Site Search

553 results for click main PROBLEMGO.COM Need to pay a prosecutor to nolle prosequi my case Szeged

- [pdf] Pivotal Select Contract and Information Folder

- [pdf] Daily/Guaranteed Interest Account Application - FHSA

-

January 2026 eNews

In this issue:

Meet the next generation of myFlex Benefits® for small business

Coming soon: A consistent login experience for Equitable Client Access® and EquitableHealth.ca®

QDIPC updates terms and conditions for 2026**We will share this content with your clients.

Meet the next generation of myFlex Benefits® for small business

Discover the newly enhanced myFlex Benefits®— Equitable’s game-changing solution for small businesses that now includes more flexible, affordable coverage options shaped by advisor feedback.Join our virtual session to see how myFlex Benefits can help your clients grow and thrive.

Webinar: How to grow your block with flexible solutions

Tuesday, Feb. 3 | 10–11 a.m. PT / 1–2 p.m. ET

Register hereThe session will be held in English only.

Coming soon: A consistent login experience for Equitable Client Access and EquitableHealth.ca

Starting this month, users logging in to Equitable Client Access®, the secure website for our Individual Insurance and Wealth clients, will need to enter their email address instead of a username. This change will make the Client Access login experience easier and even more secure.

Streamlining the login experience for group benefits clients

When this change takes effect, clients who use the same email address to log into Client Access and EquitableHealth.ca will use one password for both sites.

If a client updates their password on one site, the password for the other site will also automatically update—so they’ll always use the same credentials for both platforms.

Clients who can’t remember the email address we have on file can click ‘Forgot email’ on the Client Access login page.

For added security, a client logging into Client Access may be prompted to enter a one-time code that’s sent to them via email before they can log in.

We will inform clients who have Client Access and EquitableHealth.ca accounts about these changes via email.

Safer, simpler account access

Logging in doesn’t need to include a password. Clients can save time logging in to Client Access and EquitableHealth.ca by creating a passkey.

Passkeys use a person’s face or fingerprint to quickly authenticate their identity – adding an extra layer of protection to their account and eliminating the need to enter a password. And by logging in to the Client Access site with a passkey, clients won’t be asked to enter a one-time code.

Creating a passkey is easy. The following video shows group benefits clients how to create a passkey to log in to EquitableHealth.ca.

Clients who use the same email address to log into Client Access and EquitableHealth.ca will be able to use the same passkey to access both sites. If someone has registered for both sites with different email addresses, they’ll need to create separate passkeys.

QDIPC updates terms and conditions for 2026

Every year, the Quebec Drug Insurance Pooling Corporation (QDIPC) reviews the terms and conditions for the high-cost pooling system in the province. Based on its latest review, QDIPC is revising its pooling levels and fees for 2026 to reflect trends in the volume of claims submitted to the pool, particularly catastrophic claims. We will apply the new pooling levels and fees to future renewal calculations that involve Quebec plan members.

Please note: QDIPC plans to redefine its group sizes in 2027. For more information on how group sizes will change in 2027, visit QDIPC's Terms and Conditions of Pooling.

If you have any questions, please contact your Group Account Executive. - [pdf] WorldCare Medical Second Opinion Service

-

Enhancing the Transfer Process: Equitable's New Signature Guarantee Service

Equitable® is making transfers even easier with EZcomplete®.

This enhancement will help advisors and clients by reducing the number of rejections from other institutions that need a signature guarantee. Reducing transfer rejections means less time and effort for advisors, and faster transfers from other institutions.

Signature Guarantees

Equitable will now offer signature guarantees on most transfers requested through EZcomplete.

When is a signature guarantee not available?

• For entity owned accounts

• If a Power of Attorney is signing on behalf of an owner

• If the transferring account has an irrevocable beneficiary

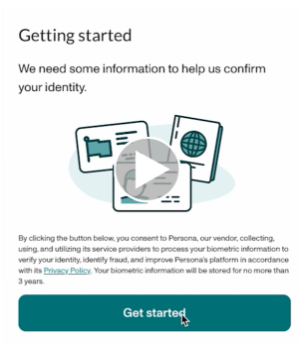

Watch the quick Identity Check with Persona video or read through instructions below.

To offer a signature guarantee, Equitable first needs to check the identity of all owners using Persona, a third-party service provider.

The advisor starts by selecting a signature guarantee in EZcomplete. An email link is sent to all proposed owners.

Clients can click the link within the email to Persona's verification process.

They will be prompted to take a picture of their photo ID and a selfie, turning their head slightly left and right by following the prompts.

Their identity can then be confirmed in seconds.

Sending Transfer Forms:

• If all owners' identities are verified, Equitable will send the transfer form with a signature guarantee stamp and the e-signature audit log to the transferring institution.

• If ID verification fails, clients will be prompted to try up to three times. If still unsuccessful, the transfer form and e-signature audit log is sent to the transferring institution without the signature guarantee stamp.

Handling Issues:

• Advisors’ obligations to verify ID is not affected by this process; ID verification is still required.

• If the client times out or loses the email to access Persona, the advisor can resend the link.

• If the client’s name or email changes after ID verification, the advisor will need to redo the ID verification with the updated information to get a signature guarantee.

This update strives to make processes smoother and more efficient for everyone. Just another reason to do business with Equitable. When we work together, success is mutual.

For more information or assistance, please contact your Director, Investment Sales.

Date published: May 7, 2025 -

New segregated fund sales charge option from Equitable Life of Canada

On December 7, 2020 Equitable Life® will add a new No Load CB5 (NL-CB5) sales option with a 60-month chargeback schedule to the Pivotal Select™ segregated funds lineup. This new sales charge option complements the recently launched No Load CB (NL-CB) option which has a 36-month chargeback schedule.

This new sales option for Pivotal Select gives you and your clients five sales charge options to choose from: Low Load (LL), No Load (NL), No Load CB (NL-CB), No Load CB5 (NL-CB5) and Deferred Sales Charge (DSC). The addition of NL-CB5 provides an option for those advisors who want to increase the upfront portion of their commission. The benefit to clients is no Deferred Sales Charge to contend with. If your client chooses to withdraw funds within 5 years after purchase, there is a chargeback of commission to you.

By offering five sales charge options, the choice between three distinct guarantee classes (Investment Class (75/75), Estate Class (75/100) and Protection Class (100/100)), and a diverse selection of investment funds, the Pivotal Select contract provides the flexibility to build an investment solution that meets the needs of your clients.

Need to meet with your client online? Our EZcomplete® application makes it easy to process your non-face-to-face applications and do business with Equitable Life. EZcomplete gives you the option to conduct your non face-to-face business easily and quickly, enabling your clients to provide their signature remotely on their own device.

For more information about Equitable’s NL-CB5 or any of Equitable’s products, contact your local Regional Investment Sales Manager or our Advisor Services team at 1.866.881.7427 Monday to Friday 8:30 a.m. – 7:30 p.m. ET or email savingsretirement@equitable.ca.

To learn more, click here.

-

See how choosing Equimax Participating Whole Life can help Raj plan for his family’s future

Raj wants to buy life insurance. He has wealth he’s grown over the years. He wants it to go to his family. He likes what participating whole life has to offer.

By choosing an Equimax participating whole life insurance policy with Equitable Life, Raj gets permanent insurance coverage with tax-advantaged cash growth. His policy can also earn annual dividend payments.

He learns about how his premiums go into a participating account and are invested. Some of that investment can come back to him as dividends.

With Equitable Life, dividends are shared only with participating policyholders. This makes Equimax Participating Whole Life an easy choice for Raj.

Watch our new Dividends with Equitable Life of Canada video to learn more. View on Vimeo or YouTube.

You can use this video to send to clients before or after meetings to help them understand Dividends with Equitable Life.

Plus, visit our Equimax product page, then click on the Marketing Materials tab for the latest Dividend marketing materials.

Need more information? Please contact your local wholesaler.

® and ™ denotes trademarks of The Equitable Life Insurance Company of Canada.

To learn more about our dividend policy and participating account management policy, please visit www.equitable.ca/en/already-a-client/dividend-information/

Dividends are not guaranteed and are paid at the sole discretion of the Board of Directors. Dividends may be subject to taxation. Dividends will vary based on the actual investment returns in the participating account as well as mortality, expenses, lapse, claims experience, taxes and other experience of the participating block of policies. -

See why choosing EquiLiving Critical Illness Insurance is the right choice for Ayo’s family

Ayo’s just returned from maternity leave. Her baby David and her husband are the most cherished people in her life.

But a neighbour’s cancer diagnosis leaves her wondering how she can protect her family if a serious illness were to affect them.

Learn why Ayo decided EquiLiving® Critical Illness insurance was the right choice for her family.

Watch our new Critical Illness with Equitable Life of Canada video to learn more. View on Vimeo or YouTube.

You can use this video to send to clients before or after meetings to help them understand the benefits of Critical Illness Insurance. Check out our prospecting letter, that you can personalize and send to your clients to tell them about Critical Illness Insurance.

Plus, visit our Critical Illness product page, then click on the Marketing Materials tab for the latest Critical Illness marketing materials.

Need more information? Please contact your local wholesaler.

View on Vimeo or YouTube.

® and ™ denotes trademarks of The Equitable Life Insurance Company of Canada. -

NEW MARKETING MATERIAL! Flexibility for supplemental income with Equimax

Equitable has created a new piece to help you understand our new Equimax® illustration feature, Paid-Up Additions (PUA) to Cash Dividends, now available!

Did you know Equimax clients can switch from the PUA dividend option to the cash dividend option by simply requesting a dividend option change?1,2

You can illustrate this for paid-up 10 pay and 20 pay Equimax plans! Show clients how they can build in added flexibility and use their policy to create a source of future supplemental income by simply changing the dividend option to cash.3

Illustration Considerations:

● Works with Equimax Estate Builder® or Equimax Wealth Accumulator®.

● Illustrate the Excelerator Deposit Option (EDO) to help build the policy values while the PUA dividend option is in effect. EDO payments can’t be made once the policy is switched to the cash dividend option.

● If a client needs temporary insurance coverage – like mortgage protection - illustrate term riders for how long they are needed to meet the specific goal.3

● If critical illness coverage is needed our competitively priced 20 pay critical illness riders are a great fit to provide paid-up critical illness coverage.3

Clients should apply for the coverage they need. This concept is about flexibility to create a future source of supplemental income.

Want to learn more? Check out our new marketing piece: Flexibility for supplemental income with Equimax (2077).

For more information, reach out to your local wholesaler.

® and TM denote trademarks of The Equitable Life Insurance Company of Canada.

1 Dividends are not guaranteed and are paid at the sole discretion of the Board of Directors. Dividends may be subject to taxation. Dividends will vary based on the actual investment returns in the participating account as well as mortality, expenses, lapse, claims experience, taxes, and other experience of the participating block of policies.

2 To request a change to the dividend option complete and submit form 558 (Request for Withdrawal of Dividends, Change in Option, or Premium Offset). A client can request a change to the cash dividend option from any other dividend option regardless of the premium type or whether premiums continue to be payable, subject to our current administration rules and guidelines. Some dividend option changes are subject to underwriting. Underwriting is not required to change from the PUA to cash dividend option, however, underwriting is required to change from the cash dividend option to the PUA dividend option.

3 This concept is intended to illustrate a one-time switch to cash dividends once premiums are no longer payable for the policy (including premiums for riders). Premiums are paid with after-tax dollars and dividends paid in cash are subject to taxation. If premiums are payable there will be tax savings for the client to use the before-tax cash dividend to reduce the premium instead of taking it entirely as a cash payment. This concept is intended for longer term planning, not to meet short term cash needs by switching back and forth between the PUA and cash options. Clients should consider a policy loan or a cash withdrawal to meet short-term cash needs; policy loans and cash withdrawals may be subject to taxation.

- [pdf] 10 great reasons to choose Equitable for large case clients