Site Search

103 results for 31

- Policy Title Changes

- Anti-money Laundering Legislation Requirements Summary

-

Ways to reduce net income after age 71 with Equitable Life

Your client is contacting you to ask how to reduce net income after age 71. While each client’s situation is unique, here are a few options to consider.

- Clients with a spouse under the age of 71 can contribute to a spousal Retirement Savings Plan (RSP) up until December 31st of the year the spouse turns 71; provided contribution room is available. This option can also work for those clients over the age of 71 with employment income. This can be useful for small business owners who are still making money over the age of 71 and forced to convert their RSP to a Retirement Income Fund (RIF) or Life Income Fund (LIF).

- For clients with a RIF or LIF, they can strategically elect to use their spouses’ age to calculate the minimum RIF income payment (minimum and maximum for LIF). The idea being that if there is an age gap between spouses:

- Your client makes a RIF/LIF minimum payment lower by using the age of the younger spouse. This is beneficial to clients who do not need a lot of income from their RIF/LIF.

- Your client makes a LIF maximum payment higher by using the age of the older spouse. This is beneficial to clients who want to withdraw as much as possible from their LIFs each year.

To learn more, contact your Regional Investment Sales Manager.

® and TM denote trademarks of The Equitable Life Insurance Company of Canada

-

Competitive GIA rates and more!

With many bond funds declining in value over the past year, clients are looking for fixed income alternatives to reduce portfolio risk while providing a principal guarantee and an attractive interest rate.

Equitable Life® Guaranteed Interest Account (GIA) investment options are ideal for clients who want to create an emergency fund or save for a special purchase. And we’ve recently increased interest rates to make our GIA options even more competitive!

A few reasons to consider Equitable Life for your GIA business:- The GIA advantage – a life insurance contract can provide many estate planning benefits.

- Industry-leading compensation – we currently pay 40bps of commission per year of term.1 Many competitors only offer 20 – 25bps per year of term.2

- Cashable option3 – allows clients to access their money in case of unexpected circumstances. Not many competitors offer this feature.2

- Advisor rate discretion – advisors can forego up to 40bps of commission for an equal increase in interest rate, making our great rates even better.

- Step Up Your Wealth Sales program – 100% of GIA net deposits4 are used to calculate the 0.75% bonus commission earned on net deposits for 2022.

- Win-Win – our GIAs allow you to give the client a better interest rate while still earning a good commission.

For more information, please contact your Equitable Life Regional Investment Sales Manager.

1 Equitable Life commission rates as at May 19, 2022.

2 Competitive information as at November 20, 2021; Equitable Life does not guarantee the accuracy of competitive information.

3 Withdrawals made prior to the maturity date will be subject to a market value adjustment and may be subject to tax.

4 All eligible deposits, sales, and redemptions occurring between January 1 and December 31, 2022, will be used to calculate an advisor’s 2022 net deposits.

® denotes a registered trademark of The Equitable Life Insurance Company of Canada.

-

Give clients guaranteed retirement income with Payout Annuities

With increased market volatility and interest rates higher than we have seen for much of the past decade, now is a great time to consider payout annuities. Payout annuities can provide regular guaranteed income regardless of how markets perform.

Clients using only a Systematic Withdrawal Plan (SWP) for retirement income are potentially vulnerable during times of market volatility due to the sequence-of-returns risk.1 When markets are down, more units are redeemed to cover income needs. When markets later rise, clients are not able to participate fully in the recovery because more units were redeemed to provide income. That is why having a guaranteed income component, like a payout annuity, as part of an overall retirement strategy is so important.

Three great reasons to consider Equitable Life® for your payout annuity business:

1. Choose from a variety of payout annuity options including:

A. Life Annuity – guaranteed income for one life

B. Joint Life Annuity – guaranteed income for two lives

C. Term Certain – guaranteed income for a specific period of time (5 to 30 years)

D. Term Certain to Age 90 – guaranteed income until age 90

2. Attractive rates, particularly in Registered and Term Certain Annuities

3. Step Up Your Wealth Sales program - 25% of payout annuity net sales qualify for the 0.75% bonus commission earned on net deposits for 20222

.png "button-(1).png")

For more information, please contact your Equitable Life Regional Investment Sales Manager.

1Sequence-of-returns risk, or sequence risk, is the risk that an investor will experience negative portfolio returns very late in their working life and/or early in retirement.

2All eligible deposits, sales, and redemptions occurring between January 1 and December 31, 2022, will be used to calculate an advisor’s 2022 net deposits.

® denotes a registered trademark of The Equitable Life Insurance Company of Canada. -

Equitable Life Dynamic Global Real Estate Fund Select: More than an inflation hedge

Some clients may be missing out on the benefits of real estate investments. In addition to providing an inflation hedge, investing in real estate can help to diversify an investment portfolio and manage overall risk.

Check out Equitable Life Dynamic Global Real Estate Fund Select in this issue of Fund Focus.

The fund aims to achieve long-term capital appreciation and income by investing in publicly listed real estate companies across a spectrum of property types and geographies.

Reasons to Invest:- Access to high-quality and diversified real estate assets through public companies from around the world

- Real estate is an asset class highly sought after by pension funds and institutional investors

- The underlying Dynamic Global Real Estate Fund is the oldest real estate mutual fund in Canada (1996)

- A key pillar is protecting capital – manager focus is on providing downside protection

- Competitive MER of 2.64%*

Date posted: April 14, 2023

* effective December 31, 2022

™ or ® denote registered trademarks of The Equitable Life Insurance Company of Canada. -

Equitable Life Webcast Series featuring Equitable Life Dynamic Asia Pacific Equity Fund Select

Benjamin Zhan and Bruce Zhang will discuss the Equitable Life Dynamic Asia Pacific Equity Fund Select along with the fund's people, philosophy, process and performance.

Equitable Life® continues to spotlight various aspects of our competitive fund lineup and product offerings. This series gives advisors an opportunity to:

• learn more about products and product features,

• hear from industry professionals,

• learn about investment strategies; and so much more.

Join your host, Joseph Trozzo, Investment Sales Vice President, MGA, Equitable Life of Canada along with Dynamic Funds.Learn More

Continuing Education Credits

This webinar has been submitted for continuing education (CE) approval with the Insurance Council of Manitoba and Alberta Insurance Council for all provinces excluding Quebec. Upon approval, you will be sent an email notification to come back to the webinar presentation console to download your personalized certificate from the tool bar. To be eligible for CE credits, you must register individually, watch the webcast in full and complete a short quiz. This webcast is available in English only.

® denote a registered trademark of The Equitable Life Insurance Company of Canada

Posted May 31, 2023 -

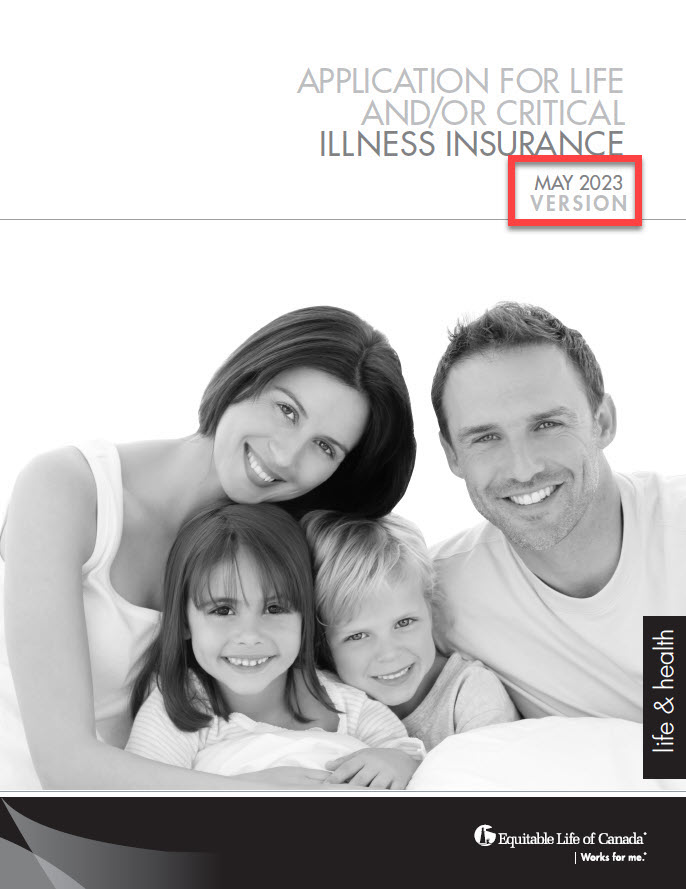

New 350 Life and CI Applications

On August 2nd, 2023, Equitable Life® will be updating the privacy and legal sections on some forms. This includes the form 350 Paper Application for Life and/or Critical Illness Insurance. This change will also be applied on our websites and our online application EZComplete®. These changes are part of Bill 64. The Bill is about the protection of personal and private information in Quebec. This will take effect on September 1st, 2023.

Due to this change, we ask all advisors to use the latest version dated May 2023 of the paper application after August 2nd. Applications in Quebec must use the lastest version from September 1, 2023 onwards.

For all regions outside Quebec, we will support a transition period from ‘old’ to ‘new’ applications until December 31st, 2023. After this date, we will no longer accept older versions of our Life and Critical Illness application.

To make sure you are using the latest version of the application, check the date on the title page. It should say May 2023. See the image below:

.jpg?width=200&height=259 "Form-350-Image-EN-(1).jpg")

To order paper copies, click here.

Email completed applications to supply@equitable.ca.

To learn more about Bill 64, please visit Assemblee nationale du Quebec - Bill 64. You may also contact your wholesaler.

® denote a registered trademark of The Equitable Life Insurance Company of Canada. -

Clients looking to add a little balance and diversification to their investment mix?

An Equitable® Guaranteed Interest Account (GIA) may be just the right fit for them. With competitive interest rates, Equitable GIAs may be an ideal solution for clients looking to create a well-diversified and balanced portfolio.

A few reasons to consider Equitable for your GIA business:

-

• The GIA advantage – a life insurance contract can provide many estate planning benefits.

-

• Advisor rate discretion – advisors can forego up to 40bps of commission for an equal increase in interest rate, making our great rates even better.

-

• Step Up Your Wealth Sales program1 – 100% of GIA net deposits are used to calculate the 0.75% bonus commission earned on net deposits for 20242.

Bookmark this page to check our current rates.

For more information, please contact your Director, Investment Sales.

1 Equitable reserves the right to alter or terminate this program at any time and without notice.

2 All eligible deposits, sales, and redemptions occurring between January 1 and December 31, 2024, will be used to calculate an advisor’s 2024 net deposits. See full Step Up Your Wealth Sales program details for more information.

® denotes a registered trademark of The Equitable Life Insurance Company of Canada.

Date posted: May 9, 2024 -

- Retirement Planner Calculator