Site Search

701 results for view site quick MAKEMUR.com pay bond online get out today Alytus

-

See why choosing EquiLiving Critical Illness Insurance is the right choice for Ayo’s family

Ayo’s just returned from maternity leave. Her baby David and her husband are the most cherished people in her life.

But a neighbour’s cancer diagnosis leaves her wondering how she can protect her family if a serious illness were to affect them.

Learn why Ayo decided EquiLiving® Critical Illness insurance was the right choice for her family.

Watch our new Critical Illness with Equitable Life of Canada video to learn more. View on Vimeo or YouTube.

You can use this video to send to clients before or after meetings to help them understand the benefits of Critical Illness Insurance. Check out our prospecting letter, that you can personalize and send to your clients to tell them about Critical Illness Insurance.

Plus, visit our Critical Illness product page, then click on the Marketing Materials tab for the latest Critical Illness marketing materials.

Need more information? Please contact your local wholesaler.

View on Vimeo or YouTube.

® and ™ denotes trademarks of The Equitable Life Insurance Company of Canada. - Login information for current advisors

-

Market Commentary July 2025

Key Takeaways

• Markets were very volatile in April to start Q2 but calmed as the quarter progressed. Volatility was driven mostly by headlines about tariffs, but other fiscal policy developments also had an impact.

• Equity markets sold off sharply at the start of the quarter, continuing Q1’s weakness. Markets rebounded sharply once worst-case fears over tariffs eased. The markets continued to rally through the quarter as trade negotiations progressed. Stronger-thanexpected corporate earnings also boosted markets. Despite the shaky start to the quarter, most global equity markets set new all-time highs in Q2.

• Canadian bond markets delivered slightly negative returns in Q2. Weak performance was driven by rising interest rates, which outweighed the impact of tighter credit spreads. Higher interest rates hurt the performance of longer-term bonds most.

• Both the Bank of Canada and the U.S. Federal Reserve adopted a wait-and-see approach. They each held rates steady during Q2, awaiting greater clarity on the impacts of tariffs on both growth and inflation before considering further cuts.

Economic and Market UpdateEconomic Summary: Most indicators of economic activity in the U.S. continued to expand at a decent pace. However, GDP data for the first quarter came in weaker than expected, as higher imports ahead of anticipated tariffs and weaker spending by consumers weighed on Q1 GDP. That said, GDP growth is expected to bounce back in Q2. Tariffs will likely continue to be an evolving story, with potential impacts on both economic growth and inflation. Those impacts will remain uncertain until trade agreements have been finalized.

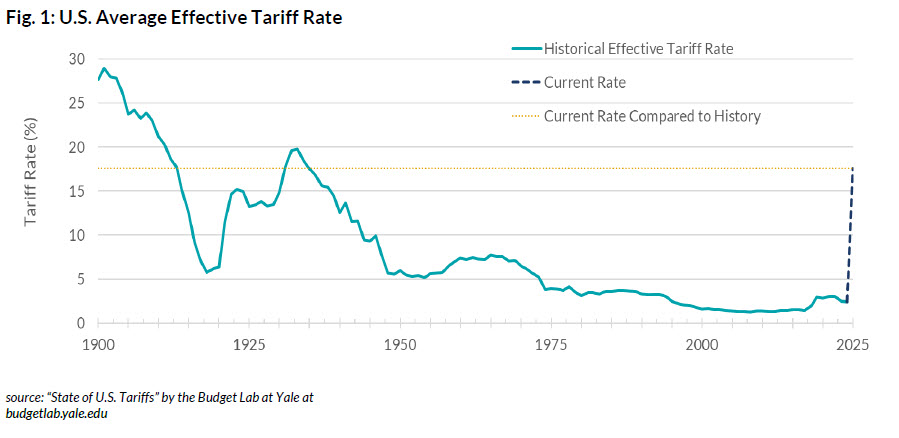

In early April, President Trump announced larger-than-expected reciprocal tariffs, with the impact most notable on trade with China. However, progress followed with a 90-day pause in tariff implementation. The U.S. then reached trade agreements with the UK, China, and Vietnam. Negotiations with other major trade partners are ongoing. The conflict between Israel and Iran raised inflation concerns, due mostly to the possibility of higher oil prices. Those concerns eased following a ceasefire. Congress passed Trump’s tax cut and spending bill, raising concerns about its potential impact on the U.S. fiscal burden. Meanwhile, U.S. labour market conditions remain resilient, with the unemployment rate remaining low. Inflation has eased slightly but remains above the Federal Reserve’s target. Amid heightened uncertainty, the Federal Reserve held interest rates steady at 4.25%–4.50% at both of its meetings in Q2. Chair Jerome Powell stated that the Fed is “well positioned to wait for greater clarity before considering any adjustments to our policy stance.”

.jpg "Fig-One-(1).jpg")

In Canada, tariffs and trade-related uncertainty continue to weigh on the economy. A pullforward of exports and inventory accumulation ahead of tariffs helped keep first-quarter GDP firm, but growth is expected to slow in the second quarter. The labour market has weakened, particularly in trade-sensitive sectors. Inflation remains within the Bank of Canada’s 1–3% preferred range. However, core CPI remains above the Bank’s preferred 2% target. Canada’s fiscal deficit is expected to widen as Prime Minister Mark Carney aims to fast-track infrastructure development and increase defense spending. Amid ongoing trade uncertainty, the Bank of Canada held its policy rate at 2.75% during its April and June meetings. Governor Tiff Macklem signaled the Bank’s readiness to cut rates further if economic conditions deteriorate.

.jpg "Fig-Two-(1).jpg")

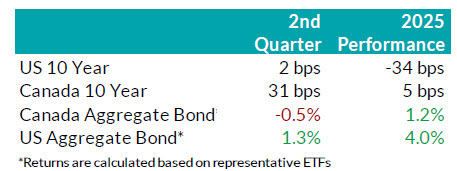

Bond Markets: During Q2, the FTSE Canada Universe Bond Index returned -0.6%. Yields for Canadian bonds rose across all maturities over the quarter. That reflected reduced expectations for rate cuts by the Bank of Canada and a higher risk premium on long-term debt. The impact of higher yields on government bonds was offset in part by tightening of credit spreads on provincial and corporate bonds. Overall corporate bonds saw a positive return for the quarter and outperformed government bonds, in part due to the strong recovery in credit spreads that started in late

April. While corporate issuance slowed considerably in April due to increased trade policy uncertainty, issuance in the Canadian bond markets during May and June were robust. There were 83 deals during Q2 that combined to raise $37 billion for issuers. June 2025 was the 3rd busiest month for issuance on record. We continue to expect higher credit spreads as the U.S. tariffs impact global growth. As such, we have maintained our conservative view with a bias towards shorter corporate bonds but remain ready to invest in longer corporate bonds as valuations become

attractive.

.jpg "Fig-Three-(1).jpg")

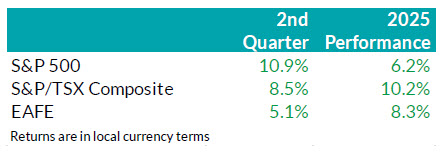

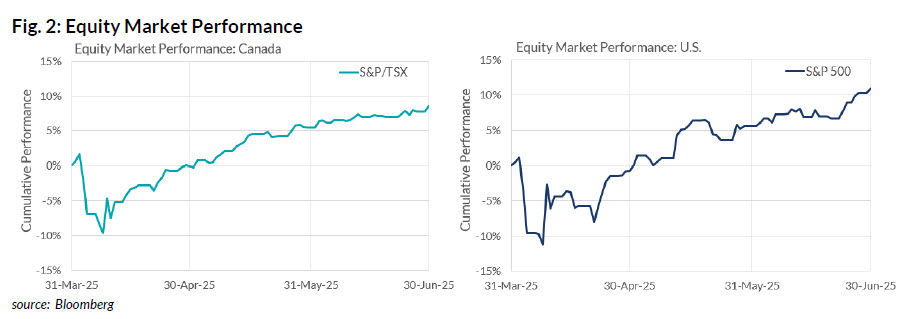

Stock Markets – Overview: Having done a round-trip following April tariff announcements, technology, consumer discretionary and industrial companies propelled the U.S. equity market to another record high. The S&P 500 ended the quarter up about 11%, outperforming Canadian and international markets. Canadian equities gained 8.5% in Q2, buoyed by front-loaded demand that benefited the Materials sector, while Financials recovered from a poor Q1. Meanwhile, as risk sentiment stabilized following the 90-day tariff pause and U.S. equities regained momentum, the appeal of the “Sell America” trade diminished. As a result, Europe, Australasia, and the Far East (EAFE) markets finished the quarter with a more modest gain of just over 5%, lagging the sharper

recovery seen in North America.

.jpg "Fig-Four-(1).jpg")

U.S. Equities: The U.S. equity market staged a V-shaped recovery on strong company earnings data in the second quarter. A stable job market and muted inflation reinforced the view of a resilient U.S. economy. At a company level, we observed positive corporate earnings surprises, steady profit margins and better-than-expected forward earnings guidance. Together they underpinned the equity market’s sharp reversal to the upside. Market breadth also improved over the quarter, with strength extending beyond Technology to include Industrials and Financials. That signalled that the market rally was supported by investors’ confidence in the U.S. economy. Furthermore, structural investment trends in artificial intelligence (AI) continued to accelerate, highlighted by rising enterprise capex in data centres. Beyond AI, Circle, a blockchain-based platform that supports stablecoin issuance, tokenized assets, and digital payment infrastructure, conducted a successful IPO. Its share price jumped 485% from its listing price as of quarter-end. On June 17, the U.S. Senate passed the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act, a regulatory framework for use of tokenized assets. While investors wait for the House’s decision, equity price actions suggest that the policy environment is increasingly supportive of blockchain innovation and digital efficiency.

Canadian Equities: Canadian equities posted solid gains in Q2, with Financials overtaking Materials to lead the market higher. Momentum from the Materials sector, which benefited from the pull-forward demand related to U.S. tariff uncertainty, faded toward quarter-end. Meanwhile, cooling inflation and muted domestic growth pushed investors towards highquality, high-dividend-paying companies. Notably, banks significantly outperformed the broader market, as investors favoured their stable corporate fundamentals. Energy surged briefly amid escalating geopolitical tensions, but those gains proved short-lived. In recap, investors in the Canadian market faced slowing resource demand and a stalling domestic economy, which fueled increased interest in high-quality, high-dividend-paying companies. That is a trend we expect to continue going forward.

Bottom line: Markets remain heavily influenced by sentiment, with U.S. policy developments and ongoing tariff negotiations continuing to cause periodic volatility. However, there is little

evidence of deterioration in the hard data to date. As such, we continue to anchor our positioning on underlying data rather than market narratives. Looking ahead, the combination of a structurally higher-for-longer interest rate environment and increasingly pro-growth policy backdrop presents selective opportunities. In the U.S., this favours highquality growth stocks, particularly within Technology, where strong balance sheets and long-term thematic tailwinds remain intact. In Canada, Financials, especially the relatively inexpensive banks, present a more compelling opportunity as earlier tailwinds from pullforward demand are beginning to wane. While we remain constructive, we are mindful of elevated equity valuations and continue to closely monitor macro conditions and policy developments for signs of inflection.

Downloadable Copy

Mark Warywoda, CFA

VP, Public InvestmentsIan Whiteside, CFA, MBA

AVP, Public InvestmentsJohanna Shaw, CFA

Director, Public InvestmentsJin Li

Director, Equity Investments

Wanyi Chen, CFA, FRM

Sr. Quantitative Analyst

Andrew Vermeer, CFA

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Edward Ng Cheng Hi

Analyst, Credit

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

-

Market Commentary July 2025

Key Takeaways

• Markets were very volatile in April to start Q2 but calmed as the quarter progressed. Volatility was driven mostly by headlines about tariffs, but other fiscal policy developments also had an impact.

• Equity markets sold off sharply at the start of the quarter, continuing Q1’s weakness. Markets rebounded sharply once worst-case fears over tariffs eased. The markets continued to rally through the quarter as trade negotiations progressed. Stronger-thanexpected corporate earnings also boosted markets. Despite the shaky start to the quarter, most global equity markets set new all-time highs in Q2.

• Canadian bond markets delivered slightly negative returns in Q2. Weak performance was driven by rising interest rates, which outweighed the impact of tighter credit spreads. Higher interest rates hurt the performance of longer-term bonds most.

• Both the Bank of Canada and the U.S. Federal Reserve adopted a wait-and-see approach. They each held rates steady during Q2, awaiting greater clarity on the impacts of tariffs on both growth and inflation before considering further cuts.

Economic and Market UpdateEconomic Summary: Most indicators of economic activity in the U.S. continued to expand at a decent pace. However, GDP data for the first quarter came in weaker than expected, as higher imports ahead of anticipated tariffs and weaker spending by consumers weighed on Q1 GDP. That said, GDP growth is expected to bounce back in Q2. Tariffs will likely continue to be an evolving story, with potential impacts on both economic growth and inflation. Those impacts will remain uncertain until trade agreements have been finalized.

In early April, President Trump announced larger-than-expected reciprocal tariffs, with the impact most notable on trade with China. However, progress followed with a 90-day pause in tariff implementation. The U.S. then reached trade agreements with the UK, China, and Vietnam. Negotiations with other major trade partners are ongoing. The conflict between Israel and Iran raised inflation concerns, due mostly to the possibility of higher oil prices. Those concerns eased following a ceasefire. Congress passed Trump’s tax cut and spending bill, raising concerns about its potential impact on the U.S. fiscal burden. Meanwhile, U.S. labour market conditions remain resilient, with the unemployment rate remaining low. Inflation has eased slightly but remains above the Federal Reserve’s target. Amid heightened uncertainty, the Federal Reserve held interest rates steady at 4.25%–4.50% at both of its meetings in Q2. Chair Jerome Powell stated that the Fed is “well positioned to wait for greater clarity before considering any adjustments to our policy stance.”

In Canada, tariffs and trade-related uncertainty continue to weigh on the economy. A pullforward of exports and inventory accumulation ahead of tariffs helped keep first-quarter GDP firm, but growth is expected to slow in the second quarter. The labour market has weakened, particularly in trade-sensitive sectors. Inflation remains within the Bank of Canada’s 1–3% preferred range. However, core CPI remains above the Bank’s preferred 2% target. Canada’s fiscal deficit is expected to widen as Prime Minister Mark Carney aims to fast-track infrastructure development and increase defense spending. Amid ongoing trade uncertainty, the Bank of Canada held its policy rate at 2.75% during its April and June meetings. Governor Tiff Macklem signaled the Bank’s readiness to cut rates further if economic conditions deteriorate.

Bond Markets: During Q2, the FTSE Canada Universe Bond Index returned -0.6%. Yields for Canadian bonds rose across all maturities over the quarter. That reflected reduced expectations for rate cuts by the Bank of Canada and a higher risk premium on long-term debt. The impact of higher yields on government bonds was offset in part by tightening of credit spreads on provincial and corporate bonds. Overall corporate bonds saw a positive return for the quarter and outperformed government bonds, in part due to the strong recovery in credit spreads that started in late

April. While corporate issuance slowed considerably in April due to increased trade policy uncertainty, issuance in the Canadian bond markets during May and June were robust. There were 83 deals during Q2 that combined to raise $37 billion for issuers. June 2025 was the 3rd busiest month for issuance on record. We continue to expect higher credit spreads as the U.S. tariffs impact global growth. As such, we have maintained our conservative view with a bias towards shorter corporate bonds but remain ready to invest in longer corporate bonds as valuations become

attractive.

Stock Markets – Overview: Having done a round-trip following April tariff announcements, technology, consumer discretionary and industrial companies propelled the U.S. equity market to another record high. The S&P 500 ended the quarter up about 11%, outperforming Canadian and international markets. Canadian equities gained 8.5% in Q2, buoyed by front-loaded demand that benefited the Materials sector, while Financials recovered from a poor Q1. Meanwhile, as risk sentiment stabilized following the 90-day tariff pause and U.S. equities regained momentum, the appeal of the “Sell America” trade diminished. As a result, Europe, Australasia, and the Far East (EAFE) markets finished the quarter with a more modest gain of just over 5%, lagging the sharper

recovery seen in North America.

U.S. Equities: The U.S. equity market staged a V-shaped recovery on strong company earnings data in the second quarter. A stable job market and muted inflation reinforced the view of a resilient U.S. economy. At a company level, we observed positive corporate earnings surprises, steady profit margins and better-than-expected forward earnings guidance. Together they underpinned the equity market’s sharp reversal to the upside. Market breadth also improved over the quarter, with strength extending beyond Technology to include Industrials and Financials. That signalled that the market rally was supported by investors’ confidence in the U.S. economy. Furthermore, structural investment trends in artificial intelligence (AI) continued to accelerate, highlighted by rising enterprise capex in data centres. Beyond AI, Circle, a blockchain-based platform that supports stablecoin issuance, tokenized assets, and digital payment infrastructure, conducted a successful IPO. Its share price jumped 485% from its listing price as of quarter-end. On June 17, the U.S. Senate passed the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act, a regulatory framework for use of tokenized assets. While investors wait for the House’s decision, equity price actions suggest that the policy environment is increasingly supportive of blockchain innovation and digital efficiency.

Canadian Equities: Canadian equities posted solid gains in Q2, with Financials overtaking Materials to lead the market higher. Momentum from the Materials sector, which benefited from the pull-forward demand related to U.S. tariff uncertainty, faded toward quarter-end. Meanwhile, cooling inflation and muted domestic growth pushed investors towards highquality, high-dividend-paying companies. Notably, banks significantly outperformed the broader market, as investors favoured their stable corporate fundamentals. Energy surged briefly amid escalating geopolitical tensions, but those gains proved short-lived. In recap, investors in the Canadian market faced slowing resource demand and a stalling domestic economy, which fueled increased interest in high-quality, high-dividend-paying companies. That is a trend we expect to continue going forward.

Bottom line: Markets remain heavily influenced by sentiment, with U.S. policy developments and ongoing tariff negotiations continuing to cause periodic volatility. However, there is little

evidence of deterioration in the hard data to date. As such, we continue to anchor our positioning on underlying data rather than market narratives. Looking ahead, the combination of a structurally higher-for-longer interest rate environment and increasingly pro-growth policy backdrop presents selective opportunities. In the U.S., this favours highquality growth stocks, particularly within Technology, where strong balance sheets and long-term thematic tailwinds remain intact. In Canada, Financials, especially the relatively inexpensive banks, present a more compelling opportunity as earlier tailwinds from pullforward demand are beginning to wane. While we remain constructive, we are mindful of elevated equity valuations and continue to closely monitor macro conditions and policy developments for signs of inflection.

Downloadable Copy

Mark Warywoda, CFA

VP, Public InvestmentsIan Whiteside, CFA, MBA

AVP, Public InvestmentsJohanna Shaw, CFA

Director, Public InvestmentsJin Li

Director, Equity Investments

Wanyi Chen, CFA, FRM

Sr. Quantitative Analyst

Andrew Vermeer, CFA

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Edward Ng Cheng Hi

Analyst, Credit

Francie Chen

Analyst, Rates

ADVISOR USE ONLY

-

Taking the guess work out of market volatility with Equitable Life

Investing during market highs and market lows can leave even the most seasoned investors scratching their heads. Knowing when to buy and when to sell is not easy, but disciplined investing can be.

Dollar cost averaging with Equitable Life® is designed to provide a long-term investment solution. This strategy helps take the guesswork out of knowing when to get into the market. It can also provide consistency for a long-term financial plan regardless of whether there is a lot or a little to invest.

And for a limited time only, we’ve increased the initial commission for the CB5 sales option from 5.6% to 7.0% on Pivotal Select™ segregated funds*, effective from May 20 to August 31, 2022.** During this time, advisors earn the increased full initial commission even if funds are placed into Equitable Life Money Market Fund to start the PAC.

For more information on dollar cost averaging, please contact your Equitable Life Regional Investment Sales Manager.

* Applies to FundSERV trades occurring between May 20 and August 31, 2022. Initial commission on non-FundSERV trades occurring between May 20 to August 31, 2022 increases from 4% to 5%. Initial commission is subject to a chargeback.

** Equitable Life reserves the right to end the campaign at any time and without notice.

™or ® denotes a registered trademark of The Equitable Life Insurance Company of Canada.

-

Digital tools for your clients and their plan members

In this issue:

- Digital tools for your clients and their plan members*

- QDIPC updates terms and conditions for 2024*

Digital tools for your clients and their plan members*

Do your clients know how to use all the available digital tools in their Equitable® benefits plans? With useful features for both plan administrators and their members, it’s even easier for your clients to access their plans online.Tools for plan administrators

- Our online plan member enrolment tool lets groups and administrators add new plan members online without completing paper forms

- The EquitableHealth.ca plan administrator portal makes it easy for plan administrators to manage their plan anytime and anywhere. Helpful features include:

- A premium calculator to calculate monthly costs for plan members

- A simple process for updating plan member information

- Digital welcome kits provide personalized information directly to plan members through email

- Easy, automated payment options help plan administrators avoid missed payments by offering pre-authorized debit or electronic funds transfer

Tools for plan members

- Our plan member portal at EquitableHealth.ca provides secure, 24/7 access to claims history and coverage details. It also lets members submit claims, and includes health and wellness resources

- Electronic notifications and claims payments give plan members claim updates via email and deposit payments directly into their bank account

- The Equitable EZClaim® mobile app lets plan members submit claims quickly and securely on-the-go from their mobile device

- Digital benefits cards give plan members the convenience to access their benefits cards easily from a mobile device

Help with digital benefits tools

We’ve created a brochure and video guide to help plan members use digital tools for a smoother, more convenient benefits experience.

Plan members can contact us at 1.800.265.4556 and select the option for Web Support if they need further assistance.

QDIPC updates terms and conditions for 2024*

Every year, the Quebec Drug Insurance Pooling Corporation (QDIPC) reviews the terms and conditions for the high-cost pooling system in the province.

Based on its latest review, QDIPC is revising its pooling levels and fees for 2024 to reflect trends in the volume of claims submitted to the pool, particularly catastrophic claims. These updates take effect January 1, 2024. You can view the updates here.

We will apply the new pooling levels and fees to future renewal calculations that involve Quebec plan members.

If you have any questions, please contact your Group Account Executive or myFlex Account Executive.

- [pdf] Daily/Guaranteed Interest Account - Product at a Glance

- [pdf] WL Annuity 20 Pay

- Change to the Performance Interest Options on universal life

- [pdf] Personalized Brochure - Benefits of segregated funds in a Tax-free Savings Account