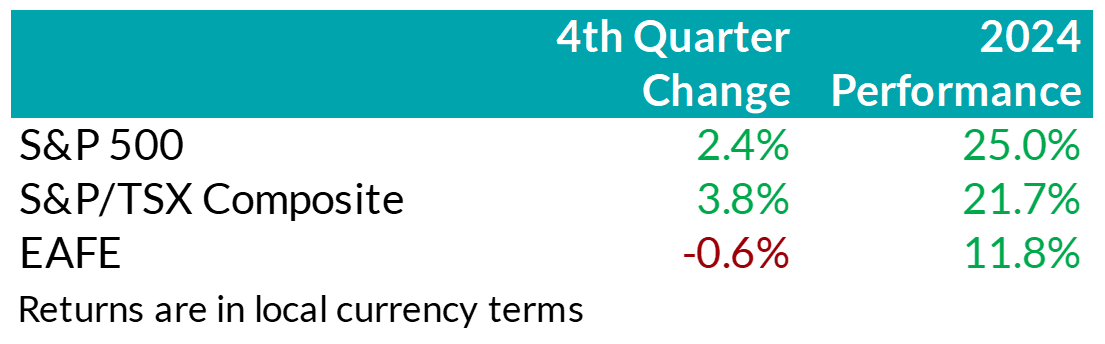

.png "Chart2-(1).png") Stock Markets – Overview: Trump’s presidential victory and the Republican party’s ‘red sweep’ in the Senate and House of Representatives sparked optimism surrounding economic growth and a new era of U.S. exceptionalism. As a result, North American equity markets extended their rally in Q4, capping off a year of robust returns. The S&P 500 returned 2.4%, bringing its year-to-date return to 25%. Within the U.S., the broadening of returns paused during the quarter as the chase for growth intensified, with mega-cap growth names like Tesla driving performance. Canadian equities surprisingly outperformed the U.S. market over the quarter, returning 3.8% in Q4, despite threats of widespread tariff negotiations looming on the horizon that could negatively impact Canadian corporate fundamentals. At a sector level, strength in the technology, financials, and energy sectors more than offset weakness in telecommunication companies as well as in the materials sector. Elsewhere, major developed markets from Europe and Asia (EAFE) underperformed last quarter as deteriorating Chinese growth prospects and weak economic growth in the Eurozone weighed on equities. Notably, foreign investors of U.S. denominated securities benefitted from a rebounding U.S. dollar with the dollar index adding over 7.6% in Q4.

Stock Markets – Overview: Trump’s presidential victory and the Republican party’s ‘red sweep’ in the Senate and House of Representatives sparked optimism surrounding economic growth and a new era of U.S. exceptionalism. As a result, North American equity markets extended their rally in Q4, capping off a year of robust returns. The S&P 500 returned 2.4%, bringing its year-to-date return to 25%. Within the U.S., the broadening of returns paused during the quarter as the chase for growth intensified, with mega-cap growth names like Tesla driving performance. Canadian equities surprisingly outperformed the U.S. market over the quarter, returning 3.8% in Q4, despite threats of widespread tariff negotiations looming on the horizon that could negatively impact Canadian corporate fundamentals. At a sector level, strength in the technology, financials, and energy sectors more than offset weakness in telecommunication companies as well as in the materials sector. Elsewhere, major developed markets from Europe and Asia (EAFE) underperformed last quarter as deteriorating Chinese growth prospects and weak economic growth in the Eurozone weighed on equities. Notably, foreign investors of U.S. denominated securities benefitted from a rebounding U.S. dollar with the dollar index adding over 7.6% in Q4.

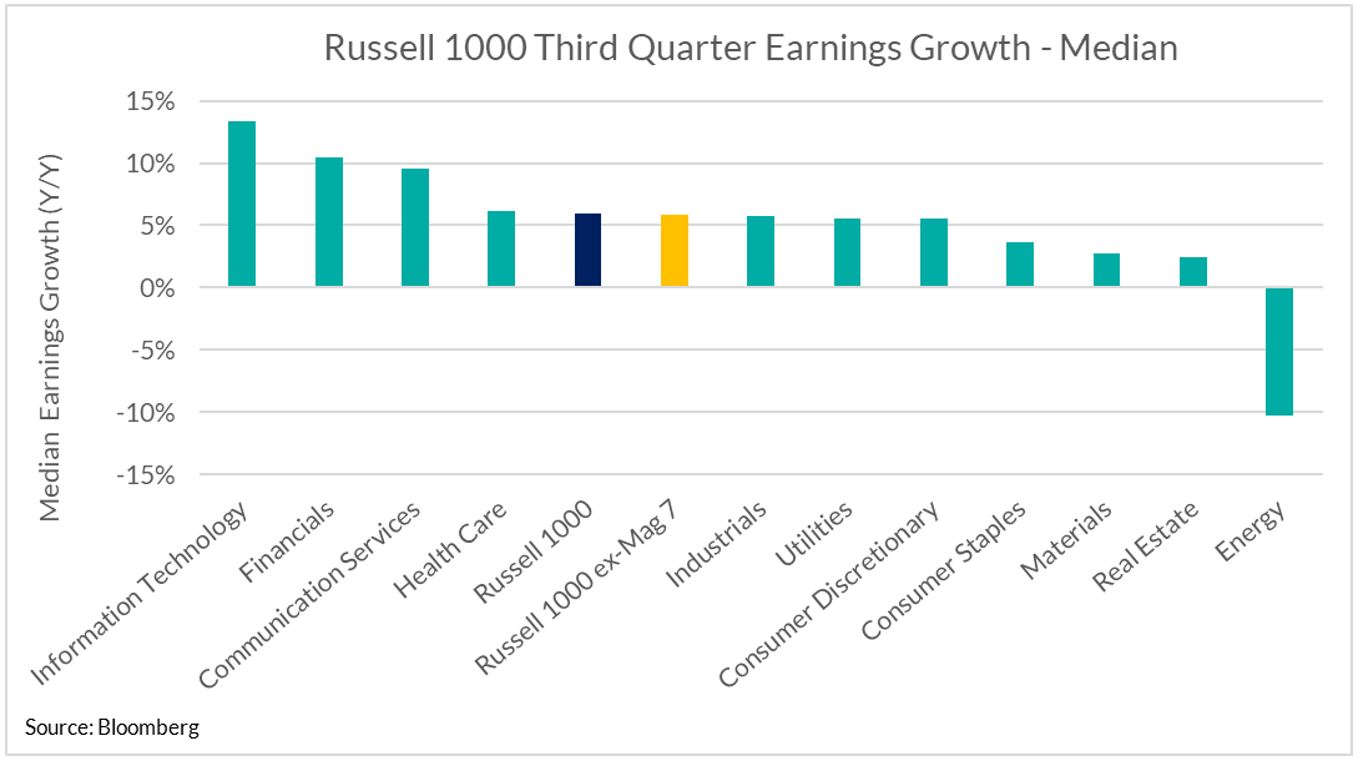

.png "Chart3-(1).png") U.S. Equities: U.S. equities remain supported by resilient margins and strong corporate earnings growth with over 70% of businesses surpassing bottom-line expectations last quarter. We remain attentive to the broadening of earnings performance and note that this trend has continued, albeit at a normalized pace versus prior quarters. More specifically, our work shows that members of the Russell 1000, excluding the Magnificent 7, posted median earnings growth of 6% last quarter, down from nearly 9% in Q3 but comparable to Q2 (6%). Looking forward to 2025, analysts continue to forecast U.S. exceptionalism, with forecasts of ~12% earnings growth.

U.S. Equities: U.S. equities remain supported by resilient margins and strong corporate earnings growth with over 70% of businesses surpassing bottom-line expectations last quarter. We remain attentive to the broadening of earnings performance and note that this trend has continued, albeit at a normalized pace versus prior quarters. More specifically, our work shows that members of the Russell 1000, excluding the Magnificent 7, posted median earnings growth of 6% last quarter, down from nearly 9% in Q3 but comparable to Q2 (6%). Looking forward to 2025, analysts continue to forecast U.S. exceptionalism, with forecasts of ~12% earnings growth.

Following Trump’s presidential victory, stocks with greater sensitivity to the U.S. economy, such as small cap businesses, benefitted from expectations of domestically focused growth initiatives. However, stubborn inflation and expectations of fewer interest rate cuts by the Federal Reserve saw the trend of broadening sources of returns pause into the end of the year. Instead, market concentration reaccelerated with investors rushing back towards mega-cap growth stocks. In fact, Tesla – which is approximately 2% of the S&P 500 Index by market cap – contributed approximately one-third of the total index return in Q4, while the Mag 7 as a group contributed over 100% of total returns. In other words, U.S. large cap companies excluding the Magnificent 7 declined in aggregate last quarter.

Canadian Equities: Against the backdrop of cooling inflation and below-trend growth, the Bank of Canada continued to loosen monetary policy. As a result, Canadian companies

showed signs of improving efficiency with return on equity – a gauge of corporate profitability – improving versus prior quarters. Under these conditions, investors remained focused on higher quality, high-dividend paying companies – particularly within the financial sector. Relative to prior quarters, this group witnessed greater contribution out of non-bank financials (such as asset managers and insurance companies), as the premium investors were willing to pay for Canadian banks remained elevated. Across other sectors, the energy sector had a positive quarter as the price of oil stabilized, but falling prices for raw industrials pushed the materials sector lower.

Bottom line: U.S. political developments and subsequent growth expectations dominated market sentiment last quarter. As a result, investors dialed back rate cut expectations and bond yields moved higher. In equity markets, the potential for an era of higher-for-longer rates prompted a resumption of investors crowding into growth stocks. Going forward, we remain cautious of elevated valuations and continue to prioritize diversified sources of returns with a long-term outlook. Nonetheless, despite rich valuations, our base case remains that investors’ enthusiasm for equities will persist in the near-term and stocks should continue to outperform bonds.

Downloadable Copy

ADVISOR USE ONLYMark Warywoda, CFA

VP, Public Portfolio ManagementIan Whiteside, CFA, MBA

AVP, Public Portfolio ManagementJohanna Shaw, CFA

Director, Portfolio ManagementJin Li

Director, Equity Portfolio Management

Tyler Farrow, CFA

Senior Analyst, Equity

Andrew Vermeer

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Francie Chen

Analyst, Rates

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

-

-

Enhanced flexibility and features make Equimax whole life a great choice for your clients

WHAT’S NEW ON MARCH 23, 2020?

The following features are available on Equimax Estate Builder® and Equimax Wealth Accumulator® plans!

.jpg?width=120&height=141 "Image-1-EDO-Prelaunch-Whatsnew-(1).jpg") 60 months of EDO payment flexibility1 that fits your clients’ situation

60 months of EDO payment flexibility1 that fits your clients’ situation- Clients can start EDO payments1 up to 60 months from the date the application was signed, or resume up to 60 months from the last EDO payment made, without additional evidence of insurability.

- Applies to Equimax2 policies with an effective date of March 23, 2020 or later.

EDO is available on cases rated 300% or less3 for new and existing clients- For existing clients, if approved, the EDO contract provisions that apply will be based on the effective date of the insurance policy, not the date the EDO was added.

- Applies to Equimax2 policies issued under the 2017 tax rules.

Built-in Disability Benefit Disbursement provides access to cash value in the event of a disability

Built-in Disability Benefit Disbursement provides access to cash value in the event of a disability

- The Disability Benefit Disbursement may provide a tax-free, lump sum payment of up to 100% of the policy’s cash value if the insured becomes disabled.4

- Will be included on Equimax2 policies issued under the 2017 tax rules.5

Want more information?

More information is available on EquiNet® on the Whole Life Insurance Product page under the Resources tab.

Ask your Equitable Life® Regional Sales Manager about Equimax today.COVID-19 & social distancing: Strategy for insurance applications

Using our EZcomplete® online application allows you to keep your distance … while keeping your business moving forward.

Learn more

1 This applies only to policies with an effective date of March 23, 2020 or later. The amount of the EDO payment allowed may be limited to the maximum EDO payment made in previous years depending on the policy year. For approved EDO amounts exceeding $150,000 annually ($12,500 monthly), clients have up to 12 months from the date the EDO application was signed or the date of the last EDO payment to make an EDO payment before a contribution cap may apply. See Admin Guide for full details. 2 Applies to Equimax Estate Builder and Wealth Accumulator; all ages; life pay and 20 pay; single and joint lives. 3 Not available if the policy has a flat extra rating. 4 See sample policy contract for full details, including the qualifications for the disbursement. Policy cash value and death benefit will decrease. Tax laws are subject to change. The payment of the disability benefit disbursement may affect the adjusted cost basis (ACB) of the policy as it is considered payment of a capital benefit. Changes in ACB can affect the future taxation of the policy. 5Subject to our administrative rules and guidelines in effect at the time of the disbursement