Site Search

770 results for PROBLEMGO.com Paying to have an arrest record sealed dark web browse here anonymity guaranteed now

-

Ways to reduce net income after age 71 with Equitable Life

Your client is contacting you to ask how to reduce net income after age 71. While each client’s situation is unique, here are a few options to consider.

- Clients with a spouse under the age of 71 can contribute to a spousal Retirement Savings Plan (RSP) up until December 31st of the year the spouse turns 71; provided contribution room is available. This option can also work for those clients over the age of 71 with employment income. This can be useful for small business owners who are still making money over the age of 71 and forced to convert their RSP to a Retirement Income Fund (RIF) or Life Income Fund (LIF).

- For clients with a RIF or LIF, they can strategically elect to use their spouses’ age to calculate the minimum RIF income payment (minimum and maximum for LIF). The idea being that if there is an age gap between spouses:

- Your client makes a RIF/LIF minimum payment lower by using the age of the younger spouse. This is beneficial to clients who do not need a lot of income from their RIF/LIF.

- Your client makes a LIF maximum payment higher by using the age of the older spouse. This is beneficial to clients who want to withdraw as much as possible from their LIFs each year.

To learn more, contact your Regional Investment Sales Manager.

® and TM denote trademarks of The Equitable Life Insurance Company of Canada

-

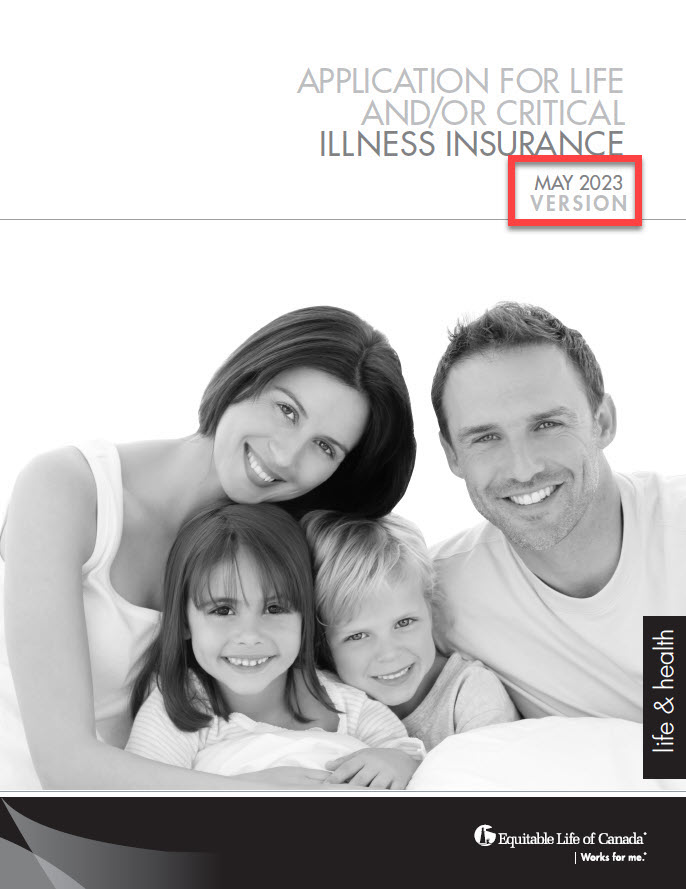

New 350 Life and CI Applications

On August 2nd, 2023, Equitable Life® will be updating the privacy and legal sections on some forms. This includes the form 350 Paper Application for Life and/or Critical Illness Insurance. This change will also be applied on our websites and our online application EZComplete®. These changes are part of Bill 64. The Bill is about the protection of personal and private information in Quebec. This will take effect on September 1st, 2023.

Due to this change, we ask all advisors to use the latest version dated May 2023 of the paper application after August 2nd. Applications in Quebec must use the lastest version from September 1, 2023 onwards.

For all regions outside Quebec, we will support a transition period from ‘old’ to ‘new’ applications until December 31st, 2023. After this date, we will no longer accept older versions of our Life and Critical Illness application.

To make sure you are using the latest version of the application, check the date on the title page. It should say May 2023. See the image below:

.jpg?width=200&height=259 "Form-350-Image-EN-(1).jpg")

To order paper copies, click here.

Email completed applications to supply@equitable.ca.

To learn more about Bill 64, please visit Assemblee nationale du Quebec - Bill 64. You may also contact your wholesaler.

® denote a registered trademark of The Equitable Life Insurance Company of Canada. -

New publication: CLHIA consumer guide for critical illness

In February, the Canadian Life and Health Insurance Association (CLHIA) published a new consumer guide for critical illness. This guide covers what clients need to know about critical illness.

Some of the topics include:

● What critical illness insurance covers in Canada

● If critical illness insurance is the right choice for a client

● What critical illness insurance policies may or may not include

● Plan types and offerings

● And more!

Equitable is committed to helping clients make informed decisions about their insurance needs. You can find links to the CLHIA critical illness consumer guide on equitable.ca and through EquiNet > Individual Insurance > Critical Illness. You can also find a link to the CLHIA agent guide for critical illness on EquiNet.

Share this with clients in addition to the great resources below!

Critical illness insurance with Equitable video: View on Vimeo.

Critical illness prospective letter template – simply fill it out and send off to your clients!

Want to earn CE credits? Check out our Critical Illness Path to Success program.

Need more information?

Your Equitable Wholesaler is here to help!

® and TM denote trademarks of The Equitable Life Insurance Company of Canada. -

Do clients imagine owning a dream home?

We’re here to help make that happen! Clients who contribute to a First Home Savings Account between May 1 and September 30, 2025, will be entered for a chance to win an incredible $8,000 in our Close to Home contest. Whether opening a new account or making an annual contribution, this is a golden opportunity to help them get one step closer to homeownership.Advisors, Your Efforts Matter Too! By guiding clients towards their homeownership dreams, you’ll be entered to win $1,000 as a special thank you for your dedication and support. At Equitable®, we believe that when we grow together, success is mutual.

Don’t Miss Out! Enter today using Equitable’s user-friendly online application platform, EZcomplete®, or process an online transaction with ease using Equitable’s EZtransact®. It’s fast, simple, and could bring clients closer to their dream home.Want to learn more? Speak to your Director, Investment Sales, and help clients take the first step towards making homeownership a reality.

Equitable’s Close to Home Contest: No purchase necessary. Contest period May 1, 2025, to September 30, 2025. Enter by making a deposit to an Equitable FHSA during the contest period or by submitting a no-purchase entry. Two prizes for a total value of $8,000 CAD to be drawn on October 15, 2025, will be awarded. The servicing advisor for the policy to which the selected entrant made the deposit is also an eligible winner and will receive a $1,000 CAD prize. For example, if an Equitable client is a winner of the $8,000 prize, the client’s servicing advisor wins a $1,000 prize. Open to legal residents of Canada of the age of majority. Odds of winning depend on number of eligible Entries received during the Contest Period. For full contest rules, including no-purchase method of entry, see the full contest rules.

- Individual insurance video library

-

Equitable Life Coronavirus Update – March 13, 2020

As the coronavirus (COVID-19) continues to spread, it’s important that you, your clients and their plan members have the most up-to-date information. We are providing timely updates on any developments that impact your clients and their plan members or their benefits coverage.

Please share this information with your clients. You can direct them to EquitableHealth.ca, where we have posted a version of these updates.

Coronavirus travel coverage*

For groups with Travel Assist coverage

The Public Health Agency of Canada has issued several Travel Health Notices advising Canadians to avoid travel to countries and regions where there have been outbreaks of coronavirus (COVID-19).

A good resource to help your clients and their plan members understand how the spread of the coronavirus may impact their travel plans is the Public Health Agency of Canada’s Coronavirus Travel Advice site. The levels of risk by country and region are regularly updated.

If your clients’ plan members cannot avoid travelling, Public Health recommends they take steps to prevent illness and seek medical attention if they become sick.

Where to find the latest information

The list and level of travel advisories can change at any time. Please check the Government of Canada’s Travel Advisor and Advisory page for the most current information.

If your clients’ plan members have coronavirus symptoms while travelling, please advise them to contact Travel Assist at the numbers listed below for assistance.

Advise plan members to call before they travel

If a plan member is travelling anywhere outside of the province or country and their benefits plan includes Travel Assist, plan administrators should advise them to make sure they’re prepared for a medical emergency by following these steps.

- Check the Government of Canada’s Travel Advisor and Advisory page. Note that it is important to click on the country to check whether any specific regions of that country have travel advisories.

- If they have questions, they should call Travel Assist before they travel for assistance and benefit information.

- Pack their Equitable Life benefits card and provincial health card.

- In a medical emergency, call the Travel Assist 24-Hour Hotline:

- Toll-free Canada/USA: 1.800.321/9998

- Global call collect: 519.742.3287

- Allianz Global Assistance ID #9089

Allianz Global Assistance administers Equitable Life’s Travel Assist benefits. Allianz has an international network of medical facilities, transportation providers, medical correspondents and multilingual administrative agents who aid with medical, legal and most travel-related emergencies 24-hours a day, seven days a week.

Early prescription refills and drug shortages*

In response to concerns about COVID-19 TELUS Health, our pharmacy benefits manager, has announced it is maintaining its standard rules for refills of medication. Plan members can refill their medications when at least two-thirds of the last dispensed supply has been used.

If plan members need more than the maximum supply allowed on their plan, they must pay out-of-pocket for the excess amount. They can then submit a claim to ask for an exception request.

TELUS is taking this position to help maintain access to medication for all patients. They continue to monitor the situation. We will provide an update if it changes.

Drug shortages

TELUS Health monitors for drug shortages and updates their system for any unavailable drugs. This helps to ensure accurate claims payment. If a referenced lowest-cost generic drug is unavailable, claims for drugs in the class will be paid at the next lowest-cost generic alternative available.

*Indicates content that will be shared with your clients

-

May 2023 eNews

Update: Introducing changes to our Diabetes Management Program

Beginning June 1, 2023, we are introducing additional standard drug plan controls as part of our Diabetes Management Program.

The controls will apply to GLP-1 agonists approved by Health Canada for the treatment of diabetes, such as: Adlyxine, Mounjaro, Ozempic, Rybelsus, Trulicity, and Victoza.

This change will help manage the impact of these high-cost diabetes medications for your clients while continuing to provide plan members with access to effective treatments to manage their disease.

Why are we introducing this change?

GLP-1 agonists are the highest cost diabetes drugs on the market. Current Diabetes Canada Clinical Practice Guidelines recommend that most Type 2 diabetics begin treatment with lower-cost and equally effective first-line therapies, such as Metformin.

Some GLP-1 agonists are also used “off-label”. In other words, they are often prescribed for conditions for which they have not been approved by Health Canada, such as weight loss.

These additional controls will help ensure that these drugs are used appropriately – only for the treatment of diabetes and only after other first-line treatments have been tried.

If a client wishes to provide coverage for drugs specifically approved by Health Canada for weight loss, we have coverage options available.

How will this program work?

Plan members who receive a new prescription for a GLP-1 agonist will need to try a first-line diabetic treatment before they are eligible for coverage of the GLP-1 agonist. If the plan member has previously tried first-line therapies and found them ineffective, they will be eligible for a GLP-1 agonist.

Plan members who are already taking a GLP-1 agonist to treat diabetes will continue to be eligible for coverage. Some claimants may need to provide confirmation of their diabetes diagnosis from their physician or pharmacist in order to maintain coverage. We will provide claimants ample time to confirm their diagnosis.

Questions?

If you have any questions about these additional standard controls or how they will impact your clients, please contact your Group Account Executive or myFlex Sales Manager.

Coming soon: Survey for plan administrators with recent disability claims

We are regularly enhancing our communication processes to help your clients with disability plans manage their workplace absences more effectively. Later this month, we will distribute a short survey to plan administrators who have submitted a disability claim in the past six months. The survey will ask recipients about their satisfaction with the frequency and detail of our disability management communications.

The email will come from GBClientFeedback@equitable.ca, and the survey will remain open until the end of the day on May 19, 2023. All responses will be confidential. Survey respondents will receive the option to provide their contact information so that we can follow up on feedback they have provided.

We plan to use the feedback to help ensure that we’re meeting your clients’ expectations and delivering industry-leading service.

In a previous issue of eNews, we published a list of the average dental fee increases for general practitioners based on the latest Provincial and Territorial Dental Association fee guides.

Since then, the Canadian Life and Health Insurance Association (CLHIA) has updated the 2023 dental fees for some provinces. Provinces with dental fee updates since our previous eNews are bolded and italicized. Equitable Life uses these guides to help determine the reimbursement limits for dental procedures. For your reference, below is the list of the average dental fee increases for general practitioners that will be used by Equitable Life for 2023.

-

Revised Witness Signature Process during COVID-19 for Individual Life and Critical Illness Insurance

Revised Witness Signature Process during COVID-19 for Individual Life and Critical Insurance Business

We are temporarily revising our policy around witness signatures during COVID-19. While the preference is to have a witness when one is available, we understand that may be difficult given our current environment.

Please follow the options below for witness signature with the first option being most preferable, and the last option being the least preferable:

1. Signature from a witness who is a disinterested party

2. Signature from a witness who is a party with an interest

3. No witness

If we receive a form that doesn’t have a witness signature, we will still process the form. Just a reminder this is only temporary during COVID-19.

- [pdf] Buy-sell agreements

-

Equitable Savings & Retirement Division rebrands as Individual Wealth

The Equitable® Savings & Retirement division has a new name: Individual Wealth.

This change reflects how the division has grown. Over time, we have added more services and tools to help clients reach their financial goals. Our new name shows this broader focus.

Why “Wealth”?

The word “Wealth” means more than just saving for retirement. It includes investing, estate planning, tax strategies, and preparing for life events. It better describes our more holistic approach to wealth management.

This update is more than just a name change. It shows our strong commitment to helping clients in new and better ways. Over the coming months you’ll notice changes across our materials, website, and contact details as we roll out this transformation. As we move forward as Individual Wealth, our commitment to supporting your business remains stronger than ever — because when we grow together, success is mutual.

If you have any questions, feel free to reach out to your Director, Investment Sales.

Date posted: July 24, 2025