Site Search

762 results for visit page here PROBLEMGO.com husband locked up need him out fast cash

-

REMINDER that paper applications with a version date prior to 2021/04/02 are set to expire July 1, 2

To comply with the Government of Canada’s anti-money laundering legislation and FATCA/CRS changes, Equitable Life® has updated its Savings and Retirement and Life Insurance applications.

If you currently have applications with a version date before 2021/04/02, please destroy them and use our online pdf applications or order new applications from our Supply Team. Paper applications with a version date prior to 2021/04/02 (located on the back page and in the bottom right-hand corner of the application) will no longer be accepted after July 1, 2021 for:

● Savings and Retirement (Form #1383, #1384, #799, #355), and

● Life Insurance (Form #350)

To learn more about the Government of Canada’s anti-money laundering legislation and FATCA/CRS review the following links:

Want to be sure you always have the most up-to-date application? Try our EZcomplete® online platform for Individual Life, Critical Illness and Segregated fund applications.

For a complete list of all forms and applications affected by the anti-money laundering legislation, refer to the following links:

● Savings and Retirement Anti-money Laundering Legislation Requirements Summary.

● Life Insurance Anti-money laundering Legislation Requirements Summary.

● Government of Canada - Guidance on the Common Reporting Standard

● Financial Transactions and Reports Analysis Centre of Canada

If you have any other questions, contact your Regional Sales Manager or Equitable Life’s Advisor Services Team

® denotes a registered trademark of The Equitable Life Insurance Company of Canada.

- About

-

Sofie wants to provide for her children long after she’s gone with Equitable Generations Universal L

Sofie knows the future is uncertain. As a mom of two children and in her late forties, Sofie wants to continue to help her kids with their life goals as they get older.

She learns that Universal Life insurance from Equitable® is a great fit for her. It has investment options, choices of death benefit and even flexibility on how she pays for her premiums. With the investment option, she can earn tax-advantaged growth*.

Watch our new Universal Life Insurance from Equitable video to learn more. See it on Vimeo

This video can help you talk with clients about Universal Life insurance. It walks them through what it is, how it works, and the affordability and flexibility it features. It highlights just how Universal Life from Equitable is an insurance solution truly designed to meet the needs of clients today and into tomorrow.

Not sure where to start? Send clients this draft prospecting letter which you can personalize specifically for them.

Plus, check out our Universal Life solution page on EquiNet®, then click on the Marketing Materials tab for the latest Universal Life Marketing Materials.

Want to learn more? Ask your Equitable wholesaler!

View on Vimeo

*Subject to the Income Tax Act of Canada.

-

Equitable 2024 dividend scale!

Equitable’s Board of Directors has approved a new dividend scale for the period of July 1, 2024, to June 30, 2025.

● The interest rate* we use for the dividend scale will change. It will go from 6.25% to 6.40% on July 1, 2024.

● Other factors used to decide the dividend scale will remain the same.

● The interest rate for policies with dividends on deposit will change. It will go from 2.25% to 3.50% on July 1, 2024.

● The interest rate for most policy loans will remain at 6.50%. This applies to both new and existing policy loans, and automatic premium loans. It specifically applies to Equimax® policies with a 9-digit policy number that starts with either "3" or "8". Older policies may have different loan rates as they are based on the prime interest rate.

Learn more:

● 2024 Advisor Dividend Scale Notice

● 2024 Client Dividend Scale Notice

● Dividend Information Page

Did you miss our Spring update & 2024 Dividend Scale announcement? Watch it now:

(*The French and Chinese events will be partially in English, with sub-titles on screen).

*The dividend scale interest rate (DSIR) is different from the participating account (PAR) rate of return. The PAR rate of return is the return on the investments in the participating account over the calendar year. The DSIR smooths out the ups and downs of the participating account experience. -

Market Commentary January 2025

Key Takeaways

Full year 2024:

-

Despite reductions of policy-setting interest rates by central banks, yields on longer-term bonds finished the year higher than they started the year.

-

Positive risk appetite helped corporate bonds perform well, led by lower-quality issuers.

-

Global equity markets posted robust returns, with U.S. equities outperforming other developed markets, driven by heavy concentration into the ‘Magnificent 7’ stocks.

Fourth Quarter:

-

Central banks continued to ease monetary policy in Q4, with the Bank of Canada cutting its policy interest rate more aggressively than did the U.S. Federal Reserve.

-

The Republican victory across both the executive and legislative branches in the U.S. ignited expectations of economic growth, pushing bond yields and stock prices higher.

-

Risk sentiment helped corporate bonds continue to outperform government bonds.

-

Markets remained volatile: while North American stock markets continued to outperform most international indices, Canadian stocks managed to outperform U.S. stocks in Q4, as sources of returns in the U.S. narrowed into year-end.

Economic and Market Update

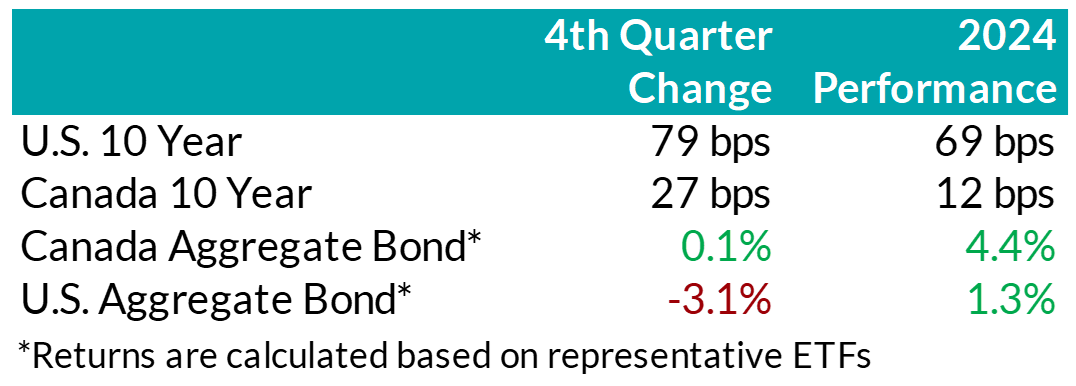

Economic Summary: In the U.S., economic activity continued to expand at a solid pace in Q4. The rate of inflation continued to slow but remained above the central bank’s 2% objective. The labour market in the U.S. remained resilient, as the unemployment rate has remained low compared to historical norms. A decisive victory for Donald Trump and the Republican Party further boosted expectations for continued growth. The return of the President-elect’s old tactics of threatening tariffs to influence trade, security, and drug control re-introduced some economic uncertainty, particularly regarding the potential return of inflationary pressures. Those concerns prompted the Federal Reserve to slow the pace of its policy easing, as it lowered rates by just 0.25% at each of its two meetings in Q4, following the 0.50% cut in September. Throughout 2024, the Fed reduced rates by a total of 100 basis points, from 5.50% to 4.50%. Nonetheless, bond yields were significantly higher for most maturity terms during the fourth quarter as the market priced in not just a stronger economy than had been the expectation during Q3, implying less interest rate cuts by the Fed, but also growing concerns about the government deficit.

In Canada, growth remained positive during 2024 and improved a bit to close the year, but continued to fall short of the Bank of Canada’s expectations. Similarly, inflation came in lower than expected and below the Bank’s 2% target. The labour market continued to soften for much of the year, with employment growth falling short of labour force growth. The weakness in the labour market and economy, along with tamed inflation, prompted the Central Bank to cut rates at the pace of 50 basis points at each of its two meetings in Q4. For the full year, the Bank of Canada ended up lowering its policy rate by a total of 175 basis points, from 5% to 3.25%. The market has been expecting the Bank of Canada to need to continue cutting rates due to slower economic growth in Canada, but the fear of a possible trade war with the U.S. has made the economic outlook somewhat murkier.

.png "Chart1-(1).png")

Bond Markets: During the quarter, yields on mid- to long-term bonds in Canada rose in sympathy with rising bond yields in the U.S. However, bond yields in Canada rose to a lesser extent, and yields on shorter-term bonds were actually little changed over the quarter. The FTSE Canada Universe Bond Index was basically flat during Q4 and posted a return of 4.2% for the full year. Although interest rates rose, credit spreads (i.e. the extra yield on corporate bonds versus government bonds to compensate for their extra risk) continued to grind lower, helping corporate bonds post positive overall returns in the quarter. Tightening credit spreads reflected the generally positive risk-on tone to the market, despite some volatility. Lower-rated BBB bonds generally performed better than higher-quality A-rated bonds. Credit spreads have now generally fallen back to levels similar to those experienced in 2021, when markets did quite well after the pandemic. The on-going appetite of investors for the extra yield offered by corporate bonds over government bonds is indicated not just by falling credit spreads, but also by investors’ enthusiasm to support the primary issuance market. Corporate bond supply continued to be very robust in the quarter, with $30 billion in new issuance, resulting in a record-breaking year with $141 billion of new issuance in 2024. Nonetheless, on balance, we do not think the current risk premium adequately compensates for downside risk, particularly in longer-dated corporate bonds, and have a bias towards shorter-dated credit where we view the risk / reward trade-off as being more favourable.

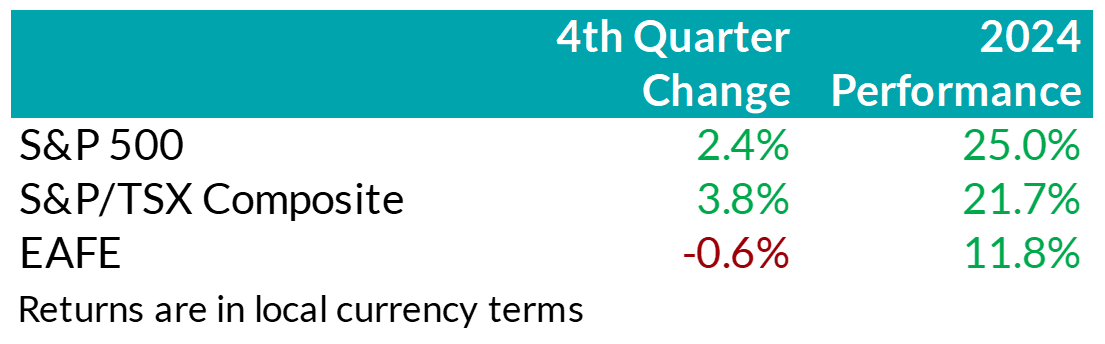

.png "Chart2-(1).png") Stock Markets – Overview: Trump’s presidential victory and the Republican party’s ‘red sweep’ in the Senate and House of Representatives sparked optimism surrounding economic growth and a new era of U.S. exceptionalism. As a result, North American equity markets extended their rally in Q4, capping off a year of robust returns. The S&P 500 returned 2.4%, bringing its year-to-date return to 25%. Within the U.S., the broadening of returns paused during the quarter as the chase for growth intensified, with mega-cap growth names like Tesla driving performance. Canadian equities surprisingly outperformed the U.S. market over the quarter, returning 3.8% in Q4, despite threats of widespread tariff negotiations looming on the horizon that could negatively impact Canadian corporate fundamentals. At a sector level, strength in the technology, financials, and energy sectors more than offset weakness in telecommunication companies as well as in the materials sector. Elsewhere, major developed markets from Europe and Asia (EAFE) underperformed last quarter as deteriorating Chinese growth prospects and weak economic growth in the Eurozone weighed on equities. Notably, foreign investors of U.S. denominated securities benefitted from a rebounding U.S. dollar with the dollar index adding over 7.6% in Q4.

Stock Markets – Overview: Trump’s presidential victory and the Republican party’s ‘red sweep’ in the Senate and House of Representatives sparked optimism surrounding economic growth and a new era of U.S. exceptionalism. As a result, North American equity markets extended their rally in Q4, capping off a year of robust returns. The S&P 500 returned 2.4%, bringing its year-to-date return to 25%. Within the U.S., the broadening of returns paused during the quarter as the chase for growth intensified, with mega-cap growth names like Tesla driving performance. Canadian equities surprisingly outperformed the U.S. market over the quarter, returning 3.8% in Q4, despite threats of widespread tariff negotiations looming on the horizon that could negatively impact Canadian corporate fundamentals. At a sector level, strength in the technology, financials, and energy sectors more than offset weakness in telecommunication companies as well as in the materials sector. Elsewhere, major developed markets from Europe and Asia (EAFE) underperformed last quarter as deteriorating Chinese growth prospects and weak economic growth in the Eurozone weighed on equities. Notably, foreign investors of U.S. denominated securities benefitted from a rebounding U.S. dollar with the dollar index adding over 7.6% in Q4.

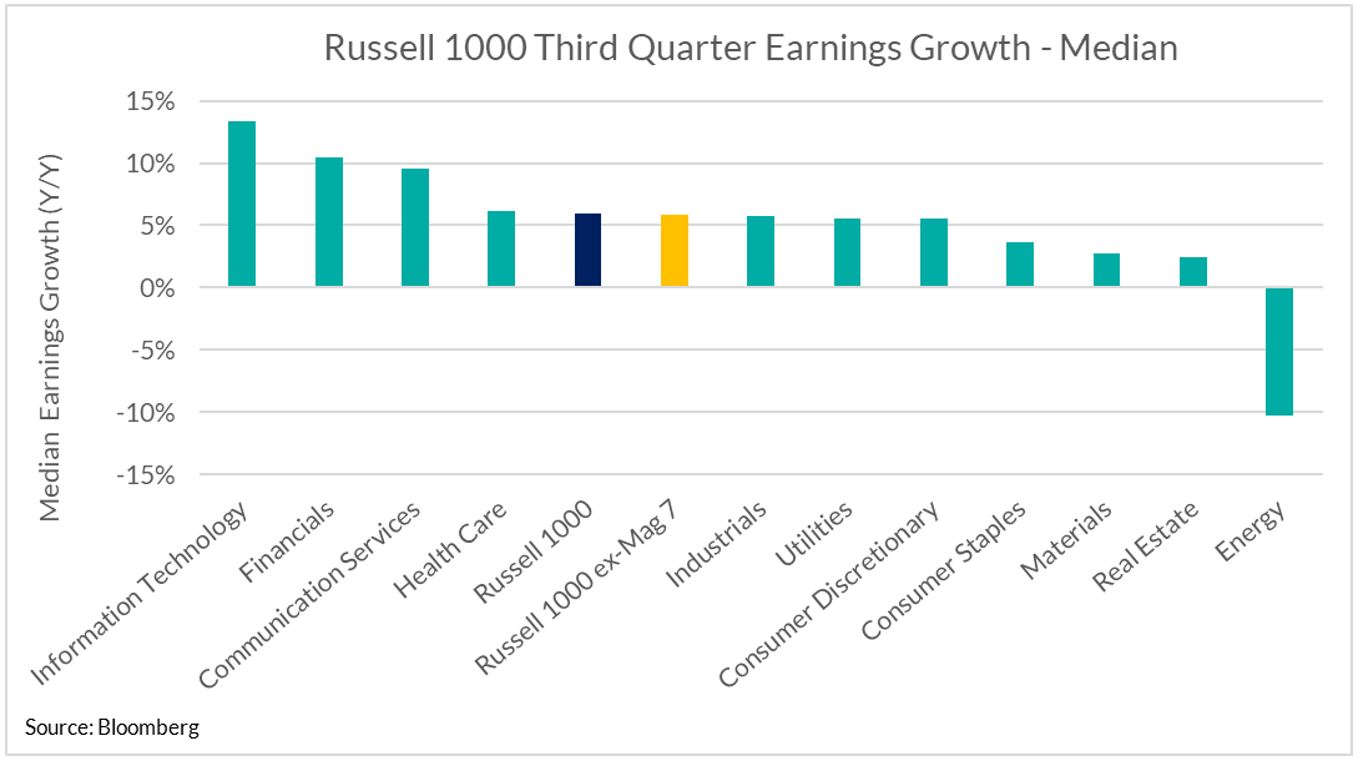

.png "Chart3-(1).png") U.S. Equities: U.S. equities remain supported by resilient margins and strong corporate earnings growth with over 70% of businesses surpassing bottom-line expectations last quarter. We remain attentive to the broadening of earnings performance and note that this trend has continued, albeit at a normalized pace versus prior quarters. More specifically, our work shows that members of the Russell 1000, excluding the Magnificent 7, posted median earnings growth of 6% last quarter, down from nearly 9% in Q3 but comparable to Q2 (6%). Looking forward to 2025, analysts continue to forecast U.S. exceptionalism, with forecasts of ~12% earnings growth.

U.S. Equities: U.S. equities remain supported by resilient margins and strong corporate earnings growth with over 70% of businesses surpassing bottom-line expectations last quarter. We remain attentive to the broadening of earnings performance and note that this trend has continued, albeit at a normalized pace versus prior quarters. More specifically, our work shows that members of the Russell 1000, excluding the Magnificent 7, posted median earnings growth of 6% last quarter, down from nearly 9% in Q3 but comparable to Q2 (6%). Looking forward to 2025, analysts continue to forecast U.S. exceptionalism, with forecasts of ~12% earnings growth.

Following Trump’s presidential victory, stocks with greater sensitivity to the U.S. economy, such as small cap businesses, benefitted from expectations of domestically focused growth initiatives. However, stubborn inflation and expectations of fewer interest rate cuts by the Federal Reserve saw the trend of broadening sources of returns pause into the end of the year. Instead, market concentration reaccelerated with investors rushing back towards mega-cap growth stocks. In fact, Tesla – which is approximately 2% of the S&P 500 Index by market cap – contributed approximately one-third of the total index return in Q4, while the Mag 7 as a group contributed over 100% of total returns. In other words, U.S. large cap companies excluding the Magnificent 7 declined in aggregate last quarter.

Canadian Equities: Against the backdrop of cooling inflation and below-trend growth, the Bank of Canada continued to loosen monetary policy. As a result, Canadian companies

showed signs of improving efficiency with return on equity – a gauge of corporate profitability – improving versus prior quarters. Under these conditions, investors remained focused on higher quality, high-dividend paying companies – particularly within the financial sector. Relative to prior quarters, this group witnessed greater contribution out of non-bank financials (such as asset managers and insurance companies), as the premium investors were willing to pay for Canadian banks remained elevated. Across other sectors, the energy sector had a positive quarter as the price of oil stabilized, but falling prices for raw industrials pushed the materials sector lower.

Bottom line: U.S. political developments and subsequent growth expectations dominated market sentiment last quarter. As a result, investors dialed back rate cut expectations and bond yields moved higher. In equity markets, the potential for an era of higher-for-longer rates prompted a resumption of investors crowding into growth stocks. Going forward, we remain cautious of elevated valuations and continue to prioritize diversified sources of returns with a long-term outlook. Nonetheless, despite rich valuations, our base case remains that investors’ enthusiasm for equities will persist in the near-term and stocks should continue to outperform bonds.

Downloadable Copy

ADVISOR USE ONLYMark Warywoda, CFA

VP, Public Portfolio ManagementIan Whiteside, CFA, MBA

AVP, Public Portfolio ManagementJohanna Shaw, CFA

Director, Portfolio ManagementJin Li

Director, Equity Portfolio Management

Tyler Farrow, CFA

Senior Analyst, Equity

Andrew Vermeer

Senior Analyst, Credit

Elizabeth Ayodele

Analyst, Credit

Francie Chen

Analyst, Rates

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

Any statements contained herein that are not based on historical fact are forward-looking statements. Any forward-looking statements represent the portfolio manager’s best judgment as of the present date as to what may occur in the future. However, forward-looking statements are subject to many risks, uncertainties, and assumptions, and are based on the portfolio manager’s present opinions and views. For this reason, the actual outcome of the events or results predicted may differ materially from what is expressed. Furthermore, the portfolio manager’s views, opinions or assumptions may subsequently change based on previously unknown information, or for other reasons. Equitable® assumes no obligation to update any forward-looking information contained herein. The reader is cautioned to consider these and other factors carefully and not to place undue reliance on forward-looking statements. Investments may increase or decrease in value and are invested at the risk of the investor. Investment values change frequently, and past performance does not guarantee future results. Professional advice should be sought before an investor embarks on any investment strategy.

-

-

Our Critical Illness Insurance Path to Success Program

Our Critical Illness Insurance Path to Success program was designed with you, the Advisor, in mind.

Path to Success: Expert Advice on navigating CI Sales provides you with actionable ideas and scripts that you can implement immediately into your critical illness insurance meetings. CE Credits are available if you review the program in its entirety and complete the quizzes at the end of each section.

Learn more about the CI Path to Success Program

Next steps:

If you have any questions or are interested in getting access to this program, please reach out to your Regional Sales Manager directly.

Enhancements to our Critical Illness Insurance product EquiLiving®

The timing couldn’t be better for connecting with your Regional Sales Manager to gain access to this program, as we have made recent enhancements to our Critical Illness product that will help you offer more options to clients. We’ve enhanced our EquiLiving plans and riders with:

• 20 pay options with coverage to age 75 or coverage for life

• Support from Cloud DX to help monitor a client’s well-being from treatment to recovery

• Added Acquired Brain Injury as a covered critical condition

• 30-day survival period removed for all non-cardiovascular covered conditions

• No age restriction to claim for Loss of Independent Existence (LOIE)

• Adult Covered Conditions definitions updated to 2018 CLHIA definitions

• Increased the number of Early Detection Benefit covered conditions from 4 to 8

• And so much more …

Contact your Regional Sales Manager to get set up in the program and learn about other CE accredited presentations happening each week. -

Celebrating our wins – 2023 Individual Insurance Marketing Recap

Equitable® would like to wish everyone a Happy New Year and we are looking forward to doing more business together in 2024!

As we start a brand new year, we would like to share with you some highlights of our 2023 initiatives in Individual Insurance. These projects aimed to make it easier to do business and enrich your experience of working with us.

Digital & Administration Enhancements

Our 2023 digital transformation initiatives ensured smoother processes, streamlined operations, and improved user experiences for advisors and clients:

● Digital Transactions for Universal Life Plans

● Text Notifications Keep You Informed on Your New Business

● New Online Policy Loan Form

● EZcomplete Enhancement for Critical Illness

● New Life & CI Application

Product Updates

Equally pivotal were our efforts in enhancing our individual life insurance solutions to empower you to confidently recommend us to clients:

● A Tune-Up for Equimax

● The Equimax Evolution Continues

● Critical Illness Insurance Update

● New Dividend Scale Interest Rate

To learn more about the above initiatives, kindly reach out to your local wholesaler.

Thank you for entrusting us with your business in 2023!

Continue watching for news from Equitable for more great launches and enhancements in 2024!

® or TM denote trademarks of The Equitable Life Insurance Company of Canada -

Equitable Life Group Benefits Bulletin – February 2022

In this issue:

- Update: Alberta biosimilar coverage changes*

- Preferred Biosimilar Program*

- Responding to Quebec’s biosimilar policy*

- Dental fee guide updates*

- Reminder: Review manual allocations for HCSAs and/or TSAs*

- Mental health resources for plan members*

Update: Alberta biosimilar coverage changes*

In 2022, Alberta’s provincial drug plan is adding four originator biologics to its Biosimilar Initiative. It has ended or will end provincial coverage of these drugs for some or all conditions, as follows:

Four originator biologics added to Alberta Biosimilar Initiative- Lovenox: Jan. 10, 2022

- Humalog: Feb. 1, 2022

- NovoRapid: April 1, 2022

- Humira: May 1, 2022

Patients 18 and over who are using these drugs for the affected conditions will be required to switch to biosimilar versions of the drugs to maintain coverage under the province’s government drug plan.

How we are responding to protect our clients

To help prevent this change from resulting in additional costs for our clients’ drug plans while still providing plan members with access to safe and effective medications, we will no longer cover these originator biologic drugs for plan members in Alberta.

Effective May 1, 2022, claimants currently taking these drugs will be required to switch to a biosimilar version of the drug to maintain coverage under their Equitable Life plan.

This is a continuation of the Alberta biosimilar switch program we launched last March, when the province first introduced its Biosimilar Initiative.

Do my clients need to take any action?

No action is required by plan sponsors. Plan members taking these targeted originator biologics will be contacted directly to allow them ample time to transition to a biosimilar. Any cost savings associated with the change will be factored in at renewal.

Groups that opted out of the biologic coverage changes we made last March will automatically be opted out of these coverage changes, as well as any future changes to our Alberta biosimilar switch program. This means that their drug plans will continue to provide coverage to existing claimants for any originator biologics we stop covering as part of our biosimilar program.

Advisors with clients who wish to opt out of our Alberta biosimilar program, or who previously opted out and want to opt back in, should speak to their Group Account Executive or myFlex Sales Manager.

Communication to plan members

We will be communicating these coverage changes with affected claimants in early March to allow them ample time to change their prescriptions and avoid any interruptions in their treatment or their coverage. Thus far, the transition to biosimilars, has been smooth and continues to be successful.

What is the difference between biologics and biosimilars?

Biologics are drugs that are engineered using living organisms like yeast and bacteria. The first version of a biologic developed is known as the “originator” biologic. Biosimilars are also biologics. Biosimilars are highly similar to the drugs they are based on and Health Canada considers them to be equally safe and effective for approved conditions.

Questions?

If you have any questions about this change, please contact your Group Account Executive or myFlex Sales Manager.Preferred Biosimilar Program*

As part of our ongoing efforts to help ensure the sustainability of your clients’ drug plans, we continue to engage in strategic partnerships with pharmaceutical manufacturers.

We are pleased to announce a partnership to make Hyrimoz our preferred biosimilar for Humira. This partnership will generate additional savings for plan sponsors.

Plan members will still have the choice to use Humira biosimilars other than Hyrimoz. However, in the absence of alternative sources of reimbursement, this may increase their out-of-pocket amount.

The Preferred Biosimilar Program will take effect March 1, 2022 for all new claimants across Canada who start using a Humira biosimilar. It will take effect May 1 for existing claimants in Alberta who switch to a Humira biosimilar, to align with changes to the provincial plan.

Questions?

If you have any questions about this change, please contact your Group Account Executive or myFlex Sales Manager.Responding to Quebec’s biosimilar policy

Last year, the Quebec government announced it is phasing out coverage of biologic drugs. Beginning April 13, 2022, patients in Quebec using originator biologics will be required to switch to the corresponding biosimilar covered on the province’s public plan in order to maintain coverage.

The following populations are excepted from this new policy:- Pregnant women, who should be transitioned to biosimilars in the 12 months after childbirth.

- Pediatric patients, who should be transitioned to biosimilars in the 12 months after their 18th birthdays.

- Patients who have experienced two or more therapeutic failures while being treated with a biologic drug for the same chronic disease.

We are actively investigating the impact of this new policy on private drug plans in Quebec. We plan to implement further enhancements to our biosimilar programs in Quebec later this year to help prevent this change from resulting in additional costs for our clients’ drug plans. We will provide more details in the coming months.Dental fee guide updates

Each year, Provincial and Territorial Dental Associations publish fee guides. Equitable Life uses these guides to help determine the reimbursement limits for dental procedures. For your reference, below is the list of the average dental fee increases for general practitioners that will be used by Equitable Life for 2022.*

Dental fee guide increases over 2021*

*Data for all provinces and territories was not available at the time of publication. This chart will be updated on EquitableHealth.ca as more information becomes available.Province/Territory Average Fee Increase Alberta 3.9% British Columbia 7.35% Manitoba 5.79% New Brunswick 5.9% Newfoundland and Labrador 5% Nova Scotia 7.05% Northwest Territories 3% Nunavut 3.1% Ontario 4.75% Prince Edward Island 4.75% Quebec 5% Saskatchewan 5.99%

Reminder: Review manual allocations for HCSAs and/or TSAs*

If your client’s Health Care Spending Account (HCSA) and/or Taxable Spending Account (TSA) has manual allocations, they need to allocate these amounts to plan members each year. Please review all your plan members’ profiles on EquitableHealth.ca to ensure they have received their allocation(s) for the current benefit year.

If your clients have Plan Administrator update access on EquitableHealth.ca, they can update these amounts online by doing the following:- Select “View certificate”

- Select “Health Care Spending Account” or “Taxable Spending Account”

- Select “Update Allocation” in Task Center

- Enter amount in “Revised Allocation Amount”

- Override Reason – “Plan Administrator Request”

- Select “Save”

- Select “Reports”

- Select “New”

- Select “Next”

- Select “HCSA” or “TSA Totals by Plan Member”

- Select “Next”

- Enter end date of “12/31/2020”

- Select “Next”

- Select “Finish”

- View “Report”

Mental health resources for plan members*

As the COVID-19 pandemic continues to evolve, many Canadians are experiencing increased levels of stress, anxiety, and depression. Through our partnership with Homewood Health®, all of our clients and their plan members have access to a number of health and wellness resources designed to provide guidance and support. These resources include a number of webinars which discuss various COVID-19 and mental health-related topics. The webinars are pre-recorded so plan members can stream them at their convenience.

Understanding the Impact of COVID-19 on Your Mental Health

English webinar

French webinar

COVID-19: Loneliness & Isolation Fatigue - Self-Care Strategies

English webinar

French webinar

COVID-19: Dealing with Seasonal Affective Disorder

English webinar

French webinar

Reducing Anxiety & Managing the Transition Back to the Classroom - for Teachers

English webinar

French webinar

COVID-19: Specialized Mental Health Support for Health Care Professionals

English webinar

French webinar

COVID-19: Supporting Children’s Mental Health

English webinar

French webinar

Additional resources, including articles, tools, videos and podcasts, are available at Homeweb.ca/Equitable. Please encourage your clients to share these resources with their plan members.

- Policy Change eDelivery